Savings

What Is the 20% Savings Strategy? Accountant Explains

Table of Contents

- The Gap Between What People Save and What They Should

- What Is the 20% Savings Strategy?

- Why 20%? The Mathematics Behind the Target

- Pay Yourself First: The Mechanism That Makes 20% Automatic

- Where to Put Your 20%: The Priority Framework for UK and US Savers

- The 20% Strategy in Real Numbers: UK and US Income Examples

- How to Implement the 20% Savings Strategy: Step by Step

- What If 20% Is Not Currently Achievable?

- Conclusion

- Frequently Asked Questions (FAQ)

The Gap Between What People Save and What They Should

The average American saves approximately 4.6% of their income. Financial advisers, retirement planning research, and every major personal finance framework recommend saving at least 20%. The gap between 4.6% and 20% is not marginal — it is the difference between financial security and financial fragility, between retiring comfortably and working longer than intended, between having an emergency fund and being one unexpected bill away from credit card debt. The Penny Hoarder's State of Savings survey found that 48% of Americans save only what is left over after paying bills — treating savings as a residual afterthought rather than a planned first allocation. For those households, the result is entirely predictable: in most months, little or nothing is left.The 20% savings strategy is the most widely recommended personal finance rule for closing this gap. It is the savings component of the famous 50/30/20 budget rule (50% needs, 30% wants, 20% savings), it is the backbone of the 80/20 pay-yourself-first framework (20% to savings, 80% to everything else), and it is independently cited by Fidelity, Vanguard, NerdWallet, and virtually every major financial institution as the target savings rate for building long-term financial security. The strategy is simple in description: save 20% of your take-home pay every month, automatically, before discretionary spending begins. It is also genuinely challenging to implement for households where essential costs consume most of the budget — which is why understanding both the goal and the realistic path to reaching it matters as much as the target itself.

This guide explains the 20% savings strategy comprehensively: where the 20% figure comes from, what it can achieve over time with the compound interest mathematics behind it, how it relates to the pay-yourself-first and reverse budgeting approaches, the seven-priority framework for where to direct the 20% for maximum financial impact, the real-number examples at common UK and US income levels, the step-by-step implementation guide including automation, and what to do when 20% is not immediately achievable. Whether you are starting from scratch or reassessing a savings rate that has not kept pace with your income or ambitions, this guide provides the complete and practical framework.

What Is the 20% Savings Strategy?

The 20% savings strategy is a personal finance guideline that recommends setting aside 20% of your monthly after-tax (take-home) income for savings, investments, and debt repayment, before any discretionary spending takes place. It is a percentage-based approach rather than a fixed amount — meaning it scales automatically with income and applies equally to someone earning £1,500 per month and someone earning £8,000 per month.The strategy appears in several closely related frameworks. In the 50/30/20 budget rule, 20% is the savings and debt repayment allocation alongside 50% for needs and 30% for wants. In the 80/20 pay-yourself-first rule, you save 20% immediately on payday and spend the remaining 80% on both needs and wants without further categorical distinction. Both frameworks share the identical 20% savings rate — the difference is whether the remaining 80% is further subdivided into needs and wants (50/30/20) or left as undifferentiated spending (80/20). Wealthvieu's May 2026 guide confirms: 'The standard target is 20% of take-home pay. The 50/30/20 budget rule: the 50/30/20 framework allocates 50% of take-home to needs, 30% to wants, and 20% to savings and debt repayment.'

A common refinement of the 20% target, cited by Yahoo Finance (January 2026), divides it into two components: 15% for retirement savings (pension or equivalent long-term investment) and 5% for short-term savings goals such as an emergency fund, a house deposit, or other medium-term objectives. This internal split ensures that both short-term financial resilience and long-term wealth building receive consistent allocation rather than one consuming the entire 20% at the expense of the other.

The savings gap the 20% strategy closes: Average US savings rate: 4.6%. Saving 20% consistently places you in the top 25% of savers by rate — Wealthvieu (May 18, 2026): 'The average US personal savings rate is approximately 4.6% — well below the 20% target. Simply reaching 15% places you in the top 25% of savers by savings rate.' NerdWallet 2025 Savings Report: employed Americans report saving an average of 23% of take-home but nearly a quarter are unsure how much they are actually saving. Penny Hoarder State of Savings: 48% of Americans save only what is left over after bills. The gap between the average and the 20% recommendation produces an enormous wealth difference over a 30-year working life (Wealthvieu, 2026)

Why 20%? The Mathematics Behind the Target

The 20% savings rate is not an arbitrary number chosen for its roundness. It is grounded in the compound interest mathematics of retirement planning and financial resilience research. Fidelity's widely cited retirement savings benchmarks — based on the principle of replacing 70-80% of pre-retirement income to maintain the same standard of living — work backward to produce the savings rate required to reach that goal over a 40-year working life at a reasonable long-run investment return of approximately 7% annually. At 20%, most people can expect to retire with sufficient assets to fund 25 to 30 years of comparable living standards from investments alone.The compound interest case for 20% is most powerfully illustrated by the starting-age comparison that WalletGrower's 2026 analysis documents: someone who saves £500 per month (equivalent to 20% of a modest income) beginning at age 25 and investing at 7% average annual return accumulates approximately £1.32 million by age 65. The same £500 per month beginning at age 35 accumulates only £607,000 — less than half, despite saving for only 10 fewer years. The lost decade of compounding in the early career is more financially damaging than three decades of identical saving that begins later. At a 20% rate, starting early transforms an ordinary income into an extraordinary retirement outcome through the power of compound interest, time, and tax-efficient investment wrappers.

The automation research adds another dimension to the mathematical case. WalletGrower (2026) cites Vanguard's research: 'Participants who use automatic enrollment in 401(k) plans have a 92% participation rate versus 57% for those who must opt in manually.' This 35-percentage-point gap in participation rates translates directly into a massive difference in total retirement savings over a career. Wealthvieu confirms the broader principle: 'People who automate savings save 30-50% more than those who transfer manually.' The 20% target works when it is automatic — and substantially underperforms when it requires active monthly decisions.

The 15% retirement + 5% short-term split: The most commonly recommended internal allocation of the 20% savings target divides it into two purposeful streams. Yahoo Finance (January 2026) cites the standard guideline: 15% for retirement savings (directed to a pension, SIPP, 401(k), or Roth IRA for long-term compound growth) and 5% for short-term savings (emergency fund, house deposit, or other medium-term goals). This split ensures that immediate financial resilience (the emergency fund) is built alongside the long-term wealth accumulation that retirement savings represent. Directing all 20% to long-term investments while carrying no emergency fund leaves the plan vulnerable to derailment by the first unexpected expense. Directing all 20% to a cash emergency fund while ignoring long-term investing sacrifices decades of compound growth.

Pay Yourself First: The Mechanism That Makes 20% Automatic

The 20% savings strategy's most important implementation principle is the pay-yourself-first approach — the idea that savings should be the first financial transaction of every pay period, not the last. The Penny Hoarder's 2026 guide describes the mechanism: 'Pay yourself first means moving a set amount of money to savings or investments before paying any bills or spending on discretionary expenses. The phrase comes from the idea of treating your future self as the first bill each pay period.'The psychological and practical case for this sequencing is compelling. When savings is treated as what remains after all spending, the amount available varies month to month with expenses, is chronically reduced by unexpected costs, and depends on consistent monthly willpower to resist spending the available balance. PNC's pay-yourself-first guide identifies the core problem: 'Many people struggle to save regularly because they wait until the end of the month to see what's left over.' The Penny Hoarder's survey result quantifies the consequence of that habit: 48% of Americans save only what is left after bills — and in many months, nothing is left.

Reverse budgeting — the alternative name for the pay-yourself-first approach — flips this sequence entirely. The 20% is the first outflow of every pay period, automated before any discretionary spending can access it. The remaining 80% is what is available for all other purposes: rent, food, utilities, transport, wants, and entertainment. What you do not see, you do not spend. This is not willpower — it is structural design. Fidelity Bank notes: 'Automated transfers move money to savings before you have a chance to spend it, reducing impulse purchases.' PFCU (December 2025): 'The pay yourself first strategy flips traditional budgeting on its head. Instead of paying bills first and hoping money remains for savings, you move money into savings before spending a dime on anything else.'

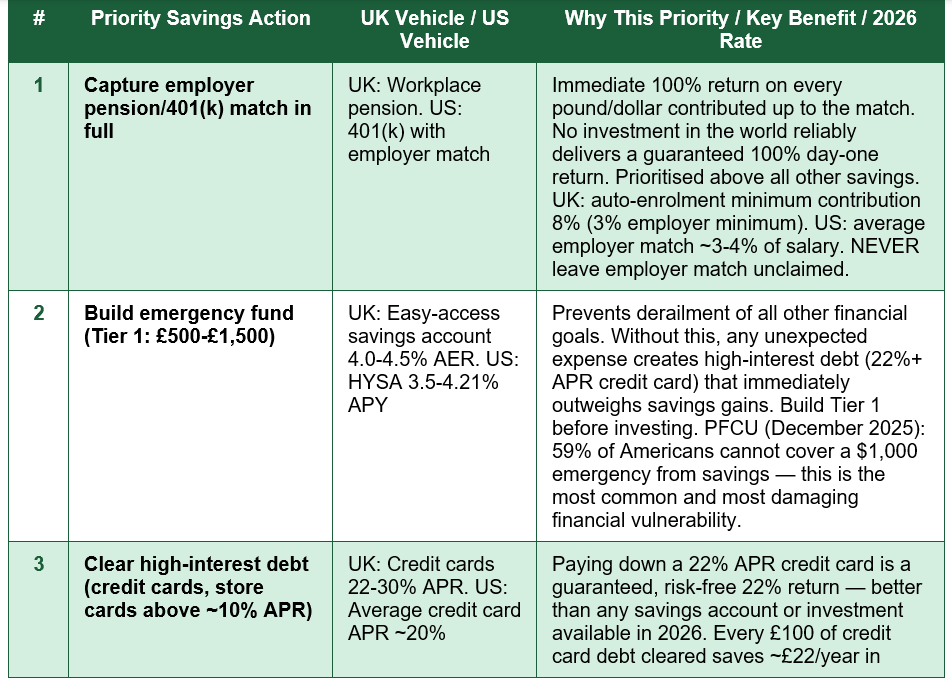

Where to Put Your 20%: The Priority Framework for UK and US Savers

Not all savings destinations are equally valuable. The order in which you direct the 20% matters significantly — some allocations produce guaranteed returns (employer match, debt clearance), others produce tax-advantaged compound growth (pension, ISA, Roth IRA), and others provide necessary liquidity (emergency fund). The priority framework below maximises the financial return on every pound or dollar of the 20% allocation:

Most people never reach priority 6 or 7 in the table above — and that is entirely fine. Consistently hitting priorities 1 through 5 (employer match, emergency fund Tier 1, high-interest debt clearance, full emergency fund, and retirement investing) puts you well ahead of the majority of savers and builds a financial structure that is genuinely resilient. The LISA (UK) at priority 6 and the general investment account at priority 7 are for those who have maximised all tax-advantaged wrappers available to them — a fortunate position that not everyone will reach with a 20% savings rate, but an aspirational target as income grows.

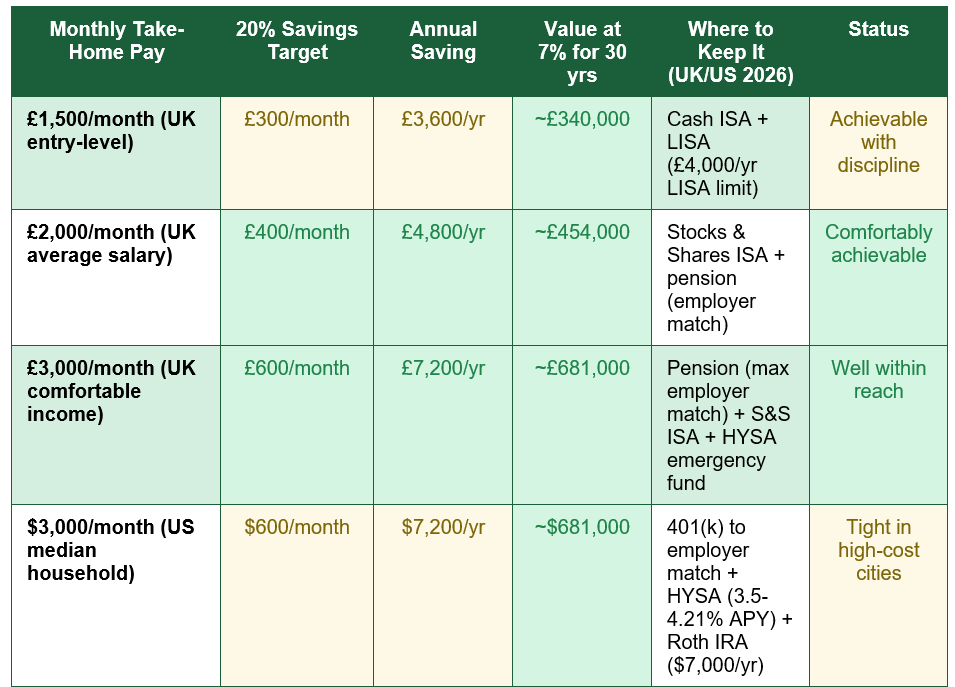

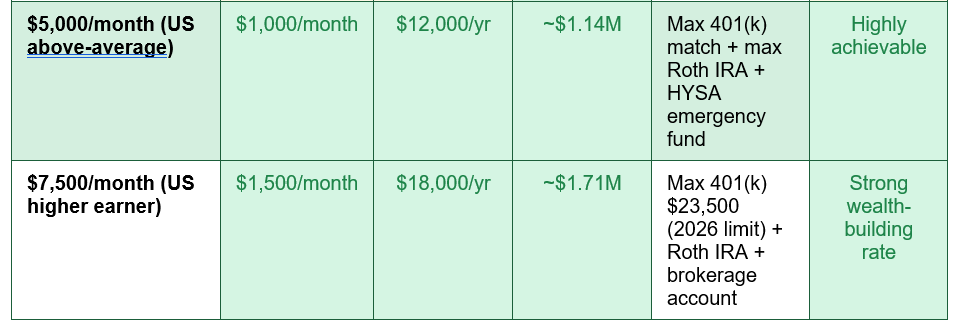

The 20% Strategy in Real Numbers: UK and US Income Examples

The table below shows exactly what 20% means in absolute terms at common UK and US income levels, the annual saving achieved, the approximate long-run value at a 7% annual return over 30 years, and the most appropriate UK or US savings vehicles for each level:

The long-term values in the table assume a 7% average annual return — the approximate long-run average real return from a globally diversified equity portfolio. They assume no additional contributions above the monthly savings amount and no employer match. Both assumptions are conservative: most working-age savers will also benefit from employer pension contributions and salary growth over time. Even at the most modest income level in the table (£1,500/month take-home, saving £300/month), the 20% strategy accumulates approximately £340,000 over 30 years at 7% — a meaningful retirement supplement, especially if state pension (UK) or Social Security (US) is also available.

How to Implement the 20% Savings Strategy: Step by Step

- Calculate your monthly after-tax take-home pay: Use your actual net bank deposit — after income tax, National Insurance (UK) or FICA taxes (US), and any pre-tax pension contributions already deducted by your employer. Do not use gross salary. If paid weekly or fortnightly, calculate the monthly equivalent. If self-employed or on variable income, use a conservative floor (the reliable minimum monthly income from the last six months).

- Calculate your 20% target: Multiply your monthly take-home by 0.20. This is your savings target. Write it down: it becomes the first standing order you set up. Also calculate the 15% retirement sub-target (multiply by 0.15) and the 5% short-term sub-target (multiply by 0.05).

- Open the right accounts before you automate: UK: Ensure you have a workplace pension enrolled (and that employer contributions are being made), a Cash ISA or easy-access savings account for the emergency fund component, and a Stocks and Shares ISA for long-term retirement investing. US: Ensure your 401(k) is enrolled up to the full employer match, open a Roth IRA at Fidelity, Vanguard, or Schwab if not already open, and open a high-yield savings account for the emergency fund.

- Set up automated transfers on payday: This single step produces the 30-50% improvement in savings outcomes that Vanguard and Wealthvieu document. Set up a standing order (UK) or automatic transfer (US) for the exact 20% amount to leave your account on the day your salary arrives or the day after. Direct the 5% emergency fund component to your HYSA/Cash ISA. Direct the 15% to your pension or investment ISA. The automation must happen before you see the money in your spending account.

- 5. Live on the remaining 80%: For the first one to three months, track whether your spending in the 80% bucket is covering all essential needs (rent, bills, food, transport, insurance) and any discretionary wants. If the 80% is insufficient to cover genuine essentials, adjust: temporarily reduce the savings rate to 15% or 10% while working to reduce essential costs (switch energy supplier, review subscriptions, meal plan to reduce food costs). The key is to keep the automation running at whatever rate is sustainable — any consistently saved percentage is better than zero.

- 6. Increase the rate by 1% every time income increases: PNC recommends this gradual escalation: 'Review your progress annually. At least once a year, evaluate how much you have saved and consider adjusting your contributions if your income has increased.' The most painless time to increase savings is when a pay rise arrives: before the higher income is incorporated into spending habits, redirect a portion of the increase directly to savings. Many UK pension providers and US 401(k) administrators support auto-escalation of contributions — enabling this feature is one of the highest-value financial actions available.

- 7. Review annually: Once per year — ideally at the start of the new tax year (April in the UK, January in the US) — review your savings rate, account performance, fee levels, and whether the allocation between retirement and short-term goals remains appropriate. Rebalance if one account has grown to represent too large a proportion of the total. Check whether you can increase the rate or access new tax-advantaged wrappers (the UK LISA, for example, is available to under-40s and provides a 25% government bonus).

THE AUTOMATION RULE — SET IT BEFORE YOU SPEND IT: The research is unambiguous: people who automate their savings save 30-50% more than those who transfer manually. The most effective implementation uses two automatic transfers set up on payday. Transfer 1: 5% of take-home pay to your emergency fund/short-term savings account (UK: Cash ISA or easy-access HYSA paying 4.0-4.5% AER. US: HYSA earning 3.5-4.21% APY). Transfer 2: 15% of take-home pay to your pension (to capture employer match) and Stocks & Shares ISA (UK) or additional 401(k)/Roth IRA (US). Name your accounts with specific goals — "Emergency Shield," "House Deposit 2028," "Retirement Fund" — research shows named accounts with clear purposes have significantly higher retention rates than unnamed savings pots.

What If 20% Is Not Currently Achievable?

For households where essential costs consume a large proportion of take-home pay — particularly in high-cost cities, on lower incomes, or during periods of high debt repayment — saving 20% immediately may not be feasible without making essential expenses unmanageable. This is a genuine constraint, not a personal failing, and the appropriate response is a phased approach rather than an all-or-nothing attempt.PNC's pay-yourself-first guide provides the standard phased recommendation: 'Determine a savings percentage. Ideally, aim to save at least 10% to 20% of your income. Start with what you can afford and gradually increase it over time.' The Penny Hoarder's 2026 guide recommends starting at 10% and increasing by 1 percentage point every few months: 'Beginners often start at 10% and increase the rate by a percentage point every few months.' This escalation approach works because each 1% increase is individually small enough to be absorbed by normal spending adjustment, but the cumulative movement from 10% to 20% over 12-24 months produces a major improvement in long-term savings outcomes.

The single non-negotiable minimum — regardless of income level — is to capture the employer pension match in full. An employer that matches pension contributions up to 3-5% of salary is offering a 100% return on those contributions with zero risk. Forfeiting that match by not contributing enough to capture it is the most expensive savings mistake available to any employed person. Even if the rest of the 20% target cannot be met immediately, every penny of employer match should be claimed. This minimum is independent of the rest of the strategy: it is not part of the 20% target — it is a prerequisite that should be achieved regardless of the overall savings rate.

THE 'SAVE WHAT'S LEFT' TRAP — WHY PASSIVE SAVING NEVER WORKS: The Penny Hoarder's State of Savings survey documents the fundamental problem: 48% of Americans save only what is left after bills. The predictable result: in most months, the amount remaining is insufficient to build meaningful savings; unexpected expenses consume what little remains; and the habit of saving never develops because it is conditional on months when nothing goes wrong. This is not a discipline problem — it is a system design problem. A system that makes saving the last allocation, subject to whatever remains after spending, will almost always produce inadequate savings regardless of income level. The 20% savings strategy succeeds precisely because it removes savings from the end of the spending sequence and makes it the first, automatic, non-negotiable outflow of every pay period. The structural change — not willpower — is what closes the gap between the 4.6% average and the 20% target.

Conclusion

The 20% savings strategy is the most widely recommended personal finance guideline because it is the savings rate that, applied consistently over a working life, produces genuine long-term financial security. The average savings rate of 4.6% in the US — and the fact that 48% of people save only what is left after bills — illustrates both how far most households fall short of this target and why the gap matters so profoundly. WalletGrower's 2026 compound interest comparison makes the stakes concrete: saving £500 per month from age 25 produces £1.32 million by 65 at 7% average annual return. Waiting until 35 to begin the identical saving produces only £607,000. The mathematically most impactful decade of a person's financial life is the earliest one — and the 20% strategy is the framework most likely to capture it productively.The priority framework in this guide — employer match first, emergency fund second, high-interest debt third, full emergency fund fourth, retirement investing fifth — maximises the financial return on every pound or dollar of the 20% allocation. Employer pension matches represent guaranteed, risk-free 100% returns. High-interest debt clearance at 22% APR produces a guaranteed 22% return. Retirement investing in ISAs and pensions builds tax-free compound growth over decades. Each priority has a different risk-return profile and a different time horizon, and directing the 20% in the right sequence ensures that the most valuable opportunities are captured first.

The implementation imperative is automation. Vanguard's research on 401(k) auto-enrollment (92% participation rate vs 57% manual) and the broader finding that automated savers save 30-50% more than manual savers both point to the same conclusion: the most important single step in any savings strategy is setting up the automatic transfer before spending begins. The 20% savings strategy does not require exceptional discipline, unusual sacrifice, or complex financial expertise. It requires one afternoon to open the right accounts, one standing order set up on payday, and one annual review to adjust for income changes. The discipline is built into the structure, not demanded of the person. That structural simplicity — saving first, spending the rest — is precisely what makes the 20% strategy the most reliably effective personal finance habit available to ordinary earners at any income level.

0 Comments Comments