Vehicles & Cars

America's Pandemic Car Bubble Is Trapping Buyers in Debt

TABLE OF CONTENTS

- How the Pandemic Created a Car Buying Frenzy

- What Negative Equity Means — and Why It Matters

- The Scale of the Problem in 2026

- How Loan Terms Became a Trap

- The Repossession Wave

- Who Is Being Hit the Hardest

- How to Tell If You Are Underwater

- What You Can Do About It

- Conclusion

- Frequently Asked Questions

- References

How the Pandemic Created a Car Buying Frenzy

In early 2020, car dealerships across America went quiet. Lockdowns, uncertainty, and collapsing consumer confidence put a sudden brake on vehicle sales. What happened next was one of the strangest chapters in American consumer history. Within months, demand roared back with a vengeance, but supply could not keep up. A worldwide semiconductor shortage crippled car production lines from Detroit to Stuttgart. With inventory scarce and demand surging, the laws of economics took over: prices went through the roof.In April 2021, the average new car cost about $41,000, according to the Wall Street Journal. That was already high by historical standards. But prices kept climbing. By March 2026, the average new vehicle sticker price had reached $51,456 — the twelfth straight month the figure had stayed above $50,000, according to Kelley Blue Book data reported by CNBC. That is a 25% increase in five years on what is, for most families, the second biggest purchase of their lives.

At the same time, buyers were flooded with what felt like easy money. Interest rates near zero made borrowing cheap. Stimulus cheques gave millions of Americans extra cash for down payments. Dealers, knowing inventory was limited, charged full sticker price — and often added markups on top. Buyers who had been putting off a purchase finally pulled the trigger, often paying more than they should have, on terms that stretched further than they realised.

That was the bubble inflating. Now it is deflating — and the consequences are falling squarely on ordinary Americans who simply needed a car to get to work.

What Negative Equity Means — and Why It Matters

Negative equity — sometimes called being "underwater" or "upside down" on a loan — happens when you owe more on your car loan than the vehicle is currently worth. For example, if you took out a $45,000 loan to buy a truck in 2022 and that truck is now worth $32,000, you have negative equity of $13,000. The car has lost value faster than you have paid down the loan.This becomes a serious financial problem the moment you want to change vehicles. When you trade in a car with negative equity, the dealer typically rolls that gap — the amount you still owe above the car's value — into your next loan. So instead of starting fresh with a clean $35,000 loan on a new vehicle, you might end up with a $42,000 loan. You are now paying interest on debt you carried over from a previous car, on top of interest on the new one. The monthly payment goes up, the loan term stretches even longer, and you are deeper underwater before you have even left the forecourt.

The trade-in is the trap. Rolling negative equity into a fresh loan is the most expensive move you can make in this market.

— THESTREET, MAY 2026, CITING EDMUNDS ANALYSIS

Consumers who rolled over negative equity from a prior vehicle loan were more than twice as likely to wind up having their car repossessed within two years, compared with those who netted money on a trade-in, according to a 2024 study from the Consumer Financial Protection Bureau. That is not a minor difference in outcome. That is a doubling of the risk of losing your vehicle entirely.

The Scale of the Problem in 2026

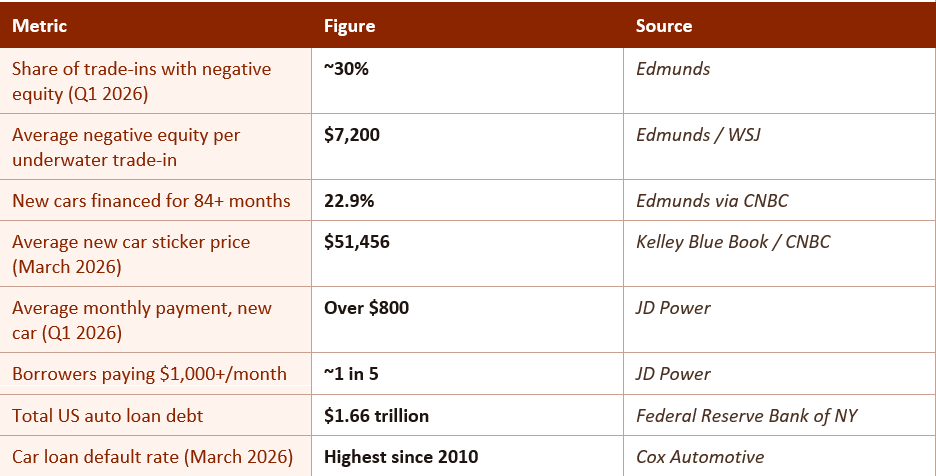

The numbers paint a clear picture of a market under serious stress. About 30% of borrowers in the first quarter of 2026 who traded in a car to buy a new one had negative equity, according to car-shopping website Edmunds. Those borrowers owed about $7,200 on average before getting a new loan — a 42% jump compared with the same period five years earlier.A record 22.9% of new-car purchases in Q1 2026 were financed for at least 84 months, according to CNBC. That means nearly one in four new car buyers is now committed to making monthly payments for seven years or more on a vehicle that will lose roughly half its value in that time. The average new-car loan in Q1 2026 was 70 months — nearly six years. Total US auto loan debt reached $1.66 trillion by the end of 2024, according to the Federal Reserve Bank of New York, making car loans the second-largest category of consumer debt in America after mortgages.

In the first quarter of 2026, the average monthly loan payment on a new car passed $800 for the first time, according to JD Power data. Nearly one in five borrowers is now paying more than $1,000 a month just for their car. For comparison, the US median household monthly income is around $5,000 after tax. That means millions of families are spending 20% or more of their take-home pay on a single car payment — before insurance, fuel, or maintenance.

How Loan Terms Became a Trap

When prices rose sharply and interest rates followed, buyers faced an impossible maths problem: how do you keep a monthly payment in budget when the car costs $10,000 more and interest rates have tripled? The answer the industry provided was simple — stretch the loan over more months. Instead of paying off a $45,000 car in four years, you pay it off in seven. The monthly bill stays manageable. But the total cost of that car balloons.On an 84-month loan at today's average interest rates, a buyer financing a $47,000 vehicle with a typical down payment ends up paying nearly double the interest compared with a 48-month loan — an extra $4,000 to $5,000 in interest charges alone, simply for the privilege of keeping payments affordable month to month. And because car loans are front-loaded with interest, early payments barely chip away at the principal while the car itself continues to lose value. The gap between what you owe and what the car is worth is at its widest in the first two to three years of a long loan — exactly the window in which most people decide they want a different vehicle.

Industry voices are becoming increasingly alarmed about ultra-long loan terms. Automotive retail expert Brian Binstock has described 84-month car loans as a death trap for customers — and bad for dealers too. When a dealership puts a customer into a seven-year loan, that customer is effectively taken out of the market for nearly a decade. They cannot trade in without triggering massive negative equity. They cannot upgrade. They are stuck.

Despite this, a record 22.9% of new-car purchases in Q1 2026 were financed for at least 84 months. Some buyers are even signing 96-month — eight-year — loans. A car financed over eight years will almost certainly be worth a fraction of the remaining loan balance by the time it is paid off, if it even runs that long.

The Repossession Wave

When monthly payments stretch budgets to breaking point and negative equity makes it impossible to sell or trade in a car without losing money, the only remaining exit for struggling borrowers is default. And default rates are climbing sharply.Car loan default rates in March 2026 rose to the highest levels seen since 2010, according to Cox Automotive. For subprime borrowers — those with lower credit scores — the picture is even more alarming. The percentage of subprime auto loan holders who are 60 or more days behind on their payments reached a 32-year record in early 2026, according to data tracked by Fitch Ratings and reported by CarEdge. In February 2026, 60-day delinquency rates on subprime auto loans reached 6.8%, just below the record 6.9% seen in January, according to Fitch's ABS Index.

More delinquencies mean more repossessions. By Q4 2025, more than 2.2 million vehicles had already been repossessed in the US. Industry analysts projected 2025 year-end repossession totals would exceed 3 million — a level not seen since the aftermath of the Great Recession. For context, repossessions had collapsed to historic lows of around 1.1 million in 2021, when stimulus payments and lender forbearance kept borrowers afloat. That leniency is long gone. The bills from the pandemic era are now coming due.

When a car is repossessed, the damage does not stop at losing the vehicle. The borrower typically still owes the difference between what the car sells for at auction and what remains on the loan. This deficiency balance averaged approximately $7,500 in 2025. A repossession also stays on a credit report for seven years, making it harder and more expensive to borrow for a home, another vehicle, or anything else.

Who Is Being Hit the Hardest

The auto debt crisis is not spread evenly across society. While prime borrowers with good credit scores are, by and large, managing their payments, the crisis is concentrated sharply among subprime borrowers — those who were approved for loans at high interest rates during the pandemic buying frenzy and are now stuck in vehicles worth far less than they owe.Younger buyers are particularly exposed. Gen Z auto loan delinquency rates rose to 4.3% in late 2023 and have remained elevated since. Many young adults bought their first car during 2021 or 2022 at peak prices, with long loan terms and high interest rates, often with little or no down payment. They are now trapped: too much debt to trade in, too little savings to pay down the gap.

The crisis also hits harder in communities with lower average incomes, where buyers had less financial cushion and were more likely to accept whatever financing terms a dealer offered. These buyers often had no access to a credit union or bank offering competitive rates and relied entirely on dealer-arranged financing, where margins and interest rates tend to be higher. The result is a feedback loop: the people who could least afford to overpay during the pandemic are now the ones most likely to face repossession and its long-term damage to their financial lives.

How to Tell If You Are Underwater

Finding out whether you have negative equity is straightforward. You need two numbers: what you owe on the loan, and what the car is actually worth right now.Three steps to check your equity position

- Step 1 — Find your loan payoff amount: Check your latest monthly statement, log into your lender's website, or call your lender directly. This is the amount you would need to pay today to own the car outright.

- Step 2 — Find your car's current market value: Use Edmunds.com, Kelley Blue Book (KBB.com), or CarGurus. Enter your car's make, model, year, mileage, and condition to get a realistic trade-in value.

- Step 3 — Calculate the gap: Subtract the market value from the payoff amount. If the result is positive, you have negative equity. For example: payoff $28,000 minus market value $21,000 = $7,000 underwater.

If you discover you are significantly underwater, do not panic — but do think carefully before making any moves. Selling or trading in right now will almost certainly lock in that loss. Continuing to pay down the loan until the equity position improves is often the least costly option, particularly if the car is reliable.

What You Can Do About It

Being trapped in a pandemic-era car loan is a difficult position, but it is not without options. Here is what financial advisers consistently recommend for people in this situation.Practical steps if you are underwater on your car loan

- Keep the car and pay it down: The single best move if your car is reliable is to keep paying — ideally making extra payments on the principal to close the equity gap faster. The longer you hold on without trading in, the better your position gets.

- Avoid rolling debt into a new loan: Resist any dealer offer to simply fold your negative equity into a new loan. You will pay interest on old debt while starting a new depreciation clock.

- Refinance if rates have improved: If your credit score has improved since you took out the original loan, refinancing at a lower interest rate can reduce your monthly payments and help you pay down principal faster.

- Consider a less expensive next vehicle: When you are ready to move on, buying a used car outright or with a short loan term will break the cycle of rolling debt forward.

- Never stretch to 84 months or longer: A seven-year loan might look affordable now, but it almost guarantees you will be underwater again within two years. Keep loan terms to 60 months or less wherever possible.

- Talk to a non-profit credit counsellor: If payments are becoming unmanageable, organisations like the National Foundation for Credit Counselling (NFCC) offer free or low-cost advice before repossession becomes inevitable.

CONCLUSION

America's pandemic car bubble was always going to have a reckoning. Chips were short, demand was high, money was cheap, and dealers charged whatever the market would bear. Millions of Americans bought vehicles at prices that made sense only in a zero-interest, government-stimulus, can't-find-inventory world. That world is gone. What remains are the loans — long, expensive, and attached to vehicles worth a fraction of what was paid for them.The best thing most affected borrowers can do is the least exciting: keep the car, make payments, pay a little extra when possible, and wait for the equity gap to close. The worst thing they can do is trade in early, roll the debt forward, and start the cycle again. Understanding the trap is the first step to avoiding it — or getting out.

0 Comments Comments