Business

Founders and Investors: It's a Two-Way Street

Investors shouldn't hold all the cards. Founders shouldn't raise too early and gift away the leverage before terms are even set. The relationship between a founder and an investor is genuinely bilateral — a long-term partnership in which both sides bring things the other cannot build alone. This guide unpacks the power dynamics, the structural forces that shift leverage before and after a term sheet is signed, and the practical playbook for founders who want to negotiate from strength without burning relationships.

Investors need founders as much as founders need investors. A venture capital fund that cannot deploy capital into high-quality companies returns nothing to its limited partners. A fund that consistently offers punitive terms acquires a reputation that ensures the best founders — those who have alternatives — choose to raise elsewhere. The investor is not doing the founder a favour by writing a cheque; they are making a calculated bet that the founder's company will generate returns that justify the risk. Both parties need the deal to work.

The power imbalance in founder-investor relationships is real but contextual, not structural. As Faurilaw's December 2025 analysis of negotiation dynamics states: 'Negotiation leverage is temporal, not positional.' The party with leverage at any given moment is the party with the better BATNA — the Best Alternative to a Negotiated Agreement. Before you have a term sheet, your leverage is limited by your BATNA: if declining this deal means stopping the company, your BATNA is weak. If declining this deal means accepting one of two competing term sheets, your BATNA is strong. Understanding how to improve your BATNA before entering negotiations is the single most important preparation a founder can do.

Negotiating with investors is less about 'winning' a battle and more about architecting a long-term marriage where you still own the house. As a founder, your leverage is your vision and your growth metrics; their leverage is the capital you need to scale.

— ALEX ARNOT, ANGEL INVESTMENT NETWORK — STARTUP ESSENTIALS: TOP 10 TIPS WHEN NEGOTIATING WITH INVESTORS (FEBRUARY 2026)

Venture capital funds operate under a power law return model. The mathematics are unforgiving: a fund needs its best investment to return the entire fund (and ideally more), because the majority of portfolio companies will return little or nothing. This means every investor is looking for potential outliers — companies that could grow ten to a hundred times in value. An investor who places a bet on a company and then actively destroys the founder's motivation through aggressive control terms, excessive board interference, or unrealistic milestone pressure is undermining the very return they are seeking. The best investors understand this and treat founder autonomy not as a concession but as an investment in the outcome.

Qubit Capital's April 2026 analysis of VC relationships identifies several things investors genuinely need from founders beyond simple financial returns: consistent, transparent communication about both progress and setbacks; early flagging of problems rather than late-stage revelation that forecloses options; the operational judgement to make good decisions under uncertainty; and the leadership quality to build and retain a team. Founders who provide these things are easier to back, easier to support, and generate better outcomes — which is why the best investors treat the relationship as genuinely bilateral rather than transactional.

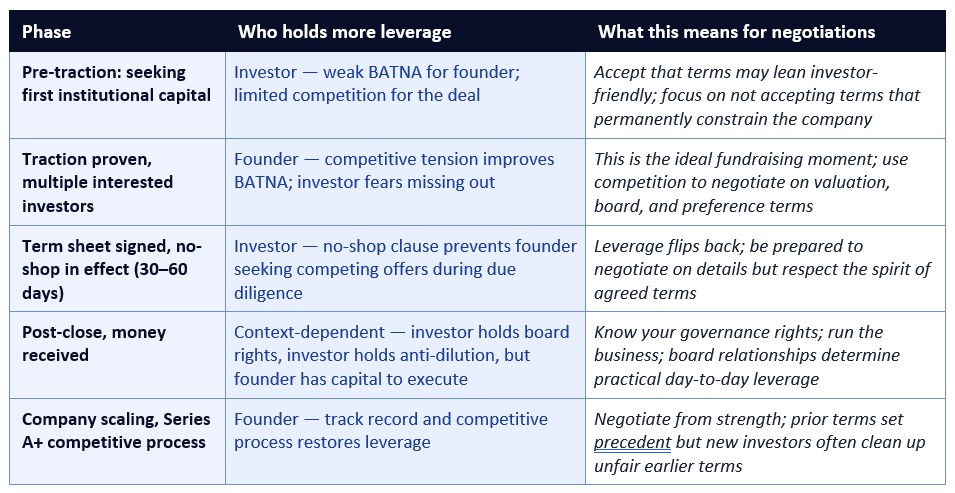

The mechanism is straightforward. When you raise early without traction, your BATNA is weak — you have few or no alternative investors interested, no revenue or user metrics to anchor valuation discussions, and potentially a time pressure created by a runway that is already short. This combination gives the investor significant pricing power. They can offer a low valuation, heavy preference terms, board control provisions, and aggressive protective provisions — and you may feel compelled to accept them because the alternative is running out of money.

The investor who receives these terms has not done anything wrong in seeking them — they are managing their own risk in a rational way given the information available. But the founder who has structured the situation to have no leverage has made a mistake that cannot be unwound. Anti-dilution provisions, liquidation preferences, and board composition decisions made at the seed stage can constrain the company's options for years. A two-times liquidation preference negotiated when the company had no leverage can prevent any financial return reaching the founders at all in an acquisition scenario unless the exit price is high enough.

The alternative is to raise from a position of developed traction, competitive tension, and clear conviction. This requires doing more with less before approaching investors — bootstrapping, using revenue, finding non-dilutive funding sources — but it produces fundamentally better outcomes in negotiation. As Faurilaw's December 2025 analysis notes, 'the founder's primary advantage is often time and singular focus.' Using that advantage to build a genuinely compelling case before the negotiation begins is the most effective use of it.

Faurilaw's December 2025 analysis describes this precisely: 'Negotiation leverage is not a fixed asset but a shifting force determined by the BATNA and the competitive tension created by multiple credible funding sources.' Before entering any fundraise, a founder should ask: what happens if this investor says no or offers unacceptable terms? If the honest answer is 'the company runs out of money within three months,' the BATNA is weak and the negotiating position will reflect that. If the honest answer is 'we continue growing on current revenue, approach one of three other interested investors, or accept a bridge from existing angels,' the BATNA is materially stronger.

The practical implication is that improving your BATNA before you need it is more valuable than any negotiating tactic during the conversation itself. Building revenue before raising, extending runway through cost management, and generating investor interest through warm introductions before you are actively in a process — all of these strengthen your BATNA and therefore your negotiating position. The investor who knows you have options must negotiate more fairly than the investor who knows you have none.

The BATNA also matters for investors. A lead investor who has spent six months building a relationship with a founder, conducted deep due diligence, and prepared a term sheet has a weak BATNA in the final negotiation — the cost of walking away from the deal at that stage is very high in time, reputation, and fund deployment pressure. An experienced founder who understands this dynamic can use it constructively, not to extract unreasonable terms, but to ensure that the investor who has already committed this much attention will stretch slightly on terms that matter most.

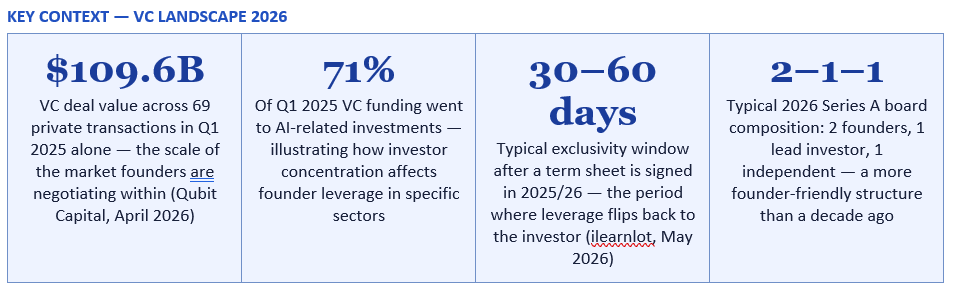

Ilearnlot's May 2026 analysis of 2025/26 Series A term sheet structures identifies the following as the current market standard: 1x non-participating liquidation preference (meaning investors get their money back once, not participating in remaining proceeds); weighted-average anti-dilution (a moderate protection against down rounds, not the punitive full ratchet); and a board composition of two founders, one lead investor, and one independent director — giving founders majority board control. The analysis notes: 'YC-friendly/many 2025–2026 Series A term sheets: founders control majority of the board (e.g., 2 founders, 1 lead investor, 1 independent), which helps retain operational control.'

What is not founder-friendly but still appears in some term sheets includes: 2x or higher liquidation preferences (meaning investors take twice their investment before founders see any proceeds in most exit scenarios); full ratchet anti-dilution (which adjusts the investor's price to the lowest future price, potentially wiping out founder equity in a down round); pay-to-play provisions that restrict future fundraising; and weighted voting provisions that give investors blocking rights on routine business decisions. Ilearnlot notes: 'Full ratchet (your price adjusts down to the lowest future price) — highly founder-unfriendly.' and 'Pay-to-play — can severely restrict your future fundraising flexibility.'

A no-shop clause — standard in term sheets and typically running for 30 to 60 days — prohibits the founder from seeking or accepting alternative investment offers during the due diligence period. The rationale is reasonable: due diligence is expensive and time-consuming for the investor, and they need assurance that the founder is not using their term sheet as leverage to get a better offer elsewhere while letting the investor do the investigative work. In exchange for accepting the no-shop, founders typically receive a degree of exclusivity commitment and good-faith progression toward close.

The practical effect, as Faurilaw's December 2025 analysis documents, is a 'leverage flip': 'Once a term sheet is signed and a no-shop clause takes effect, the advantage shifts back to the investor during the due diligence phase.' During due diligence, the investor has the ability to re-examine every assumption in the deal, raise concerns, and request re-trading of terms — while the founder has no competitive alternatives to use as counterpressure. Issues that were glossed over in the headline term sheet negotiation may resurface during due diligence as investor-requested changes to specific provisions.

The defence against this is thorough preparation before signing. Every representation the company makes in due diligence should be accurate and supportable. Every term that matters should be negotiated and agreed in the term sheet itself before it is signed — because after signing, your ability to resist re-trading requests is structurally weaker. The 30 to 60 day no-shop window is not a period to continue negotiating; it is a period to complete the process on the basis of what was agreed.

Competitive tension works because it directly improves the founder's BATNA. When an investor knows you have alternative term sheets — or credible alternatives in process — their BATNA is that you accept a competing offer. This constrains how aggressively they can push on terms. An investor who knows they are the only option has no such constraint. The difference in behaviour between an investor negotiating in a competitive process and one negotiating as the sole option is significant and predictable.

Building competitive tension is easier when you start the process early, run a parallel process with multiple investors simultaneously rather than sequentially, and create scarcity through a defined fundraising timeline. As the Angel Investment Network's February 2026 guide advises: 'Congratulations on getting to the table. Negotiating with investors is less about winning a battle and more about architecting a long-term marriage where you still own the house.' You own the house better when multiple people want to invest in the neighbourhood.

The important qualification is that competitive tension should be real, not manufactured. Claiming to have competing offers you do not have is dishonest and will be discovered — the VC community is small and well-connected, and a reputation for misrepresentation in fundraising conversations is lasting and damaging. The sustainable version is to build genuine interest from multiple parties through outstanding work, warm introductions, and a compelling narrative — and then to run the process professionally so that interested parties move through due diligence on a coordinated timeline.

Capnamic's analysis of investor-founder power dynamics makes this explicit: 'As a mandatory part of due diligence from the founder on me, I will ask the founder to look in the market for references about myself to get better gut feeling around me as an investor.' The investor in this case is explicitly welcoming and expecting reference checks. Founders who do not conduct them are leaving important information on the table.

What should founders investigate about prospective investors? The key questions are: How has this investor behaved with portfolio companies in difficult situations — down rounds, pivots, missed milestones? Do they have a reputation for re-trading terms, for passive-aggressive board behaviour, or for pushing out founding CEOs during growth phases? Do they follow through on the value-add commitments (introductions, hiring support, strategic advice) they make during the courtship phase? Are their portfolio companies genuinely willing to give enthusiastic references, or do founders describe the relationship as tolerable rather than valuable?

The check should be structured. Speak to two or three portfolio founders who have experienced both good and difficult periods with this investor — easy references are uninformative. Ask specific questions: Did the investor behave supportively during a difficult board meeting? Did they follow through on specific introductions they promised? Have they ever pushed to replace a founding CEO and under what circumstances? The answers will tell you whether you are signing up for a partner or an adversary.

Qubit Capital's April 2026 research on investor-founder relationships identifies the critical elements that determine relationship quality over time: clear and consistent communication, particularly during difficult periods; transparent reporting that does not sugarcoat problems until they become crises; shared goal alignment that is revisited as the company's direction evolves; and proactive use of the investor's network and expertise rather than treating them purely as capital providers.

Capnamic's investor perspective captures a dynamic that founders should understand: 'As I am aware of the change in power dynamics after the money has been wired, I will try to set an anchor by using some time to advertise the smartness of the money that I am going to invest through value adding services.' The investor is consciously managing the transition from pre-investment courtship to post-investment partnership — an acknowledgement that the power dynamic does shift once capital is deployed and that good investors actively work to maintain a constructive relationship despite that shift.

The best post-investment relationships share three characteristics. First, the founder treats the investor as a partner in solving problems, not a manager to be managed or a threat to be contained. Second, the investor treats the founder's operational autonomy as an asset to be protected, not a risk to be managed through intervention. Third, both parties communicate about what is not working before it reaches a crisis — the problems that destroy investor-founder relationships are almost always ones that were visible months before they became unmanageable, where neither party had the conversation that could have resolved them.

The practical takeaway is consistent with the data: build your BATNA before you need it, raise when you have traction rather than when you are desperate, negotiate governance terms as carefully as valuation, and invest in the post-close relationship with the same energy you invested in the courtship. The best founder-investor partnerships are not the product of clever negotiating tactics — they are the product of mutual respect, shared conviction about what the company can become, and the kind of honest, early communication that prevents small problems from becoming catastrophic ones. That is what a two-way street actually looks like.

Qubit Capital — 21 Ways to Strengthen Investor-Founder Relationships for Startup Success (December 2025) https://qubit.capital/blog/investor-founder-relationships

Qubit Capital — How Do Founders Build Venture Capital Relationships (April 2026) https://qubit.capital/blog/venture-capital-relationships

Ilearnlot — Term Sheet Negotiation for Founders in 2026 (May 2026) https://www.ilearnlot.com/term-sheet-negotiation-for-founders/2825341/

Angel Investment Network — Startup Essentials: Top 10 Tips When Negotiating With Investors (February 2026) https://www.angelinvestmentnetwork.net/startup-essentials-top-10-tips-when-negotiating-with-investors/

Capnamic — Power Dynamics in Investor-Founder Relations https://capnamic.com/post/power-dynamics-in-investor-founder-relations

NVCA — 2025 Model Legal Documents for VC Transactions (updated 2025) https://nvca.org/model-legal-documents/

Y Combinator — Safe Financing Documents and Standard Seed Round Terms https://www.ycombinator.com/documents

First Round Capital — The Dos and Don'ts of Fundraising (founder resource library) https://review.firstround.com/the-dos-and-donts-of-fundraising

TABLE OF CONTENTS

- The Myth of the All-Powerful Investor

- What Investors Actually Need From Founders

- Why Raising Too Early Destroys Founder Leverage

- The Leverage Timeline: Who Holds the Cards and When

- BATNA: The Concept Every Founder Must Understand

- What 'Founder-Friendly' Really Means in 2026 Term Sheets

- The Term Sheet Clauses That Actually Matter

- The No-Shop Clause: Where Leverage Flips

- Building Competitive Tension: The Only Sustainable Leverage Strategy

- Due Diligence Goes Both Ways: How to Vet Your Investor

- The Long-Term Relationship After the Money Is Wired

- What Good Investor-Founder Partnerships Look Like

- The Practical Negotiation Framework for Founders in 2026

- Conclusion

- Frequently Asked Questions

- References

The Myth of the All-Powerful Investor

The prevailing narrative in most startup ecosystems treats the investor as the powerful party and the founder as the supplicant. The founder pitches. The investor decides. The founder takes whatever terms are offered and is grateful to receive funding at all. This narrative is not just unflattering to founders — it is structurally incorrect, and accepting it as accurate going into a fundraise is one of the most expensive mistakes a founder can make.Investors need founders as much as founders need investors. A venture capital fund that cannot deploy capital into high-quality companies returns nothing to its limited partners. A fund that consistently offers punitive terms acquires a reputation that ensures the best founders — those who have alternatives — choose to raise elsewhere. The investor is not doing the founder a favour by writing a cheque; they are making a calculated bet that the founder's company will generate returns that justify the risk. Both parties need the deal to work.

The power imbalance in founder-investor relationships is real but contextual, not structural. As Faurilaw's December 2025 analysis of negotiation dynamics states: 'Negotiation leverage is temporal, not positional.' The party with leverage at any given moment is the party with the better BATNA — the Best Alternative to a Negotiated Agreement. Before you have a term sheet, your leverage is limited by your BATNA: if declining this deal means stopping the company, your BATNA is weak. If declining this deal means accepting one of two competing term sheets, your BATNA is strong. Understanding how to improve your BATNA before entering negotiations is the single most important preparation a founder can do.

Negotiating with investors is less about 'winning' a battle and more about architecting a long-term marriage where you still own the house. As a founder, your leverage is your vision and your growth metrics; their leverage is the capital you need to scale.

— ALEX ARNOT, ANGEL INVESTMENT NETWORK — STARTUP ESSENTIALS: TOP 10 TIPS WHEN NEGOTIATING WITH INVESTORS (FEBRUARY 2026)

What Investors Actually Need From Founders

The founder-investor relationship looks different from the other side of the table — and understanding what investors genuinely need is as important as understanding what you need from them. This is not a soft observation about empathy. It is a strategic point: the more clearly you understand an investor's constraints, incentives, and needs, the more effectively you can structure a negotiation in which both parties feel they have achieved something valuable.Venture capital funds operate under a power law return model. The mathematics are unforgiving: a fund needs its best investment to return the entire fund (and ideally more), because the majority of portfolio companies will return little or nothing. This means every investor is looking for potential outliers — companies that could grow ten to a hundred times in value. An investor who places a bet on a company and then actively destroys the founder's motivation through aggressive control terms, excessive board interference, or unrealistic milestone pressure is undermining the very return they are seeking. The best investors understand this and treat founder autonomy not as a concession but as an investment in the outcome.

Qubit Capital's April 2026 analysis of VC relationships identifies several things investors genuinely need from founders beyond simple financial returns: consistent, transparent communication about both progress and setbacks; early flagging of problems rather than late-stage revelation that forecloses options; the operational judgement to make good decisions under uncertainty; and the leadership quality to build and retain a team. Founders who provide these things are easier to back, easier to support, and generate better outcomes — which is why the best investors treat the relationship as genuinely bilateral rather than transactional.

Why Raising Too Early Destroys Founder Leverage

One of the most counterintuitive pieces of fundraising advice — and one of the most important — is that raising money too early is not just premature, it is strategically damaging. Founders who raise before they have meaningful traction, product-market fit signals, or competitive fundraising interest enter the negotiation at their maximum vulnerability. They are asking for money they need urgently from people who do not yet have compelling evidence that this company will generate returns. The result, predictably, is investor-friendly terms.The mechanism is straightforward. When you raise early without traction, your BATNA is weak — you have few or no alternative investors interested, no revenue or user metrics to anchor valuation discussions, and potentially a time pressure created by a runway that is already short. This combination gives the investor significant pricing power. They can offer a low valuation, heavy preference terms, board control provisions, and aggressive protective provisions — and you may feel compelled to accept them because the alternative is running out of money.

The investor who receives these terms has not done anything wrong in seeking them — they are managing their own risk in a rational way given the information available. But the founder who has structured the situation to have no leverage has made a mistake that cannot be unwound. Anti-dilution provisions, liquidation preferences, and board composition decisions made at the seed stage can constrain the company's options for years. A two-times liquidation preference negotiated when the company had no leverage can prevent any financial return reaching the founders at all in an acquisition scenario unless the exit price is high enough.

The alternative is to raise from a position of developed traction, competitive tension, and clear conviction. This requires doing more with less before approaching investors — bootstrapping, using revenue, finding non-dilutive funding sources — but it produces fundamentally better outcomes in negotiation. As Faurilaw's December 2025 analysis notes, 'the founder's primary advantage is often time and singular focus.' Using that advantage to build a genuinely compelling case before the negotiation begins is the most effective use of it.

The Leverage Timeline: Who Holds the Cards and When

Leverage in a startup fundraise is not static — it shifts through distinct phases, and understanding where you are in this timeline determines what negotiating strategies are available to you.BATNA: The Concept Every Founder Must Understand

BATNA — Best Alternative to a Negotiated Agreement — is the single most important concept in any negotiation. Your BATNA is what you will do if this deal falls through. An investor's BATNA is what they will do if you walk away from their term sheet. The party with the stronger BATNA has more leverage, because they can credibly walk away from a bad deal without catastrophic consequences.Faurilaw's December 2025 analysis describes this precisely: 'Negotiation leverage is not a fixed asset but a shifting force determined by the BATNA and the competitive tension created by multiple credible funding sources.' Before entering any fundraise, a founder should ask: what happens if this investor says no or offers unacceptable terms? If the honest answer is 'the company runs out of money within three months,' the BATNA is weak and the negotiating position will reflect that. If the honest answer is 'we continue growing on current revenue, approach one of three other interested investors, or accept a bridge from existing angels,' the BATNA is materially stronger.

The practical implication is that improving your BATNA before you need it is more valuable than any negotiating tactic during the conversation itself. Building revenue before raising, extending runway through cost management, and generating investor interest through warm introductions before you are actively in a process — all of these strengthen your BATNA and therefore your negotiating position. The investor who knows you have options must negotiate more fairly than the investor who knows you have none.

The BATNA also matters for investors. A lead investor who has spent six months building a relationship with a founder, conducted deep due diligence, and prepared a term sheet has a weak BATNA in the final negotiation — the cost of walking away from the deal at that stage is very high in time, reputation, and fund deployment pressure. An experienced founder who understands this dynamic can use it constructively, not to extract unreasonable terms, but to ensure that the investor who has already committed this much attention will stretch slightly on terms that matter most.

What 'Founder-Friendly' Really Means in 2026 Term Sheets

The term 'founder-friendly' has become a marketing phrase used by almost every VC firm regardless of their actual term practices. Understanding what it means in concrete, 2026 market terms — rather than as a brand claim — is essential for any founder evaluating a term sheet.Ilearnlot's May 2026 analysis of 2025/26 Series A term sheet structures identifies the following as the current market standard: 1x non-participating liquidation preference (meaning investors get their money back once, not participating in remaining proceeds); weighted-average anti-dilution (a moderate protection against down rounds, not the punitive full ratchet); and a board composition of two founders, one lead investor, and one independent director — giving founders majority board control. The analysis notes: 'YC-friendly/many 2025–2026 Series A term sheets: founders control majority of the board (e.g., 2 founders, 1 lead investor, 1 independent), which helps retain operational control.'

What is not founder-friendly but still appears in some term sheets includes: 2x or higher liquidation preferences (meaning investors take twice their investment before founders see any proceeds in most exit scenarios); full ratchet anti-dilution (which adjusts the investor's price to the lowest future price, potentially wiping out founder equity in a down round); pay-to-play provisions that restrict future fundraising; and weighted voting provisions that give investors blocking rights on routine business decisions. Ilearnlot notes: 'Full ratchet (your price adjusts down to the lowest future price) — highly founder-unfriendly.' and 'Pay-to-play — can severely restrict your future fundraising flexibility.'

The Term Sheet Clauses That Actually Matter

Founders negotiating their first term sheet often focus on valuation — the number that determines ownership percentage — while underweighting the governance and preference terms that may ultimately have greater practical impact on outcomes. This is a prioritisation error.The term sheet clauses every founder must negotiate carefully

- Liquidation preference: This determines how proceeds are distributed in an acquisition or other liquidity event. A 1x non-participating preference means investors get their money back first, and then the remaining proceeds are distributed pro-rata by ownership. A 2x participating preference means investors get twice their money back AND participate in the remaining proceeds — significantly reducing founder returns in most exit scenarios. The market standard in 2025/26 is 1x non-participating. Any higher multiple or participation right should be resisted unless you have no alternatives.

- Anti-dilution provisions: These protect investors if the company raises a future round at a lower valuation (a 'down round'). Weighted-average anti-dilution is the current market standard and provides moderate protection. Full ratchet anti-dilution — which adjusts the investor's conversion price to the lowest future price — is highly punitive in down round scenarios and has become rare in founder-friendly markets, though it still appears in weaker negotiating positions. Carve out standard employee option issuances from anti-dilution calculations.

- Board composition: Who controls the board largely determines who controls the company. In a 2-1-1 structure (two founders, one lead investor, one independent), founders retain majority control and can outvote the investor on most decisions, though major decisions typically require the independent director's alignment. An equal split (2-2 with an independent) creates deadlock risk. An investor-majority board means the investor can theoretically remove the founder-CEO — a risk that is not theoretical in difficult times.

- Protective provisions (investor veto rights): These give investors blocking rights on specific decisions — new share issuances, acquisitions, debt above a threshold, hiring of C-suite executives. Standard protective provisions cover genuine risk-management scenarios. Aggressive protective provisions that give investors veto rights over ordinary business decisions are an overreach that founders should resist. As Ilearnlot's May 2026 analysis notes, these provisions 'determine who runs the company.'

- Pro-rata rights: The right for investors to participate in future funding rounds at their existing ownership percentage. This is standard and generally reasonable — it protects existing investors from dilution. Founders should be aware of the implications when multiple investors hold pro-rata rights across a cap table, as it can constrain how much a Series A round is available to new investors.

The No-Shop Clause: Where Leverage Flips

The moment a term sheet is signed and a no-shop clause takes effect, the leverage in the negotiation structurally shifts from founder to investor. This is one of the most important dynamics in startup fundraising and one that founders frequently underestimate.A no-shop clause — standard in term sheets and typically running for 30 to 60 days — prohibits the founder from seeking or accepting alternative investment offers during the due diligence period. The rationale is reasonable: due diligence is expensive and time-consuming for the investor, and they need assurance that the founder is not using their term sheet as leverage to get a better offer elsewhere while letting the investor do the investigative work. In exchange for accepting the no-shop, founders typically receive a degree of exclusivity commitment and good-faith progression toward close.

The practical effect, as Faurilaw's December 2025 analysis documents, is a 'leverage flip': 'Once a term sheet is signed and a no-shop clause takes effect, the advantage shifts back to the investor during the due diligence phase.' During due diligence, the investor has the ability to re-examine every assumption in the deal, raise concerns, and request re-trading of terms — while the founder has no competitive alternatives to use as counterpressure. Issues that were glossed over in the headline term sheet negotiation may resurface during due diligence as investor-requested changes to specific provisions.

The defence against this is thorough preparation before signing. Every representation the company makes in due diligence should be accurate and supportable. Every term that matters should be negotiated and agreed in the term sheet itself before it is signed — because after signing, your ability to resist re-trading requests is structurally weaker. The 30 to 60 day no-shop window is not a period to continue negotiating; it is a period to complete the process on the basis of what was agreed.

Building Competitive Tension: The Only Sustainable Leverage Strategy

The single most effective way to improve your negotiating position in a fundraise is to have multiple credible investors genuinely interested simultaneously. This is not a negotiating tactic — it is the structural creation of competitive tension that produces better terms, faster processes, and more respectful negotiations as a natural consequence.Competitive tension works because it directly improves the founder's BATNA. When an investor knows you have alternative term sheets — or credible alternatives in process — their BATNA is that you accept a competing offer. This constrains how aggressively they can push on terms. An investor who knows they are the only option has no such constraint. The difference in behaviour between an investor negotiating in a competitive process and one negotiating as the sole option is significant and predictable.

Building competitive tension is easier when you start the process early, run a parallel process with multiple investors simultaneously rather than sequentially, and create scarcity through a defined fundraising timeline. As the Angel Investment Network's February 2026 guide advises: 'Congratulations on getting to the table. Negotiating with investors is less about winning a battle and more about architecting a long-term marriage where you still own the house.' You own the house better when multiple people want to invest in the neighbourhood.

The important qualification is that competitive tension should be real, not manufactured. Claiming to have competing offers you do not have is dishonest and will be discovered — the VC community is small and well-connected, and a reputation for misrepresentation in fundraising conversations is lasting and damaging. The sustainable version is to build genuine interest from multiple parties through outstanding work, warm introductions, and a compelling narrative — and then to run the process professionally so that interested parties move through due diligence on a coordinated timeline.

Due Diligence Goes Both Ways: How to Vet Your Investor

Most founders think of due diligence as something investors do to them. The more useful framing is that due diligence is something both parties should do to each other — and that a founder who neglects to investigate their prospective investors thoroughly is making a significant mistake.Capnamic's analysis of investor-founder power dynamics makes this explicit: 'As a mandatory part of due diligence from the founder on me, I will ask the founder to look in the market for references about myself to get better gut feeling around me as an investor.' The investor in this case is explicitly welcoming and expecting reference checks. Founders who do not conduct them are leaving important information on the table.

What should founders investigate about prospective investors? The key questions are: How has this investor behaved with portfolio companies in difficult situations — down rounds, pivots, missed milestones? Do they have a reputation for re-trading terms, for passive-aggressive board behaviour, or for pushing out founding CEOs during growth phases? Do they follow through on the value-add commitments (introductions, hiring support, strategic advice) they make during the courtship phase? Are their portfolio companies genuinely willing to give enthusiastic references, or do founders describe the relationship as tolerable rather than valuable?

The check should be structured. Speak to two or three portfolio founders who have experienced both good and difficult periods with this investor — easy references are uninformative. Ask specific questions: Did the investor behave supportively during a difficult board meeting? Did they follow through on specific introductions they promised? Have they ever pushed to replace a founding CEO and under what circumstances? The answers will tell you whether you are signing up for a partner or an adversary.

The Long-Term Relationship After the Money Is Wired

The negotiation ends when the money is wired. The relationship is just beginning. And the relationship phase is longer, more complex, and more consequential than any individual negotiation. Founders who win every negotiating point on the term sheet but build a poor relationship with their investors in the months and years after closing have not actually won.Qubit Capital's April 2026 research on investor-founder relationships identifies the critical elements that determine relationship quality over time: clear and consistent communication, particularly during difficult periods; transparent reporting that does not sugarcoat problems until they become crises; shared goal alignment that is revisited as the company's direction evolves; and proactive use of the investor's network and expertise rather than treating them purely as capital providers.

Capnamic's investor perspective captures a dynamic that founders should understand: 'As I am aware of the change in power dynamics after the money has been wired, I will try to set an anchor by using some time to advertise the smartness of the money that I am going to invest through value adding services.' The investor is consciously managing the transition from pre-investment courtship to post-investment partnership — an acknowledgement that the power dynamic does shift once capital is deployed and that good investors actively work to maintain a constructive relationship despite that shift.

The best post-investment relationships share three characteristics. First, the founder treats the investor as a partner in solving problems, not a manager to be managed or a threat to be contained. Second, the investor treats the founder's operational autonomy as an asset to be protected, not a risk to be managed through intervention. Third, both parties communicate about what is not working before it reaches a crisis — the problems that destroy investor-founder relationships are almost always ones that were visible months before they became unmanageable, where neither party had the conversation that could have resolved them.

What Good Investor-Founder Partnerships Look Like

Positive examples of investor-founder relationships are rarer and less publicised than the adversarial horror stories that circulate in startup communities. But they exist in large numbers and share identifiable characteristics that are worth understanding as a target state.Characteristics of high-quality investor-founder partnerships

- Honest communication flows in both directions before problems become crises: The founder brings bad news to the investor when it is still early enough to course-correct, rather than managing the narrative until a problem becomes unresolvable. The investor responds to bad news with problem-solving rather than blame and control-seeking. Both parties have established, through early relationship-building, that honesty is valued more than a sanitised performance.

- The investor uses their network actively and specifically: Not 'I can introduce you to people' but 'I spoke to my contact at Amazon this week about your use case and they want to have a call on Thursday.' The quality of smart money is measured by the specificity and follow-through of the help it provides, not the volume of the commitment during pitching.

- Board meetings are productive rather than performative: Good boards discuss real strategic choices rather than reviewing backward-looking metrics that everyone already knows. The best board meetings end with decisions or clearly defined next steps. Founders who run genuinely useful board meetings — with pre-read materials, focused agendas, and honest discussion of challenges — get more from their investors and build stronger relationships in the process.

- The investor advocates for the founder in difficult situations: When the company hits a hard patch — a down round, a key hire departure, a failed product launch — the quality of an investor is revealed in whether they stand behind the founding team or become a source of pressure and uncertainty. Investors who provide constructive private feedback and public support during difficulties are worth far more than their cheque size suggests.

- Both parties conduct themselves with long-term reputational awareness: The startup and VC ecosystems are small. How a founder behaves toward investors — and how an investor behaves toward founders — is visible, remembered, and consequential for future fundraising and deal sourcing respectively. The best partnerships are run with an awareness that both parties will work with many others in the future, and that the reputation built in each relationship is cumulative.

The Practical Negotiation Framework for Founders in 2026

Drawing together the dynamics covered in this guide, the following framework gives founders a practical, sequenced approach to fundraising negotiations in the current market environment.Steps

- Build traction before raising: Extend your runway through revenue, non-dilutive grants, or cost management until you have metrics that create genuine FOMO for investors. The best time to raise is when you do not desperately need to — because that is when your BATNA is strongest.

- Map your ideal investor universe before starting: Identify 15 to 20 investors who are specifically relevant to your sector, stage, and geography. Focus energy on warm introductions rather than cold outreach — the quality of the introduction is a significant signal to the investor. Begin relationship-building before you are actively in a process.

- Run a parallel process with a defined timeline: Contact your target list within a two-week window and set a clear timeline for getting to term sheets. A timeline that creates natural scarcity — 'we plan to close this round by [date]' — generates competitive tension without being artificial.

- Negotiate the headline terms before accepting a term sheet: Agree on valuation, board composition, and any non-standard terms verbally before accepting a term sheet and entering a no-shop. Once the no-shop is in effect, your leverage to negotiate these points is significantly reduced.

- Prioritise governance over valuation: A higher valuation with an investor-majority board or aggressive liquidation preferences will likely produce worse outcomes than a lower valuation with founder-majority board control and a clean 1x non-participating preference structure. The governance terms determine who runs the company; the valuation determines ownership percentage at that point in time.

- Do your reference checks thoroughly: Speak to two or three portfolio founders who have experienced difficult periods with this investor, not just the smooth ones. Ask specific questions about investor behaviour in board meetings, during down rounds, and when they disagreed with a founder decision.

- Invest in the relationship from day one post-close: Send a well-structured monthly update. Flag problems early. Use the investor's network actively and specifically. The relationship will be tested — build the trust reserves before they are needed.

CONCLUSION

The founder-investor relationship is a two-way street — and both parties are better served by treating it that way. Investors who hold all the cards by offering punitive terms, excessive control provisions, and aggressive participation rights eventually find that the best founders choose other backers. Founders who raise too early, without traction or competitive tension, negotiate from weakness and accept terms that constrain them for years. Both mistakes produce worse outcomes than the alternative.The practical takeaway is consistent with the data: build your BATNA before you need it, raise when you have traction rather than when you are desperate, negotiate governance terms as carefully as valuation, and invest in the post-close relationship with the same energy you invested in the courtship. The best founder-investor partnerships are not the product of clever negotiating tactics — they are the product of mutual respect, shared conviction about what the company can become, and the kind of honest, early communication that prevents small problems from becoming catastrophic ones. That is what a two-way street actually looks like.

Frequently Asked Questions

When is the best time for a founder to raise funding?

The best time to raise is when you do not desperately need to — because that is when your BATNA is strongest and your negotiating position is most favourable. In practical terms, this means raising when you have meaningful traction (revenue, active users, demonstrable product-market fit signals), when your runway is comfortable enough that you are not under severe time pressure, and when you have taken the time to build relationships with target investors before actively entering a process. Faurilaw's December 2025 analysis notes that 'the founder's primary advantage is often time and singular focus' — using that advantage to build compelling traction before raising is the highest-return use of it. Raising too early, without traction or alternatives, puts you at your maximum vulnerability in term negotiations.What is a BATNA and why does it matter in fundraising?

BATNA stands for Best Alternative to a Negotiated Agreement — what you will do if this deal falls through. Your BATNA determines your negotiating leverage: the stronger your BATNA (the better your alternatives), the more credibly you can walk away from bad terms, and the more fairly the investor must negotiate to secure the deal. A founder with two competing term sheets has a strong BATNA. A founder with no alternatives and three months of runway has a weak BATNA. Faurilaw's December 2025 analysis identifies the BATNA as 'a shifting force determined by competitive tension created by multiple credible funding sources.' The most important pre-fundraising activity is strengthening your BATNA by building traction, extending runway, and generating genuine investor interest from multiple sources simultaneously before entering a formal process.What are the most important terms to negotiate in a term sheet?

Ilearnlot's May 2026 analysis of 2025/26 term sheets identifies the following as the highest-priority terms for founders to negotiate carefully: (1) Liquidation preference — push for 1x non-participating rather than 2x or participating structures; (2) Board composition — the 2025/26 market standard of 2 founders, 1 investor, 1 independent gives founders majority control; (3) Anti-dilution provisions — weighted-average is standard and reasonable; full ratchet is highly punitive and should be resisted; (4) Protective provisions — investor veto rights over ordinary business decisions are an overreach; standard protective provisions covering major transactions are reasonable; (5) Redemption rights — negotiate for narrow triggers (change of control only) and limited annual amounts. Valuation matters but governance terms often have greater long-term impact on founder outcomes.How should founders conduct due diligence on prospective investors?

Treat investor due diligence as rigorously as you would expect the investor to treat theirs on you. Capnamic's analysis of investor-founder dynamics explicitly notes that a good investor will 'ask the founder to look in the market for references about myself to get better gut feeling around me as an investor.' The process should include: speaking to two or three portfolio company founders who have experienced both smooth and difficult periods with this investor; asking specifically about investor behaviour during down rounds, board disagreements, and difficult strategic decisions; checking whether the investor follows through on the value-add commitments they make during pitching; and assessing whether their portfolio founders give enthusiastic references or merely adequate ones. The startup and VC ecosystems are well-connected — most investors' reputations are discoverable with a few targeted conversations.What does a healthy founder-investor relationship look like post-investment?

Qubit Capital's April 2026 research identifies the key characteristics as: consistent and transparent communication (including about problems, not just progress), proactive use of the investor's network and resources, board meetings that address real strategic choices rather than reviewing backward-looking metrics, and honest conversation when things are going wrong before they reach a crisis. From the investor side, Capnamic notes that good investors 'try to advertise the smartness of the money' by actively providing value — specific introductions, operational guidance, constructive board participation — rather than passively holding shares. The strongest indicator of relationship quality is how both parties behave during the company's most difficult period: whether the investor becomes a source of pressure and control or a source of support and problem-solving.References

Faurilaw — Investor-Founder Negotiation Dynamics in VC Term Sheets (December 2025) https://www.faurilaw.ca/blog/investor-founder-negotiation-dynamics-a-founders-guide/Qubit Capital — 21 Ways to Strengthen Investor-Founder Relationships for Startup Success (December 2025) https://qubit.capital/blog/investor-founder-relationships

Qubit Capital — How Do Founders Build Venture Capital Relationships (April 2026) https://qubit.capital/blog/venture-capital-relationships

Ilearnlot — Term Sheet Negotiation for Founders in 2026 (May 2026) https://www.ilearnlot.com/term-sheet-negotiation-for-founders/2825341/

Angel Investment Network — Startup Essentials: Top 10 Tips When Negotiating With Investors (February 2026) https://www.angelinvestmentnetwork.net/startup-essentials-top-10-tips-when-negotiating-with-investors/

Capnamic — Power Dynamics in Investor-Founder Relations https://capnamic.com/post/power-dynamics-in-investor-founder-relations

NVCA — 2025 Model Legal Documents for VC Transactions (updated 2025) https://nvca.org/model-legal-documents/

Y Combinator — Safe Financing Documents and Standard Seed Round Terms https://www.ycombinator.com/documents

First Round Capital — The Dos and Don'ts of Fundraising (founder resource library) https://review.firstround.com/the-dos-and-donts-of-fundraising

0 Comments Comments