Finance

Gender & Generational Gaps in UK Financial Optimism

Six in ten UK adults feel positive about their finances for 2026. But that headline figure conceals a 10-percentage-point gender gap, a generation that is markedly left behind, and a set of financial priorities driven by survival rather than prosperity. Aegon's annual Financial Priorities survey — one of the most comprehensive measures of UK financial sentiment — provides the data. This guide unpacks every finding and explains what it means.

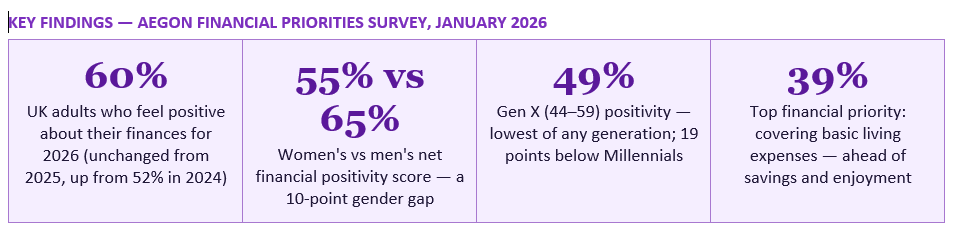

Every January, Aegon publishes its annual Financial Priorities survey — one of the most widely cited measures of UK financial sentiment. The 2026 edition, published in January 2026, found that 60% of UK adults feel positive about their finances for the year ahead. Broken down further: 11% feel 'extremely positive' and 49% 'somewhat positive', compared with 36% who feel negative overall.

On its face, the 60% figure is encouraging. It matches last year's result — which was itself an improvement on the 52% positivity recorded in early 2024, representing a significant recovery from the depths of the cost of living crisis. The fact that the rate held firm into 2026 despite renewed inflationary pressures from energy prices and ongoing cost of living concerns suggests a degree of genuine resilience in UK household financial sentiment.

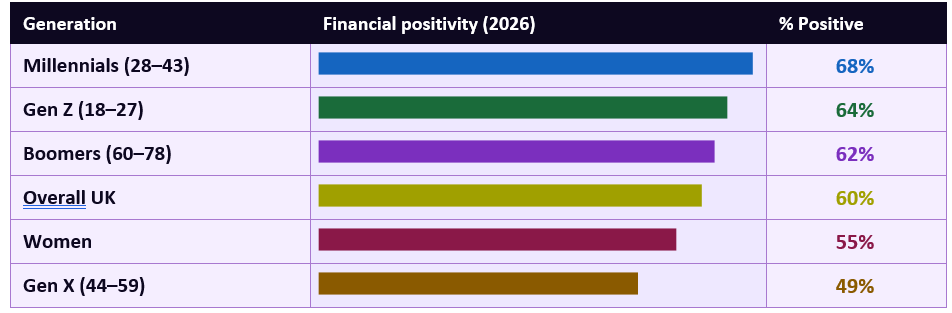

But headline figures are designed to be reassuring, and this one is no different. The 60% overall figure is the product of averaging across groups with very different experiences of financial confidence. It includes the 68% of Millennials who feel positive and the 64% of Gen Z who feel positive — groups whose relative optimism pulls the average up — while obscuring the 49% of Gen X who feel positive and the 55% of women who feel positive. These gaps are not statistical noise. They are meaningful, structural, and in some cases widening.

The picture isn't uniform. Women remain less positive than men, and Gen X stands out as the least upbeat generation when it comes to their finances for 2026. Covering basic living costs continues to dominate priorities — with building emergency savings and enjoying life second and third in the priority list.

— KATE SMITH, HEAD OF PENSIONS, AEGON UK (JANUARY 2026)

Source: Aegon Financial Priorities Survey, January 2026.

The Millennial generation (aged 28 to 43 in 2026) is the most financially optimistic at 68% — a finding that may surprise those who assume younger generations are universally more pessimistic. Gen Z (64%) is second. At the other end of the spectrum, Gen X (49%) is the only generation below the overall average and the only age group that fails to clear the majority threshold for financial positivity. Boomers (62%) sit modestly above the overall average.

The J.P. Morgan Personal Investing survey of 1,000 UK retail investors, published in February 2026, provides a consistent picture from the investment angle: younger investors are more bullish than older ones, with Gen Z investors the most confident about securing positive returns in 2026, followed by Millennials. Gen X investors, while largely optimistic about markets, show lower confidence levels than younger cohorts — and this broadly maps to the Aegon financial sentiment data.

The explanation lies in what researchers sometimes call the 'sandwich generation' dynamic. Gen X is disproportionately likely to be supporting ageing parents while simultaneously funding children through higher education or supporting adult children who cannot afford independent living in the current housing market. Both of these responsibilities impose significant and often unexpected financial demands. The cost of care for an ageing parent — whether direct care support or residential care costs averaging £800 to £1,200 per week — can devastate even comfortable savings. The decision to continue supporting adult children who cannot access the housing market or whose graduate salaries do not stretch to London rents creates a persistent drain on family finances.

Gen X is also the generation most likely to have a mortgage that has recently transitioned from a low fixed rate to the current higher rate environment. Homeowners in their late 40s who took out a 25-year mortgage in their early 20s would have been remortgaging in 2022 to 2025, precisely when rates were rising most sharply. The House of Commons Library's analysis of the cost of living crisis confirms that variable-rate mortgage holders and those remortgaging from fixed rates were among the hardest hit by rate rises — and this group is disproportionately Gen X.

Additionally, Gen X faces a specific pension anxiety. Unlike Baby Boomers, most of whom benefited from defined-benefit final salary pension schemes through working life, Gen X workers have primarily accumulated defined-contribution pensions, which are smaller, less predictable, and more exposed to market volatility. Yet unlike Millennials and Gen Z, Gen X does not have 30 or 40 years of additional saving ahead of them. They are close enough to retirement to see the destination clearly — and many do not like what they see. The Aegon data, which shows pension saving as a top three priority for only 12% of respondents overall, likely reflects an even sharper concern among Gen X specifically.

The UK FinWell Index, produced by Stream and behavioural scientists at CogCo, found in its 2025 report that the gender gap in financial wellbeing widened from 5.2 points in 2024 to 6.7 points in 2025 — a 29% increase in inequality in a single year. The Money and Pensions Service's Adult Financial Wellbeing Survey found that 'women are faring less well than men on almost all key financial wellbeing measures', with the largest gaps relating to pensions and retirement planning.

The structural drivers of the gender gap in financial optimism are multiple and interconnected. The gender pay gap — median full-time earnings for women in the UK remain approximately 7 to 8% below men's according to ONS data — directly reduces women's ability to build financial buffers, save, and invest. Career breaks for childcare, which remain disproportionately taken by women in UK households, create gaps in pension accumulation and compound the pay gap further. Women are also more likely to work part-time, which reduces not only current income but pension auto-enrolment contributions. According to the Money and Pensions Service analysis, women's pension pots are significantly smaller than men's at every age group, meaning their financial insecurity is more acute in retirement — the life stage when financial optimism is most dependent on pension adequacy.

There is also evidence of a confidence gap that compounds the structural one. Women are measurably less likely than men to describe themselves as financially confident, to engage with investment products, or to negotiate salary increases — behavioural patterns that reduce the financial outcomes available to them over time. The ONS Public Opinions and Lifestyle Survey for January to February 2026 provides an interesting counterpoint: it found that women were more likely than men to report high levels of hope for the future (73% vs 65%) — suggesting that the financial optimism gap is specific to financial matters rather than a generalised difference in outlook.

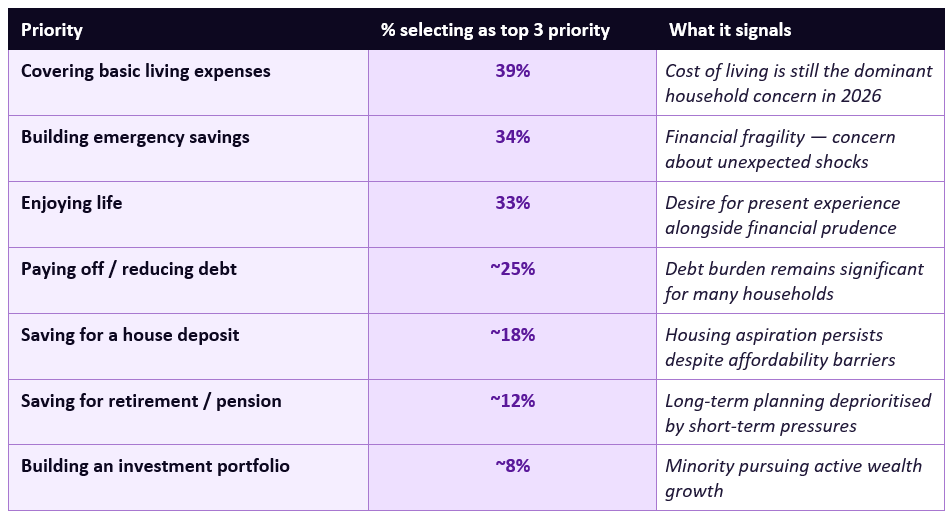

The top three priorities reveal a household financial landscape still dominated by immediate and near-term concerns rather than long-term wealth building. The dominance of 'covering basic living expenses' at 39% — after five years of cost of living crisis — is a reminder that for a substantial minority of UK households, the crisis is not over. It has simply become normalised.

The placement of 'enjoying life' as the third priority at 33% is not frivolous — it reflects a deliberate balance between financial prudence and quality of life. The Confused.com research published in January 2026, covering 3 in 5 UK adults who put financial security at the top of their 2026 goals, found that travel and experiences remain highly prioritised even among financially cautious households. People are not simply economising — they are making deliberate trade-offs between security and experience.

Pension under-saving is a structural problem that has been building for decades in the UK. Auto-enrolment, introduced in 2012, dramatically increased the proportion of workers saving anything into a pension — but the minimum contribution rates (currently 8% of qualifying earnings combined employer and employee) are widely agreed by pension experts to be insufficient to generate an adequate retirement income for most workers. The Pensions and Lifetime Savings Association estimates that a 'moderate' retirement standard of living in the UK requires a pension pot of approximately £490,000 for a single person. Few defined-contribution savers who have contributed only at minimum auto-enrolment rates throughout their career will approach this figure.

The problem is compounded by the generational dynamics already discussed. Gen X — the generation with the most urgent pension need and the least time to course-correct — is also the least financially optimistic, suggesting that many in this group are aware of the problem but feel unable to address it given current financial pressures. The short-term priority of covering living costs inevitably displaces the longer-term priority of pension saving, even when individuals understand the trade-off they are making. As Kate Smith from Aegon noted in the survey commentary: 'for many people, pension saving will need to be given greater priority in future if they are to build up an adequate income for retirement.'

Homeownership with significant equity correlates strongly with financial confidence, particularly for older households where the mortgage may be small or paid off. The asymmetry between homeowners with locked-in low rates (who are insulated from housing cost inflation) and renters or recent remortgagors (who face market-rate increases) is a significant structural driver of the financial confidence gap. Boomers, many of whom own their homes outright or have small mortgages relative to current valuations, show above-average positivity at 62% — consistent with this dynamic.

Which?'s Consumer Insight Tracker for March 2026 found that 49% of households had made at least one adjustment to cover essential spending in the previous month — cutting back on essentials, dipping into savings, selling possessions, or borrowing. Consumer confidence in the future UK economy fell to -55 in March, its lowest level since late 2022. These broader economic anxieties are the backdrop against which individual financial optimism is formed, and they help explain why the 40% who feel negative about their finances in the Aegon data do so despite the headline positivity remaining at 60%.

The pension system is perhaps the clearest structural contributor to the gender gap. Women's pension pots are smaller at every age group. Career breaks for childcare create multi-year gaps in pension accumulation. Part-time work (more common among women) reduces auto-enrolment contributions. The state pension triple lock protects the basic income floor for retirees, but it cannot compensate for a lifetime of lower pension savings driven by structural labour market inequality. Women in their 50s and 60s — many of them Gen X — face a combination of lower financial optimism and real pension underfunding that represents a genuine future financial security risk.

The housing market is the clearest structural contributor to generational differences in financial outlook. Baby Boomers who bought property in the 1980s and 1990s — when prices relative to income were far more accessible — have accumulated substantial housing wealth that acts as a financial security buffer. Gen Z and Millennials face the highest price-to-income ratios in history, making homeownership either inaccessible or highly leveraged. Gen X is caught between: many own homes but face the highest mortgage payment increases from rate rises, and their adult children's inability to afford independent housing creates financial obligations that limit their own savings capacity.

The ONS Public Opinions and Lifestyle Survey (January to February 2026) found that overall, 69% of UK adults report high levels of hope for the future — significantly higher than the 60% who feel financially positive, suggesting that many people whose financial outlook is cautious or negative retain broader life optimism. Interestingly, the ONS data shows women are more likely than men to report high levels of hope (73% vs 65%) — the reverse of the financial optimism pattern. This divergence suggests the gender gap in financial confidence is specifically financial in nature, not a generalised pessimism among women, and is therefore more likely to be addressable through structural changes (equal pay, better childcare provision, pension reform) than through attitudinal interventions.

The FinWell Index 2025 data provides further context: while overall financial wellbeing has declined slightly, the 25 to 34 age group (younger Millennials) bucked the trend with a 4.7-point improvement in wellbeing scores. This aligns with the Aegon finding that Millennials are the most financially optimistic generation and suggests a genuine underlying improvement in the financial position of younger-middle-aged adults — possibly reflecting the beginning of peak earning years combined with pandemic-era savings habits.

But the gaps embedded in that average are a more important story than the average itself. A 10-percentage-point gender gap that has been widening for years, driven by structural inequalities in pay, pension accumulation, and caregiving responsibilities, is not a statistical curiosity — it is a policy failure in plain sight. Gen X's position as the least optimistic generation, sandwiched between care responsibilities and an inadequate pension, is a warning of a retirement crisis that is decades in the making and still not fully visible in the aggregate data. And the dominance of 'covering basic living costs' as the top financial priority — ahead of savings, investment, and long-term planning — after five years of cost of living crisis tells us that the financial recovery is incomplete for a very large number of UK households.

Understanding which group you are in, what structural forces are shaping your financial confidence, and what practical steps are most likely to improve your situation is the starting point for turning financial anxiety into financial action.

IFA Magazine — Majority Upbeat on Finances for 2026 But Gender and Generation Gaps Persist https://ifamagazine.com/majority-upbeat-on-finances-for-2026-but-gender-and-generation-gaps-persist/

ONS — Public Opinions and Social Trends: January 2026 (household finances, wellbeing) https://www.ons.gov.uk/peoplepopulationandcommunity/wellbeing/bulletins/publicopinionsandsocialtrendsgreatbritain/january2026

Stream — UK FinWell Index 2025: State of Financial Wellbeing https://stream.co/en/reports/the-state-of-financial-wellbeing-2025

Money and Pensions Service — Gender, Mental Health and Ethnicity in UK Financial Wellbeing https://moneyandpensionsservice.org.uk/2023/01/10/cross-cutting-themes-adult-financial-wellbeing-survey/amp

J.P. Morgan Personal Investing — Younger Investors Are More Bullish Than Older Generations for 2026 https://www.personalinvesting.jpmorgan.com/insights/younger-investors-are-more-bullish

Confused.com — 3 in 5 Brits Put Financial Security at Top of 2026 Goals (January 2026) https://www.confused.com/press/releases/2026/3-in-5-brits-put-financial-security-at-the-top-of-their-2026-goals

Which? — Financial Wellbeing in March 2026 (Consumer Insight Tracker) https://www.which.co.uk/policy-and-insight/article/financial-wellbeing-in-march-2026-aSMyI5I1b1hr

MoneyHelper — Free Financial Guidance (pensions, budgeting, debt) https://www.moneyhelper.org.uk

GOV.UK — Check Your State Pension https://www.gov.uk/check-state-pension

TABLE OF CONTENTS

- The Headline: 60% Financial Positivity — What It Really Means

- Financial Optimism by Generation: The Full Picture

- The Gen X Paradox: Sandwiched, Squeezed and Left Behind

- The Gender Gap: Why Women Are Less Financially Positive

- The Top Financial Priorities for 2026

- The Pension Saving Gap: A Silent Crisis in the Data

- What Drives Financial Optimism — and What Erodes It

- The Structural Forces Behind the Gaps

- How the Gaps Compare to Wider Wellbeing Data

- What These Findings Mean for Different Groups

- How to Improve Your Own Financial Optimism in 2026

- Conclusion

- Frequently Asked Questions

- References

The Headline: 60% Financial Positivity — What It Really Means

Every January, Aegon publishes its annual Financial Priorities survey — one of the most widely cited measures of UK financial sentiment. The 2026 edition, published in January 2026, found that 60% of UK adults feel positive about their finances for the year ahead. Broken down further: 11% feel 'extremely positive' and 49% 'somewhat positive', compared with 36% who feel negative overall.On its face, the 60% figure is encouraging. It matches last year's result — which was itself an improvement on the 52% positivity recorded in early 2024, representing a significant recovery from the depths of the cost of living crisis. The fact that the rate held firm into 2026 despite renewed inflationary pressures from energy prices and ongoing cost of living concerns suggests a degree of genuine resilience in UK household financial sentiment.

But headline figures are designed to be reassuring, and this one is no different. The 60% overall figure is the product of averaging across groups with very different experiences of financial confidence. It includes the 68% of Millennials who feel positive and the 64% of Gen Z who feel positive — groups whose relative optimism pulls the average up — while obscuring the 49% of Gen X who feel positive and the 55% of women who feel positive. These gaps are not statistical noise. They are meaningful, structural, and in some cases widening.

The picture isn't uniform. Women remain less positive than men, and Gen X stands out as the least upbeat generation when it comes to their finances for 2026. Covering basic living costs continues to dominate priorities — with building emergency savings and enjoying life second and third in the priority list.

— KATE SMITH, HEAD OF PENSIONS, AEGON UK (JANUARY 2026)

Financial Optimism by Generation: The Full Picture

The generational breakdown of financial optimism in Aegon's 2026 data is perhaps its most striking finding, and it defies some common assumptions about which age groups feel most confident about money.Source: Aegon Financial Priorities Survey, January 2026.

The Millennial generation (aged 28 to 43 in 2026) is the most financially optimistic at 68% — a finding that may surprise those who assume younger generations are universally more pessimistic. Gen Z (64%) is second. At the other end of the spectrum, Gen X (49%) is the only generation below the overall average and the only age group that fails to clear the majority threshold for financial positivity. Boomers (62%) sit modestly above the overall average.

The J.P. Morgan Personal Investing survey of 1,000 UK retail investors, published in February 2026, provides a consistent picture from the investment angle: younger investors are more bullish than older ones, with Gen Z investors the most confident about securing positive returns in 2026, followed by Millennials. Gen X investors, while largely optimistic about markets, show lower confidence levels than younger cohorts — and this broadly maps to the Aegon financial sentiment data.

The Gen X Paradox: Sandwiched, Squeezed and Left Behind

The finding that Gen X — born between approximately 1965 and 1980, aged 44 to 59 in 2026 — is the least financially optimistic generation deserves extended examination. It is, on first inspection, surprising. Gen X workers are typically at or approaching peak earning years. Many are homeowners with significant equity accumulated before the post-2008 house price explosion. They are not the generation dealing with entry-level wages or sky-high rents as first-time renters. Yet only 49% feel positive about their finances — 19 points below Millennials and 15 points below Gen Z.The explanation lies in what researchers sometimes call the 'sandwich generation' dynamic. Gen X is disproportionately likely to be supporting ageing parents while simultaneously funding children through higher education or supporting adult children who cannot afford independent living in the current housing market. Both of these responsibilities impose significant and often unexpected financial demands. The cost of care for an ageing parent — whether direct care support or residential care costs averaging £800 to £1,200 per week — can devastate even comfortable savings. The decision to continue supporting adult children who cannot access the housing market or whose graduate salaries do not stretch to London rents creates a persistent drain on family finances.

Gen X is also the generation most likely to have a mortgage that has recently transitioned from a low fixed rate to the current higher rate environment. Homeowners in their late 40s who took out a 25-year mortgage in their early 20s would have been remortgaging in 2022 to 2025, precisely when rates were rising most sharply. The House of Commons Library's analysis of the cost of living crisis confirms that variable-rate mortgage holders and those remortgaging from fixed rates were among the hardest hit by rate rises — and this group is disproportionately Gen X.

Additionally, Gen X faces a specific pension anxiety. Unlike Baby Boomers, most of whom benefited from defined-benefit final salary pension schemes through working life, Gen X workers have primarily accumulated defined-contribution pensions, which are smaller, less predictable, and more exposed to market volatility. Yet unlike Millennials and Gen Z, Gen X does not have 30 or 40 years of additional saving ahead of them. They are close enough to retirement to see the destination clearly — and many do not like what they see. The Aegon data, which shows pension saving as a top three priority for only 12% of respondents overall, likely reflects an even sharper concern among Gen X specifically.

The Gender Gap: Why Women Are Less Financially Positive

The 10-percentage-point gap between women's financial positivity (55%) and men's (65%) is one of the most consistent and most concerning findings in UK financial wellbeing research. It is not unique to the Aegon 2026 data — it appears across multiple datasets and has been widening in recent years.The UK FinWell Index, produced by Stream and behavioural scientists at CogCo, found in its 2025 report that the gender gap in financial wellbeing widened from 5.2 points in 2024 to 6.7 points in 2025 — a 29% increase in inequality in a single year. The Money and Pensions Service's Adult Financial Wellbeing Survey found that 'women are faring less well than men on almost all key financial wellbeing measures', with the largest gaps relating to pensions and retirement planning.

The structural drivers of the gender gap in financial optimism are multiple and interconnected. The gender pay gap — median full-time earnings for women in the UK remain approximately 7 to 8% below men's according to ONS data — directly reduces women's ability to build financial buffers, save, and invest. Career breaks for childcare, which remain disproportionately taken by women in UK households, create gaps in pension accumulation and compound the pay gap further. Women are also more likely to work part-time, which reduces not only current income but pension auto-enrolment contributions. According to the Money and Pensions Service analysis, women's pension pots are significantly smaller than men's at every age group, meaning their financial insecurity is more acute in retirement — the life stage when financial optimism is most dependent on pension adequacy.

There is also evidence of a confidence gap that compounds the structural one. Women are measurably less likely than men to describe themselves as financially confident, to engage with investment products, or to negotiate salary increases — behavioural patterns that reduce the financial outcomes available to them over time. The ONS Public Opinions and Lifestyle Survey for January to February 2026 provides an interesting counterpoint: it found that women were more likely than men to report high levels of hope for the future (73% vs 65%) — suggesting that the financial optimism gap is specific to financial matters rather than a generalised difference in outlook.

The Top Financial Priorities for 2026

Aegon's survey asked respondents to pick their top financial priorities from a long list. The results paint a revealing picture of what UK households are managing for in 2026 — and the balance between short-term survival and longer-term wealth building.The top three priorities reveal a household financial landscape still dominated by immediate and near-term concerns rather than long-term wealth building. The dominance of 'covering basic living expenses' at 39% — after five years of cost of living crisis — is a reminder that for a substantial minority of UK households, the crisis is not over. It has simply become normalised.

The placement of 'enjoying life' as the third priority at 33% is not frivolous — it reflects a deliberate balance between financial prudence and quality of life. The Confused.com research published in January 2026, covering 3 in 5 UK adults who put financial security at the top of their 2026 goals, found that travel and experiences remain highly prioritised even among financially cautious households. People are not simply economising — they are making deliberate trade-offs between security and experience.

The Pension Saving Gap: A Silent Crisis in the Data

The finding that pension saving ranks as a top three priority for only 12% of UK adults in 2026 is one of the most concerning in the entire dataset — and deserves more attention than it typically receives in coverage of the survey.Pension under-saving is a structural problem that has been building for decades in the UK. Auto-enrolment, introduced in 2012, dramatically increased the proportion of workers saving anything into a pension — but the minimum contribution rates (currently 8% of qualifying earnings combined employer and employee) are widely agreed by pension experts to be insufficient to generate an adequate retirement income for most workers. The Pensions and Lifetime Savings Association estimates that a 'moderate' retirement standard of living in the UK requires a pension pot of approximately £490,000 for a single person. Few defined-contribution savers who have contributed only at minimum auto-enrolment rates throughout their career will approach this figure.

The problem is compounded by the generational dynamics already discussed. Gen X — the generation with the most urgent pension need and the least time to course-correct — is also the least financially optimistic, suggesting that many in this group are aware of the problem but feel unable to address it given current financial pressures. The short-term priority of covering living costs inevitably displaces the longer-term priority of pension saving, even when individuals understand the trade-off they are making. As Kate Smith from Aegon noted in the survey commentary: 'for many people, pension saving will need to be given greater priority in future if they are to build up an adequate income for retirement.'

What Drives Financial Optimism — and What Erodes It

Understanding what creates the gap between the 60% who feel financially positive and the 36% who feel negative requires looking beyond the raw demographic splits to the structural factors that determine financial confidence.Factors that correlate with higher financial optimism

Employment status is the strongest single predictor of financial optimism. The FinWell Index consistently identifies unemployment as one of the most severe drivers of low financial wellbeing — both objectively and subjectively. Job security, regular income, and employer pension contributions are the foundation on which most households' financial confidence rests. The fact that the overall positivity rate has held at 60% despite renewed inflationary pressures in 2026 likely reflects the relative resilience of the UK labour market, with unemployment remaining low.Homeownership with significant equity correlates strongly with financial confidence, particularly for older households where the mortgage may be small or paid off. The asymmetry between homeowners with locked-in low rates (who are insulated from housing cost inflation) and renters or recent remortgagors (who face market-rate increases) is a significant structural driver of the financial confidence gap. Boomers, many of whom own their homes outright or have small mortgages relative to current valuations, show above-average positivity at 62% — consistent with this dynamic.

Factors that erode financial optimism

The top concern cited by one third of Aegon survey respondents is unexpected expenses — the worry that an unforeseen cost (car repair, home repair, health expense, redundancy) will derail their finances. This concern is directly related to the emergency savings priority identified by 34% of respondents. A household with three to six months of living costs in easily accessible savings approaches unexpected expenses with relative equanimity; one without that buffer approaches them with dread. The cost of living crisis has depleted emergency savings for many households, and rebuilding that buffer is clearly a conscious priority for a significant proportion of UK adults in 2026.Which?'s Consumer Insight Tracker for March 2026 found that 49% of households had made at least one adjustment to cover essential spending in the previous month — cutting back on essentials, dipping into savings, selling possessions, or borrowing. Consumer confidence in the future UK economy fell to -55 in March, its lowest level since late 2022. These broader economic anxieties are the backdrop against which individual financial optimism is formed, and they help explain why the 40% who feel negative about their finances in the Aegon data do so despite the headline positivity remaining at 60%.

The Structural Forces Behind the Gaps

The gender and generational gaps in financial optimism are not accidental or random. They are the product of structural features of the UK economy, tax system, benefit system, and housing market that create systematically different financial outcomes for different groups.The pension system is perhaps the clearest structural contributor to the gender gap. Women's pension pots are smaller at every age group. Career breaks for childcare create multi-year gaps in pension accumulation. Part-time work (more common among women) reduces auto-enrolment contributions. The state pension triple lock protects the basic income floor for retirees, but it cannot compensate for a lifetime of lower pension savings driven by structural labour market inequality. Women in their 50s and 60s — many of them Gen X — face a combination of lower financial optimism and real pension underfunding that represents a genuine future financial security risk.

The housing market is the clearest structural contributor to generational differences in financial outlook. Baby Boomers who bought property in the 1980s and 1990s — when prices relative to income were far more accessible — have accumulated substantial housing wealth that acts as a financial security buffer. Gen Z and Millennials face the highest price-to-income ratios in history, making homeownership either inaccessible or highly leveraged. Gen X is caught between: many own homes but face the highest mortgage payment increases from rate rises, and their adult children's inability to afford independent housing creates financial obligations that limit their own savings capacity.

How the Gaps Compare to Wider Wellbeing Data

The financial optimism gaps identified in the Aegon data do not exist in isolation — they correspond to and in some cases contradict patterns found in wider wellbeing research, which helps contextualise their significance.The ONS Public Opinions and Lifestyle Survey (January to February 2026) found that overall, 69% of UK adults report high levels of hope for the future — significantly higher than the 60% who feel financially positive, suggesting that many people whose financial outlook is cautious or negative retain broader life optimism. Interestingly, the ONS data shows women are more likely than men to report high levels of hope (73% vs 65%) — the reverse of the financial optimism pattern. This divergence suggests the gender gap in financial confidence is specifically financial in nature, not a generalised pessimism among women, and is therefore more likely to be addressable through structural changes (equal pay, better childcare provision, pension reform) than through attitudinal interventions.

The FinWell Index 2025 data provides further context: while overall financial wellbeing has declined slightly, the 25 to 34 age group (younger Millennials) bucked the trend with a 4.7-point improvement in wellbeing scores. This aligns with the Aegon finding that Millennials are the most financially optimistic generation and suggests a genuine underlying improvement in the financial position of younger-middle-aged adults — possibly reflecting the beginning of peak earning years combined with pandemic-era savings habits.

What These Findings Mean for Different Groups

Tailored implications by group — what the data means for you

- Gen X (44–59): If you are in this group and among the 51% who are not positive about your finances, the most impactful actions are: a full pension review (how much are you projected to have at 67? Is it enough?), an assessment of what your adult children and/or parents are costing you and whether any of those costs could be reduced, and a check on your mortgage rate situation if you are approaching a fixed-rate renewal.

- Women: The gender gap in financial optimism reflects real structural disadvantages that require structural solutions — but there are individual steps that help. Checking your National Insurance record for gaps (which reduce your state pension entitlement) and making voluntary contributions to fill gaps is one of the highest-return financial actions available. Reviewing your pension contributions and ensuring they are at least matched by your employer is another. If you have taken a career break, consider whether catching up on pension contributions via one-off payments is feasible.

- Gen Z (18–27) and Millennials (28–43): Your relatively higher optimism is encouraging — but make sure it is grounded in concrete financial foundations rather than general positivity. The 34% emergency savings priority is directly relevant: if you do not have three months of living costs in accessible savings, building that buffer before any other financial goal is the highest-priority action. The 12% pension saving priority is a warning: starting or increasing pension contributions in your 20s and 30s has a disproportionate long-term impact compared with starting later.

- Baby Boomers (60–78): Your above-average positivity at 62% likely reflects housing equity and pension entitlements that provide security. Key risks to monitor: the real cost of long-term care (which is not covered by the NHS and can rapidly deplete even substantial savings), the impact of inheritance planning on your own financial security, and whether your investment portfolio is appropriately positioned for a retirement drawdown strategy rather than an accumulation strategy.

- Anyone in the 36% who feel negative: The top concerns in the Aegon data — unexpected expenses and covering basic costs — are addressable. Check your full benefit entitlement (many households are not claiming everything they are entitled to via Turn2Us or entitledto.co.uk). Review all bills for switching opportunities. Seek free debt advice from StepChange or Citizens Advice if debt is a factor. Small, systematic improvements across multiple areas compound over time into meaningful financial resilience.

How to Improve Your Own Financial Optimism in 2026

Financial optimism is not just a feeling — it is closely correlated with concrete financial behaviours and outcomes. Research consistently shows that households with documented plans, adequate emergency savings, and an accurate understanding of their financial position feel more positive about their finances than those who manage reactively. Here are the most evidence-backed steps to improve both your financial position and your confidence about it.Seven evidence-backed steps to build financial confidence in 2026

- Build your emergency fund first: The top concern in the Aegon data is unexpected expenses. A fund of three months' essential costs in an instant-access savings account (use a high-rate easy-access account at 4.5%+ to make the most of current rates) removes the single greatest source of financial anxiety for most households.

- Get a complete picture of your financial position: Write down all income, outgoings, savings, debts, and pension projections in one place. Research consistently shows that people who know their numbers feel more in control — even when those numbers are challenging — than those who avoid looking. Use the MoneyHelper pension calculator at moneyhelper.org.uk to project your pension.

- Check your State Pension forecast: Visit the Check Your State Pension page at gov.uk/check-state-pension. If you have gaps in your National Insurance record, consider whether voluntary contributions are worthwhile. For women who took career breaks, this can represent a significant improvement in retirement income at relatively low cost.

- Prioritise pension contributions: Pension saving at 12% of priorities is too low given the scale of the under-saving problem in the UK. If you can increase your pension contribution — particularly to take full advantage of employer matching — even a 1% to 2% increase today compounds significantly over 10 to 20 years. Use salary sacrifice if your employer offers it to save on National Insurance as well.

- Negotiate your salary or seek higher-paying opportunities: The gender pay gap and career break effects on women's financial outcomes are most effectively closed through higher earnings. Benchmarking your salary using Glassdoor, LinkedIn Salary, and ONS earnings data, and negotiating proactively, is one of the most financially impactful actions available — particularly for women who are below market rate.

- Connect financial goals to life goals: Research from MoneyHelper and the Money and Pensions Service consistently shows that people who connect their saving and financial planning to specific life goals — a holiday, a home, financial independence — are more motivated to maintain those plans than those who save abstractly. Know what you are saving for.

- Seek advice early: Only a small minority of UK adults use regulated financial advice, partly due to cost. MoneyHelper provides free guidance. The FCA's register (register.fca.org.uk) lists qualified advisers. For those with more complex situations — pensions, investments, inheritance — the cost of advice is almost always justified by the outcomes it produces.

CONCLUSION

The 60% financial positivity figure from Aegon's 2026 survey is a genuine achievement — particularly given that it has held firm against renewed inflationary pressures and marks a significant improvement on the 52% recorded in early 2024. The UK's financial resilience, built through five years of navigating the most severe cost of living crisis in four decades, is real.But the gaps embedded in that average are a more important story than the average itself. A 10-percentage-point gender gap that has been widening for years, driven by structural inequalities in pay, pension accumulation, and caregiving responsibilities, is not a statistical curiosity — it is a policy failure in plain sight. Gen X's position as the least optimistic generation, sandwiched between care responsibilities and an inadequate pension, is a warning of a retirement crisis that is decades in the making and still not fully visible in the aggregate data. And the dominance of 'covering basic living costs' as the top financial priority — ahead of savings, investment, and long-term planning — after five years of cost of living crisis tells us that the financial recovery is incomplete for a very large number of UK households.

Understanding which group you are in, what structural forces are shaping your financial confidence, and what practical steps are most likely to improve your situation is the starting point for turning financial anxiety into financial action.

Frequently Asked Questions

What is the source of the 60% UK financial positivity figure?

The 60% figure comes from Aegon's annual Financial Priorities survey, published in January 2026. Aegon is one of the UK's largest pension and insurance providers. The survey is conducted annually and is designed to measure UK financial sentiment and priorities. The January 2026 edition found that 60% of UK adults feel positive about their finances for 2026 — matching the 2025 figure and up from 52% in early 2024. Broken down, 11% feel 'extremely positive' and 49% 'somewhat positive', compared with 36% who feel negative. The original survey findings are available at aegon.co.uk.Why do Millennials feel more financially positive than Gen X?

Several structural factors explain this counterintuitive finding. Millennials (aged 28 to 43) are generally in or approaching peak earning years, benefiting from career progression and salary growth. Many have avoided the specific pressures facing Gen X: they are less likely to be supporting ageing parents in a care context and less likely to have adult children whose housing costs they are partly subsidising. They also have more time to address retirement savings shortfalls than Gen X. Gen X faces the 'sandwich generation' dynamic — simultaneously supporting both older and younger generations financially — combined with higher mortgage transition costs from fixed-rate periods ending and a pension funding gap with less time to correct it.Why is the gender gap in financial optimism so persistent?

The gender gap in financial confidence reflects structural inequalities rather than attitudes. The gender pay gap (women earning approximately 7–8% less than men for full-time work, per ONS data) directly reduces women's ability to save and build financial buffers. Career breaks for childcare, disproportionately taken by women, create gaps in pension accumulation. Women are more likely to work part-time, which reduces pension auto-enrolment contributions. The UK FinWell Index found the gender gap in financial wellbeing widened 29% in a single year (2024 to 2025). Closing the gender pay gap, improving childcare provision, and pension contribution catch-up policies are the most effective structural solutions.What are the most important financial priorities for UK adults in 2026?

Aegon's 2026 survey found that covering basic living expenses (39%) is the top priority, followed by building emergency savings (34%) and enjoying life (33%). Pension saving is a top three priority for only 12% of respondents — a concern given the scale of pension under-saving in the UK. Unexpected expenses are the top financial concern, cited by approximately one third of respondents. This data suggests that short-term financial stability and resilience are dominating household financial planning, with longer-term wealth building taking a back seat for most households.Why is pension saving ranked so low as a priority?

Aegon and pension experts including Kate Smith have flagged the 12% figure as a concern. The low ranking reflects the dominance of short-term financial pressures — covering living costs, building emergency savings — over long-term planning. When households are managing essentials, pension saving is naturally deprioritised. However, the compounding effect of pension under-saving means that decisions made today have large long-term consequences. The Pensions and Lifetime Savings Association estimates that a 'moderate' retirement income requires a pension pot of approximately £490,000 for a single person — a figure that few defined-contribution savers at minimum auto-enrolment rates will reach. Anyone who can increase pension contributions, even incrementally, is well-advised to do so as early as possible.What practical steps can I take if I am in the 36% who feel financially negative?

Start with the fundamentals: check your full benefit entitlement at turn2us.org.uk or entitledto.co.uk; review all bills for switching opportunities (energy, insurance, broadband); and seek free budgeting or debt advice from StepChange (stepchange.org) or Citizens Advice (citizensadvice.org.uk) if debt is a factor. For pensions, check your state pension forecast at gov.uk/check-state-pension and review workplace pension contributions. The MoneyHelper service at moneyhelper.org.uk provides free, impartial guidance on budgeting, debt, savings, and pensions without any obligation. Small, systematic improvements across multiple areas compound meaningfully over 12 to 24 months.References

Aegon UK — New Year Financial Positivity But Gaps Persist (January 2026) https://www.aegon.co.uk/media-centre/news/new-year-financial-positivity-but-gaps-persist-IFA Magazine — Majority Upbeat on Finances for 2026 But Gender and Generation Gaps Persist https://ifamagazine.com/majority-upbeat-on-finances-for-2026-but-gender-and-generation-gaps-persist/

ONS — Public Opinions and Social Trends: January 2026 (household finances, wellbeing) https://www.ons.gov.uk/peoplepopulationandcommunity/wellbeing/bulletins/publicopinionsandsocialtrendsgreatbritain/january2026

Stream — UK FinWell Index 2025: State of Financial Wellbeing https://stream.co/en/reports/the-state-of-financial-wellbeing-2025

Money and Pensions Service — Gender, Mental Health and Ethnicity in UK Financial Wellbeing https://moneyandpensionsservice.org.uk/2023/01/10/cross-cutting-themes-adult-financial-wellbeing-survey/amp

J.P. Morgan Personal Investing — Younger Investors Are More Bullish Than Older Generations for 2026 https://www.personalinvesting.jpmorgan.com/insights/younger-investors-are-more-bullish

Confused.com — 3 in 5 Brits Put Financial Security at Top of 2026 Goals (January 2026) https://www.confused.com/press/releases/2026/3-in-5-brits-put-financial-security-at-the-top-of-their-2026-goals

Which? — Financial Wellbeing in March 2026 (Consumer Insight Tracker) https://www.which.co.uk/policy-and-insight/article/financial-wellbeing-in-march-2026-aSMyI5I1b1hr

MoneyHelper — Free Financial Guidance (pensions, budgeting, debt) https://www.moneyhelper.org.uk

GOV.UK — Check Your State Pension https://www.gov.uk/check-state-pension

0 Comments Comments