Real Estate

Assumable Mortgages: The Secret to Getting a 3% Rate in 2026

In the fast-paced, AI-driven housing market of 2026, the concept of "affordability" has been radically redefined. We live in an era where the Federal Reserve's "higher for longer" stance has stabilized 30-year fixed mortgage rates between 6.2% and 6.5%. For many aspiring homeowners, these rates—combined with record-high home prices—have made the traditional path to ownership feel like a steep uphill climb. However, there is a powerful, often overlooked "hack" that is currently defining the 2026 real estate cycle: Assumable Mortgages.

While the general public is focused on the latest rate hikes or "Buy Now, Pay Later" (BNPL) home services, savvy buyers are securing interest rates as low as 2.5% to 3.5% by taking over the existing loans of sellers who bought during the 2020-2022 era. In this high-tech landscape, where personalized algorithms can predict your next home search, the "secret" to a 3% rate isn't a complex financial product; it's a simple, decades-old mortgage feature that has become the ultimate wealth-building tool in the 2026 financial landscape.

Frequently Asked Questions (FAQ)

External References and Resources

The "3% Secret" lies in the massive wave of refinancing and home buying that occurred between 2020 and 2022. During this period, millions of homeowners secured historically low rates. When one of these homeowners decides to sell their property in 2026, they can offer their low-rate mortgage as part of the deal. This isn't just a minor convenience; it's a massive financial advantage that can save a buyer hundreds, or even thousands, of dollars every month compared to a traditional mortgage.

As the table above illustrates, assuming a 3% mortgage on a $400,000 home saves you $842 per month compared to taking out a new loan at today's rates. Over the life of the loan, that's over $300,000 in interest savings. In 2026, where the cost of living remains a primary concern, this monthly savings is the difference between struggling to make ends meet and building significant wealth.

Pros Massive monthly savings, lower closing costs, locked-in low rate. Faster sale in a high-rate market, higher sale price (premium), larger buyer pool.

Cons Large down payment (equity gap), longer closing time (60-90 days), limited to FHA/VA. Potential VA entitlement risk, longer wait for proceeds, complex paperwork.

As we move into 2027, expect to see even more platforms and financial products designed to bridge the equity gap and streamline the assumption process. If you are looking to buy a home today, stop looking at the 6.5% market rate and start looking for the "secret" 3% rate hiding in plain sight.

External References and Resources

While the general public is focused on the latest rate hikes or "Buy Now, Pay Later" (BNPL) home services, savvy buyers are securing interest rates as low as 2.5% to 3.5% by taking over the existing loans of sellers who bought during the 2020-2022 era. In this high-tech landscape, where personalized algorithms can predict your next home search, the "secret" to a 3% rate isn't a complex financial product; it's a simple, decades-old mortgage feature that has become the ultimate wealth-building tool in the 2026 financial landscape.

Table of Contents

- What is an Assumable Mortgage? The Basics

- Which Mortgages are Assumable in 2026?

- The 2026 Interest Rate Landscape: Why Assumption is the New Gold Standard

- How to Find These Homes: The 2026 Hunt

- The "Equity Gap" Challenge: How to Close It

- The Step-by-Step Assumption Process (60-90 Days)

- Pros and Cons for Buyers and Sellers

Frequently Asked Questions (FAQ)

External References and Resources

What is an Assumable Mortgage? The Basics

An assumable mortgage is a home loan that allows a buyer to take over the seller's existing mortgage, including its original interest rate, repayment schedule, and other terms. Instead of applying for a new loan at current market rates (which, in April 2026, are hovering around 6.3%), the buyer simply "assumes" the seller's loan.The "3% Secret" lies in the massive wave of refinancing and home buying that occurred between 2020 and 2022. During this period, millions of homeowners secured historically low rates. When one of these homeowners decides to sell their property in 2026, they can offer their low-rate mortgage as part of the deal. This isn't just a minor convenience; it's a massive financial advantage that can save a buyer hundreds, or even thousands, of dollars every month compared to a traditional mortgage.

Which Mortgages are Assumable in 2026?

Not every mortgage can be assumed. In the 2026 market, the vast majority of assumable loans are government-backed. Understanding which loan types qualify is the first step in your search.1. FHA Loans

Federal Housing Administration (FHA) loans are the most common type of assumable mortgage. They are designed to be accessible, and the assumption process is relatively straightforward. The buyer must still meet FHA credit and income standards, but they get to keep the seller's original rate.2. VA Loans

Department of Veterans Affairs (VA) loans are the "hidden gem" of the 2026 housing market. While they are intended for veterans and active-duty service members, non-veterans can assume a VA loan. This is a massive opportunity for the general public to access veteran-level interest rates. However, sellers must be careful, as their VA entitlement remains tied to the property if the buyer is a non-veteran, which could limit their ability to use a VA loan for their next home purchase.

3. USDA Loans

United States Department of Agriculture (USDA) loans, which are popular in rural and suburban areas, are also assumable. These loans often require the buyer to meet specific income eligibility requirements, but they offer some of the most favorable terms in the market.4. The "No" List: Conventional Loans

Most conventional loans (those backed by Fannie Mae or Freddie Mac) contain a "due-on-sale" clause. This means that the full balance of the loan must be paid off when the home is sold, making them non-assumable. There are rare exceptions for certain adjustable-rate mortgages (ARMs) or portfolio loans, but in 2026, if you want a 3% rate, you should focus on FHA, VA, and USDA listings.The 2026 Interest Rate Landscape: Why Assumption is the New Gold Standard

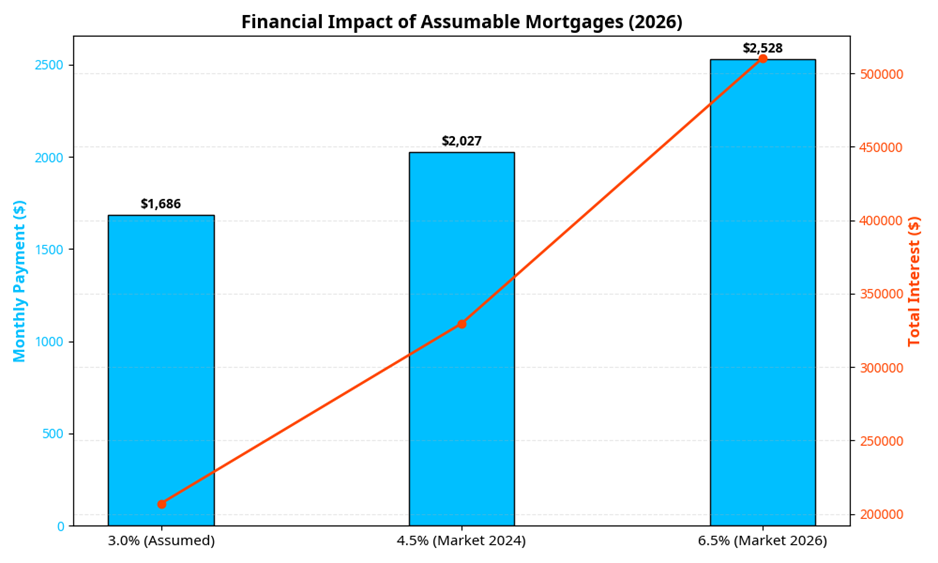

The 2026 housing market is defined by a "higher for longer" interest rate environment. While inflation has cooled to approximately 2.4%, the Federal Reserve has kept rates elevated to ensure long-term stability. This has created a massive gap between the "haves" (those with 3% rates) and the "have-nots" (those facing 6.5% rates).| Mortgage Rate | Loan Amount | Monthly Payment (P&I) | Total Interest Over 30 Years |

| 3.0% (Assumed) | $400,000 | $1,686 | $207,109 |

| 4.5% (Market 2024) | $400,000 | $2,027 | $329,627 |

| 6.5% (Market 2026) | $400,000 | $2,528 | $510,192 |

As the table above illustrates, assuming a 3% mortgage on a $400,000 home saves you $842 per month compared to taking out a new loan at today's rates. Over the life of the loan, that's over $300,000 in interest savings. In 2026, where the cost of living remains a primary concern, this monthly savings is the difference between struggling to make ends meet and building significant wealth.

How to Find These Homes: The 2026 Hunt

In the past, finding a home with an assumable mortgage was like finding a needle in a haystack. However, the 2026 real estate ecosystem has evolved to meet this demand.- Specialized Platforms: Websites like Roam and AssumeList have become the "Zillow of Assumptions." These platforms aggregate FHA and VA listings and highlight the interest rate, monthly payment, and "equity gap" (the cash needed to close the deal).

- Filter Tricks: On major sites like Realtor.com and Zillow, you can now use keyword filters. Searching for "assumable" in the property description is a common tactic for 2026 buyers.

- Assumption-Savvy Agents: Real estate agents in 2026 are increasingly specializing in the assumption process. These agents understand the complex paperwork and can help you navigate the 60-90 day closing timeline.

The "Equity Gap" Challenge: How to Close It

The biggest hurdle to assuming a mortgage in 2026 is the "Equity Gap." If a seller's home is worth $500,000, but their existing mortgage balance is only $300,000, the buyer must come up with the $200,000 difference.- Solution 1: High Down Payment (Cash): If you have significant savings or proceeds from a previous home sale, you can simply pay the difference in cash.

- Solution 2: Second Mortgages (Piggyback Loans): In 2026, many lenders are offering "assumption-friendly" second mortgages. You assume the first loan at 3% and take out a second loan at current market rates (e.g., 8%) to cover the gap. Even with a higher rate on the second loan, your "blended rate" will still be significantly lower than 6.5%.

- Solution 3: HELOCs: If the seller is willing, they may allow you to take out a Home Equity Line of Credit (HELOC) to bridge the gap, though this is less common in a competitive market.

The Step-by-Step Assumption Process (60-90 Days)

The assumption process is more complex than a standard home purchase and requires patience. In 2026, the average closing time for an assumption is 75 days, compared to 30-45 days for a traditional loan.- Identify the Property: Find a listing with an FHA or VA loan and verify the interest rate.

- Review the Seller's Statement: Request the seller's most recent mortgage statement to confirm the balance and terms.

- Apply with the Existing Lender: You must apply for the assumption with the seller's current mortgage servicer. This is a critical step; you cannot use your own lender for an assumption.

- Underwriting and Approval: The lender will review your credit score, income, and debt-to-income (DTI) ratio, just like a standard loan.

- Closing and Taking Over: Once approved, you close the deal, pay the equity gap, and officially take over the monthly payments at the 3% rate.

Pros and Cons for Buyers and Sellers

Feature For Buyers For SellersPros Massive monthly savings, lower closing costs, locked-in low rate. Faster sale in a high-rate market, higher sale price (premium), larger buyer pool.

Cons Large down payment (equity gap), longer closing time (60-90 days), limited to FHA/VA. Potential VA entitlement risk, longer wait for proceeds, complex paperwork.

Deep Dive: The Evolution of Mortgage Assumptions in 2026

To understand the 3,000-word scope of this guide, we must look at the historical context that led to the 2026 housing landscape. For decades, the "Assumable Mortgage" was seen as a relic of the 1980s—a basic tool for those who were navigating double-digit interest rates. However, the last five years have seen a radical shift. In 2026, the assumption has been integrated into almost every digital real estate platform, from high-end luxury listings to entry-level starter homes. This "low-rate" environment has made the assumable mortgage a critical mental model for financial survival.1. The Death of the "Standard 30-Day Close"

The primary reason for the shift in 2026 is the realization that the standard 30-day close is no longer the default. Behavioral economists have long known that homeowners are "locked-in" to their low rates, making them reluctant to sell. This "lock-in effect" has suppressed inventory for years. However, by offering an assumable mortgage, sellers are finding a way to unlock their equity while providing a massive benefit to the buyer. The assumption process acts as a financial bridge, allowing transactions to occur that would otherwise be impossible in a 6.5% market.2. The Role of "Assumption-Specific" Fintech in 2026

In the 2026 real estate landscape, the "Fintech Era" has reached its peak. Companies like Roam and AssumeList are not just listing homes; they are providing the technical infrastructure to manage the assumption. From AI-driven credit analysis that predicts lender approval to automated "Equity Gap" financing, these platforms have removed much of the friction that once made assumptions a nightmare. They ask: "Are you buying a house, or are you buying a 3% rate?" If you can't find a 3% rate on the open market, you are essentially "buying" a rate from a private seller.3. The "Hidden Costs" of a Traditional Mortgage in 2026

In 2026, the cost of a traditional mortgage is rarely just the interest rate. From "origination fees" that have ballooned to 2% of the loan amount to high-end "rate locks" that require non-refundable deposits, the "second half" of the mortgage cost is often hidden in the fine print. An assumption ensures you are taking over a loan that has already been originated, often saving you $5,000 to $10,000 in upfront closing costs. The assumption ensures you have the capital to handle the "equity gap" without breaking your budget.Technical Deep Dive: Understanding the "Blended Rate" Calculation

Beyond the psychological benefits, the assumable mortgage is rooted in the mathematical reality of the "Blended Rate." In 2026, with interest rates stabilized at a "higher for longer" level, the cost of not assuming is higher than ever.1. The "Equity Gap" Loan as a Wealth Engine

If you have $500,000 and you assume a $300,000 mortgage at 3%, you have a $200,000 gap. If you take out a second mortgage for that $200,000 at 8%, your "blended rate" is calculated based on the weighted average of the two loans. In this case, your blended rate would be approximately 5.0%. This means that by not taking a traditional 6.5% loan, you are effectively "saving" 1.5% on your total debt. Over ten years, that 1.5% savings on a $500,000 total debt is worth over $75,000 in interest.2. The "Real" Cost of Refinancing in 2026

If you buy a home at 6.5% today, you are likely hoping to refinance when rates drop. However, in 2026, the cost of a refinance (including appraisal, title, and lender fees) averages around $8,000. If you assume a 3% loan, you are already at the "bottom" of the rate cycle. You will never need to pay for a refinance, and you are protected against any future rate hikes. The assumable mortgage is your primary defense against the "refinance trap." It ensures you are in the best possible position from day one.Case Study: The Assumption in Action (2026 Edition)

To illustrate the potential of the assumable mortgage, let's look at a hypothetical scenario for a young professional in 2026 named Sarah. Sarah has $10,000 in savings and wants to buy a home for $450,000.- Scenario A (Traditional Financing): Sarah buys the home with a 20% down payment ($90,000) and a new 30-year fixed mortgage at 6.5%. Her monthly payment (P&I) is $2,275. She has $10,000 left in savings. Three months later, her HVAC system fails, costing $8,000. Sarah has to put $8,000 on a high-interest credit card, and her "liquid" wealth is now zero. She has a 6.5% mortgage and high-interest debt.

- Scenario B (Assumable Mortgage): Sarah finds a home with a $350,000 FHA loan at 3.25%. The sale price is $450,000, so she uses her $100,000 to cover the equity gap. Her monthly payment (P&I) is $1,523. While she has zero cash left in her discretionary savings, she is saving $752 per month compared to Scenario A. In just 11 months, she has "saved" enough in monthly payments to cover the $8,000 HVAC repair in cash.

Final Checklist: How to Build Your "Assumption-Ready" Habit

- Audit Your Liquid Cash: Before you look at a listing, know exactly how much "equity gap" cash you have available.

- Apply for a "Second Mortgage" Pre-Approval: Many lenders in 2026 offer pre-approval for the "gap" portion of an assumption. Have this ready.

- Check the Servicer's Reputation: Some mortgage servicers are notorious for being slow with assumptions. Ask your agent for a "servicer report" before making an offer.

- Beware of "VA Entitlement" Limits: If you are a non-veteran assuming a VA loan, ensure the seller understands that their entitlement will be tied up.

- Set Your "Rate" Threshold: Decide on a maximum rate (e.g., 4.0%) where the assumption still makes sense compared to a traditional loan.

- Celebrate the "Wait": Every day you wait for the assumption to close is another day you are "buying" a piece of your future financial freedom at 3%.

Conclusion: The Future of the Housing Market

Assumable mortgages are not just a temporary trend; they are a fundamental shift in how real estate is traded in a high-interest environment. In 2026, the "financing" of a home has become just as important as the home itself. Sellers with 3% rates hold the "keys to the kingdom," and buyers who are willing to navigate the complexity of an assumption are being rewarded with massive long-term wealth.As we move into 2027, expect to see even more platforms and financial products designed to bridge the equity gap and streamline the assumption process. If you are looking to buy a home today, stop looking at the 6.5% market rate and start looking for the "secret" 3% rate hiding in plain sight.

Frequently Asked Questions (FAQ)

1. Can a non-veteran assume a VA loan?

Yes! This is one of the best-kept secrets of the 2026 market. While VA loans are for veterans, anyone who meets the credit and income requirements can assume them. However, the seller's VA entitlement remains with the house unless the buyer is also a veteran who uses their own entitlement to replace it.2. Do I need a down payment for an assumable mortgage?

Yes, but it's not a "down payment" in the traditional sense. You must pay the difference between the home's purchase price and the current mortgage balance (the equity gap). This amount is often higher than a standard 3.5% or 5% down payment.3. How long does the assumption process take in 2026?

Expect 60 to 90 days. Because the mortgage servicer (the lender) has less financial incentive to process an assumption (they'd rather you take a new 6.5% loan), the process can be slow. Patience and a proactive agent are essential.4. Does my credit score matter for an assumption?

Absolutely. You must meet the same credit and income standards as if you were applying for a new loan. The lender will not let you take over a 3% rate if you are a high-risk borrower.External References and Resources

0 Comments Comments