Budgeting

Fixed vs Variable Expenses: What Is the Difference?

Table of Contents

- Why This Distinction Is the Foundation of Every Budget

- What Are Fixed Expenses?

- What Are Variable Expenses?

- The Third Category: Semi-Fixed (Hybrid) Expenses

- Fixed, Variable, and Semi-Fixed: The Complete UK & US Expense Reference

- Fixed vs Variable: The Core Differences Side by Side

- Worked Example: A Complete Monthly Budget Breakdown

- How to Reduce Fixed and Variable Expenses: Practical Strategies

- Reducing Fixed Expenses: Bigger Changes, Bigger Savings

- Reducing Variable Expenses: Faster Results, Smaller Amounts

- Conclusion

- Frequently Asked Questions (FAQ)

Why This Distinction Is the Foundation of Every Budget

Before you can manage your money, you have to understand where it goes. And before you can understand where it goes, you need to know which expenses you have meaningful control over and which are largely predetermined by choices you have already made. This is the foundational purpose of distinguishing between fixed and variable expenses — and it is the starting point for every budget, from the simplest household spreadsheet to the most sophisticated corporate financial plan.Fixed expenses are costs that remain the same in amount and frequency regardless of what you do month to month. Your rent or mortgage is the same in January as it is in August. Your car loan payment does not change because you drove less this week. Your car insurance premium does not vary because the weather was good. These costs are predictable, largely contractual, and often the first expenses you prioritise paying because missing them typically carries significant consequences: missed rent risks eviction; a missed loan payment damages your credit score; a lapsed insurance policy leaves you legally exposed.

Variable expenses are costs that change in amount from month to month depending on your usage, choices, and circumstances. You spend more on groceries in a month when you host dinner parties. You spend more on fuel in summer when you drive to holidays. You spend more on heating in winter. You spend more on gifts in December. You spend more — or less — on dining out, entertainment, clothing, and personal care based on decisions you make every week. Variable expenses respond to your choices and your life events in ways that fixed expenses do not.

Understanding this distinction matters because it determines your budgeting strategy for each category, your options for reducing spending when times are tight, and the sequencing in which you allocate monthly income across your financial obligations. This guide explains the complete picture: the definitions and examples of both categories, the important third category of semi-fixed expenses, the core differences in how each type affects budget flexibility and control, the practical budgeting approach for each, the worked example of a complete household budget breakdown, and the specific strategies for reducing both types of expense when needed.

What Are Fixed Expenses?

Fixed expenses are financial obligations that remain approximately the same amount every time you pay them, at a regular and predictable interval. WalletHub's February 2026 guide provides a concise definition: 'A fixed expense is a cost that's typically the same amount each month, like your mortgage or rent payment. Fixed expenses are highly predictable and easy to budget for since you can count on the amount being consistent.'The predictability of fixed expenses is their defining characteristic and their primary budgeting advantage. Because you know exactly how much you owe and when, you can automate payment, include the precise amount in your monthly budget without estimation, and eliminate the mental load of tracking fluctuations. Chase's personal finance guide identifies this structural benefit: 'The consistency of a fixed expense comes with certain expectations. One of the best ways to manage a fixed expense is to schedule an automatic payment to process on a recurring basis. When the size and timing of the payment is predictable, paying it manually every month takes up focus you could be using elsewhere in your budget.'

Fixed expenses also carry an important caveat that many people miss: fixed does not mean permanent or necessarily essential. SoFi's March 2026 analysis makes this distinction: 'Keep in mind that not all fixed expenses are necessities — or big budget line items. For example, an online TV streaming service subscription, which is withdrawn in the same amount every month, is a fixed expense. It's also a want as opposed to a need.' A Netflix subscription is just as fixed as a mortgage payment in its payment structure — but one is a survival necessity and the other is discretionary entertainment. Recognising that some fixed expenses are wants (subscriptions, gym memberships, premium insurance add-ons) creates genuine opportunities to reduce them that many people overlook.

Fixed expenses dominate household budgets: Housing alone — typically the largest fixed expense — can consume 30-50% of take-home pay in UK and US cities in 2026 — Empower research (Federal Reserve SHED 2024, May 2025): fixed expenses are the foundation of any household budget because they are typically contractual and consistent. SoFi (March 2026): 'Fixed expenses tend to make up a large percentage of a monthly budget since housing costs, typically the largest part of a household budget, are generally fixed expenses.' UK average rent £1,327/month (HomeLet 2025). US average mortgage $2,317/month. These single line items alone represent 28-40% of average household gross income

What Are Variable Expenses?

Variable expenses are costs that change in amount from month to month, driven by your usage, choices, lifestyle events, and the time of year. Empower's personal finance guide captures the essential characteristic: 'Variable expenses fluctuate based on usage or lifestyle choices.' Unlike fixed expenses where the amount is predetermined, the amount you spend on variable categories depends on decisions you make — how much you drive, how often you shop, whether you eat out, what medical care you need, how you heat your home.Yahoo Finance's guide articulates the budgeting challenge this creates: 'Variable expenses are financial obligations that tend to move up and down in cost within your budget. Because these expenses fluctuate, they can be more difficult to plan for in advance.' This difficulty is not a reason to ignore variable expenses in the budget — quite the opposite. Because they are harder to predict precisely, they require more active monitoring and a different budgeting technique than fixed expenses. The standard approach recommended by WalletHub (February 2026) is to divide the prior year's total spending in each variable category by 12 to produce a monthly average, and use that average as the budget allocation. This smooths out the inevitable monthly variation and creates a realistic planning figure even for highly irregular spending.

An important distinction within variable expenses is between essential variable costs and discretionary variable costs. Groceries are variable in amount from month to month, but they are essential — you cannot choose to stop buying food. Fuel is variable and essential for those who drive to work. Utilities are variable in amount but essential for heat, light, and water. On the other hand, dining out, entertainment, clothing upgrades, and holidays are variable and discretionary — you can reduce or eliminate them in a month where cash is tight without threatening health, safety, or employment. The essential vs discretionary split within variable expenses determines how much of the variable category can realistically be cut when needed.

The Third Category: Semi-Fixed (Hybrid) Expenses

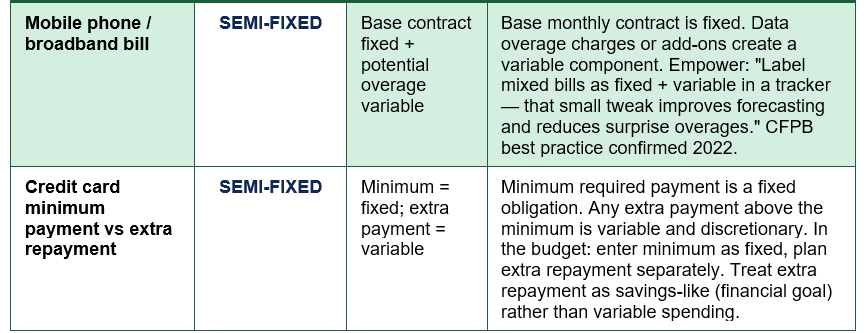

Between the clearly fixed and clearly variable sits a third category that causes significant budgeting confusion: semi-fixed expenses, sometimes called hybrid or mixed expenses. These are bills that have both a fixed component (a guaranteed minimum or base charge) and a variable component (an amount that fluctuates with usage). Understanding that these are hybrid in nature — and treating them correctly in the budget — meaningfully improves budget accuracy.Ramp's definition from their July 2026 analysis is the clearest available: 'Most utilities are variable: your electric, water, and gas bills change based on usage and weather. However, many utility plans include a fixed base charge plus a metered usage component, making them semi-fixed. For budgeting accuracy, split the base charge (fixed) from the usage portion (variable).' Empower's guide from the CFPB provides the most practical pro tip: 'Label mixed bills (like utilities or phone plans) as fixed + variable in a tracker. That small tweak improves forecasting and reduces surprise overages.'

The most common semi-fixed expenses in UK and US household budgets are energy bills (gas and electricity: standing charge fixed, units used variable), mobile phone contracts (monthly contract price fixed, data overage variable), broadband (monthly line rental fixed, excess data charges variable), and credit card repayments (minimum payment is a fixed obligation; any extra payment above the minimum is discretionary and variable). The practical test offered by Ramp: 'If a line item varies by more than 10% month over month, treat it as variable. For semi-variable expenses, separate the fixed base from the variable portion in your budget.'

The subscription audit — the overlooked fixed expense trap: Subscription services — streaming platforms, cloud storage, app subscriptions, gym memberships, magazine subscriptions, software licences, delivery boxes, music services — each appear to be a small, affordable fixed expense individually. But SoFi's March 2026 analysis highlights the cumulative trap: 'Subscription services can seem affordable until they start accumulating and perhaps become unaffordable.' A household carrying 8-10 streaming and digital subscriptions at an average of £8-£12 each is paying £64-£120 per month in fixed discretionary expenses — a meaningful budget line that accumulates invisibly because each individual charge feels trivial. Quarterly subscription audits (reviewing every recurring direct debit and standing order) are one of the highest-value, lowest-effort budget optimisation activities available.

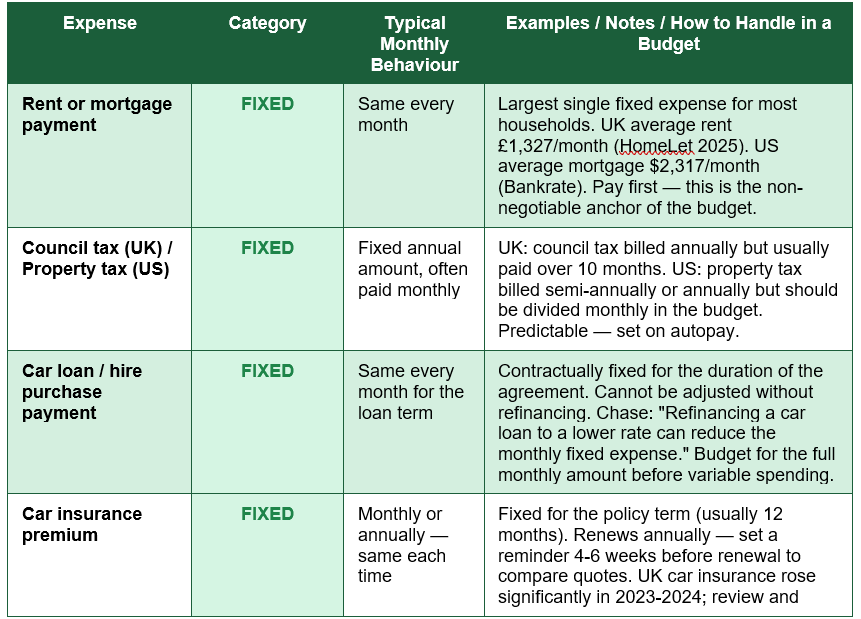

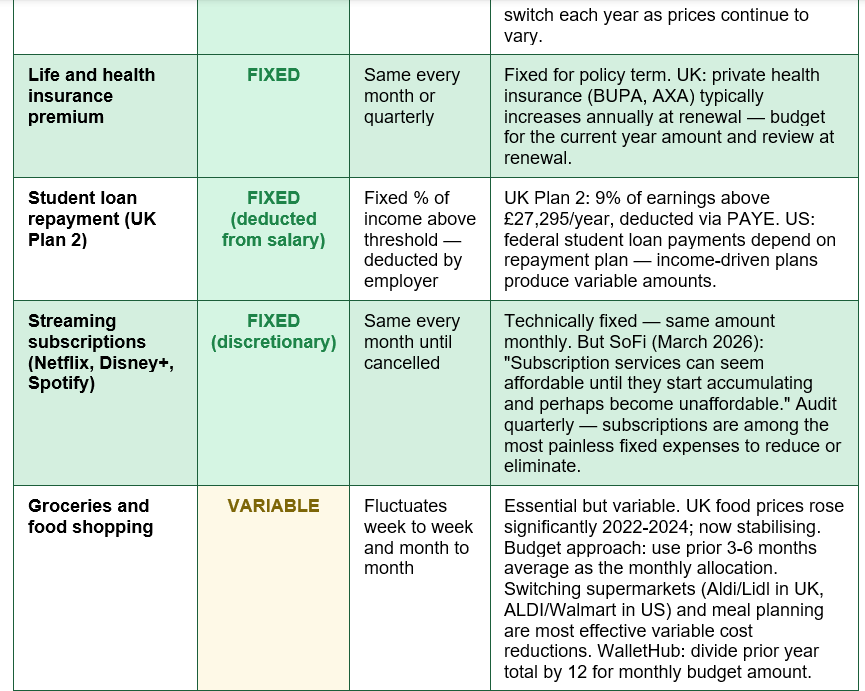

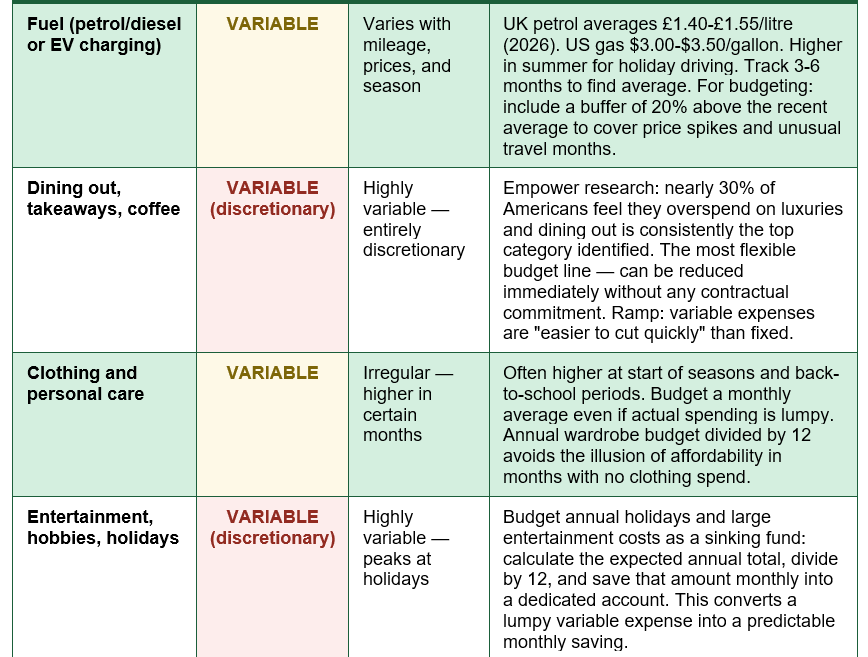

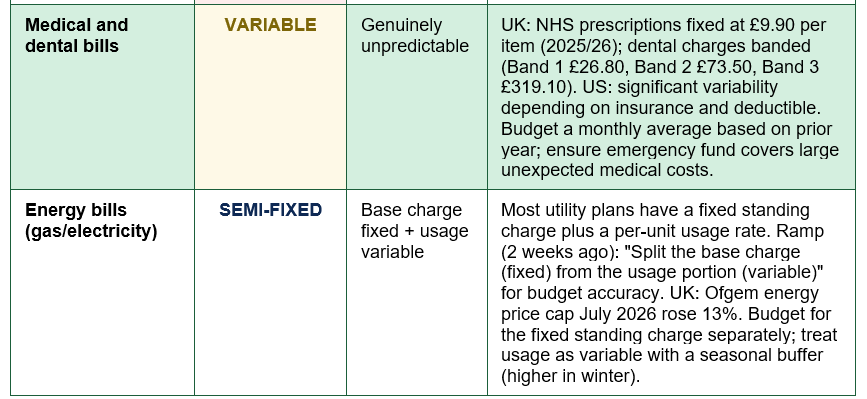

Fixed, Variable, and Semi-Fixed: The Complete UK & US Expense Reference

The table below categorises every major household expense type across all three categories, with budgeting approach notes and UK-specific context for 2026:

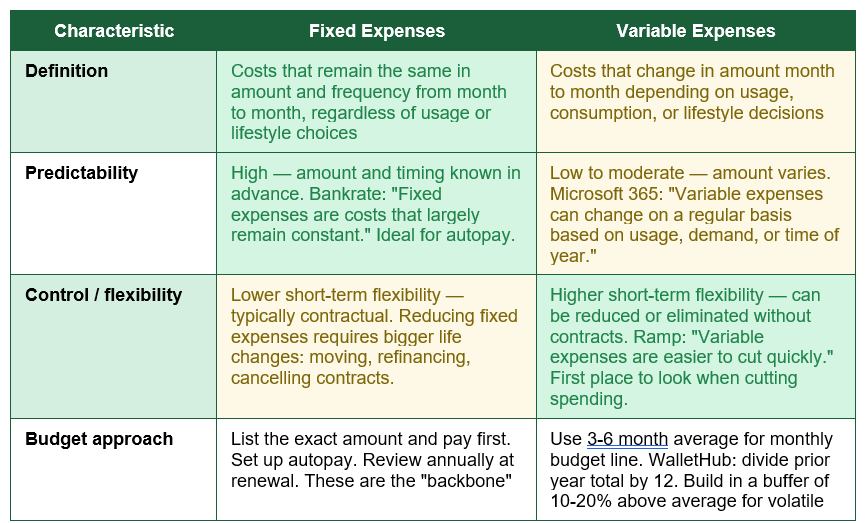

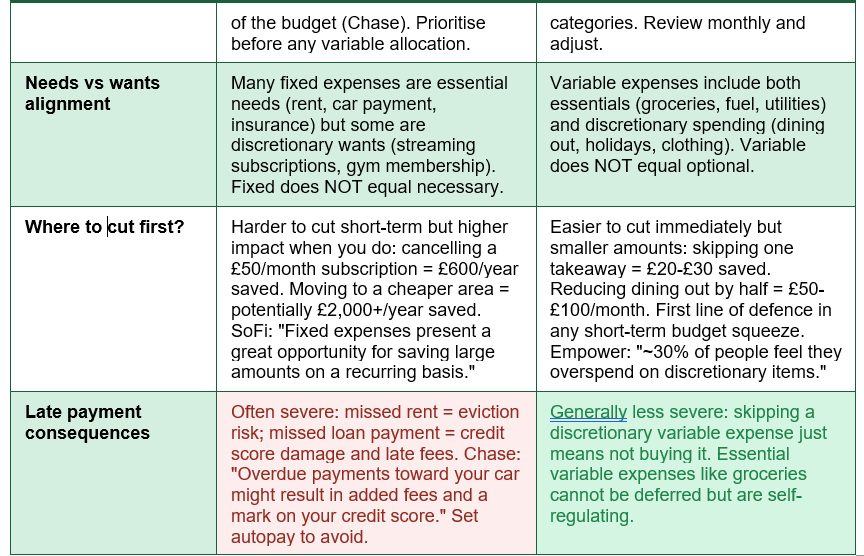

Fixed vs Variable: The Core Differences Side by Side

The table below maps every key dimension of the fixed vs variable distinction — definition, predictability, control, budget approach, needs vs wants alignment, where to cut first, and late payment consequences:

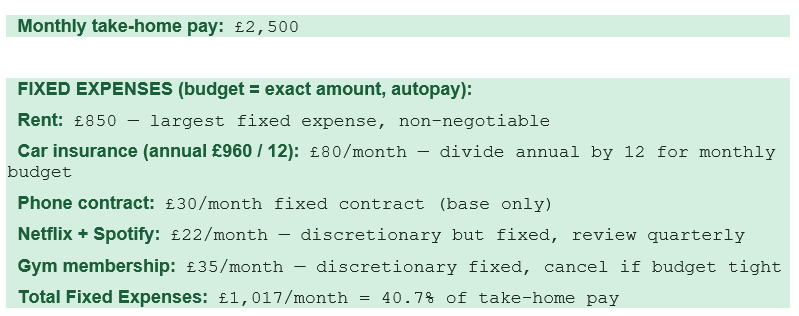

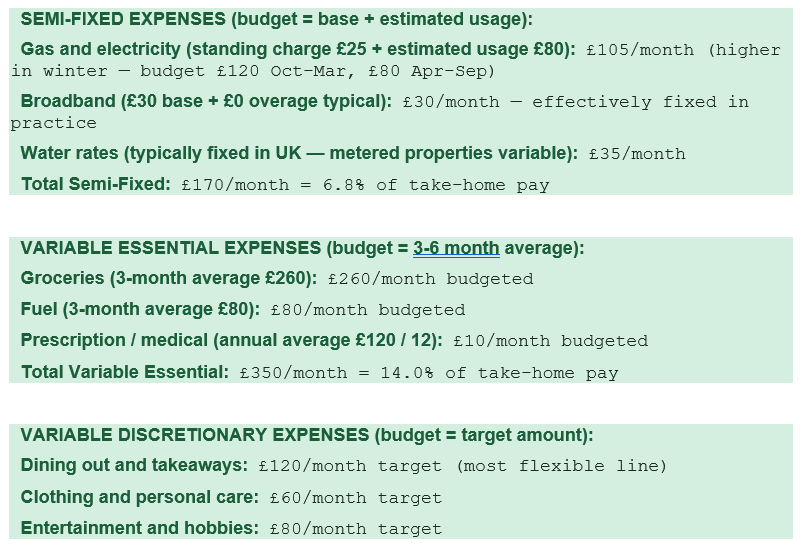

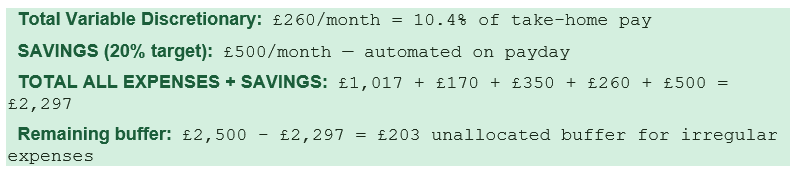

Worked Example: A Complete Monthly Budget Breakdown

The following example maps a UK household budget for a single person earning £2,500 net per month, showing fixed, variable, and semi-fixed expenses with the correct budget treatment for each:

This worked example illustrates the sequencing principle: fixed expenses are listed and committed first (autopay), semi-fixed are estimated with seasonal buffers, variable essentials are budgeted from historical averages, variable discretionary spending uses target amounts based on the remaining income after all other obligations. The 20% savings allocation is automated on payday — it is treated as the first commitment, not the residual.

How to Reduce Fixed and Variable Expenses: Practical Strategies

Reducing Fixed Expenses: Bigger Changes, Bigger Savings

Fixed expenses are harder to reduce in the short term but yield the largest recurring savings when you do manage to cut them. Chase identifies the primary options: 'Refinancing your car. Downsizing your living space. Ending or switching memberships.' The recurring nature of fixed expense savings means every pound saved on a monthly bill is saved every month indefinitely — a £50/month reduction in a subscription or insurance premium is worth £600/year in perpetual savings.- Review and switch insurance annually: Car, home, and life insurance are highly competitive markets — staying with the same provider year after year almost always results in paying more than new customers. UK comparison sites (Confused.com, Compare the Market, MoneySuperMarket) make switching straightforward and typically deliver savings of 10-40% for equivalent cover. Set a calendar reminder 4-6 weeks before each renewal date.

- Refinance loans at lower rates: If interest rates have fallen since you took out a mortgage, car loan, or personal loan, refinancing can reduce the fixed monthly payment and the total interest paid. WalletHub: 'You can refinance loans like your mortgage or student loans to get a lower interest rate and a lower monthly payment.' Check whether any early repayment charge applies before refinancing.

- Conduct a quarterly subscription audit: Review every direct debit, standing order, and recurring card charge. Cancel any subscription you have not used in the past 30 days. Downgrade any subscription to a lower tier if the premium features are not regularly used. Netflix, Disney+, Spotify, cloud storage, and app subscriptions are all candidates for immediate cancellation without any structural impact on daily life.

- Negotiate existing fixed costs: WalletHub specifically recommends: 'Negotiate bills. You may be able to contact companies like your internet provider to see if they are willing to offer you a lower price in exchange for keeping you as a customer.' Broadband, mobile, and TV providers in both the UK and US routinely offer retention discounts to customers who call to cancel or threaten to switch.

Reducing Variable Expenses: Faster Results, Smaller Amounts

Variable expenses are the first line of defence when short-term cash flow is tight — they can be reduced immediately without any contractual commitment or structural life change. The most effective variable expense reductions are those that address the categories where Empower's research identifies the biggest overspend tendency: dining out and discretionary entertainment.- Meal planning and cooking at home: Replacing restaurant and takeaway meals with home cooking is the single highest-impact variable expense reduction for most households. The difference between a £15 takeaway and a £3 home-cooked equivalent of the same meal is £12 per occurrence — at two takeaways per week, meal planning saves approximately £100 per month with no loss of nutrition.

- Grocery shopping strategies: Switching from a premium supermarket (Waitrose, Marks & Spencer) to a mid-range (Tesco, Sainsbury's) or budget alternative (Aldi, Lidl) can reduce grocery bills by 20-40% for comparable food quality. Using own-brand products, buying in bulk for non-perishables, and meal planning to eliminate food waste further reduce this essential variable cost.

- Fuel and transport variable costs: Trip-batching (combining multiple errands in one journey), carpooling, or switching to public transport for regular commutes reduces fuel consumption directly. For EV users, off-peak charging (typically overnight on Economy 7 tariffs in the UK) can halve energy costs per mile compared to daytime charging.

- Use the 30-day rule for discretionary purchases: For any non-essential variable purchase above £50 (or $50), wait 30 days before buying. Research consistently shows that a significant proportion of impulse purchases are not made after the waiting period — the desire fades. This single technique reduces discretionary variable spending without requiring any ongoing tracking.

THE 10% VARIATION TEST: Ramp's July 2026 guide offers the most practical diagnostic for categorising any expense you are unsure about: "If a line item varies by more than 10% month over month, treat it as variable." Apply this to every line in your budget. If your electricity bill varies between £80 and £145 over a year (a range of 81%), it is variable for budgeting purposes — budget the 12-month average plus a seasonal buffer. If your phone contract is exactly £30 every month without exception, it is fixed — enter the exact amount and set autopay. This test removes the ambiguity from every grey-area expense and ensures your budget accurately reflects how each cost actually behaves.

Conclusion

The distinction between fixed and variable expenses is the most fundamental building block of any effective personal budget. Fixed expenses — the same amount at the same time each month, typically contractual — form the backbone of the budget: they are listed first, paid first, and ideally automated to remove any risk of missed payment. Variable expenses — those that change with usage, season, and lifestyle choices — require a different approach: averaging past spending, building seasonal buffers, and actively monitoring month to month to stay within target.The third category — semi-fixed or hybrid expenses — adds important nuance. Energy bills, mobile contracts, and broadband plans all contain both a fixed base component and a variable usage component. Empower's tip from the CFPB guidance is the most actionable: label mixed bills as 'fixed + variable' in your budget tracker, separating the predictable base from the usage-driven portion. This single step improves budget accuracy and eliminates the surprise overages that cause budgets to fail in the months they are most needed.

The right strategy for reducing expenses depends entirely on which category they fall into. Variable discretionary expenses — dining out, entertainment, clothing, subscriptions used occasionally — can be reduced immediately, without any structural change, and are always the first place to look when cash flow is tight. Fixed expenses are harder to reduce but yield the largest and most durable savings when addressed: switching insurance providers, refinancing loans, downsizing subscriptions, and negotiating existing bills can each produce annual savings that compound indefinitely. The worked example in this guide shows a £2,500/month household running comfortably within budget with 20% directed to savings — not by earning more, but by understanding precisely which costs are fixed, which are variable, and which can be reduced without sacrificing anything essential.

0 Comments Comments