Finance

How to Open a Bank Account and What You Need in The UK

Table of Contents

- Why a Bank Account Matters and How Easy It Is to Open One

- Who Can Open a Bank Account in the UK?

- What Documents You Need: The Complete Reference

- Types of Bank Account: Which One Is Right for You?

- How to Open a Bank Account Online: Step by Step

- Opening a Bank Account In Branch: When and How

- If You Do Not Have Standard ID: Basic Bank Accounts

- Switching Accounts and Protecting Your Money

- The Current Account Switching Service (CASS)

- FSCS Protection: Your Savings Are Safe

- Opening a UK Bank Account as a Non-UK National or New Arrival

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why a Bank Account Matters and How Easy It Is to Open One

A bank account is the foundation of your financial life in the UK. It is where your salary lands, where your bills are paid, where your savings grow, and where your financial identity is established. Without one, everyday tasks that most people take for granted — receiving a wage, setting up a direct debit, paying rent, accessing government benefits — become complicated or impossible. Yet the process of opening a bank account is simpler than many people realise, and in 2026, it has never been faster.

Most UK banks now offer fully online account opening. For the majority of applicants with a valid passport or UK driving licence, the entire process — from starting the application to receiving account details — takes under 30 minutes. Digital-first banks like Monzo, Starling, Chase, and Revolut complete identity verification through a smartphone selfie and a photo of your ID, and can have your account live within minutes of approval. Traditional high-street banks process most applications within the same day online, or 30 to 45 minutes in branch. The account details are typically available immediately or the next working day, with a debit card arriving in the post within a few days.

This guide explains exactly what you need to open a bank account in the UK in 2026 — the documents, the eligibility requirements, and what happens if you do not have standard ID. It covers every major type of account, from standard current accounts and student accounts to basic accounts for those with credit issues and digital app-only accounts for those who want to open in minutes. It explains how FSCS deposit protection works, what the Current Account Switching Service (CASS) does, and how the process works differently for children, students, non-UK nationals, and those arriving new to the country.

Who Can Open a Bank Account in the UK?

Most UK banks set the following general eligibility criteria for their standard current accounts:- Age: The minimum age for most adult current accounts is 18. Some banks offer accounts from age 16 (Starling accepts 16-year-olds; NatWest has accounts from 11 with parental involvement). Children's accounts are available from as young as six with parental or guardian support.

- UK residency: You must be a UK resident to open most UK bank accounts. This means you must have a UK address where you currently live. Non-UK citizens can open accounts as long as they have the legal right to reside in the UK — confirmed by a valid visa, Biometric Residence Permit, or other immigration documentation. Banks are legally required to conduct Immigration Act status checks and cannot open accounts for those who do not have the right to be in the UK.

- Credit status (for overdrafts and some accounts): Banks will run a credit check when you apply for certain accounts, particularly those offering overdrafts. A poor credit history may mean you are offered a more basic account rather than a full current account, or an account without an overdraft facility. A failed credit check does not prevent you from banking entirely — you remain entitled to a basic bank account regardless of credit history.

- No history of fraud: If you have a record of fraud or banking fraud specifically, this may result in a refusal. Banks share information about fraudulent behaviour through a database called CIFAS. A CIFAS marker against your name — indicating a previous account was used fraudulently — can prevent standard account opening, though basic accounts may still be available.

KYC — the legal requirement that drives the document list: Every UK bank must verify your identity under FCA Know Your Customer rules — under the Money Laundering Regulations 2017 and the FCA's Know Your Customer (KYC) requirements, all UK banks are legally obligated to verify the identity and address of every new customer before opening an account. This is the reason the document requirements exist — they are a regulatory obligation, not a bank preference. Banks that fail to comply face significant FCA penalties (Revolut UK, May 2026 / FCA).

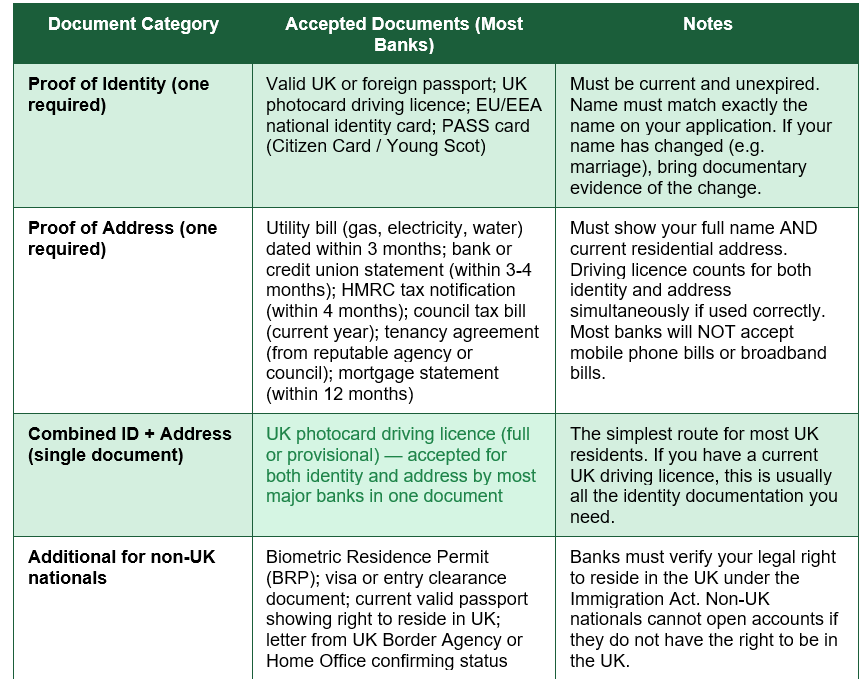

What Documents You Need: The Complete Reference

The table below provides the definitive reference for every document type accepted by UK banks in 2026, sourced from the current published requirements of NatWest, HSBC, Lloyds, Barclays, and digital banks including Revolut, Monzo, and Starling:

THE QUICKEST DOCUMENT COMBINATION: A valid UK photocard driving licence (full or provisional) serves as proof of identity AND proof of address simultaneously at most UK banks — it is the fastest way to complete the documentation requirements with a single document. If you do not have a driving licence, your passport combined with a recent utility bill (under 3 months) is the most widely accepted alternative combination.

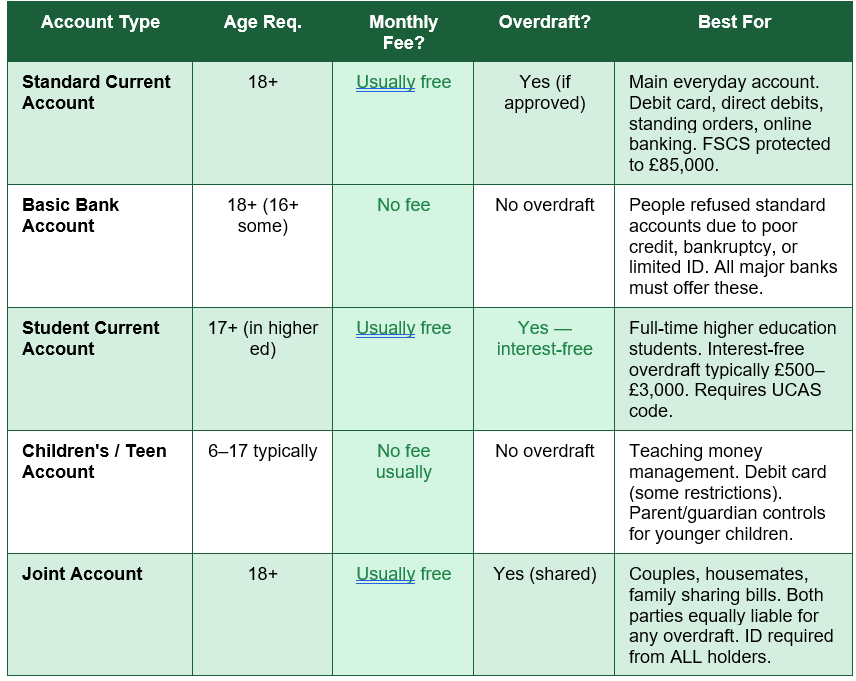

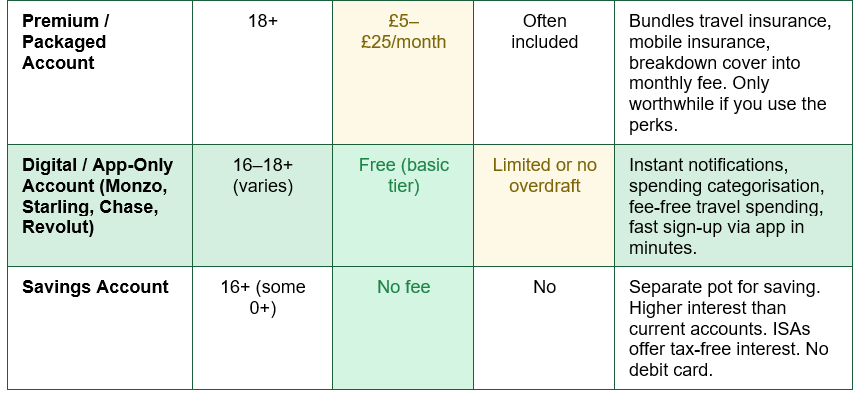

Types of Bank Account: Which One Is Right for You?

Choosing the right account before you apply saves time and ensures you end up with the account that suits your actual needs. The table below compares every major type of UK bank account available in 2026:

How to Open a Bank Account Online: Step by Step

The majority of UK bank account applications are now completed entirely online — either through a bank's website or, increasingly, through a smartphone app. The standard online process follows these steps:- Choose the right type of account and provider: Compare accounts using MoneySuperMarket, GoCompare, or MoneySavingExpert's best buys before starting. Consider whether you want a traditional high-street bank with branch access, a digital-only bank with faster setup, or a specific account type (student, basic, packaged). Check the provider's specific eligibility requirements for your age, residency, and circumstances before beginning.

- Gather your documents before starting: Have your proof of identity and proof of address to hand before you begin. For an online application, you will need to photograph both documents using your phone or computer camera. Make sure documents are not expired, the details are clearly legible, and the name on your documents exactly matches the name you will enter in the application.

- Complete the online application form: Most applications ask for: your full legal name (and any previous names); date of birth; nationality and any dual nationalities; current residential address (and previous addresses if you have lived at your current address for less than three years); contact details (mobile number, email address); employment status and income details; National Insurance number (most banks ask for this, though not all require it upfront); how you intend to use the account (main account, second account, etc.).

- Complete digital identity verification: Under FCA Know Your Customer rules, banks must verify your identity before opening any account. Online, this typically means: uploading a photograph of your identity document (passport or driving licence) taken using your device's camera; completing a liveness check — a selfie photograph or short selfie video — so the bank's system can compare your face to the photo on your ID. Some banks use live video verification where you briefly interact with a system or a member of staff.

- Receive your decision and account details: Most applications are processed automatically and produce a decision within minutes. If approved, your sort code and account number are typically displayed immediately on screen and sent to your email. Your debit card is sent by first-class post and usually arrives within 3-5 working days. Some banks (Monzo, Starling, Chase) can provide immediate digital card access through their app while your physical card is in transit.

- Set up your account: Once your account is live, set up any direct debits or standing orders you need, provide your new account details to your employer for salary payments, and download the bank's mobile app if you have not already. If you are switching from an existing bank account, the Current Account Switching Service (CASS) can transfer all your direct debits, standing orders, and incoming payments automatically within 7 working days — see the switching section below.

Opening a Bank Account In Branch: When and How

In-branch account opening remains available at all major high-street banks and is sometimes the better option if: you are opening your very first account and want assistance; your online application has been referred for manual review; you have non-standard documentation that needs to be reviewed in person; you prefer face-to-face interaction; or you are opening an account that requires specific in-branch verification.In branch, a member of staff will take you through the application form, verify your original documents directly (you do not need to photograph them), and ask a few straightforward questions about your financial situation — primarily to confirm your identity and assess overdraft eligibility. The whole process typically takes 30 to 45 minutes. Your account details are usually available immediately or the same day, and your debit card is sent by post. Some branches may be able to provide a temporary card if you need it urgently.

Note that branch banking has reduced significantly in the UK over the past decade — Lloyds, for example, has been closing branches at pace, and many smaller towns now have no high-street bank branch. Check your local branch's opening hours and availability before making a special trip, and always check whether the same outcome is achievable through the online process before travelling.

Digital banks: the fastest route in 2026: App-based banks including Monzo, Starling, Chase UK, and Revolut have transformed the account-opening experience. Monzo's application takes a few minutes: download the app, enter your details, photograph your ID, take a selfie video, and your account is typically verified and live within the same session. Starling Bank and Chase UK operate the same model. All are fully FCA-regulated, FSCS-protected to £85,000, and carry Visa or Mastercard debit cards. They are particularly well-suited to those who want instant notifications, spending analysis, and fee-free spending abroad. Digital bank accounts are now the fastest option for most people in 2026.

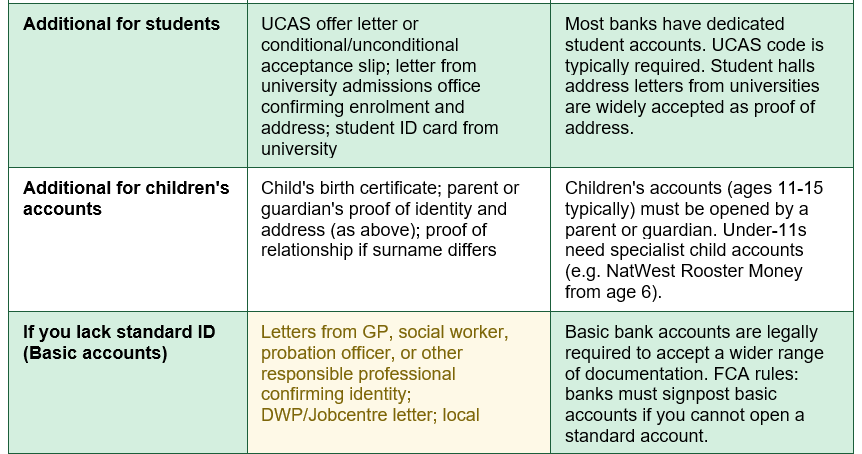

If You Do Not Have Standard ID: Basic Bank Accounts

Every UK bank that offers current accounts is legally required by the FCA to also offer basic bank accounts — accounts with no overdraft facility and simplified eligibility requirements, specifically designed to ensure that everyone in the UK has access to basic banking services regardless of credit history, bankruptcy status, or limited documentation.Basic bank accounts accept a wider range of identity documents than standard accounts, including letters from a GP, social worker, probation officer, DWP, local authority, or other responsible organisation confirming your identity and address. They provide the essential banking services most people need: a debit card, direct debit capability, and online and mobile banking access. They do not provide overdrafts, and some may have restrictions on the number of free transactions.

Citizens Advice's guidance on bank accounts explicitly states: 'If you don't have any of the documents that the bank wants, they should accept a letter from a responsible person who knows you, such as a GP, teacher, social worker or probation officer.' This safeguard means that even without a passport, driving licence, or utility bill, you can access basic banking services in the UK through the right documentation and with the right account type.

The major banks — Barclays, Lloyds, HSBC, NatWest, Santander, and others — all offer basic accounts and must tell you about them if you ask. Credit unions also provide accessible accounts for people who cannot access mainstream banking. MoneyHelper's helpline (0800 138 7777) and Citizens Advice can both provide guidance on accessing a basic account if you are having difficulty.

Switching Accounts and Protecting Your Money

The Current Account Switching Service (CASS)

If you already have a UK bank account and want to move to a different bank, the Current Account Switching Service (CASS) makes this automatic and guaranteed. As HSBC's official guidance confirms: 'All you need to do is tell us your old bank details and when you want to switch. All of your payments will be moved automatically, including regular payments like Direct Debits and your salary within 7 working days.' The switching service is free, legally protected, and used by millions of UK consumers every year. Any payment misdirected to your old account after switching is automatically redirected to your new one for 36 months.FSCS Protection: Your Savings Are Safe

All deposits in UK-regulated bank accounts — current accounts, savings accounts, and cash ISAs — are protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per person per banking group. This means that if your bank fails, your money is protected and returned to you by the FSCS up to this limit. Joint accounts receive £85,000 per account holder — effectively £170,000 per couple. If you hold significant cash savings and want to maximise your FSCS protection, spreading funds across multiple banking groups (not just multiple brands under the same parent) provides additional coverage.CHECK YOUR BANKING GROUP: Some banks share FSCS protection limits because they are part of the same banking group. Halifax and Bank of Scotland, for example, are both part of Lloyds Banking Group — deposits across both banks share the £85,000 limit, not get separate limits. The FSCS's own checker at fscs.org.uk shows which banks share limits. If you hold more than £85,000 in savings, splitting it across genuinely separate banking groups ensures maximum protection.

Opening a UK Bank Account as a Non-UK National or New Arrival

Non-UK nationals who have the legal right to live and work in the UK can open standard bank accounts with most major banks, but may face additional documentation requirements and, in some cases, a more limited choice of accounts than UK citizens with established credit histories. The additional documentation most commonly required includes your passport showing your right to reside, your Biometric Residence Permit (BRP) if you have one, your visa or entry clearance document, and in some cases your visa expiry date (some banks will not issue accounts with terms exceeding your visa validity).If you are arriving in the UK for the first time and do not yet have UK address documentation, some banks will accept letters from your employer, university, or the organisation that sponsored your visa as proof of address. Barclays, HSBC, and Lloyds all have specific guidance for international arrivals and in some cases offer international student accounts or expat accounts designed for this transition period. Digital banks — particularly Monzo and Starling — tend to have simpler processes for non-UK nationals, provided you have a valid passport or national ID card and a UK address.

Wise (formerly TransferWise) offers a multi-currency account that can be particularly useful for those who have recently arrived in the UK and need to manage money in multiple currencies while establishing their UK banking relationship. It is not a full UK bank account but provides an IBAN and debit card and can serve as a bridge while a standard account application is processed.

Conclusion

Opening a bank account in the UK in 2026 requires just two documents: a proof of identity and a proof of address. For most UK residents, a current driving licence satisfies both requirements with a single document. For those without a driving licence, a valid passport combined with a recent utility bill, bank statement, or HMRC letter serves the same purpose. The entire process, for most applicants, takes under 30 minutes online — and for digital banks like Monzo, Starling, and Chase, it can be completed in minutes via a smartphone app with instant account access.For those facing specific barriers — no standard photo ID, poor credit history, new to the UK without established address documentation — the basic bank account system ensures that banking access is never entirely out of reach. All major UK banks are legally required by the FCA to offer basic accounts, which accept a wider range of identity documentation and do not require a credit check. Citizens Advice, MoneyHelper, and local credit unions can all provide support for those who encounter difficulties with standard account applications.

Once your account is open, FSCS protection guarantees your deposits up to £85,000 per banking group. The Current Account Switching Service makes changing banks effortless and automatic within 7 working days. And the competitive landscape of UK banking in 2026 — with digital-first banks offering instant notifications, fee-free overseas spending, and cashback on purchases alongside traditional banks with branch networks and established overdraft facilities — means there genuinely is an account suited to every financial situation, lifestyle, and need.

Frequently Asked Questions (FAQ)

What documents do I need to open a bank account in the UK?

You need two types of documentation: proof of identity and proof of address. For proof of identity, most banks accept a valid UK or foreign passport, a UK photocard driving licence (full or provisional), or an EU/EEA national identity card. For proof of address, they accept a utility bill (gas, electricity, or water) dated within the last three months, a recent bank statement, an HMRC letter, a council tax bill for the current year, or a tenancy agreement. A UK photocard driving licence is the most convenient option because it counts as proof of both identity and address in a single document — no second document required.How long does it take to open a bank account in the UK?

The time depends on whether you apply online, in branch, or via a digital bank app. Digital app-based banks (Monzo, Starling, Chase, Revolut) can have your account live and accessible within minutes of submitting your application, as long as your identity verification passes automatically. Traditional high-street banks processing online applications typically take a few hours to the same day for approval, with account details available immediately and a debit card arriving by post within three to five working days. In-branch applications take 30 to 45 minutes of your time in the branch, with account details typically available immediately. If your application requires manual review — because documents are unclear or identity cannot be confirmed automatically — it may take one to three business days.Can I open a bank account if I have bad credit?

Yes — you can open a basic bank account regardless of your credit history. All major UK banks are legally required by the FCA to offer basic bank accounts, which do not involve a credit check and are specifically designed for people who cannot access standard current accounts. Basic accounts provide the core banking services most people need: a debit card, direct debit capability, and online banking. They do not provide overdraft facilities. If you are refused a standard account due to a poor credit history, ask the bank specifically about their basic account — they are required to tell you if they offer one and what you need to qualify. Citizens Advice (0808 223 1133) can also provide guidance on accessing banking services with poor credit.Can I open a UK bank account online from abroad?

It depends on the bank and your circumstances. Some banks — HSBC, Barclays, and Lloyds — have specific international or pre-arrival account services that allow you to open an account before you arrive in the UK, though these typically require you to demonstrate your connection to the UK (a job offer, university place, or visa). Most standard UK banks require you to be a UK resident with a UK address before they will open an account. Digital banks including Revolut and Wise offer multi-currency accounts that can be useful for international money management while you establish your UK banking relationship, though these are not the same as a full UK current account with FSCS protection.Is my money safe in a UK bank account?

Yes — deposits in UK-regulated bank accounts are protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per person per banking group. If your bank fails, the FSCS will return your money up to this limit, typically within seven days. Joint accounts receive £85,000 per account holder, providing up to £170,000 protection per couple. Digital banks including Monzo, Starling, Chase UK, and Revolut Bank UK are all FCA-regulated and FSCS-protected — they carry the same protection as traditional high-street banks. Check fscs.org.uk to confirm protection for any specific bank or to check which banks share a banking group for protection purposes.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. NatWest — What You Need to Open a Bank Account (Updated July 2026)

https://www.natwest.com/current-accounts/what-do-you-need-to-open-a-current-account.html

2. HSBC UK — What Do You Need to Open a Bank Account / Documents for ID Check

https://www.hsbc.co.uk/current-accounts/what-do-you-need-to-open-a-current-account/

3. Lloyds Bank — What You Need to Open a Bank Account (March 2026)

https://www.lloydsbank.com/current-accounts/help-and-guidance/opening-a-bank-account.html

4. Citizens Advice — Getting a Bank Account

https://www.citizensadvice.org.uk/debt-and-money/banking/getting-a-bank-account/

5. Revolut UK — What Do You Need to Open a Bank Account in the UK? (May 2026)

https://www.revolut.com/blog/post/what-do-you-need-to-open-a-bank-account-in-the-uk/

6. Zopa — How to Open a Bank Account in the UK: What You Need and What to Expect (April 2026)

https://www.zopa.com/blog/article/how-to-open-a-bank-account-in-the-uk-what-you-need-and-what-to-expect

7. MoneyHelper — Bank Accounts and FSCS Protection Guidance

https://www.moneyhelper.org.uk/en/everyday-money/banking

8. FSCS — Protecting Your Deposits (Check Your Banking Group)

https://www.fscs.org.uk/check/deposit-checker/

0 Comments Comments