Spending

How to use The 30% Rule & Debt Secrets of the Wealthy

Table of Contents

- What the 30% Rule Actually Says — and Where It Came From

- How the Wealthy Think About Debt Entirely Differently

- The Strategy Everyone Is Talking About: Buy, Borrow, Die

- Other Debt Strategies the Wealthy Actually Use

- Securities-Based Lines of Credit (SBLOCs)

- Good Debt vs Bad Debt: The Wealth-Building Framework

- Leveraged Buyouts and Arbitrage

- What This Means for People Who Are Not Billionaires

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

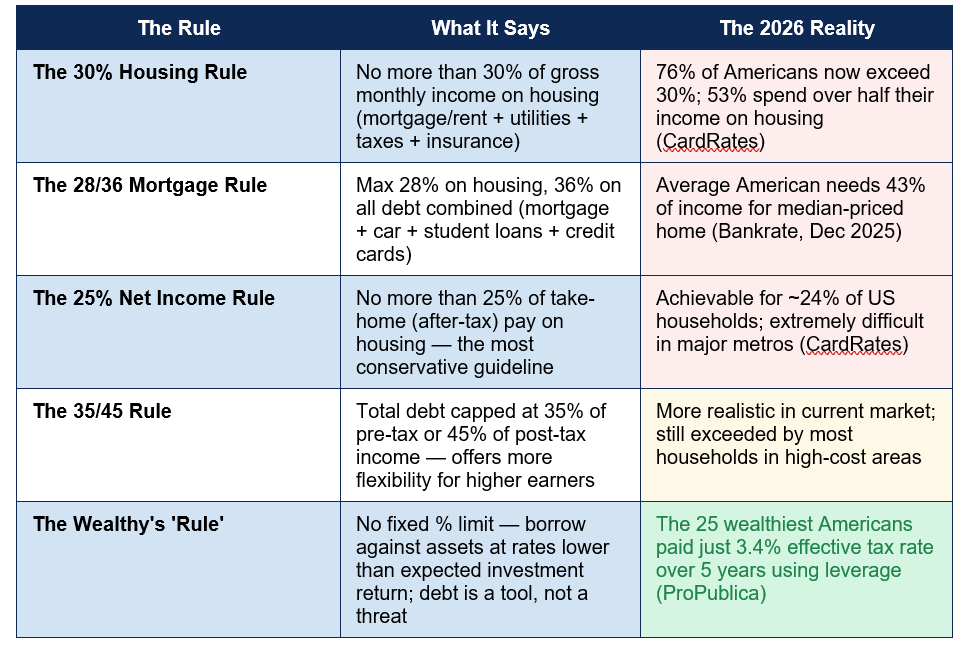

There is a rule everyone in personal finance knows and almost nobody actually follows: spend no more than 30% of your gross monthly income on housing. It sounds sensible. It has been repeated by financial advisers, mortgage lenders, and personal finance educators for decades. And according to a CardRates study, 76% of Americans are now blowing past that threshold, with 53% spending more than half their monthly income on housing alone.

The 30% rule is broken — not because the people ignoring it are irresponsible, but because housing costs have simply outpaced wages at such a scale that for most households in most markets, the rule is no longer achievable. Bankrate's December 2025 analysis found the typical US household needs to dedicate 43% of income to afford a median-priced home. In San Francisco, New York, or Miami, that figure climbs significantly higher. The rule that was designed to protect Americans from becoming 'house poor' has become, for many, a standard no one can reach without moving somewhere most people do not want to live.

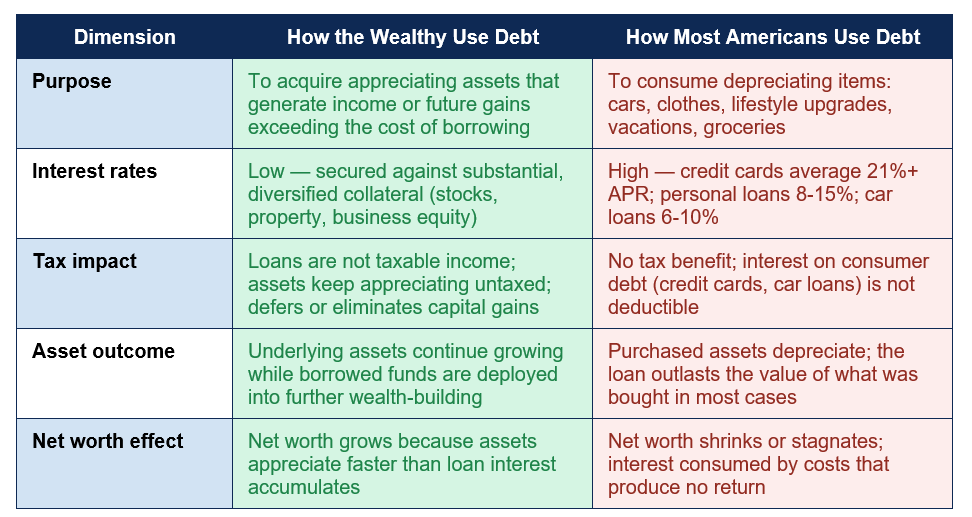

But here is what the personal finance world rarely discusses alongside the 30% rule: the wealthy do not use the 30% rule at all. They do not budget for debt in the same way. They do not treat debt as something to be minimised and eventually eliminated. For the ultra-rich, debt is a precision instrument — a way to generate liquidity without triggering taxes, to amplify investment returns, and to build wealth faster than any savings rate could achieve. Understanding this gap is not just intellectually interesting. It is practically important for anyone thinking seriously about their long-term financial position.

What the 30% Rule Actually Says — and Where It Came From

The 30% rule traces its origins to 1969, when US public housing regulations capped rent for low-income residents at 25% of income. In the early 1980s, that cap was raised to 30%, and the figure was subsequently adopted as a general housing affordability guideline by lenders, financial planners, and government agencies. It was never designed to be a universal law — it was a policy threshold for assisted housing that became, through repetition, a widely accepted rule of thumb.The table below provides the full picture of debt-to-income guidelines in use today, including where the 30% rule fits alongside related standards and — critically — how the wealthy actually approach debt:

The 30% rule in 2026: 76% of Americans exceed it, and the average household needs 43% for a median home — the rule that was designed to prevent 'house poor' outcomes now describes an income-to-housing ratio achievable only by a minority of households, particularly outside lower-cost markets (CardRates / Bankrate, December 2025).

Why the rule broke: The 30% guideline was conceived in a housing market where incomes and home prices rose in broadly parallel fashion. Since approximately 2020, that relationship has fractured sharply. US home prices rose approximately 40% over the pandemic era while median wages rose far more slowly, a divergence that no fixed-percentage rule can adequately account for. In the most expensive markets, the affordability math does not work at any reasonable income percentage without a very substantial down payment.

How the Wealthy Think About Debt Entirely Differently

The most fundamental difference between how the wealthy and the average American relate to debt is not about discipline or financial sophistication — it is about purpose. Kevin Reed, chief revenue officer at Aquilance, summarised it bluntly: 'Most regular people use debt to consume things that depreciate: cars, clothes, vacations. Debt is a survival or consumption tool.' Wealthy investors, by contrast, borrow to acquire assets that appreciate and generate income — and they do it at rates far below the 21% credit card APR that most Americans pay on their consumer debt.The contrast is stark and compounding. US consumer credit card debt reached $1.28 trillion in late 2025, mostly financing purchases that lose value from the moment they are made. Meanwhile, billionaires like Elon Musk regularly borrow against vast holdings of appreciated stock specifically to avoid selling it — keeping the underlying asset growing while accessing liquidity through low-rate loans secured against that collateral. The two approaches to debt describe two fundamentally different relationships with money, not two points on the same spectrum.

The Strategy Everyone Is Talking About: Buy, Borrow, Die

The phrase that has become shorthand for elite debt strategy is 'Buy, Borrow, Die' — a three-step framework first articulated by tax law scholar Edward McCaffery and subsequently brought to mainstream attention by a landmark ProPublica investigation that revealed the 25 wealthiest Americans paid an effective true tax rate of just 3.4% over five years by borrowing against rather than selling their appreciated assets.The mechanics are straightforward once understood. Wealthy individuals buy appreciating assets — stocks, real estate, private business equity — and allow those assets to grow without selling. Since unsold assets are not taxable events under current US tax law, no capital gains tax is triggered as long as the asset is held. When the owner needs cash, they borrow against the value of those appreciated assets using low-interest secured loans. The loan proceeds are not taxable income — debt is not income under the tax code. The loans are serviced using investment returns or new borrowing. When the owner eventually dies, their heirs inherit the assets with a 'stepped-up' cost basis, meaning the accumulated, untaxed capital gains effectively disappear — and the estate can sell assets to repay the loans without paying the tax that would have applied during the owner's lifetime.

Unrealised gains held by US billionaires and centi-millionaires: $8.5 trillion (2022 estimate) — representing profits from unsold investments that may never be taxed under current US law, according to analysis by Americans for Tax Fairness of Federal Reserve data — the bedrock of the Buy, Borrow, Die strategy.

BNY Wealth's banking and lending head Rick Calero illustrated the long-term mathematical advantage of this approach with a concrete example: two investors, each with $30 million in the S&P 500, both facing a $3 million annual tax bill. Investor 1 sells $3 million of portfolio assets each year to pay the bill, sacrificing that capital's future compounding. Investor 2 borrows against her portfolio each year, allowing the full $30 million to continue appreciating. After five years, Investor 2's portfolio is worth more than $22.4 million more than Investor 1's — not because of any complex scheme, but simply because borrowed money allowed all the invested capital to keep compounding.

Is Buy, Borrow, Die a loophole? The strategy has attracted significant political attention, with Senators Elizabeth Warren and Ron Wyden arguing it should be closed. Jeff Bezos, notably, told CNBC in May 2026 that he does not use it. Research from the Yale Budget Lab and scholars Liscow and Fox (2025) found that borrowing actually represents only approximately 1% of the economic income of the top 0.1% by net worth — suggesting the primary wealth preservation mechanism is not borrowing to consume, but simply never selling appreciating assets ('Buy, Save, Die'). The strategy is real and legal; its scale and universality among the ultra-wealthy is somewhat overstated.

Other Debt Strategies the Wealthy Actually Use

Securities-Based Lines of Credit (SBLOCs)

Wealthy investors with substantial brokerage portfolios can access a Securities-Based Line of Credit — essentially a revolving loan secured against the market value of their investment holdings. As Charles Schwab's May 2026 wealth management guidance explains, this allows investors to 'meet short-term cash needs while keeping wealth invested for potential long-term growth.' Interest rates on SBLOCs are typically far below consumer lending rates, since the lender holds liquid, marketable securities as collateral. The borrower does not need to sell investments to fund a tax payment, a business acquisition, or a real estate purchase — they simply draw on the credit line.The risk, as Schwab explicitly notes, is that if the portfolio value falls below a minimum threshold, the borrower may be forced to deposit additional funds or face liquidation of the collateral — potentially at the worst possible market moment. This is why leverage strategies that work well for the ultra-wealthy with diversified, multi-million-dollar portfolios are considerably more dangerous for investors whose entire wealth is concentrated in a single stock or whose portfolio is of modest size.

Good Debt vs Bad Debt: The Wealth-Building Framework

The framework the wealthy use to evaluate any borrowing decision is simple but consistently applied: good debt finances an asset expected to generate more income or capital growth than the interest cost of the loan. Bad debt finances consumption that produces no return and leaves the borrower servicing interest on something that has already depreciated in value. The Equifund analysis of wealthy debt behaviour illustrates this with a rental property example: a wealthy investor buys a $1 million property, borrows $800,000 against it at 6% APR, generates $100,000 in annual rental income, and retains $52,000 in positive cash flow annually after debt service — plus $800,000 in fresh investment capital from the loan proceeds, plus ongoing depreciation deductions that further reduce the taxable income from the property.This is the arithmetic the wealthy intuitively apply to every borrowing decision: not 'can I afford the monthly payment?' but 'does this debt, properly structured, generate more than it costs?' That cognitive reframe — from affordability thinking to return-on-capital thinking — is arguably the single most transferable insight from how the wealthy approach debt, applicable at almost any level of wealth.

Leveraged Buyouts and Arbitrage

At the institutional level of wealth, debt is used even more aggressively. Private equity firms and ultra-wealthy investors conducting Leveraged Buyouts (LBOs) routinely finance 70-90% of an acquisition's price with borrowed money, acquiring revenue-generating businesses and using those businesses' own cash flows to service the acquisition debt — a structure in which the asset effectively pays for itself. The wealthy individual or fund puts in a small slice of equity, borrows the rest at competitive rates, and benefits disproportionately from any appreciation in the business's value because the gains accrue to the equity holder.What This Means for People Who Are Not Billionaires

The honest assessment, delivered by every financial expert quoted in the wealth management literature on this topic, is that high-leverage debt strategies are genuinely more risky for smaller portfolios than for the ultra-wealthy, for a straightforward structural reason: a billionaire borrowing against a $30 billion portfolio has enormous margin for error. A middle-income investor borrowing against a $200,000 brokerage account or a $400,000 home equity position has far less cushion if asset values fall or income is disrupted.That said, several principles from wealthy debt strategy are meaningfully applicable regardless of wealth level:

- Separate good debt from bad debt explicitly in your budget: Most 30% rule discussions treat all debt equivalently. A mortgage on a property that is appreciating and costs less than local rent is structurally different from credit card debt funding consumables. Track them separately and prioritise eliminating high-cost, non-income-producing debt before worrying about 'good' debt ratios.

- Evaluate borrowing as a return-on-capital decision, not just an affordability decision: Before taking on any significant debt, apply the wealthy's arithmetic: does the asset this debt is financing generate returns above the interest rate? If the answer is no, the debt is consuming wealth rather than building it.

- American homeowners have more leverage equity than most realise: As of March 2026, the Intercontinental Exchange's Mortgage Monitor found American homeowners hold approximately $17 trillion in total equity, with roughly $11 trillion considered accessible. Home equity lines of credit (HELOCs) at current rates offer a significantly lower-cost source of borrowing than credit cards for homeowners who qualify, and that equity can be deployed into further wealth-building rather than lying dormant.

- Tax-advantaged accounts are the average person's version of the stepped-up basis: The wealthy avoid capital gains through the step-up at death. Ordinary investors can defer or eliminate capital gains by maximising Roth IRA contributions, where investments grow and can be withdrawn tax-free. While not identical, this represents the same underlying principle: allowing assets to appreciate without triggering a taxable event.

Conclusion

The 30% rule is a well-intentioned guideline with a honourable history, but it describes a housing affordability standard that 76% of Americans can no longer meet and that the typical US household would need to be earning significantly above the median to achieve in most major housing markets in 2026. This is not a personal finance failure on the part of those who exceed it — it is a structural reality of a decade in which housing costs have risen far faster than wages.The far more revealing contrast is not between the 30% rule and what Americans actually spend, but between how ordinary Americans and the wealthy relate to debt as a category. For most people, debt is an unavoidable burden arising from the gap between income and the cost of housing, transport, and consumption — a liability to be managed, reduced, and eventually eliminated. For the ultra-wealthy, debt is a strategic instrument: the mechanism through which they access liquidity without selling appreciating assets, defer or permanently avoid capital gains taxes, and amplify the returns on already-substantial portfolios.

The strategy known as Buy, Borrow, Die is both legally sound and intellectually coherent. But it is genuinely more powerful — and more safely deployed — at the scale of billions of dollars in diversified assets than at the scale of a middle-class investment portfolio. The most transferable insight is not the specific mechanics of the strategy but the underlying cognitive framework: that debt, chosen deliberately and deployed against assets with expected returns above the cost of borrowing, is a tool for building wealth rather than merely a cost of living. That reframe is available to anyone, at any wealth level, willing to apply it.

Frequently Asked Questions (FAQ)

What is the 30% rule for debt and housing?

The 30% rule is a personal finance guideline stating that no more than 30% of your gross (pre-tax) monthly income should go toward housing costs, including your mortgage or rent payment, utilities, property taxes, and insurance. It originated from 1969 US public housing regulations that capped assisted housing rents at 25% of income, raised to 30% in the early 1980s. While still cited as a standard, it is now exceeded by 76% of Americans according to CardRates data, and Bankrate's December 2025 analysis found the typical household must spend 43% of income to afford a median-priced home.What is the Buy, Borrow, Die strategy?

Buy, Borrow, Die is a wealth preservation and tax minimisation strategy used primarily by ultra-high-net-worth individuals. It involves three steps: buying appreciating assets (stocks, real estate, business equity) and holding them without selling — since unsold assets are not taxable events; borrowing against the appreciated value of those assets to generate spendable cash, since loan proceeds are not taxable income; and holding the assets until death, at which point heirs inherit them with a stepped-up cost basis, effectively eliminating the accumulated capital gains tax liability. A ProPublica investigation found the 25 wealthiest Americans paid an effective tax rate of just 3.4% over five years using strategies of this type.What is the difference between good debt and bad debt?

In the framework used by wealthy investors, good debt is borrowed money used to acquire assets whose expected income or appreciation exceeds the interest cost of the loan — rental properties generating positive cash flow, for example, or business acquisitions financed through leverage. Bad debt finances consumption that produces no return and depreciates immediately — credit card balances on daily expenses, car loans for vehicles that lose value, or personal loans for purchases with no asset value. The distinction is not about the type of loan product but about what the borrowed funds are purchasing and whether that purchase produces returns above the cost of borrowing.Can ordinary people apply wealthy debt strategies?

Some principles apply broadly. Separating income-producing debt (mortgages on appreciating properties, student loans that verifiably increase earning power) from pure consumption debt (credit cards, depreciating car loans) and prioritising elimination of the latter is the most actionable version of the wealthy mindset. Home equity — with approximately $11 trillion in tappable equity held by US homeowners as of early 2026 — represents a lower-cost borrowing source than credit cards for homeowners who qualify. And maximising Roth IRA contributions embodies the same underlying principle as Buy, Borrow, Die: allowing assets to grow without triggering a taxable event. The more leveraged strategies (securities-based lines of credit, margin borrowing) carry amplified risk at smaller portfolio sizes and require professional guidance before deployment.Is the 30% housing rule still relevant in 2026?

As a strict spending target, the 30% rule is unachievable for the majority of American households in 2026, particularly in high-cost metropolitan areas where Bankrate's analysis found the typical income-to-housing cost ratio now running at 43%. As a directional principle — that housing costs should not crowd out savings, retirement contributions, and other financial goals — it retains genuine value. Some financial planners now argue the more relevant benchmark is ensuring housing costs leave sufficient disposable income for retirement contributions, emergency savings, and debt service on non-housing obligations, rather than targeting a specific percentage that the current housing market makes impractical for most households.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. Bankrate — The 30% Rule Is Broken: Americans Need 43% of Income for a Median Home (December 2025)

https://www.bankrate.com/mortgages/the-30-percent-housing-rule-is-broken/

2. Moneywise / CardRates — The 30% Rule for Housing Costs Is Ignored by Almost 8 in 10 Americans

https://moneywise.com/real-estate/30-rule-for-housing-costs-is-ignored-by-almost-8-in-10-americans

3. Yahoo Finance — How the Rich Use Debt Differently — and What You Can Learn From It

https://finance.yahoo.com/news/rich-debt-differently-learn-121306178.html

4. BNY Wealth — Adopting a Billionaire Mindset with Borrowing (2026)

https://www.bny.com/wealth/global/en/insights/adopting-a-billionaire-mindset-with-borrowing.html

5. Yahoo Finance — Buy, Borrow, Die: The Strategy Everyone Is Talking About (June 2026)

https://finance.yahoo.com/economy/policy/articles/buy-borrow-die-strategy-everyone-161500661.html

6. Charles Schwab — Leveraging Your Assets to Manage Your Wealth (May 2026)

https://www.schwab.com/learn/story/leveraging-your-assets-to-manage-your-wealth

7. Equifund — 3 Ways to Use Debt to Build Wealth and Avoid Taxes Like the Rich

https://equifund.com/blog/how-to-use-debt-to-build-wealth/

8. Tax Project Institute — Buy, Borrow, Die: What the Wealthy Know That You Don't

https://taxproject.org/buy-borrow-die/

0 Comments Comments