Taxes

What Is Tax Relief and How to Claim It? UK Complete Guide

Table of Contents

- The Billions in Unclaimed Tax Relief Every Year

- What Is Tax Relief?

- Every Major UK Tax Relief in 2026/27: The Complete Reference

- Pension Tax Relief: The Most Valuable Relief Most People Underuse

- Relief at Source (Personal and Workplace Pensions)

- Salary Sacrifice Pensions: The Most Tax-Efficient Option

- Working From Home Tax Relief in 2026/27

- Marriage Allowance: £252 Per Year Many Couples Never Claim

- Gift Aid: How Charitable Donations Reduce Your Tax Bill

- How to Claim Tax Relief: The Four Routes

- Worked Examples: How Much Could You Reclaim?

- Example 1 — PAYE Employee (Basic Rate), 4-Year Backdate

- Example 2 — Higher-Rate Taxpayer with Multiple Missed Claims

- The Four-Year Backdating Window: Do Not Miss Your Deadline

- Common Tax Relief Mistakes to Avoid

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Billions in Unclaimed Tax Relief Every Year

HMRC estimates that billions of pounds in legitimate tax relief goes unclaimed in the UK every year. The primary reason is not complexity — the claims process for most common reliefs is straightforward — but awareness. Many PAYE employees assume they have nothing to claim because their income tax is handled automatically through their payslip. In practice, a basic-rate taxpayer who works in a qualifying occupation, pays professional subscriptions, sometimes works from home, and donates to charity through Gift Aid could easily be entitled to £200 to £400 in annual refunds they have never once claimed. A higher-rate taxpayer who is not claiming additional pension relief or Gift Aid rebates through Self Assessment is almost certainly overpaying, often by hundreds of pounds per year.Tax relief is not a government favour or a loophole. It is the mechanism by which HMRC reduces your tax bill on specific expenditure and circumstances that Parliament has decided should not attract full taxation — pension savings designed to fund your retirement, charitable giving, costs you genuinely incur in doing your job, the transfer of unused personal allowance between partners, and investments in small businesses. The reliefs exist in law, they belong to you if you qualify, and the only reason many people do not receive them is that they do not know to claim.

This guide covers every major UK tax relief available in 2026/27, how each one works, what it is worth at basic and higher rate, how to claim it, and critically — the four-year backdating window that allows you to reclaim relief you should have claimed in previous tax years. Whether you are a PAYE employee, a self-employed sole trader, a landlord, a charitable donor, or a higher-rate earner with pension contributions, this guide provides the complete picture of what you are entitled to and the specific steps to claim it.

What Is Tax Relief?

Tax relief is a reduction in your taxable income — or in the tax directly calculated on that income — that HMRC allows on qualifying expenditure or circumstances. It is not a payment from the government; it is a reduction in the amount of tax you would otherwise owe.The mechanism works in one of two ways. Most reliefs work by reducing your taxable income: if you earn £40,000 and claim £1,200 in allowable relief, you pay tax only on £38,800. At the basic rate of 20%, that saves £240. At the higher rate of 40%, the same £1,200 saves £480. This is why tax relief is proportionately more valuable to higher-rate taxpayers — and why it is especially important for those near or above the £50,270 higher-rate threshold to claim everything they are entitled to.

Some reliefs — particularly the Marriage Allowance and investment-related reliefs like EIS — work as direct tax credits or allowance transfers rather than income reductions, but the net effect is the same: less tax paid. The amount of relief available in any given tax year depends on what you have spent, what allowances apply to your situation, and which tax band your income falls into.

The 2026/27 UK income tax framework: Personal allowance £12,570 — Basic rate 20% (to £50,270) — Higher rate 40% (to £125,140) — Additional rate 45% — the UK personal allowance is frozen at £12,570 through 2027/28. The higher-rate threshold of £50,270 is also frozen, meaning wage growth is dragging more workers into the 40% bracket each year — making higher-rate relief claims increasingly valuable as a growing proportion of UK taxpayers cross this threshold (HMRC / PocketWise, 2026/27).

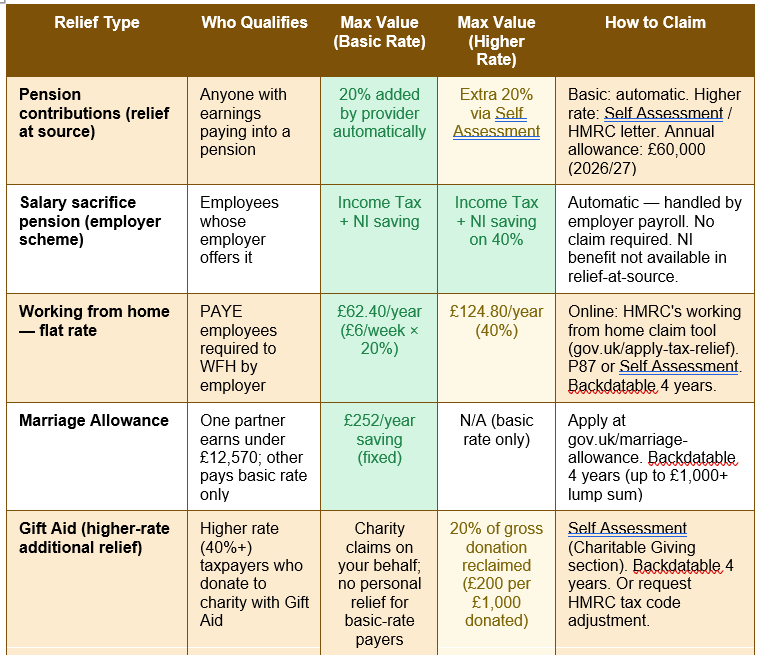

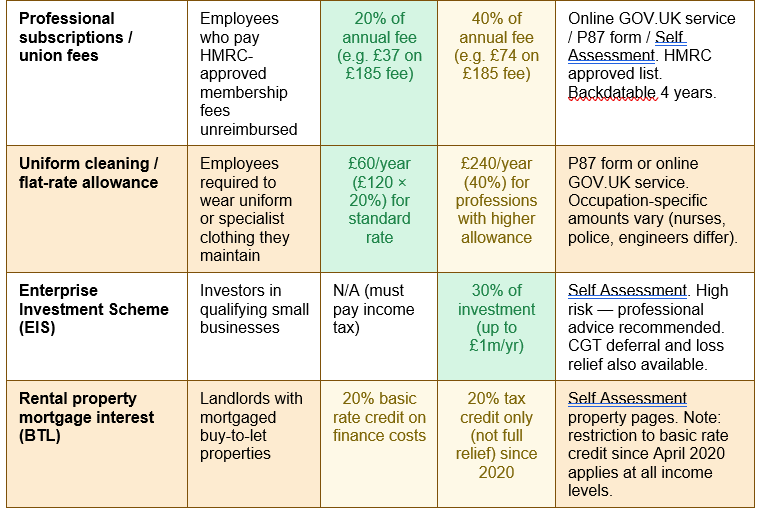

Every Major UK Tax Relief in 2026/27: The Complete Reference

The table below provides a definitive reference for every major tax relief available to UK taxpayers in 2026/27, including who qualifies, what it is worth at basic and higher rate, and how to claim:

Pension Tax Relief: The Most Valuable Relief Most People Underuse

Pension contributions attract the single most valuable tax relief available to most UK taxpayers. The principle is that money you save for retirement should not be taxed as you earn it — tax is instead deferred until you draw your pension, when your income may be lower and you may pay tax at a lower rate or not at all. For many taxpayers, particularly those in the 40% or 45% band, pension contributions are the most tax-efficient use of money available.Relief at Source (Personal and Workplace Pensions)

Most personal pensions and many workplace pensions operate on a relief-at-source basis. When you contribute, your pension provider claims basic rate tax relief (20%) from HMRC and adds it to your pot automatically. If you contribute £800 from your take-home pay, the provider adds £200, making your total pension contribution £1,000. You do not need to do anything to receive this 20% relief — it happens automatically.However, if you are a higher-rate (40%) or additional-rate (45%) taxpayer, you are entitled to claim the remaining relief — the difference between your marginal tax rate and the 20% already claimed by your provider. For a higher-rate taxpayer contributing £1,000 gross to a pension, the full relief should be £400, but only £200 is added automatically. The remaining £200 must be claimed separately, either through a Self Assessment tax return or by writing to HMRC. According to PocketWise's 2026/27 guide, this is the most common and most expensive oversight — higher-rate taxpayers whose employers offer relief-at-source pensions are routinely leaving their additional 20% unclaimed.

Salary Sacrifice Pensions: The Most Tax-Efficient Option

Where an employer offers salary sacrifice, this is typically the most tax-efficient pension arrangement available. Under salary sacrifice, you agree to reduce your gross salary by the amount of your pension contribution before tax and National Insurance are calculated. This means you save not only income tax but also employee National Insurance (8% in 2026/27 at the basic rate) on the contributed amount. Your employer also saves their National Insurance contribution (13.8%) and many employers share a portion of this saving with employees. If your employer offers salary sacrifice, it is almost always financially beneficial to use it rather than contributing to a personal pension outside of payroll.The annual allowance for pension contributions in 2026/27 is £60,000, or 100% of your earnings, whichever is lower. You can also carry forward unused allowance from the previous three tax years, which can allow significantly larger single-year contributions if you have the funds available.

September 2025 change: telephone pension relief claims discontinued. From September 2025, HMRC discontinued the option to claim personal pension tax relief by telephone. Higher-rate taxpayers claiming additional pension relief must now either file a Self Assessment return or write to HMRC. Do not attempt to claim pension relief by phone — the service no longer exists. The GOV.UK pension relief claim service remains available online (gov.uk/claim-tax-relief-pension).

Working From Home Tax Relief in 2026/27

If your employer requires you to work from home — rather than you choosing to do so — you can claim tax relief on the additional household costs you incur. The simplest route is the HMRC flat rate of £6 per week, which you can claim without providing receipts or calculating actual costs. Over a full year, this £312 annual relief saves a basic-rate taxpayer £62.40 and a higher-rate taxpayer £124.80.Alternatively, if your actual additional costs (additional heating, electricity, broadband) exceed the flat rate, you can claim your actual costs instead. You will need to keep records of the additional expenditure, the total cost of the bill, and the proportion that relates to work use. Most taxpayers find the flat rate simpler and claim that instead.

Working from home relief can be claimed for up to four previous complete tax years. The current backdating window (from July 2026) covers the tax years 2022/23, 2023/24, 2024/25, and 2025/26. The 2021/22 window closed permanently on 5 April 2026 — any unclaimed relief for that year is now lost. Claims are made online through the HMRC job expenses tool at gov.uk, through a P87 form, or through Self Assessment for the self-employed.

FOUR YEARS = SIGNIFICANT MONEY: If you have been working from home since 2022/23 and have never claimed, a basic-rate taxpayer can claim approximately £249.60 from four years of backdated working from home relief (4 × £62.40). A higher-rate taxpayer can claim £499.20. This takes approximately 10 minutes on the HMRC online service. Do not delay — the 2022/23 window closes on 5 April 2027 permanently.

Marriage Allowance: £252 Per Year Many Couples Never Claim

The Marriage Allowance allows one partner in a married couple or civil partnership to transfer £1,260 of their unused personal allowance to the other partner, saving the higher-earning partner up to £252 in income tax per year. The eligibility conditions are specific: the transferring partner must earn less than the personal allowance (£12,570 in 2026/27) — meaning they pay no income tax — and the receiving partner must be a basic rate taxpayer, paying 20% but not yet crossing into the 40% band.The claim is made online at gov.uk/marriage-allowance and is processed by HMRC adjusting both partners' tax codes — reducing the lower earner's code to reflect the transferred allowance and increasing the higher earner's code to reflect the received allowance. The benefit is applied automatically once claimed and continues each year until circumstances change. Backdating is available for up to four years, meaning couples who have been eligible but never claimed can receive a lump sum of over £1,000. PocketWise's 2026/27 tax relief guide confirms: 'You can backdate claims for up to four years, potentially receiving a lump sum of over £1,000.'

Gift Aid: How Charitable Donations Reduce Your Tax Bill

Gift Aid is the mechanism by which UK charities can claim an additional 25p from HMRC for every £1 donated by a UK taxpayer. For basic-rate taxpayers, the benefit flows entirely to the charity — the donation is treated as if it had been paid net of basic rate tax, so a donation of £80 becomes £100 in the charity's hands. You receive no personal relief as a basic-rate taxpayer, but your donation goes further at no cost to you.For higher-rate and additional-rate taxpayers, Gift Aid also produces a personal tax benefit. The charity claims 20% basic rate relief, but since you pay 40% income tax, the remaining 20% belongs to you — not the charity, not HMRC. On a £1,000 donation, a 40% taxpayer personally reclaims £200 through Self Assessment. An additional-rate (45%) taxpayer reclaims £250. Over a year of meaningful charitable giving, these amounts are significant and are among the most consistently unclaimed reliefs in the UK tax system.

There is an additional, particularly powerful application of Gift Aid for those earning over £100,000. The personal allowance is withdrawn at £1 for every £2 of income above £100,000, creating an effective marginal tax rate of 60% on income between £100,000 and £125,140. Gift Aid donations reduce Adjusted Net Income for this purpose — a £10,000 Gift Aid donation becomes £12,500 gross and reduces ANI by £12,500, potentially restoring personal allowance worth significantly more than the donation itself. Pocketwise's May 2026 analysis shows a £10,000 Gift Aid donation costing a £110,000 earner a net £2,472 after all tax effects.

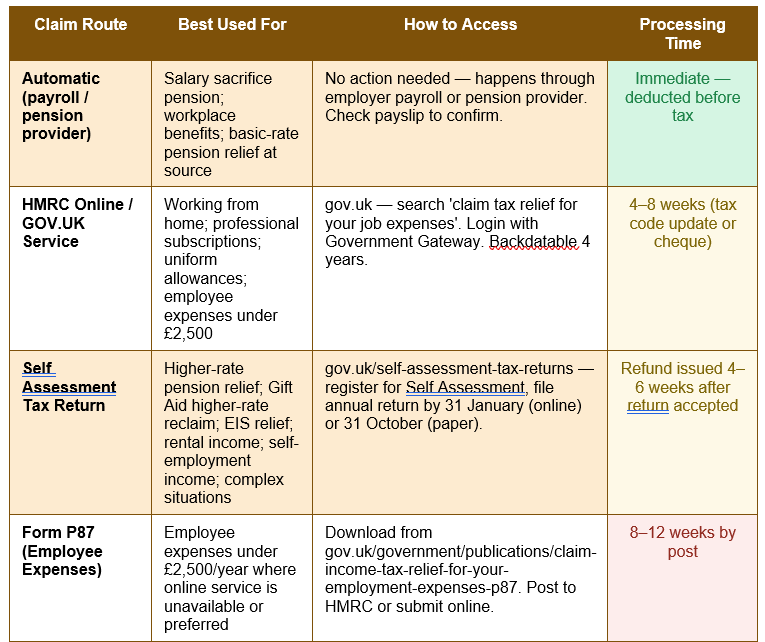

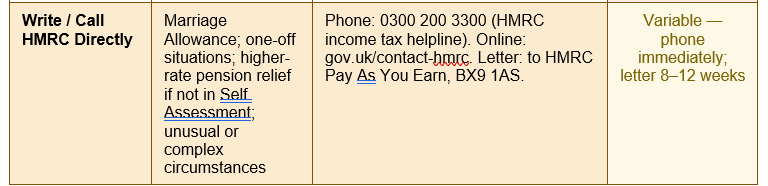

How to Claim Tax Relief: The Four Routes

Tax relief in the UK is claimed through one of four main routes, depending on the type of relief and your tax status. The table below maps each claim route to the reliefs it serves, how to access it, and how long it takes:

Worked Examples: How Much Could You Reclaim?

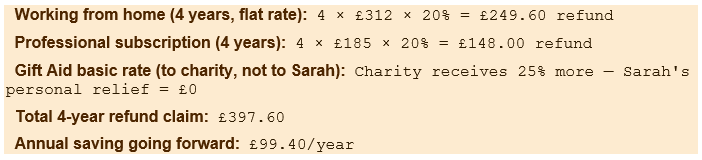

Example 1 — PAYE Employee (Basic Rate), 4-Year Backdate

Sarah is a nurse earning £35,000 per year (basic-rate taxpayer). She has worked partly from home for four years without claiming. She pays a Royal College of Nursing subscription of £185 per year unreimbursed. She donates £50 per month to charity under Gift Aid.

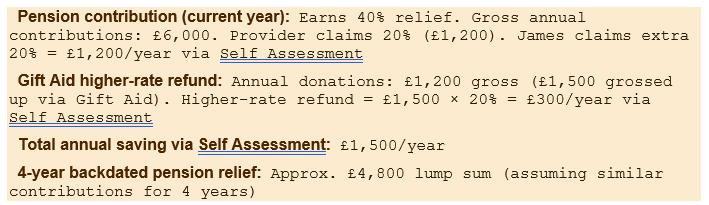

Example 2 — Higher-Rate Taxpayer with Multiple Missed Claims

James earns £65,000 and is in a relief-at-source workplace pension. He donates £100 per month to charity with Gift Aid. He has never filed a Self Assessment return to claim his higher-rate relief.

The Four-Year Backdating Window: Do Not Miss Your Deadline

Most PAYE tax relief claims can be backdated four complete tax years. As of the 2026/27 tax year, the currently open backdating window covers: 2022/23, 2023/24, 2024/25, and 2025/26. Each year's claim is submitted separately and generates a separate refund.The critical deadline note: the 2021/22 backdating window closed permanently on 5 April 2026. After a tax year's deadline passes, HMRC will not accept claims for that year under any circumstances — there is no appeal, no extension, and no hardship exception. This means every year you delay is a year of potential refund lost permanently. The 2022/23 deadline closes on 5 April 2027.

Self Assessment taxpayers follow different timing rules — reliefs are claimed on the annual return for the relevant tax year, subject to the same four-year principle but tied to the Self Assessment filing calendar. The online Self Assessment deadline is 31 January each year for the prior tax year, and the paper return deadline is 31 October.

The most expensive oversight for higher-rate taxpayers: Crossing the 40% income tax threshold and contributing to a relief-at-source pension without filing Self Assessment to claim the extra 20% is the single most common source of unclaimed tax relief in the UK. HMRC is holding that relief in a pot with your name on it — but they will not send it to you until you claim it. If you crossed the £50,270 threshold at any point in the last four tax years and contributed to a pension, check whether you have claimed all of your higher-rate pension relief. If you have not, register for Self Assessment at gov.uk, file your returns, and claim what belongs to you.

Common Tax Relief Mistakes to Avoid

- Only claiming the current year and ignoring the backlog: Many people claim one year of working from home relief and miss four years of entitlement. Always ask: have I been eligible for this relief for previous years? The backdating window is there precisely for this reason.

- Assuming salary sacrifice and relief at source deliver the same total benefit: They do not — salary sacrifice saves National Insurance as well as income tax. If your employer offers salary sacrifice, this is almost always the better option.

- Basic-rate pension savers assuming no further claim is possible: Basic-rate relief is added automatically, but the pension provider claims it — you should verify your provider is doing this and that contributions are being reported correctly.

- Donating to charity without ticking Gift Aid: The charity receives 25% less, at no benefit to you. If you are a UK taxpayer, always tick the Gift Aid box. It costs you nothing and benefits the charity meaningfully.

- Not registering for Self Assessment when higher-rate relief applies: Once your income crosses £50,270, higher-rate pension relief and Gift Aid higher-rate relief both require Self Assessment to claim. If you are not registered, you are not claiming.

- Claiming personal expenses as business costs: HMRC's automated systems in 2026 are significantly better at identifying patterns inconsistent with genuine business activity. Only claim costs that are genuinely and wholly incurred in performing your job.

Conclusion

Tax relief in the UK is not a technicality for accountants — it is a set of statutory entitlements that Parliament has created for every UK taxpayer, on specific expenditure and circumstances, that HMRC will honour in full when you claim. The reliefs covered in this guide — pension contributions, working from home, Marriage Allowance, Gift Aid, professional subscriptions, uniform allowances, and investment relief — together represent a landscape where most UK taxpayers can identify at least one and often several claims they have never made.The four-year backdating window means the cost of not claiming is cumulative. A basic-rate employee who has never claimed working from home relief or professional subscriptions may have four years of refunds waiting. A higher-rate taxpayer who has never filed Self Assessment to claim additional pension relief or Gift Aid may be owed thousands of pounds. The 2022/23 backdating window closes on 5 April 2027 — claims not made by that date for that tax year are permanently lost.

The claim process for most reliefs is simpler than it sounds. The HMRC online job expenses tool handles most PAYE claims in minutes. The Marriage Allowance application at gov.uk/marriage-allowance takes five minutes and applies automatically every year thereafter. Self Assessment, while requiring more time to set up, is a straightforward annual process once registered. The common thread across every claim in this guide is the same: HMRC holds the relief until you ask for it. This guide has shown you what to ask for, and how.

Frequently Asked Questions (FAQ)

What is tax relief and how does it work in the UK?

Tax relief is a reduction in the amount of income on which you pay tax, or in some cases a direct reduction in your tax bill. It works by HMRC allowing you to deduct certain qualifying expenditure from your taxable income — pension contributions, work expenses, charitable donations — before calculating the tax you owe. A basic-rate taxpayer (20%) saves 20p for every £1 of relief claimed. A higher-rate taxpayer (40%) saves 40p for every £1 of relief. For 2026/27, the key thresholds are: personal allowance £12,570 (no tax below this), basic rate 20% up to £50,270, higher rate 40% up to £125,140, and additional rate 45% above that.How do I claim tax relief if I am a PAYE employee?

Most PAYE employees can claim relief online through the HMRC job expenses tool at gov.uk. You log in with your Government Gateway credentials, enter the type of expense and the amount, and HMRC adjusts your tax code to reflect the relief — resulting in less tax being deducted from future pay, or a refund for overpaid tax. The types of relief you can claim this way include: working from home (£6/week flat rate or actual costs), professional subscriptions and union fees on HMRC's approved list, uniform cleaning allowances, and other job-specific expenses up to £2,500 per year. Claims can be backdated four years. If the online service does not cover your claim type, use Form P87 or contact HMRC directly.How many years can I backdate a tax relief claim?

You can backdate most UK tax relief claims for up to four complete tax years. As of the 2026/27 tax year (July 2026), the open backdating window covers: 2022/23, 2023/24, 2024/25, and 2025/26. The 2021/22 window closed permanently on 5 April 2026 — any unclaimed relief for that year cannot be recovered. The 2022/23 window closes on 5 April 2027. Each tax year is claimed separately as a standalone submission. Once a deadline passes, there is no appeal or extension — the relief is permanently lost. This is why it is important to claim as soon as you identify an entitlement rather than waiting.Do I need to register for Self Assessment to claim pension tax relief?

It depends on which tax rate you pay and how your pension is structured. Basic-rate taxpayers in relief-at-source pension schemes have the 20% relief added automatically by their pension provider — no Self Assessment is required. Higher-rate (40%) and additional-rate (45%) taxpayers who want to claim the extra relief above 20% must either register for Self Assessment and include pension contributions on their return, or write to HMRC to have their tax code adjusted. From September 2025, telephone pension relief claims were discontinued — you must use the online GOV.UK pension relief service or Self Assessment. If you have crossed the £50,270 threshold and have not claimed additional pension relief, registering for Self Assessment is strongly advisable.Can I claim tax relief on charitable donations?

Basic-rate taxpayers receive no personal relief from Gift Aid — the benefit flows entirely to the charity, which claims an additional 25p from HMRC for every £1 donated. To enable this, you must tick the Gift Aid box when donating and confirm you are a UK taxpayer who has paid sufficient tax to cover the claim. Higher-rate (40%) and additional-rate (45%) taxpayers can also claim the difference between their marginal rate and the 20% basic rate already claimed by the charity — worth 20% or 25% of the grossed-up donation, claimed through Self Assessment. This relief is backdatable four years. There is an additional application for those earning over £100,000, where Gift Aid donations reduce Adjusted Net Income and can restore the personal allowance, producing tax savings that significantly exceed the headline relief percentages.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. GOV.UK — Claim Tax Relief for Your Job Expenses (HMRC Official Tool)

https://www.gov.uk/tax-relief-for-employees

2. GOV.UK — Claim Income Tax Relief for Your Employment Expenses (P87 Form)

https://www.gov.uk/government/publications/claim-income-tax-relief-for-your-employment-expenses-p87

3. PocketWise — Tax Relief for Employees and Self-Employed UK 2026/27 (Updated 2026)

https://pocketwise.co.uk/tax/tax-relief/

4. PocketWise — Gift Aid Higher-Rate Tax Relief UK 2026/27 (May 3, 2026)

https://pocketwise.co.uk/tax/tax-relief/gift-aid-higher-rate-tax-relief/

5. Low Incomes Tax Reform Group (LITRG) — Gift Aid: Full Technical Guide (June 2026)

https://www.litrg.org.uk/tax-nic/income-tax/gift-aid

6. Pure Magazine — What Is Tax Relief? Save Money in 2026 (April 4, 2026)

https://puremagazine.co.uk/what-is-tax-relief/

7. GOV.UK — Marriage Allowance: Apply Online

https://www.gov.uk/marriage-allowance

8. GOV.UK — Self Assessment Tax Returns: Register and File

https://www.gov.uk/self-assessment-tax-returns

0 Comments Comments