Taxes

What Is Capital Gains Tax? The UK 2026/27 Complete Guide

Table of Contents

- A Tax That Has Changed Dramatically Since 2022

- What Is Capital Gains Tax?

- What Triggers CGT? Common Chargeable Disposals

- What Is NOT Subject to CGT?

- CGT Rates, Allowances, and Exemptions: Complete 2026/27 Reference

- How CGT Is Calculated: The Step-by-Step Process

- Step 1 — Calculate the Gain

- Step 2 — Subtract the Annual Exempt Amount

- Step 3 — Stack the Gain on Top of Your Income

- Step 4 — Apply the Rate and Report

- Worked Examples — 2026/27

- CGT on Property: Key Rules for Landlords and Second Homeowners

- CGT on Shares, Funds, and Cryptocurrency

- Shares and Investment Funds

- Cryptocurrency

- How to Reduce Your CGT Bill: Eight Legal Planning Strategies

- How to Report and Pay CGT

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

A Tax That Has Changed Dramatically Since 2022

Capital Gains Tax (CGT) is one of the most misunderstood taxes in the UK — and one that has changed more significantly in the past three years than at almost any point in its history. In 2022/23, the annual exempt amount (the amount of gains you could make each year before CGT applied) stood at £12,300. By 2024/25, it had been cut to £3,000 — a reduction of over 75% in two years. In October 2024, the Labour government raised CGT rates from 10%/20% (shares) and 18%/28% (residential property) to a unified 18%/24% across all assets. And from 6 April 2026, the Business Asset Disposal Relief rate rose again, from 14% to 18%.These changes matter for a much wider group of people than CGT traditionally affected. With the annual exempt amount at just £3,000, many investors, second property owners, and crypto holders who previously stayed well within the threshold are now facing CGT bills on gains they would have made completely free of tax three years ago. The House of Commons Library's April 2026 rates briefing confirms all CGT parameters for 2026/27 are unchanged from 2025/26, with the single unified rate structure — 18% for basic-rate taxpayers and 24% for higher or additional-rate taxpayers — applying equally to shares, property, cryptocurrency, and all other chargeable assets.

This guide explains what Capital Gains Tax is, what triggers it, what is exempt, what the 2026/27 rates and allowances are, how CGT is calculated in practice with worked examples, and the eight legal strategies for reducing your bill. Whether you are an investor, a landlord, a business owner, or someone who has simply sold an asset that has increased in value, this guide provides the complete picture of your CGT position in 2026/27.

What Is Capital Gains Tax?

Capital Gains Tax is charged on the profit — the gain — you make when you sell, give away, exchange, or otherwise dispose of an asset that has increased in value. You are not taxed on the full amount you receive for the asset — only on the difference between what you paid for it (the cost basis, also called the acquisition cost) and what you receive when you dispose of it (the disposal proceeds), after deducting allowable costs.The key distinction is that CGT is a tax on gains from capital assets, not on income. It sits alongside income tax rather than within it. Income tax applies to money you earn through work, a business, pension income, savings interest, or dividends. CGT applies to the appreciation in value of capital assets — things you own rather than income you receive. The two taxes are calculated separately, but they interact: your income determines how much of your basic-rate band is available when CGT is calculated, affecting whether 18% or 24% applies to your gains.

What Triggers CGT? Common Chargeable Disposals

CGT is triggered by a disposal — and a disposal is broader than just a sale. The following events all constitute disposals that can trigger a CGT charge:- Selling shares, investment funds, or exchange-traded funds (ETFs) held outside an ISA or pension

- Selling a second home, buy-to-let property, or any residential property that is not your main home

- Selling or exchanging cryptocurrency (each trade is a separate disposal — including crypto-to-crypto exchanges)

- Giving assets away to someone other than your spouse or civil partner

- Selling or transferring a business or qualifying business assets

- Selling valuable personal possessions (chattels) worth more than £6,000 — jewellery, antiques, artwork

- Receiving insurance compensation for a damaged or destroyed asset that you then do not reinvest

What Is NOT Subject to CGT?

Several major categories of asset are wholly or partially exempt from CGT:- Your main home: Private Residence Relief (PRR) exempts the gain on a property that was your only or main home throughout your period of ownership. The final nine months of ownership are also always exempt, even if the property was not your main home during that period. Letting out part of your home, using part of it as a business, or having a large garden or grounds can create a partial CGT charge.

- ISA and pension investments: Gains made inside an ISA (cash ISA, stocks and shares ISA, Lifetime ISA) or inside a pension (SIPP, workplace pension) are completely exempt from CGT and income tax. This is the most powerful long-term tax shelter available to UK savers and investors.

- Cars: Private cars are specifically exempt from CGT, even if they have appreciated in value (which classic cars sometimes do). Commercial vehicles and other motorised assets are treated differently.

- Gifts to charities: Assets gifted to registered UK charities are free of CGT.

- UK Government gilts and qualifying corporate bonds: These are specifically exempt from CGT.

- Winnings and compensation: Lottery and gambling winnings are not subject to CGT. Compensation for personal injury is also exempt.

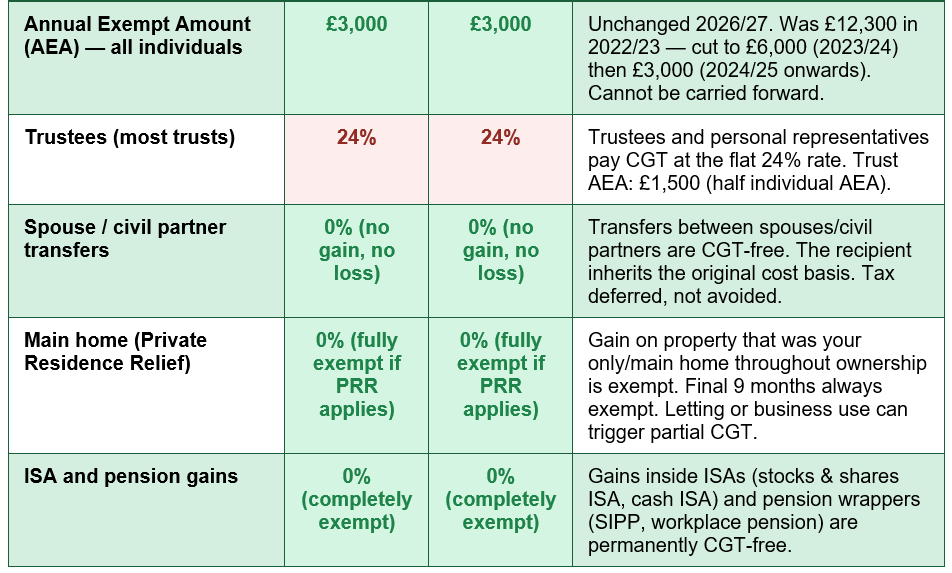

The AEA has been cut by 76% since 2022/23: £12,300 in 2022/23 → £6,000 in 2023/24 → £3,000 from April 2024 onwards — the dramatic reduction in the annual exempt amount has brought significantly more investors, property owners, and crypto holders into scope for CGT who were previously sheltered by the larger allowance. The £3,000 AEA is confirmed unchanged for 2026/27 — House of Commons Library, April 2026.

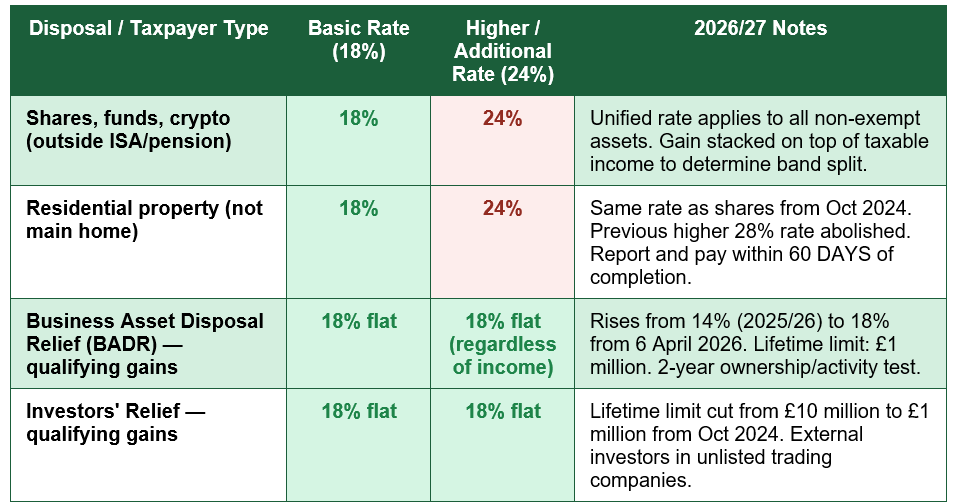

CGT Rates, Allowances, and Exemptions: Complete 2026/27 Reference

The table below provides a complete reference for every CGT rate, allowance, and exemption in 2026/27, updated for the October 2024 Budget changes and the April 2026 BADR rate rise:

How CGT Is Calculated: The Step-by-Step Process

Calculating your CGT liability follows a specific sequence that determines not only how much tax you owe but at what rate. The stacking mechanism — adding your gain on top of your taxable income — is the most important and most frequently misunderstood element.Step 1 — Calculate the Gain

The gain is the disposal proceeds minus the acquisition cost minus allowable costs. Allowable costs include: the original purchase price; costs of acquisition (solicitor's fees, stamp duty, broker commissions); costs of improving the asset (capital improvements, not maintenance or repairs); and costs of disposal (estate agent fees, solicitor's fees, broker commissions on sale). You cannot deduct income tax, interest on loans to purchase the asset, or general maintenance costs.Step 2 — Subtract the Annual Exempt Amount

Deduct the £3,000 annual exempt amount from your net gains (gains after any losses in the same year). This is a use-it-or-lose-it allowance — it cannot be carried forward to a future year if unused. Apply it against the gains that would be taxed at the highest rate first, as GOV.UK's official guidance confirms.Step 3 — Stack the Gain on Top of Your Income

Your gains are stacked on top of your taxable income for the year. The basic-rate band runs from £0 to £37,700 of taxable income (income above the personal allowance of £12,570). If your employment income takes up part of the basic-rate band, the remaining space is how much of your gain can be taxed at 18%. Any gain above the remaining basic-rate band space is taxed at 24%.Step 4 — Apply the Rate and Report

For residential property disposals where CGT is owed, you must report and pay within 60 days of completion using HMRC's online property reporting service. For all other assets, gains are reported on your Self Assessment tax return by 31 January following the end of the relevant tax year. If you are not currently in Self Assessment, you must register with HMRC to report CGT above your annual exempt amount.Worked Examples — 2026/27

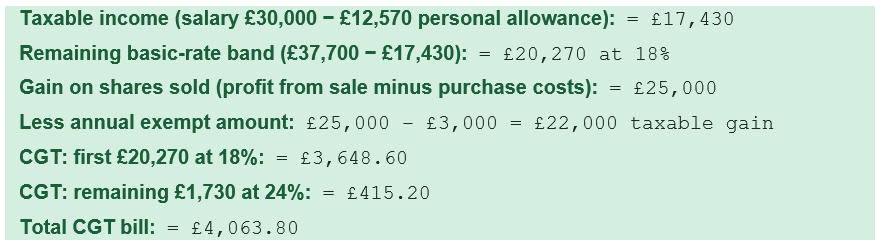

Example 1 — Shares, basic-rate taxpayer with remaining band:

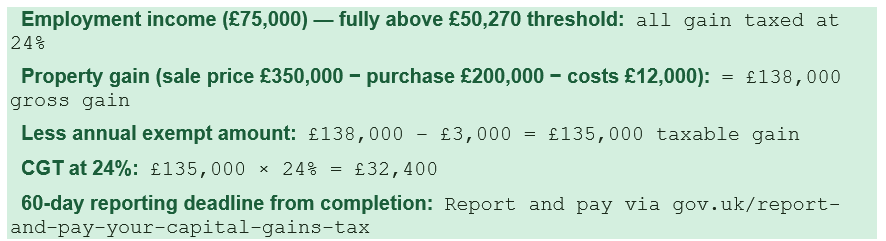

Example 2 — Buy-to-let property, higher-rate taxpayer (no remaining basic-rate band):

CGT on Property: Key Rules for Landlords and Second Homeowners

Residential property that is not your main home — buy-to-let properties, second homes, inherited properties, properties held as investments — is subject to CGT at the unified 2026/27 rates of 18% and 24%. This is a notable change from before October 2024, when residential property carried a higher rate of 28% for higher-rate taxpayers. The reduction to 24% represents a genuine decrease in the CGT burden for property investors, though the lower annual exempt amount (£3,000 versus the historic £12,300) significantly increases the number of smaller gains that are fully chargeable.The 60-day reporting rule is the most important procedural requirement for property CGT. If you sell a UK residential property and CGT is owed, you must report and pay the tax within 60 calendar days of the completion date, regardless of when the tax year ends. Missing this deadline triggers automatic penalties starting at £100, with additional daily penalties for extended delays. The report is made through HMRC's online 'Report and pay Capital Gains Tax on UK property' service at gov.uk/report-and-pay-your-capital-gains-tax, and payment is made at the same time.

Private Residence Relief (PRR) is the key exemption for property owners. If a property has been your only or main home throughout your entire period of ownership, the full gain is exempt from CGT. The final nine months of ownership are always exempt, even if the property was not your main home in that period — this provision exists to help people who have moved into a new home before selling the old one. If you have let your main home or lived elsewhere for any period, the gain attributable to those periods (calculated proportionally) may be chargeable.

Inherited property and the CGT base cost: When you inherit a property, the cost base for CGT purposes is the probate value — the market value at the date of death, not the original purchase price. This means if you sell an inherited property for more than its probate value, CGT is only due on the gain above the probate value. If you sell for less than the probate value (a capital loss), this loss can be offset against other gains. Always confirm the probate value from the estate paperwork before calculating any CGT position on an inherited property.

CGT on Shares, Funds, and Cryptocurrency

Shares and Investment Funds

Shares and investment funds held outside an ISA or pension wrapper are subject to CGT when sold. UK shares and funds use the 'Section 104 pool' (average cost) method for calculating gains — all shares in the same company are treated as a single pool, and the average acquisition cost per share is used for each disposal. This prevents investors from selectively selling their highest-cost shares to minimise gains. The same-day rule and the 30-day (bed and breakfast) rule prevent certain tax-motivated disposal-and-repurchase strategies: if you sell shares and buy the same shares within 30 days, the repurchased shares are matched against the sale for CGT purposes rather than the pooled shares.Cryptocurrency

Cryptocurrency is treated as a capital asset for CGT purposes. Each disposal — whether a sale for sterling, an exchange of one cryptocurrency for another, or using crypto to purchase goods or services — is a taxable event. HMRC's position is explicit: crypto-to-crypto exchanges are disposals and can trigger CGT even if you never receive sterling. The Section 104 pooling rules apply to each separate cryptocurrency (not across different cryptos). HMRC has significantly increased its focus on crypto tax compliance in 2025 and 2026, requiring exchanges operating in the UK to report customer transaction data.THE BED AND ISA STRATEGY: One of the most powerful CGT reduction tools for investors is the Bed and ISA. You sell investments held outside an ISA, use your £3,000 annual exempt amount to shelter the gain where possible, and immediately repurchase the same investments inside your ISA using your annual £20,000 ISA allowance. The 30-day rule does not apply to ISA repurchases. All future growth and income on those investments inside the ISA is permanently CGT and income tax free. This is a completely legal, HMRC-accepted strategy that works best when done at the start of a new tax year.

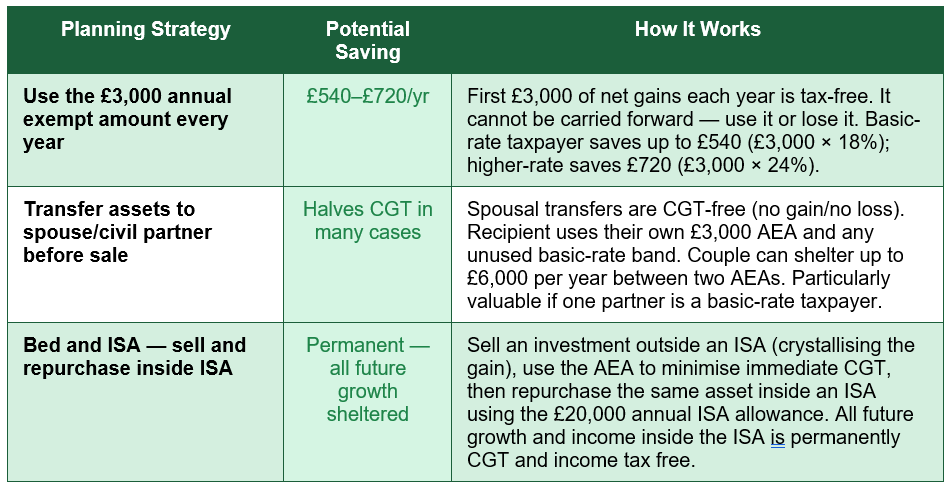

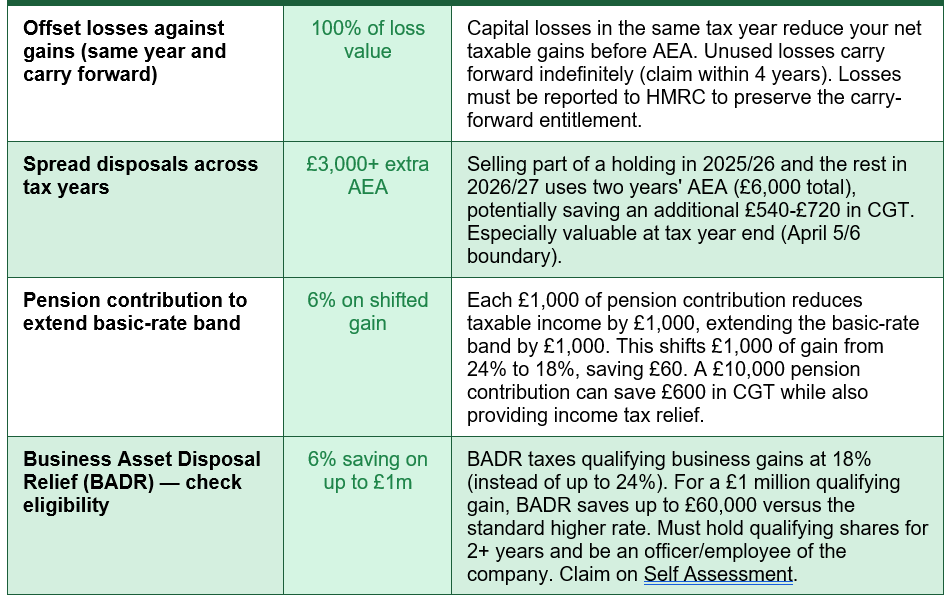

How to Reduce Your CGT Bill: Eight Legal Planning Strategies

The following strategies are all legal, HMRC-accepted methods for reducing CGT liability. The table maps each strategy to its potential saving and the mechanism through which it works:

How to Report and Pay CGT

How you report and pay CGT depends on what asset you have sold and whether your gains exceed the annual exempt amount:- Residential property (UK): If you owe CGT on a UK residential property disposal, you must report and pay within 60 calendar days of completion using the HMRC online service at gov.uk/report-and-pay-your-capital-gains-tax. This applies even if you are a Self Assessment taxpayer who will also report the gain on your annual return. The 60-day payment is a provisional payment that is reconciled through Self Assessment.

- All other assets (including shares, crypto, business assets): Report through your annual Self Assessment tax return. The deadline is 31 January following the end of the tax year in which the disposal occurred. If you have never filed Self Assessment, register with HMRC at gov.uk/register-for-self-assessment. First-time registration should be completed by 5 October in the year after the disposal.

- Gains below the annual exempt amount: If your net gains for the year are below £3,000, you do not owe any CGT and do not need to report unless you are already in Self Assessment (in which case you should still declare them on your return). Losses should still be reported within four years to preserve the carry-forward entitlement.

Conclusion

Capital Gains Tax in 2026/27 operates under a simplified but more demanding framework than existed three years ago. The annual exempt amount, which stood at £12,300 in 2022/23, is now £3,000 — bringing a significantly larger number of investors, property owners, and crypto holders into regular CGT liability. The rates of 18% (basic rate) and 24% (higher rate) now apply uniformly across all chargeable assets — shares, property, cryptocurrency, and other capital assets — ending the previous distinction between property and non-property rates. Business Asset Disposal Relief, which once offered a 10% flat rate on qualifying business gains, now charges 18% from April 2026, rising from 14% in 2025/26.Despite these increases, the framework for CGT planning remains robust. The annual exempt amount, though smaller, is still a use-it-or-lose-it allowance worth up to £720 in tax savings each year at the higher rate. Spousal transfers before disposal can double the effective annual allowance to £6,000. ISA and pension wrappers remain completely CGT-exempt, and the Bed and ISA strategy allows investors to progressively shelter existing portfolios from future CGT. Capital losses, whether from the current year or carried forward from previous years, offset gains before the AEA is applied. And pension contributions extend the basic-rate band, shifting gains from 24% to 18%.

The most important practical rule in 2026/27 is timing and reporting. For residential property, the 60-day reporting and payment window is a strict deadline with automatic penalties for late submission — it is not the same as the Self Assessment year-end deadline and must be treated separately. For all other assets, 31 January is the reporting deadline, with 5 October as the registration deadline for first-time Self Assessment filers. The underlying principle across all CGT planning is the same: make decisions before disposal, not after. Once an asset is sold, the gain is crystallised and the rate is fixed. The planning happens before the sale.

Frequently Asked Questions (FAQ)

What are the capital gains tax rates for 2026/27?

For 2026/27, CGT is charged at 18% for basic-rate taxpayers and 24% for higher-rate and additional-rate taxpayers, on all chargeable assets including shares, investment funds, residential property, cryptocurrency, and other capital assets. These unified rates apply from 30 October 2024 and represent a simplification of the previous system, which had different rates for property (previously 18%/28%) and non-property assets (previously 10%/20%). Business Asset Disposal Relief (BADR) reduces the CGT rate to 18% on up to £1 million of qualifying lifetime gains from business disposals, rising from 14% in 2025/26. The annual exempt amount is £3,000 per individual.Do I pay capital gains tax when I sell my home?

Usually not. Your main home is exempt from CGT under Private Residence Relief (PRR), provided it has been your only or main residential property throughout the period of ownership. The final nine months of ownership are always CGT-exempt, even if the property was not your main home during that period. Situations that can create a partial CGT charge on a main home include: using part of the property exclusively for business; having grounds larger than 0.5 hectares; letting the property (or part of it) out; or periods where the property was not your main residence. Buy-to-let properties, second homes, and investment properties are fully subject to CGT at the standard 2026/27 rates.How is capital gains tax calculated on shares?

The gain on shares is calculated as the disposal proceeds minus the acquisition cost minus allowable costs (broker commissions on purchase and sale). UK shares use the Section 104 pool method — all shares in the same company are averaged into a single pool, preventing selective identification of highest-cost shares. Deduct the £3,000 annual exempt amount from your net gains (after any losses). Stack the remaining gain on top of your taxable income. The portion of the gain that fits within the remaining basic-rate band (up to £37,700 of combined income and gain) is taxed at 18%; any gain above is taxed at 24%. The 30-day bed and breakfast rule prevents disposal and immediate repurchase to reset the cost base.Is cryptocurrency subject to capital gains tax in the UK?

Yes. HMRC treats cryptocurrency as a capital asset, and every disposal is a taxable event potentially subject to CGT. Disposals include selling crypto for sterling, exchanging one cryptocurrency for another, using crypto to buy goods or services, and giving crypto to someone who is not your spouse or civil partner. The Section 104 pooling rules apply to each cryptocurrency separately — all holdings of the same coin are averaged into a pool, and the average cost per coin is used for each disposal calculation. The same CGT rates (18%/24%), annual exempt amount (£3,000), and reporting rules apply to crypto as to other assets. HMRC has significantly increased its focus on crypto tax compliance, with UK exchanges now required to share customer transaction data.What is Business Asset Disposal Relief and who qualifies?

Business Asset Disposal Relief (BADR), formerly known as Entrepreneurs' Relief, taxes qualifying gains from the disposal of a business or business assets at a reduced flat rate of 18% in 2026/27 (up from 14% in 2025/26 and 10% before April 2025), on up to a £1 million lifetime limit. BADR applies to: sole traders and partners selling all or part of a qualifying trading business; directors and employees who hold at least 5% of shares in a qualifying personal company, have held them for at least two years, and have been an officer or employee of the company throughout that period. The company must be a trading company (not primarily an investment company). BADR must be claimed on your Self Assessment tax return — it is not applied automatically.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. GOV.UK — Capital Gains Tax Rates and Allowances (Updated April 2026)

https://www.gov.uk/guidance/capital-gains-tax-rates-and-allowances

2. GOV.UK — Capital Gains Tax: What You Pay It On, Rates and Allowances

https://www.gov.uk/capital-gains-tax/rates

3. House of Commons Library — Direct Taxes: Rates and Allowances for 2026/27 (April 7, 2026)

https://commonslibrary.parliament.uk/research-briefings/cbp-10618/

4. UKCapitalGainsTaxCalculator.co.uk — CGT Rates 2026/27 (Updated June 2026)

https://ukcapitalgainstaxcalculator.co.uk/capital-gains-tax-rates-2026-27

5. UKTax.Tools — UK Capital Gains Tax Basics 2026/27 (Updated July 2026)

https://uktax.tools/tax-insights/capital-gains-tax-basics/

6. Headway Wealth — Capital Gains Tax in 2026 and 2026/27: What Investors and Business Owners Need to Know (March 2026)

https://headwaywealth.com/headway-blog/capital-gains-tax-in-2026-and-2026-27-what-investors-and-business-owners-need-to-know/

7. TaxFly — Capital Gains Tax Rates 2026/27 (Updated 1 week ago)

https://www.taxfly.co.uk/guides/capital-gains-tax-rates-2026-27

8. Deloitte Taxscape — UK Tax Rates 2026/27 (Autumn Budget 2025 Edition)

https://taxscape.deloitte.com/taxtables/deloitte-uk-tax-rates-2026-27.pdf

0 Comments Comments