Investing

Investment Accounts to Prioritise When You Have a Baby

A baby born today has eighteen years before they need money for education or independence, and potentially fifty years before retirement. That time is the most valuable financial asset they will ever have — but only if it is put to work in the right accounts. This guide covers every major investment account available to new parents in the UK and US in 2026, explains the specific advantages of each, and gives you the sequencing framework for opening them in the right order.

A child born today and invested for from birth has something that no adult investor can ever recover: time. At a 7% average annual real return — the long-run historical average of broad stock market index funds — a single £100 or $100 invested at birth grows to approximately £762 or $762 by the child's eighteenth birthday. The same £100 invested at age ten grows to only £338 by their eighteenth birthday. The difference is not the amount invested. It is the number of years available for compound growth.

Stretched to retirement age, the numbers become staggering. £5,000 invested at birth in a broadly diversified index fund grows to approximately £270,000 by age 65 at 7% real returns — all from a single one-off investment. The same £5,000 invested at age 30 grows to only £52,000 by age 65. This is the compounding argument for why the accounts you open in the first year of a child's life are among the most consequential financial decisions you will ever make for them.

The accounts themselves — 529 plans, Junior ISAs, custodial Roth IRAs, Trump Accounts, UGMA/UTMA accounts — are simply the vessels through which this compounding happens. Each has different tax treatment, different contribution limits, different withdrawal rules, and different flexibility. Choosing the right combination and opening them in the right order determines how much of the available compound growth your child actually captures.

Parents are increasingly recognising the importance of early financial education. Investment accounts for children have emerged as vital tools for parents devoted to securing their children's financial futures — with Junior ISAs gaining traction for their tax benefits and 529 Plans continuing to be a top choice for families focused on funding higher education.

— BRIGHT ADVISERS — INVESTMENT ACCOUNTS FOR CHILDREN: COMPARING JUNIOR ISAS, CUSTODIAL ACCOUNTS, AND 529 PLANS

Your baby's financial future is best served by parents who are financially secure — not by parents who have sacrificed their own retirement savings to overfund a child's education account. The investment hierarchy for new parents, in order, is: (1) ensure you have a three-to-six-month emergency fund in a high-yield savings account; (2) contribute at least to the employer match on your 401(k) or workplace pension — this is a guaranteed 50% to 100% immediate return; (3) maximise your own tax-advantaged retirement accounts (Roth IRA at $7,500 limit in 2026, or Stocks and Shares ISA at £20,000 in 2026/27); (4) only then direct surplus funds to child investment accounts.

FH Associates' March 2026 investment account guide puts this parent-first principle succinctly: 'Education as the primary focus: make a 529 plan the core education vehicle — but only after your own retirement savings are on track.' This is not a failure of parental generosity. It is a recognition that you cannot fund your child's future from a financially insecure position, and that your own retirement security is itself a form of providing for your child — reducing the likelihood that they will need to support you financially in your old age.

* 529 and UGMA/UTMA contributions are subject to gift tax rules above $19,000/year per person in 2026 (annual gift tax exclusion). Sources: NerdWallet May 2026, Which? 2026/27, CNBC Select May 2026, Bankrate 2026, GOV.UK, MoneyHelper.

NerdWallet's May 2026 guide explains the investment mechanism: '529 accounts come with a curated list of investment options, such as target-date funds, which are mutual funds that automatically adjust how much risk they take as the target date approaches — in this case, that date is your child's college age.' This automatic risk adjustment is a significant operational advantage for new parents who do not want to actively manage investment allocation over eighteen years.

Several states offer an additional state income tax deduction on 529 contributions — making contributions up to the deductible limit particularly high-value in those states. The contribution limits are governed by federal gift tax rules rather than annual IRA-style limits: contributions are treated as gifts, with the annual gift tax exclusion of $19,000 per person per year in 2026 applying. A unique 529 'superfunding' provision allows front-loading up to five years of annual gift tax exclusions ($95,000 per person, or $190,000 per couple) into a 529 in a single year without gift tax implications.

A notable 2024 rule change expanded 529 flexibility significantly: unused 529 balances can now be rolled over to a Roth IRA in the child's name, subject to annual IRA contribution limits and a 15-year account seasoning requirement. This addresses the primary historical objection to 529 plans — the risk that the child does not attend college — by providing a meaningful retirement savings fallback for unused education funds.

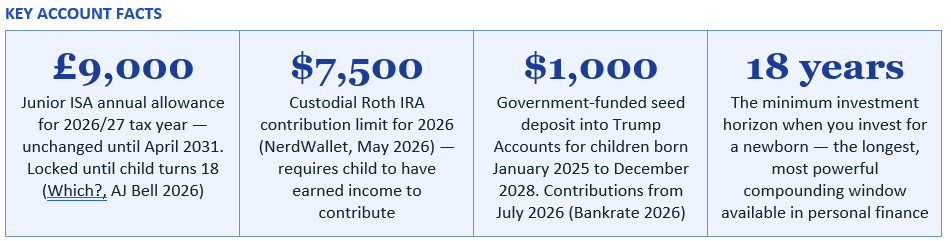

Starting in July 2026, parents and employers can begin making contributions to these accounts. The annual contribution limits are $5,000 per year from individuals and $2,500 from employers until the child turns 18. After age 18, annual contributions can go up to the standard IRA limit ($7,000 as of 2025). FH Associates' March 2026 guide describes their positioning: 'A capped starter wealth-building vehicle to capture federal seed funding and possible employer/philanthropic contributions, typically used alongside 529s, Roth IRAs, and other accounts rather than as the sole savings vehicle.'

For parents of children born in the qualifying window, the Trump Account represents an exceptional baseline: a $1,000 government seed deposit in a stock index fund at birth, with the ability to add up to $5,000 per year from July 2026. At a 7% real annual return over 18 years, the $1,000 government seed alone grows to approximately $3,380 by the child's 18th birthday without any further contribution. With annual $5,000 parental contributions beginning from age one, the account could reach approximately $170,000 at 18 — a meaningful head-start on education or early adult financial independence.

CNBC Select's May 2026 guide explains the tax structure: 'Custodial Roth IRAs behave similarly to your traditional Roth IRA — contributions are made post-tax, there is tax-free growth, and contributions (not investment gains) can be withdrawn at any time, penalty- and tax-free.' NerdWallet's May 2026 guide confirms: 'The contribution limit for 2026 is $7,500. Eligibility: the child must have earned income. This can be from a part-time job such as babysitting, raking leaves, etc.'

The compounding mathematics of a Roth IRA opened at age 14 or 15 with modest earned income contributions are extraordinary. $2,000 contributed per year from age 14 to 18 ($10,000 total) invested in a broad index fund at 7% real annual return grows to approximately $256,000 by age 65 — with all growth completely tax-free. The parent who helps their teenager open a Roth IRA with the first income they ever earn is giving them a financial asset that will compound tax-free for approximately fifty years.

FH Associates' March 2026 guide identifies the key use case: 'Broad flexibility (car, first apartment, business seed money): consider a custodial account or an adult-owned brokerage account, weighing ownership, control, and tax rates.' The flexibility is genuinely differentiated — a 529 penalises non-educational withdrawals with tax and a 10% penalty, while a UGMA/UTMA account has no such restriction.

The trade-off is tax treatment. UGMA/UTMA accounts are taxable rather than tax-advantaged. Investment income is subject to the Kiddie Tax rules: for tax year 2025, CNBC Select explains that 'if your child has no earned income and their investment income is less than $1,350, it is not taxed. If it exceeds $2,900, the excess is taxed at the parents' rate.' For the long-term compound growth potential of an account held from birth to adulthood, the tax drag of a UGMA/UTMA account over a 529 or Roth IRA is real and meaningful. UGMA/UTMA accounts are best used as a complement to tax-advantaged accounts — providing flexibility for non-education goals after the tax-advantaged options are maximised.

MoneyHelper's official guidance confirms: 'The £9,000 limit is separate from, and in addition to, the adult ISA allowance (£20,000 in 2026/27). With a Junior Stocks and Shares ISA, you can put your child's savings into investments like funds, shares and bonds. Any profits you earn from investing are free from tax.' The accounts are parent-opened (children under 16 cannot open their own) but anyone — parents, grandparents, aunts and uncles, friends — can contribute up to the £9,000 annual limit without affecting their own ISA allowance.

For a Junior ISA, the Stocks and Shares variant almost always outperforms the Cash variant over an 18-year investment horizon. Hargreaves Lansdown, Which?, and AJ Bell all emphasise this distinction: 'Investing for 5+ years increases your chances of positive returns compared to cash savings.' Over 18 years, the difference between a cash Junior ISA earning 4% and a Stocks and Shares Junior ISA earning 7% on the same £100/month contribution is approximately £37,000 — a significant gap that compounds in favour of equities over the long horizon available when investing from birth.

Key operational points for the Junior ISA: the money belongs to the child from the moment it is deposited; the child takes control of the account at 16 (but cannot withdraw until 18); the account converts automatically to an adult ISA when the child turns 18; and any unused annual allowance is lost at the end of the tax year and cannot be carried forward.

AJ Bell's Junior ISA guide notes the pension option: 'Kick-start their pension with our hands-on, self-invested account with an annual investment allowance of £3,600.' The tax relief mechanism means the government effectively adds 25% to every contribution a parent makes — £2,880 contributed becomes £3,600 in the pension, immediately. That 25% uplift is a guaranteed immediate return before any investment growth occurs.

The compounding mathematics over a lifetime are extraordinary. £3,600 per year contributed from birth to age 18 (a total of £64,800 gross, or £51,840 out of pocket after tax relief) invested at 5% annual real return, then untouched from age 18 to 57, grows to approximately £780,000 at retirement. The child would enter adulthood with a pension fund on track for significant retirement wealth — funded by contributions made decades before they entered the workforce.

The critical constraint is that pension funds are locked until age 57 under current UK rules, making the Junior SIPP entirely unsuitable as a vehicle for education or early adult expenses. It is a pure retirement-building tool — the most powerful one available, but only relevant as a supplement to education-focused accounts (the Junior ISA) rather than a replacement for them.

The key structural difference from the Junior ISA is ownership and control: money in a Junior ISA belongs irrevocably to the child and can only be accessed by them from age 18. Money in an adult ISA earmarked for a child belongs to the parent and can be accessed or redirected if circumstances change — if the child decides not to attend university, if a family emergency requires the funds, or if you want to make a conditional gift rather than an unconditional one.

For parents who are already maximising their own pension contributions and 401(k) equivalent, and whose Junior ISA allowance is already being fully used, the adult ISA earmarked strategy provides an overflow channel. The tax treatment is identical — no income tax or capital gains tax within the ISA wrapper — and the investment options are as wide as the Junior ISA's.

The reasoning is straightforward. Over 18-year periods, passive index funds that track the global or US stock market have consistently outperformed the majority of actively managed funds after fees. The cost of active management — typically 0.75% to 1.5% annual charges versus 0.10% to 0.20% for the best index funds — compounds dramatically over 18 years. On a £9,000/year contribution, the difference in charges between a 0.15% and a 1.0% fund amounts to tens of thousands of pounds of additional cost over the full investment horizon.

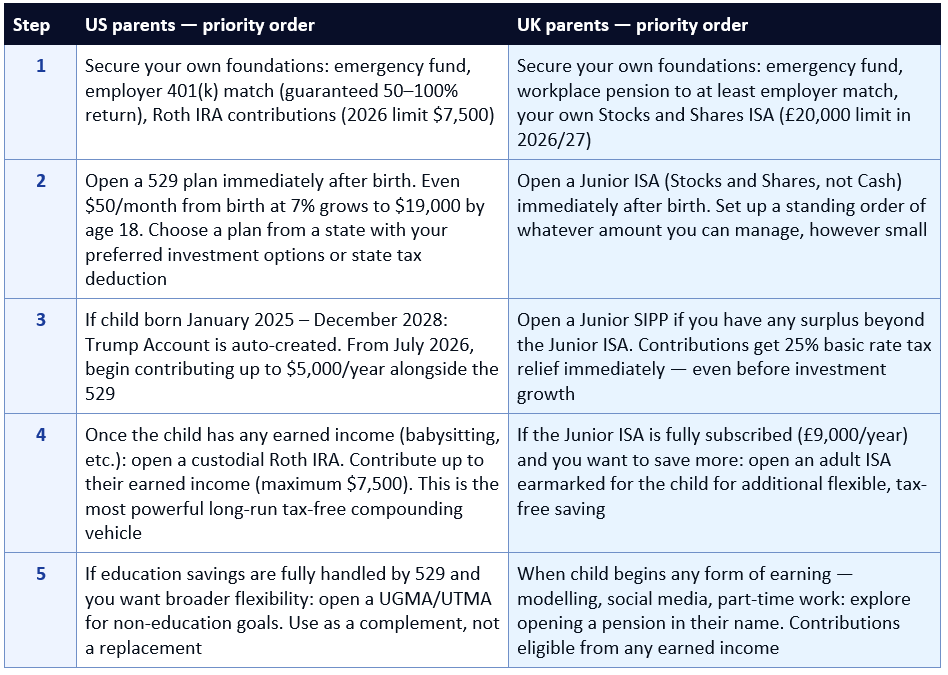

The sequencing principle is clear: your own financial foundations first, then the child's accounts, prioritised by tax efficiency. For US parents, open a 529 immediately and ensure any child born between 2025 and 2028 has their Trump Account in place from July 2026. For UK parents, open a Stocks and Shares Junior ISA from birth and consider a Junior SIPP if there is surplus beyond the JISA. In both countries, the custodial Roth IRA or equivalent pension contribution becomes available when the child earns their first income — and that moment is when the most powerful long-run compounding vehicle opens.

CNBC Select — 6 Best Investment Accounts for Kids in May 2026 https://www.cnbc.com/select/best-investment-accounts-for-kids/

FH Associates — Investment Accounts for Kids: Five Common Choices and How to Pick the Right One (March 2026) https://fhassoc.com/investment-accounts-for-kids-five-common-choices-how-to-pick-the-right-one/

Bankrate — 7 Investments to Set Your Kids Up for Life: Including Trump Accounts (2026) https://www.bankrate.com/investing/7-investments-to-set-your-kids-up-for-life/

Which? — Best Junior ISA Rates 2026: Rules and Top Picks (May 2026) https://www.which.co.uk/money/savings-and-isas/isas/best-junior-cash-isas-aTblN9u99wlN

MoneyHelper — Junior ISAs: Official UK Guidance https://www.moneyhelper.org.uk/en/savings/types-of-savings/junior-isas

AJ Bell — Junior ISA Allowance 2026/27: Rules Explained (April 2026) https://www.ajbell.co.uk/isa/junior-isa/allowance

GOV.UK — Junior Individual Savings Accounts (ISA): Official Overview https://www.gov.uk/junior-individual-savings-accounts

Hargreaves Lansdown — Junior ISA Allowance 2026/27 https://www.hl.co.uk/investment-services/junior-isa/junior-isa-allowance

TABLE OF CONTENTS

- Why the Day a Baby Is Born Is the Best Investment Day of Their Life

- Before You Open Any Child Account: Your Priorities Come First

- The Full Comparison: Every Account Side-by-Side (US and UK)

- US Account 1: The 529 Education Savings Plan

- US Account 2: Trump Accounts — The New Government-Seeded Account (2025–2028 births)

- US Account 3: Custodial Roth IRA

- US Account 4: UGMA and UTMA Custodial Accounts

- UK Account 1: Junior ISA (JISA) — Stocks and Shares

- UK Account 2: Junior SIPP — Starting a Pension at Birth

- UK Account 3: An Adult Stocks and Shares ISA Earmarked for the Child

- The Sequencing: Which Account to Open First, Second, and Third

- What to Invest in Once the Accounts Are Open

- Conclusion

- Frequently Asked Questions

- References

Why the Day a Baby Is Born Is the Best Investment Day of Their Life

A child born today and invested for from birth has something that no adult investor can ever recover: time. At a 7% average annual real return — the long-run historical average of broad stock market index funds — a single £100 or $100 invested at birth grows to approximately £762 or $762 by the child's eighteenth birthday. The same £100 invested at age ten grows to only £338 by their eighteenth birthday. The difference is not the amount invested. It is the number of years available for compound growth.Stretched to retirement age, the numbers become staggering. £5,000 invested at birth in a broadly diversified index fund grows to approximately £270,000 by age 65 at 7% real returns — all from a single one-off investment. The same £5,000 invested at age 30 grows to only £52,000 by age 65. This is the compounding argument for why the accounts you open in the first year of a child's life are among the most consequential financial decisions you will ever make for them.

The accounts themselves — 529 plans, Junior ISAs, custodial Roth IRAs, Trump Accounts, UGMA/UTMA accounts — are simply the vessels through which this compounding happens. Each has different tax treatment, different contribution limits, different withdrawal rules, and different flexibility. Choosing the right combination and opening them in the right order determines how much of the available compound growth your child actually captures.

Parents are increasingly recognising the importance of early financial education. Investment accounts for children have emerged as vital tools for parents devoted to securing their children's financial futures — with Junior ISAs gaining traction for their tax benefits and 529 Plans continuing to be a top choice for families focused on funding higher education.

— BRIGHT ADVISERS — INVESTMENT ACCOUNTS FOR CHILDREN: COMPARING JUNIOR ISAS, CUSTODIAL ACCOUNTS, AND 529 PLANS

Before You Open Any Child Account: Your Priorities Come First

This is the most important section of this guide, and the one most likely to be skipped in the excitement of new parenthood. Before you open a single investment account in your baby's name, your own financial foundations must be in place. The sequencing matters enormously.Your baby's financial future is best served by parents who are financially secure — not by parents who have sacrificed their own retirement savings to overfund a child's education account. The investment hierarchy for new parents, in order, is: (1) ensure you have a three-to-six-month emergency fund in a high-yield savings account; (2) contribute at least to the employer match on your 401(k) or workplace pension — this is a guaranteed 50% to 100% immediate return; (3) maximise your own tax-advantaged retirement accounts (Roth IRA at $7,500 limit in 2026, or Stocks and Shares ISA at £20,000 in 2026/27); (4) only then direct surplus funds to child investment accounts.

FH Associates' March 2026 investment account guide puts this parent-first principle succinctly: 'Education as the primary focus: make a 529 plan the core education vehicle — but only after your own retirement savings are on track.' This is not a failure of parental generosity. It is a recognition that you cannot fund your child's future from a financially insecure position, and that your own retirement security is itself a form of providing for your child — reducing the likelihood that they will need to support you financially in your old age.

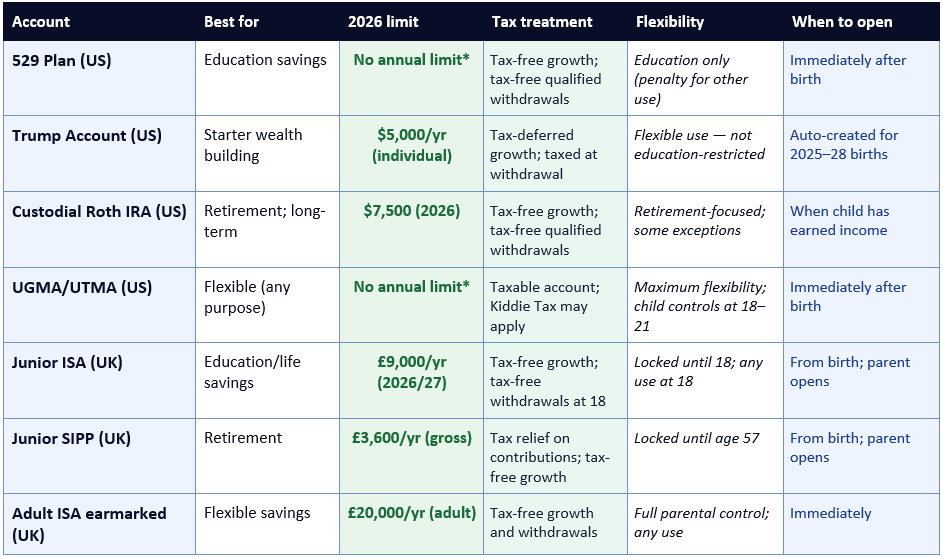

The Full Comparison: Every Account Side-by-Side (US and UK)

* 529 and UGMA/UTMA contributions are subject to gift tax rules above $19,000/year per person in 2026 (annual gift tax exclusion). Sources: NerdWallet May 2026, Which? 2026/27, CNBC Select May 2026, Bankrate 2026, GOV.UK, MoneyHelper.

US Account 1: The 529 Education Savings Plan

For US parents focused on funding higher education, the 529 plan is the first account to open — ideally within the first few months of birth. A 529 is a state-sponsored, tax-advantaged savings plan specifically designed for education expenses. Contributions grow tax-free and withdrawals for qualified education expenses (tuition, fees, books, room and board) are tax-free at the federal level and in most states.NerdWallet's May 2026 guide explains the investment mechanism: '529 accounts come with a curated list of investment options, such as target-date funds, which are mutual funds that automatically adjust how much risk they take as the target date approaches — in this case, that date is your child's college age.' This automatic risk adjustment is a significant operational advantage for new parents who do not want to actively manage investment allocation over eighteen years.

Several states offer an additional state income tax deduction on 529 contributions — making contributions up to the deductible limit particularly high-value in those states. The contribution limits are governed by federal gift tax rules rather than annual IRA-style limits: contributions are treated as gifts, with the annual gift tax exclusion of $19,000 per person per year in 2026 applying. A unique 529 'superfunding' provision allows front-loading up to five years of annual gift tax exclusions ($95,000 per person, or $190,000 per couple) into a 529 in a single year without gift tax implications.

A notable 2024 rule change expanded 529 flexibility significantly: unused 529 balances can now be rolled over to a Roth IRA in the child's name, subject to annual IRA contribution limits and a 15-year account seasoning requirement. This addresses the primary historical objection to 529 plans — the risk that the child does not attend college — by providing a meaningful retirement savings fallback for unused education funds.

US Account 2: Trump Accounts — The New Government-Seeded Account (2025–2028 births)

Trump Accounts — formally established under the One Big Beautiful Bill Act — are a new government-backed investment account created specifically for children born between January 1, 2025, and December 31, 2028. Bankrate's 2026 coverage explains the key features: children in this birth window will automatically receive a Trump Account with a $1,000 government-funded deposit invested in a stock index fund. No action is required by parents.Starting in July 2026, parents and employers can begin making contributions to these accounts. The annual contribution limits are $5,000 per year from individuals and $2,500 from employers until the child turns 18. After age 18, annual contributions can go up to the standard IRA limit ($7,000 as of 2025). FH Associates' March 2026 guide describes their positioning: 'A capped starter wealth-building vehicle to capture federal seed funding and possible employer/philanthropic contributions, typically used alongside 529s, Roth IRAs, and other accounts rather than as the sole savings vehicle.'

For parents of children born in the qualifying window, the Trump Account represents an exceptional baseline: a $1,000 government seed deposit in a stock index fund at birth, with the ability to add up to $5,000 per year from July 2026. At a 7% real annual return over 18 years, the $1,000 government seed alone grows to approximately $3,380 by the child's 18th birthday without any further contribution. With annual $5,000 parental contributions beginning from age one, the account could reach approximately $170,000 at 18 — a meaningful head-start on education or early adult financial independence.

US Account 3: Custodial Roth IRA

The custodial Roth IRA is the most powerful long-term wealth-building account available for children — but it comes with a critical eligibility requirement: the child must have earned income. A baby or young child with no earned income cannot contribute. However, once a child begins earning money from any legitimate work — babysitting, lawn mowing, modelling, social media content, or any other self-employment or W-2 income — a Roth IRA contribution up to the lesser of earned income or the annual IRA limit becomes available.CNBC Select's May 2026 guide explains the tax structure: 'Custodial Roth IRAs behave similarly to your traditional Roth IRA — contributions are made post-tax, there is tax-free growth, and contributions (not investment gains) can be withdrawn at any time, penalty- and tax-free.' NerdWallet's May 2026 guide confirms: 'The contribution limit for 2026 is $7,500. Eligibility: the child must have earned income. This can be from a part-time job such as babysitting, raking leaves, etc.'

The compounding mathematics of a Roth IRA opened at age 14 or 15 with modest earned income contributions are extraordinary. $2,000 contributed per year from age 14 to 18 ($10,000 total) invested in a broad index fund at 7% real annual return grows to approximately $256,000 by age 65 — with all growth completely tax-free. The parent who helps their teenager open a Roth IRA with the first income they ever earn is giving them a financial asset that will compound tax-free for approximately fifty years.

US Account 4: UGMA and UTMA Custodial Accounts

A Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) custodial account is a taxable investment account legally owned by the child, with an adult custodian managing the account until the child reaches the age of majority (typically 18 or 21 depending on the state). Unlike 529 plans, there are no restrictions on what the money can be used for — it can fund education, a car, a first apartment, a business, or anything else.FH Associates' March 2026 guide identifies the key use case: 'Broad flexibility (car, first apartment, business seed money): consider a custodial account or an adult-owned brokerage account, weighing ownership, control, and tax rates.' The flexibility is genuinely differentiated — a 529 penalises non-educational withdrawals with tax and a 10% penalty, while a UGMA/UTMA account has no such restriction.

The trade-off is tax treatment. UGMA/UTMA accounts are taxable rather than tax-advantaged. Investment income is subject to the Kiddie Tax rules: for tax year 2025, CNBC Select explains that 'if your child has no earned income and their investment income is less than $1,350, it is not taxed. If it exceeds $2,900, the excess is taxed at the parents' rate.' For the long-term compound growth potential of an account held from birth to adulthood, the tax drag of a UGMA/UTMA account over a 529 or Roth IRA is real and meaningful. UGMA/UTMA accounts are best used as a complement to tax-advantaged accounts — providing flexibility for non-education goals after the tax-advantaged options are maximised.

UK Account 1: Junior ISA (JISA) — Stocks and Shares

The Junior ISA is the UK's primary tax-advantaged investment account for children and the first account most UK parents should open for a new baby. The 2026/27 Junior ISA allowance is £9,000 per child per tax year, unchanged from 2025/26 and confirmed as fixed until April 2031 by Which?'s May 2026 analysis. Contributions grow entirely free of UK income tax and capital gains tax, and the money can be withdrawn tax-free when the child turns 18.MoneyHelper's official guidance confirms: 'The £9,000 limit is separate from, and in addition to, the adult ISA allowance (£20,000 in 2026/27). With a Junior Stocks and Shares ISA, you can put your child's savings into investments like funds, shares and bonds. Any profits you earn from investing are free from tax.' The accounts are parent-opened (children under 16 cannot open their own) but anyone — parents, grandparents, aunts and uncles, friends — can contribute up to the £9,000 annual limit without affecting their own ISA allowance.

For a Junior ISA, the Stocks and Shares variant almost always outperforms the Cash variant over an 18-year investment horizon. Hargreaves Lansdown, Which?, and AJ Bell all emphasise this distinction: 'Investing for 5+ years increases your chances of positive returns compared to cash savings.' Over 18 years, the difference between a cash Junior ISA earning 4% and a Stocks and Shares Junior ISA earning 7% on the same £100/month contribution is approximately £37,000 — a significant gap that compounds in favour of equities over the long horizon available when investing from birth.

Key operational points for the Junior ISA: the money belongs to the child from the moment it is deposited; the child takes control of the account at 16 (but cannot withdraw until 18); the account converts automatically to an adult ISA when the child turns 18; and any unused annual allowance is lost at the end of the tax year and cannot be carried forward.

UK Account 2: Junior SIPP — Starting a Pension at Birth

The Junior Self-Invested Personal Pension (SIPP) is one of the most remarkable and least-used investment vehicles available to UK parents. Parents can open a pension for a child from the day they are born — with no earned income requirement — and contribute up to £2,880 per year net, which receives basic rate tax relief to produce a gross contribution of £3,600 per year.AJ Bell's Junior ISA guide notes the pension option: 'Kick-start their pension with our hands-on, self-invested account with an annual investment allowance of £3,600.' The tax relief mechanism means the government effectively adds 25% to every contribution a parent makes — £2,880 contributed becomes £3,600 in the pension, immediately. That 25% uplift is a guaranteed immediate return before any investment growth occurs.

The compounding mathematics over a lifetime are extraordinary. £3,600 per year contributed from birth to age 18 (a total of £64,800 gross, or £51,840 out of pocket after tax relief) invested at 5% annual real return, then untouched from age 18 to 57, grows to approximately £780,000 at retirement. The child would enter adulthood with a pension fund on track for significant retirement wealth — funded by contributions made decades before they entered the workforce.

The critical constraint is that pension funds are locked until age 57 under current UK rules, making the Junior SIPP entirely unsuitable as a vehicle for education or early adult expenses. It is a pure retirement-building tool — the most powerful one available, but only relevant as a supplement to education-focused accounts (the Junior ISA) rather than a replacement for them.

UK Account 3: An Adult Stocks and Shares ISA Earmarked for the Child

Before the Junior ISA allowance is fully utilised, or when parents want to maintain control over the timing and conditions of access to savings, investing through an adult Stocks and Shares ISA earmarked for the child is a flexible and tax-efficient alternative. The adult ISA has a £20,000 annual allowance in 2026/27 — more than double the Junior ISA's £9,000 — and the parent retains full control over when and how the money is accessed.The key structural difference from the Junior ISA is ownership and control: money in a Junior ISA belongs irrevocably to the child and can only be accessed by them from age 18. Money in an adult ISA earmarked for a child belongs to the parent and can be accessed or redirected if circumstances change — if the child decides not to attend university, if a family emergency requires the funds, or if you want to make a conditional gift rather than an unconditional one.

For parents who are already maximising their own pension contributions and 401(k) equivalent, and whose Junior ISA allowance is already being fully used, the adult ISA earmarked strategy provides an overflow channel. The tax treatment is identical — no income tax or capital gains tax within the ISA wrapper — and the investment options are as wide as the Junior ISA's.

The Sequencing: Which Account to Open First, Second, and Third

What to Invest in Once the Accounts Are Open

Opening the right accounts is the structural decision. What you invest in within those accounts is the operational one. For parents investing on an 18-year or longer horizon for a child, the evidence consistently points toward one approach: low-cost, broadly diversified global equity index funds, held consistently rather than managed actively.The reasoning is straightforward. Over 18-year periods, passive index funds that track the global or US stock market have consistently outperformed the majority of actively managed funds after fees. The cost of active management — typically 0.75% to 1.5% annual charges versus 0.10% to 0.20% for the best index funds — compounds dramatically over 18 years. On a £9,000/year contribution, the difference in charges between a 0.15% and a 1.0% fund amounts to tens of thousands of pounds of additional cost over the full investment horizon.

What to hold inside child investment accounts — practical recommendations

- For a 0–10 year investment horizon: hold a high-equity allocation — 80% to 100% global equity index fund. The long time horizon absorbs short-term volatility and maximises the compounding growth from equities. Both Vanguard FTSE All-World (UK, available in Junior ISA) and Vanguard Total World Stock ETF (US, available in 529 and UGMA/UTMA) provide cheap, single-fund global equity diversification.

- For a 10–18 year investment horizon (approaching college or independence): gradually shift toward a more conservative allocation (60% equities, 40% bonds) as the spending date approaches, reducing the risk of a market downturn just before the money is needed. 529 target-date funds do this automatically and are a practical choice for parents who do not want to actively manage allocation.

- Within a Junior SIPP or custodial Roth IRA where the horizon is 40–50+ years: maintain maximum equity exposure throughout. The volatility at the 18-year mark is irrelevant for a retirement account that will not be accessed until the mid-2070s.

- For cost: prioritise fund expense ratios below 0.20% per year. For UK parents: Vanguard LifeStrategy or Global All Cap Index funds within a Junior ISA are the standard low-cost recommendations. For US parents: Vanguard, Fidelity, or iShares broad market index funds within a 529 or custodial account. Avoid funds with sales loads, redemption fees, or annual charges above 0.5%.

- For simplicity: a single global equity index fund in each account, set to reinvest dividends automatically, and contributed to via a standing order or automatic transfer, is the strategy most likely to be maintained consistently over 18 years. Complexity invites tinkering and interruption. Simplicity compounds.

CONCLUSION

A baby born today is the most powerful investment case you will ever encounter. They have time — decades of it — and compound interest rewards time above all other variables. The accounts in this guide — 529 plans, Trump Accounts, custodial Roth IRAs, UGMA/UTMA accounts, Junior ISAs, Junior SIPPs — are the instruments through which that time is converted into financial security. You do not need to use all of them. You need to use the right ones for your family's goals, in the right order, with the right investment approach inside them.The sequencing principle is clear: your own financial foundations first, then the child's accounts, prioritised by tax efficiency. For US parents, open a 529 immediately and ensure any child born between 2025 and 2028 has their Trump Account in place from July 2026. For UK parents, open a Stocks and Shares Junior ISA from birth and consider a Junior SIPP if there is surplus beyond the JISA. In both countries, the custodial Roth IRA or equivalent pension contribution becomes available when the child earns their first income — and that moment is when the most powerful long-run compounding vehicle opens.

Frequently Asked Questions

What is the best investment account to open for a newborn baby in the US?

For most US parents, the 529 education savings plan is the first account to open after birth — it can be opened immediately, has no annual contribution limit within gift tax rules, grows tax-free, and withdrawals for education expenses are completely tax-free. For children born between January 2025 and December 2028, a Trump Account will be automatically created with a $1,000 government seed deposit, with parental contributions of up to $5,000 per year available from July 2026. A custodial Roth IRA becomes available once the child has any earned income — and at $7,500 for 2026 (NerdWallet, May 2026), it is the most powerful long-run tax-free compounding account available. UGMA/UTMA custodial accounts provide the broadest flexibility for non-education goals but are taxable. The recommended sequence is: 529 first, Trump Account automatically, Roth IRA when the child earns income.What is the best investment account for a baby in the UK?

The Junior ISA (Stocks and Shares variant) is the primary account for UK parents and should be opened as close to birth as possible. The 2026/27 Junior ISA allowance is £9,000 per child per tax year, confirmed unchanged until April 2031 by Which? and AJ Bell. Contributions grow completely tax-free and can be withdrawn tax-free from age 18. For parents with surplus beyond the £9,000 Junior ISA allowance, the Junior SIPP (pension from birth) provides 25% basic rate tax relief on contributions (up to £3,600 gross per year) and extraordinary long-run compounding for retirement. An adult Stocks and Shares ISA earmarked for the child provides the most flexibility but requires parental discipline to maintain. Open the Junior ISA first, SIPP second if budget allows.What is a Trump Account and is my baby eligible?

Trump Accounts are a new government-backed investment account created under the One Big Beautiful Bill Act for children born between January 1, 2025, and December 31, 2028. Children in this birth window are automatically enrolled and receive a $1,000 government-funded seed deposit invested in a stock index fund — no action is required by parents. From July 2026, parents and employers can contribute up to $5,000 per year (individuals) and $2,500 per year (employers) until the child turns 18, after which contributions can reach the annual IRA limit. FH Associates' March 2026 guide describes Trump Accounts as a 'starter wealth-building vehicle' best used alongside 529 plans, Roth IRAs, and other accounts rather than as a standalone solution. The $1,000 seed at birth, invested at 7% real return for 18 years, grows to approximately $3,380 without any additional contributions.Can I open a Junior ISA and still contribute to my own ISA?

Yes — the Junior ISA allowance (£9,000 for 2026/27) is completely separate from and in addition to the adult ISA allowance (£20,000 for 2026/27). Contributing to a Junior ISA for your child does not reduce your own ISA allowance in any way. MoneyHelper's official guidance confirms this: 'The £9,000 limit is separate from, and in addition to, the adult ISA allowance.' Additionally, anyone — not just the child's parents — can contribute to a Junior ISA, provided they do not exceed the £9,000 annual limit in total across all contributors. Grandparents, aunts, uncles, and family friends can all contribute to the same Junior ISA. The account must be opened by a parent or legal guardian, but contributions from others do not affect the contributor's own ISA allowance.Should I prioritise a 529 plan or my own retirement savings?

Your own retirement savings come first — specifically, at minimum, contributing enough to your 401(k) to capture the employer match (which is a guaranteed 50% to 100% immediate return), and then maximising your Roth IRA ($7,500 for 2026). This is not a failure of parental generosity — it is sound financial sequencing. Your child can fund education through scholarships, student loans, work, or grants. You cannot borrow to fund retirement. A parent who neglects their own retirement to fund a child's 529 may create a dependency on the child in old age that costs the child more than the 529 saved them. FH Associates' March 2026 guide advises: '529 plans are the core education vehicle — but only after your own retirement savings are on track.' Once your retirement contributions are at a sustainable level, 529 contributions are highly efficient and worth prioritising over taxable saving.References

NerdWallet — How to Invest for Kids: 7 Best Investing Accounts (May 2026) https://www.nerdwallet.com/investing/best/investment-accounts-for-kidsCNBC Select — 6 Best Investment Accounts for Kids in May 2026 https://www.cnbc.com/select/best-investment-accounts-for-kids/

FH Associates — Investment Accounts for Kids: Five Common Choices and How to Pick the Right One (March 2026) https://fhassoc.com/investment-accounts-for-kids-five-common-choices-how-to-pick-the-right-one/

Bankrate — 7 Investments to Set Your Kids Up for Life: Including Trump Accounts (2026) https://www.bankrate.com/investing/7-investments-to-set-your-kids-up-for-life/

Which? — Best Junior ISA Rates 2026: Rules and Top Picks (May 2026) https://www.which.co.uk/money/savings-and-isas/isas/best-junior-cash-isas-aTblN9u99wlN

MoneyHelper — Junior ISAs: Official UK Guidance https://www.moneyhelper.org.uk/en/savings/types-of-savings/junior-isas

AJ Bell — Junior ISA Allowance 2026/27: Rules Explained (April 2026) https://www.ajbell.co.uk/isa/junior-isa/allowance

GOV.UK — Junior Individual Savings Accounts (ISA): Official Overview https://www.gov.uk/junior-individual-savings-accounts

Hargreaves Lansdown — Junior ISA Allowance 2026/27 https://www.hl.co.uk/investment-services/junior-isa/junior-isa-allowance

0 Comments Comments