Investing

What Is a Certificate of Deposit? Strategic Guide

Table of Contents

- Why CDs Matter in 2026

- What Is a Certificate of Deposit? The Core Definition

- FDIC and NCUA Insurance: The Safety Foundation

- How CDs Work: The Complete Mechanics

- Interest Calculation and Compounding

- Terms: From 3 Months to 10 Years

- Early Withdrawal Penalties

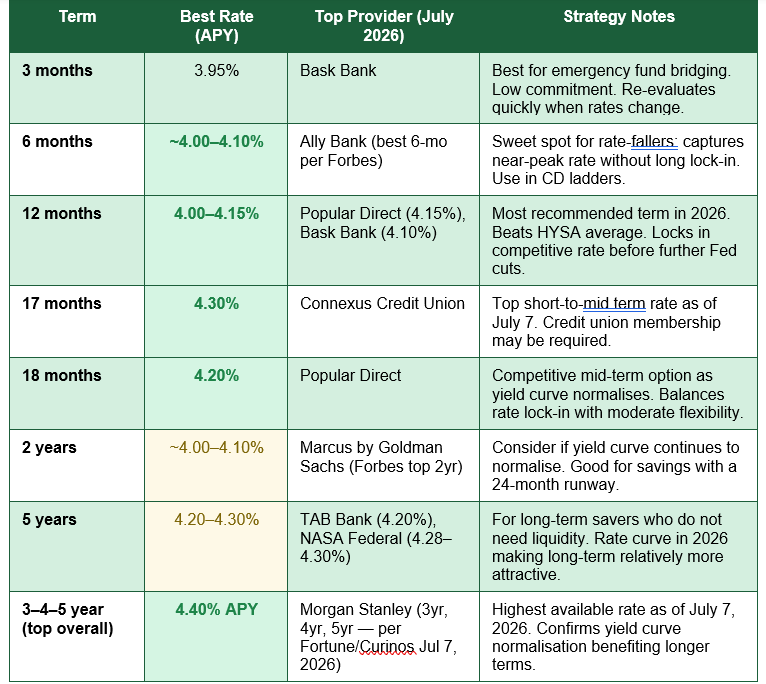

- Best CD Rates Available: July 7, 2026

- Types of CDs: Every Variety Explained

- The CD Ladder Strategy: The Optimal Approach for 2026

- Building a $50,000 CD Ladder: A Worked Example

- Where to Find the Best CD Rates: Online Banks vs Credit Unions vs Big Banks

- CDs vs High-Yield Savings Accounts vs Treasury Bills: The 2026 Comparison

- When CDs Are Not the Right Choice

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why CDs Matter in 2026

A Certificate of Deposit (CD) is one of the simplest and safest financial products available to US savers — and in July 2026, it is also one of the most rewarding. Following three Federal Reserve rate cuts in late 2025, CD rates have declined from their 2023-2024 peaks but remain historically attractive: the best rate available as of July 7, 2026 is 4.40% APY from Morgan Stanley on 3, 4, and 5-year CDs, per Fortune's Curinos data. Connexus Credit Union offers 4.30% APY on a 17-month certificate. The best 1-year CDs hover around 4.00-4.15% APY. All of these rates significantly outpace the national average savings account rate and, when the Fed is pausing or cutting, offer the additional advantage of locking in today's rate against future reductions.The Federal Reserve lowered its benchmark interest rate three times in late 2025 and has kept its rate steady in 2026 — though Bankrate notes that according to CME FedWatch projections, rates may rise later in 2026 depending on macroeconomic factors including inflation, which stood at 3.8% year-over-year as of April 2026. This environment — rates declining but still well above historical norms, with inflation creeping up — creates both an opportunity and a strategic challenge for CD savers. Lock in too short a term and you face reinvestment risk if rates fall further. Lock in too long and you sacrifice liquidity. The CD ladder strategy, which this guide covers in depth, is the primary tool for navigating this trade-off.

Whether you are exploring CDs for the first time, comparing them to high-yield savings accounts and Treasury bills, looking to build a CD ladder, or evaluating specialty products like no-penalty CDs and bump-up CDs, this guide provides the complete strategic framework for getting the most from certificates of deposit in 2026.

What Is a Certificate of Deposit? The Core Definition

A Certificate of Deposit is a time-deposit savings product offered by banks and credit unions in which you agree to deposit a fixed sum of money for a specified period — the term — in exchange for a guaranteed fixed interest rate (the APY, or Annual Percentage Yield). At the end of the term (maturity), you receive your original deposit back plus all the interest earned. If you withdraw your money before maturity, you typically pay an early withdrawal penalty, which in most cases reduces some or all of your earned interest.CDs are not investment products in the securities sense — they carry no market risk and do not fluctuate in value. They are savings products, closely related to a savings account but with two key distinctions: the interest rate is fixed for the full term (regardless of what happens to market rates), and the deposit is locked until maturity. These characteristics make CDs the tool of choice for the portion of a saver's cash that does not need to be immediately accessible and that benefits from certainty of return.

FDIC and NCUA Insurance: The Safety Foundation

All deposits in CDs held at FDIC-insured banks are protected up to $250,000 per depositor, per institution, per account category. CDs at NCUA-insured credit unions carry equivalent protection. This insurance means that even if the bank or credit union fails, your principal and accrued interest up to the coverage limit are guaranteed by the federal government. This makes CDs among the safest financial products available — safer than money market funds, which are not FDIC-insured, and with a more certain return than Treasury bills, which require a secondary market transaction to access before maturity.For savers with more than $250,000 to deposit, the coverage limit can be exceeded by distributing funds across multiple FDIC-insured institutions — each institution provides a separate $250,000 coverage limit for the same ownership category. Joint accounts provide $250,000 per co-owner, effectively doubling coverage for married couples.

How CDs Work: The Complete Mechanics

Interest Calculation and Compounding

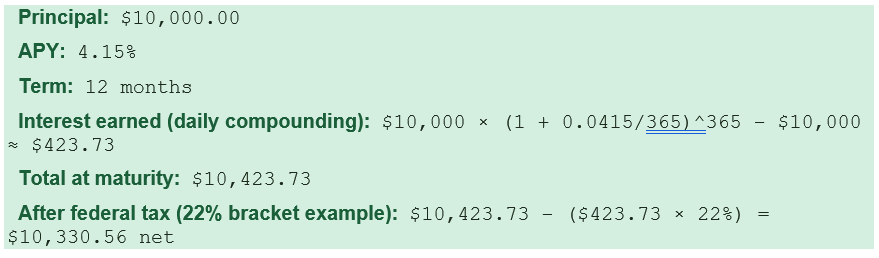

CD interest is quoted as an APY — the Annual Percentage Yield — which reflects the total return including compounding over a 12-month period. Most CDs compound interest daily, which means interest accrues each day based on the principal plus all previously accrued interest. Some compound monthly or quarterly. The more frequent the compounding, the slightly higher the effective yield.The worked example below shows how interest accrues on a $10,000 CD at 4.15% APY for 12 months, compounding daily:

Terms: From 3 Months to 10 Years

CD terms typically range from one month to ten years, with the most commonly offered and most competitively priced terms clustered in the 3-month to 5-year range. The relationship between term length and APY is not always intuitive. In a normal yield curve environment, longer terms pay higher rates. In 2023-2024, the yield curve was inverted — short-term CDs paid more than long-term CDs. Wealthvieu's June 2026 analysis confirms the yield curve is now normalising in 2026: longer-term CDs are becoming relatively more attractive as the gap between short and long rates narrows, with Fortune's July 7, 2026 data showing the top rate of 4.40% at Morgan Stanley on 3, 4, and 5-year CDs — consistent with normalisation.Early Withdrawal Penalties

The price of certainty in a CD is liquidity — and the cost of breaking that contract early is the early withdrawal penalty. These penalties vary by institution and by term but typically range from 90 days of interest for short-term CDs to 12 months of interest for CDs of 5 years or more. Some institutions charge a penalty that can dip into the principal if you withdraw very early in a long-term CD. Before opening any CD, read the specific penalty terms in the account agreement. The penalty should factor into your decision between a standard CD and a no-penalty CD, particularly for funds where near-term access is a possibility.Best CD Rates Available:

The table below reflects the best available CD rates as of July 7, 2026, sourced from NerdWallet, Bankrate, Forbes Advisor, and Fortune/Curinos. Rates change daily — always verify directly with the institution before opening an account:

The rate environment in one sentence: Top rates 4.10–4.40% APY in July 2026 — still well above historical norms and beating 3.8% CPI inflation — the Fed cut three times in late 2025 and has paused in 2026. Inflation at 3.8% YoY (April CPI) means the real return on a top 4.40% CD is approximately +0.6% before tax — positive but narrowing. Act before further cuts reduce available rates (Bankrate / Fortune / NerdWallet, July 7, 2026).

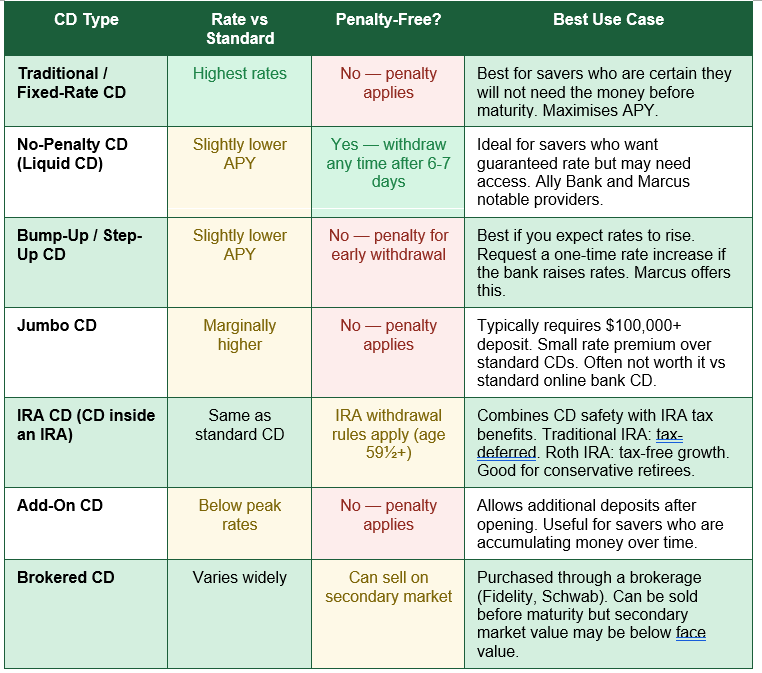

Types of CDs: Every Variety Explained

The market for CDs in 2026 includes several distinct product types, each designed for different savers and different strategic needs. Understanding which type suits your situation is as important as finding the best rate:

No-penalty CDs vs High-Yield Savings Accounts in 2026: No-penalty CDs typically offer slightly lower APYs than comparable standard CDs but remove the liquidity constraint. In July 2026, the best no-penalty CDs offer around 4.00-4.10% APY, while competitive high-yield savings accounts (HYSAs) offer 4.00-5.00% APY — but HYSA rates are variable and track Fed movements. If the Fed cuts rates again in 2026, a no-penalty CD at a fixed 4.00% outperforms a HYSA that falls to 3.50%. The CD locks in the rate; the HYSA follows it down.

The CD Ladder Strategy: The Optimal Approach for 2026

A CD ladder is a savings strategy in which you divide your total investment across multiple CDs with different maturity dates, rather than placing everything in a single CD of one term. The result is a portfolio that provides regular access to maturing funds, reduces the risk of being locked out of rising rates, and — when rates are falling — captures today's rates on a portion of your savings while maintaining flexibility through the other rungs.The classic CD ladder divides a lump sum equally across five CDs — for example, one each of 1-year, 2-year, 3-year, 4-year, and 5-year terms. When the 1-year CD matures, you reinvest it into a new 5-year CD, again at whatever the best available rate is at that point. After the initial setup period, you end up with a CD maturing every year, giving you annual access to a portion of your savings while always holding some money in longer-term, higher-rate CDs.

In 2026, Wealthvieu's rate forecast analysis describes the CD ladder as 'the most prudent strategy when the rate outlook is uncertain — it gives you regular maturity dates to reinvest at whatever rate is available, while keeping a portion locked in at today's higher rates.' The normalising yield curve reinforces this: with 5-year CDs now paying more than 1-year CDs again (unlike 2023-2024 when the curve was inverted), the ladder fully captures rate premiums across the term spectrum.

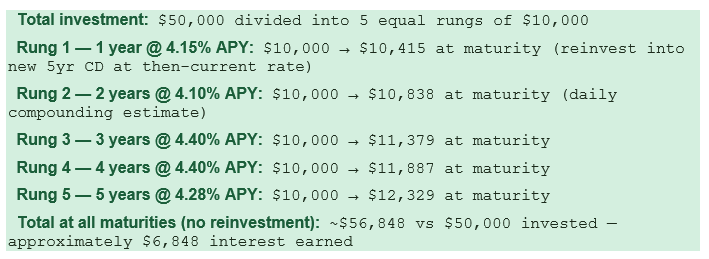

Building a $50,000 CD Ladder: A Worked Example

The following example constructs a $50,000 CD ladder using the best available rates as of July 2026 and illustrates the annual maturities and projected returns:

Where to Find the Best CD Rates: Online Banks vs Credit Unions vs Big Banks

One of the most consistent and well-documented findings in the CD market is the significant gap between rates offered by online banks and credit unions versus traditional brick-and-mortar banks. Fortune's July 7, 2026 analysis notes directly that 'online banks can typically offer better rates than financial institutions with physical branches — largely due to digital-only banks and credit unions not having the overhead that comes with maintaining branches, allowing them to pass their savings on to customers in the form of better interest rates.'The difference is not marginal. The national average CD rate for 1-year CDs is well below the best available rate from online institutions. A saver who opens a CD at a traditional brick-and-mortar bank may earn 0.5-1.0% APY, while the same saver could earn 4.00-4.15% APY at an online bank — a difference of $350 to $365 per year on a $10,000 CD. Over five years of reinvesting at these respective rates, the compounding difference becomes thousands of dollars.

The practical implication: always compare online banks and credit unions before accepting a CD offer from your primary bank. NerdWallet, Bankrate, and Forbes Advisor all maintain live, updated rate comparison tools that show the best rates nationally by term length, updated daily.

- Online banks: Typically the most competitive rates. No minimum deposit at some (Ally, Marcus, Synchrony). Fully FDIC-insured. Best current examples include Ally Bank, Synchrony Bank, Marcus by Goldman Sachs, Popular Direct, and Bask Bank.

- Credit unions: Often among the highest rates available, particularly for non-standard terms. Require membership, which is typically easy to obtain. NCUA-insured to $250,000. Connexus Credit Union (4.30% on 17 months) and NASA Federal Credit Union (4.30% on 49 months) are current examples.

- Traditional banks: Lowest rates across the spectrum. The convenience of having your CD at your primary bank is almost never worth the rate sacrifice. Always compare externally.

CDs vs High-Yield Savings Accounts vs Treasury Bills: The 2026 Comparison

Savers with short-to-medium-term cash face three main high-safety options in 2026: CDs, high-yield savings accounts (HYSAs), and US Treasury bills. Understanding the trade-offs between them determines which is right for a given amount and timeline:- Certificates of Deposit: Fixed rate for the full term. Best when you want rate certainty and can commit the money for the full period. Currently offering 4.00-4.40% APY at top institutions. Early withdrawal penalty if you need access. FDIC insured to $250,000. Best choice when Fed rate cuts are expected — locks in today's rate.

- High-Yield Savings Accounts: Variable rate that adjusts with Fed moves. Top HYSAs in July 2026 offer 4.00-5.00% APY. No lock-in — full liquidity at all times. Best for emergency funds and money you may need at short notice. If the Fed cuts further, HYSA rates fall with it.

- US Treasury Bills: Short-term government debt (4-week to 52-week). Currently yielding approximately 4.2-4.4% (July 2026 estimates). Interest is exempt from state and local income tax, which makes T-bills particularly attractive in high-tax states. Purchased through TreasuryDirect.gov. No FDIC insurance needed — backed by the full faith and credit of the US government.

The state tax advantage of Treasury bills: CD interest is subject to federal, state, and local income tax. Treasury bill interest is exempt from state and local income tax. For savers in high-tax states — California (up to 13.3%), New York City, New Jersey — the after-tax return from T-bills can meaningfully exceed the after-tax return from an equivalent-rate CD. Always calculate the after-tax return for your specific state and local tax situation when comparing these two products.

When CDs Are Not the Right Choice

CDs are genuinely excellent tools for the right money in the right situation, but understanding when they are not appropriate is equally important. Several situations call for a different approach:- Emergency fund: Your emergency fund — typically 3-6 months of living expenses — should be in a fully liquid account. An HYSA or money market account is the right home for this money, not a CD with an early withdrawal penalty. Only allocate money to a CD that you are genuinely comfortable not accessing for the full term.

- Long-term wealth building (5+ year horizon): Wealthvieu's rate forecast analysis states directly that investors with a 5+ year horizon should consider whether diversified index funds might outperform a CD over that period. Historically, stock market returns have significantly exceeded CD rates over multi-decade periods. CDs beat the market for safety — not for long-term growth.

- When rates are expected to rise significantly: If the Fed signals rate increases, locking into a long-term CD at today's rate could mean missing better rates available in six or twelve months. In a rising rate environment, shorter-term CDs or no-penalty CDs provide flexibility to reinvest at higher rates.

Conclusion

A Certificate of Deposit in July 2026 is one of the most straightforward high-value decisions available to US savers: guaranteed returns of up to 4.40% APY, FDIC insurance to $250,000, and a fixed rate that will not decline regardless of what the Federal Reserve does next. Following three Fed rate cuts in late 2025 and a pause in 2026, today's CD rates remain well above historical norms — and the normalising yield curve means longer-term CDs are now offering rates competitive with or exceeding shorter terms, restoring the classic incentive to lock in further out.The strategic choice in 2026 is not whether to use CDs — for most savers with medium-term savings they do not need immediate access to, the answer is clearly yes. The choice is which type, which term, and how to structure them. The CD ladder provides the optimal balance of rate capture and liquidity. Online banks and credit unions provide the highest rates, often by 300-400 basis points over traditional branches. No-penalty CDs provide a hedge against unexpected liquidity needs at a modest rate cost. And for savers in high-tax states, the state income tax exemption on Treasury bills makes a direct comparison worthwhile before choosing a CD.

The one discipline that matters most across every CD strategy is this: never default to your existing bank. The difference between the national average CD rate and the best available online rate is often 3 percentage points or more — the equivalent of hundreds of dollars per year on a modest $10,000 deposit, compounding year over year across a ladder. Shop the market, use the comparison tools, and put your savings where they earn the most. That is the entire strategic principle behind getting the most from a certificate of deposit in 2026.

Frequently Asked Questions (FAQ)

What is the best CD rate available right now (July 2026)?

As of July 7, 2026, the highest available CD rate is 4.40% APY from Morgan Stanley on 3-year, 4-year, and 5-year CDs, per Fortune's Curinos data. Among shorter-term options, Connexus Credit Union offers 4.30% APY on a 17-month certificate, and Popular Direct offers 4.15% on a 12-month CD. NerdWallet reports Connexus Credit Union and NASA Federal Credit Union at 4.30% APY on longer specialty terms. Rates change daily — always verify directly with the institution and compare on NerdWallet, Bankrate, or Forbes Advisor before opening an account.How does a CD differ from a regular savings account?

A savings account offers a variable interest rate that the bank can change at any time, and full liquidity — you can deposit or withdraw whenever you want. A CD offers a fixed interest rate guaranteed for the full term, but restricts access to your funds until maturity — early withdrawal incurs a penalty. The trade-off is predictability of return (CD) versus flexibility (savings account). In a falling rate environment, the CD's fixed rate becomes more valuable, because a savings account rate will fall with the Fed while the CD stays the same. In a rising rate environment, the savings account benefits from rising rates while the CD remains locked at the lower original rate.What is a CD ladder and should I use one?

A CD ladder divides your total CD investment across multiple certificates with different maturity dates — typically annual increments from 1 year to 5 years. When each CD matures, you reinvest it into a new 5-year CD. The strategy provides regular access to a portion of your savings each year, while maintaining exposure to longer-term, higher-rate CDs at all times. It also reduces reinvestment risk: rather than having all your money mature at once (when rates might be low), you spread maturities across the rate cycle. In 2026 — with rates declining but uncertain — the CD ladder is the approach recommended by Wealthvieu, Bankrate's Senior Economic Analyst, and most rate-cycle analysis. Yes, for most savers with $5,000 or more to allocate to CDs, a ladder is the optimal structure.Are CDs safe? What happens if the bank fails?

CDs held at FDIC-insured banks are safe up to $250,000 per depositor per institution per account ownership category. If the bank fails, the FDIC pays your principal plus all accrued interest up to that limit, typically within a few business days. CDs at NCUA-insured credit unions carry equivalent protection. This makes CDs among the safest financial products available — the only product with comparable safety and no market risk. For deposits above $250,000, you can maintain full coverage by spreading CDs across multiple FDIC-insured institutions, each providing a separate $250,000 coverage limit.Is CD interest taxable?

Yes — CD interest is taxable as ordinary income at the federal level and, in most states, at the state and local level as well. You owe tax on CD interest in the year it is received, not just when the CD matures — for multi-year CDs, this means you may owe tax on interest each year even before you can access it, depending on the bank's reporting structure. The bank will send you a Form 1099-INT reporting your interest income annually. This tax treatment is one key reason to compare CDs against Treasury bills, which are exempt from state and local income tax — making T-bills more tax-efficient in high-tax states despite potentially similar pre-tax rates. Holding CDs within a Traditional or Roth IRA defers or eliminates this tax obligation, depending on the IRA type.External References

The following authoritative sources were used in researching this article and are recommended for further reading and live rate comparisons:1. NerdWallet — Best CD Rates of July 2026 (Updated July 6, 2026)

https://www.nerdwallet.com/banking/best/cd-rates

2. Bankrate — Current CD Rates for July 7, 2026 (Daily tracking, hundreds of institutions)

https://www.bankrate.com/banking/cds/current-cd-interest-rates/

3. Forbes Advisor — Best CD Rates of July 2026 (Analysis of 458 CDs from 148 institutions)

https://www.forbes.com/advisor/banking/cds/best-cd-rates/

4. Fortune — Top CD Rates Tuesday July 7, 2026 (Curinos data)

https://fortune.com/article/cd-rates-7-7-26/

5. Wealthvieu — CD Rate Forecast 2026: Where Rates Are Headed (Updated May 2026)

https://wealthvieu.com/cd-rate-forecast/

6. CNBC Select — 13 Best CD Rates of July 2026 (Updated July 2026)

https://www.cnbc.com/select/best-certificates-of-deposits/

7. FDIC — Deposit Insurance: How Your Accounts Are Protected

https://www.fdic.gov/deposit/deposits/

8. TreasuryDirect — Buy Treasury Bills Direct from the US Government

https://www.treasurydirect.gov/

0 Comments Comments