Financial Literacy

How to Avoid Falling Behind Financially: Complete Guide

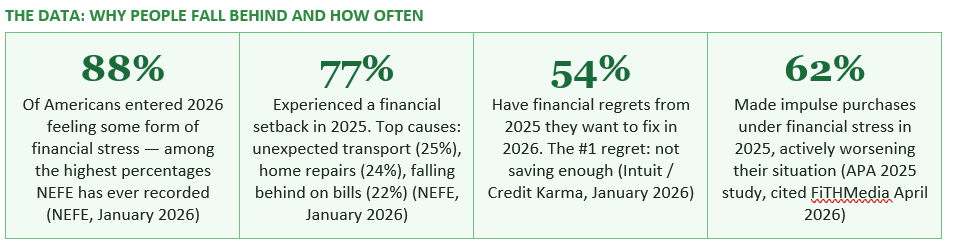

Seventy-seven per cent of Americans experienced a financial setback in 2025, according to NEFE's January 2026 nationwide poll — the highest figure the organisation has recorded in years of tracking financial wellbeing. Eighty-eight per cent entered 2026 feeling financial stress. And forty-nine per cent say their financial situation actively worsened last year, according to Credit Karma's Qualtrics research. These are not fringe statistics. This is the mainstream experience of people who did not have the right systems in place before setbacks hit. This guide gives you those systems.

Falling behind financially is almost never a single dramatic event. It is usually a slow accumulation of small vulnerabilities that leave a person or household with no margin when a shock arrives. NEFE's January 2026 nationwide poll identifies the most common financial setbacks of 2025: unexpected transportation expenses (25%), unexpected home repairs or maintenance (24%), falling behind on bill payments or debt obligations (22%), medical expenses from injury or illness (21%), and job loss or significant income reduction (20%). Not one of these is unusual or unpredictable in category — they are the standard life events that have always created financial setbacks for households without the right buffers in place.

Credit Karma's Qualtrics research, covering over 1,000 US adults in late 2025, found that 49% said their financial situation worsened in 2025, with unexpected expenses cited by 28% as the primary cause. This points to the most important insight in this guide: most financial setbacks are not caused by bad luck in the catastrophic sense — they are caused by predictable categories of events (car repairs, medical bills, job changes, home maintenance) arriving without the financial buffer to absorb them.

The second cause is structural: the combination of credit card debt at 22% APR and no savings means that when a setback hits, the only available response is debt, which compounds the original problem. FiTHMedia's April 2026 resilience guide documents this cycle: 'Credit-card APRs hover near 22 percent in early 2026. When a setback hits someone carrying high-interest debt and no savings buffer, the shock does not just cost what it cost — it costs what it cost plus compound interest on the debt required to cover it.' Northwestern Mutual's January 2026 data confirms the baseline: 70% of Americans carry personal debt outside their mortgages, with an average of $21,500 — the majority of it credit card debt.

In 2026 America, financial security is no longer something households can take for granted — it has become something that must be deliberately built through smart systems, intentional planning, and steady daily habits.

— FITHMEDIA — FINANCIAL RESILIENCE 2026: U.S. GUIDE TO THRIVING CHANGE (APRIL 2026)

NEFE's January 2026 data shows the top two financial setbacks of 2025 were unexpected transportation expenses (25%) and unexpected home repairs (24%). Both are predictable in category — everyone with a car knows it will need repairs; everyone with a home knows it will need maintenance — and both are manageable in amount for most households if an emergency fund is present. Without one, both become debt events.

The target for most financial guidance, including Fidelity's 2025 Financial Resolutions Study, is three to six months of essential living expenses held in a high-yield savings account. In the US in 2026, the best easy-access HYSA rates are up to 5.00% APY (Varo Money), meaning the emergency fund itself earns meaningful interest while providing the buffer function.

For households starting from zero, the initial target is a micro emergency fund of $500 to $1,000 — enough to cover the most common setbacks (a car repair, a medical copay, a utility bill when an account runs short) without credit card debt. Kiplinger's December 2025 financial planning guide confirms: 'According to Fidelity's 2025 Financial Resolutions Study, 80% of respondents say having a plan and structure in place helps them deal with surprise events.' The emergency fund is the structural protection that makes that plan work.

Build the emergency fund in a separate account from your everyday checking — the separation prevents it from being spent on non-emergencies. Name the account explicitly: 'Emergency Fund' or 'Shield Account.' Automate a fixed transfer on payday, even if it is only $25 per week. At $25 per week, the $1,000 micro emergency fund is fully funded in 40 weeks. Every setback absorbed without credit card debt prevents the compounding spiral that makes financial recovery so slow.

Spending visibility does not require a complex budgeting system. It requires one thing: knowing, in real time or near-real time, what you have spent this week against what you planned to spend. Three tools make this accessible for any budget in 2026. In the US, Empower Personal Dashboard (free), Rocket Money (free for subscription tracking), and SoFi Relay (free, links all accounts) all provide automatic categorisation of spending across linked accounts. In the UK, Monzo and Starling current accounts provide real-time spending categorisation with no additional tools required. For anyone who prefers not to link financial accounts to a third-party app, a simple weekly total in a notes app or spreadsheet, updated every two or three days, is sufficient.

The specific spending visibility practice that most consistently prevents falling behind is the weekly review: once a week, total your spending by category and compare it to your target allocations. This review — the thirty-minute weekly money review described in the companion guide in this series — allows course corrections in real time rather than end-of-month shock. A household that discovers on Thursday that it has already spent its full food budget for the week can make adjustments on Thursday. A household that discovers the same thing in the bank statement at the end of the month has already done the damage.

Northwestern Mutual's January 2026 data found that for the third consecutive year, reducing debt was Americans' highest financial priority — ahead of saving. This prioritisation is correct for anyone paying 22% interest: the guaranteed, risk-free return from eliminating credit card debt is 22% — higher than any investment reliably available to most retail investors. But the prioritisation must not come at the expense of the emergency fund, because eliminating debt without a buffer means the next unexpected expense immediately creates new debt, resetting the paydown to zero.

The correct sequencing is: emergency fund to at least $500 first, then debt paydown. The most efficient paydown method for multiple debts is the debt avalanche — directing all extra payments to the highest-APR debt while maintaining minimum payments on all others. This saves the most in total interest. For those who need motivational wins to sustain the effort, the debt snowball (paying off the smallest balance first, then rolling that payment to the next) generates faster visible progress at a slightly higher total interest cost. Either method — consistently applied — eliminates the compounding drag that keeps millions of households financially behind year after year.

The tool that converts predictable setbacks into managed expenditures is the sinking fund — a named savings pot dedicated to a specific planned cost, funded in small weekly or monthly amounts well in advance of the expense. As covered in our companion guides, a Christmas fund that saves £40 per month from January means Christmas costs nothing extra in December. An annual car insurance fund that saves one-twelfth of the annual premium each month means the renewal is a zero-drama non-event. The annual insurance renewal that triggers a panic in November would have been £50 per month from January.

The triage sequence for someone who is already behind is: first, stop the active bleeding — if you are adding to credit card debt every month, identify the specific gap between income and spending and address it before anything else. Second, contact creditors early — if you are at risk of missing bill payments, contacting creditors before missing a payment consistently produces better outcomes (payment plans, reduced interest, temporary payment deferrals) than waiting until a missed payment triggers penalties and credit damage. Third, seek free debt advice if the situation is serious — in the UK, StepChange provides free, non-judgmental professional debt counselling online and by phone; in the US, the National Foundation for Credit Counseling (NFCC) provides the equivalent service. Both are entirely free.

Kiplinger's December 2025 year-end financial planning guide captures the right mindset for recovery: 'Successful financial planning is not necessarily about perfection, but consistency. Small, deliberate actions taken regularly can compound into significant results over time.' The person who is behind today and takes two specific actions this week is better off than the person who waits for the perfect moment to start a comprehensive plan. The emergency fund, the budget, the debt paydown — all of them start with a single first action, not a perfect plan.

The goal of this guide is not a perfect financial life — NEFE's data shows that financial setbacks are a normal part of life at the population level. The goal is a financially resilient one, in which setbacks are absorbed rather than amplified by the compounding of high-interest debt. Each pillar in this guide is buildable in weeks rather than years. Start with the emergency fund. Build $500 before the next car repair, medical bill, or home maintenance issue arrives and converts a manageable expense into a debt spiral. From there, each additional pillar strengthens the system. The 93% of people who entered 2026 planning to change how they manage their money are right to prioritise it. This guide is how.

Intuit — 2026 Financial Forecast: Staying Mindful Amid Money Stress (January 2026) https://www.intuit.com/blog/innovative-thinking/2026-financial-forecast-mindful-stress/

Credit Karma / Qualtrics — Nearly Half of Americans Say Their Finances Worsened in 2025 (December 2025) https://www.creditkarma.com/about/commentary/nearly-half-of-americans-say-their-finances-worsened-in-2025-but-most-are-planning-a-reset-in-the-new-year

Northwestern Mutual — Simple Resolutions to Unlock Your Financial Potential in 2026 (January 2026) https://www.northwesternmutual.com/life-and-money/simple-resolutions-to-unlock-your-financial-potential-in-2026/

FiTHMedia — Financial Resilience 2026: U.S. Guide to Thriving Change (April 2026) https://fithmedia.com/timeless-finance/financial-resilience-2026-u-s-guide-to-thriving-change/

Kiplinger — Financial To-Dos to Finish 2025 Strong and Start 2026 Stronger (December 2025) https://www.kiplinger.com/personal-finance/financial-to-dos-to-finish-2025-strong-and-start-2026-stronger

Monarch Money — Financial Resolutions for 2026: Tips to Achieve Your Money Goals (February 2026) https://www.monarch.com/blog/personal-finance/financial-resolutions

StepChange — Free Debt Advice (UK) https://www.stepchange.org

TABLE OF CONTENTS

- Why People Fall Behind: The Real Causes

- The Five Pillars of Financial Resilience

- Pillar 1: The Emergency Fund — Your First Line of Defence

- Pillar 2: Spending Visibility — Knowing Before You Overspend

- Pillar 3: Debt Management — Stopping the Compounding Trap

- Pillar 4: Income Protection — Defending What You Earn

- Pillar 5: Forward Planning — Preparing for the Predictable

- Warning Signs You Are Starting to Fall Behind

- What to Do If You Are Already Behind

- Conclusion

- Frequently Asked Questions

- References

Why People Fall Behind: The Real Causes

Falling behind financially is almost never a single dramatic event. It is usually a slow accumulation of small vulnerabilities that leave a person or household with no margin when a shock arrives. NEFE's January 2026 nationwide poll identifies the most common financial setbacks of 2025: unexpected transportation expenses (25%), unexpected home repairs or maintenance (24%), falling behind on bill payments or debt obligations (22%), medical expenses from injury or illness (21%), and job loss or significant income reduction (20%). Not one of these is unusual or unpredictable in category — they are the standard life events that have always created financial setbacks for households without the right buffers in place.Credit Karma's Qualtrics research, covering over 1,000 US adults in late 2025, found that 49% said their financial situation worsened in 2025, with unexpected expenses cited by 28% as the primary cause. This points to the most important insight in this guide: most financial setbacks are not caused by bad luck in the catastrophic sense — they are caused by predictable categories of events (car repairs, medical bills, job changes, home maintenance) arriving without the financial buffer to absorb them.

The second cause is structural: the combination of credit card debt at 22% APR and no savings means that when a setback hits, the only available response is debt, which compounds the original problem. FiTHMedia's April 2026 resilience guide documents this cycle: 'Credit-card APRs hover near 22 percent in early 2026. When a setback hits someone carrying high-interest debt and no savings buffer, the shock does not just cost what it cost — it costs what it cost plus compound interest on the debt required to cover it.' Northwestern Mutual's January 2026 data confirms the baseline: 70% of Americans carry personal debt outside their mortgages, with an average of $21,500 — the majority of it credit card debt.

In 2026 America, financial security is no longer something households can take for granted — it has become something that must be deliberately built through smart systems, intentional planning, and steady daily habits.

— FITHMEDIA — FINANCIAL RESILIENCE 2026: U.S. GUIDE TO THRIVING CHANGE (APRIL 2026)

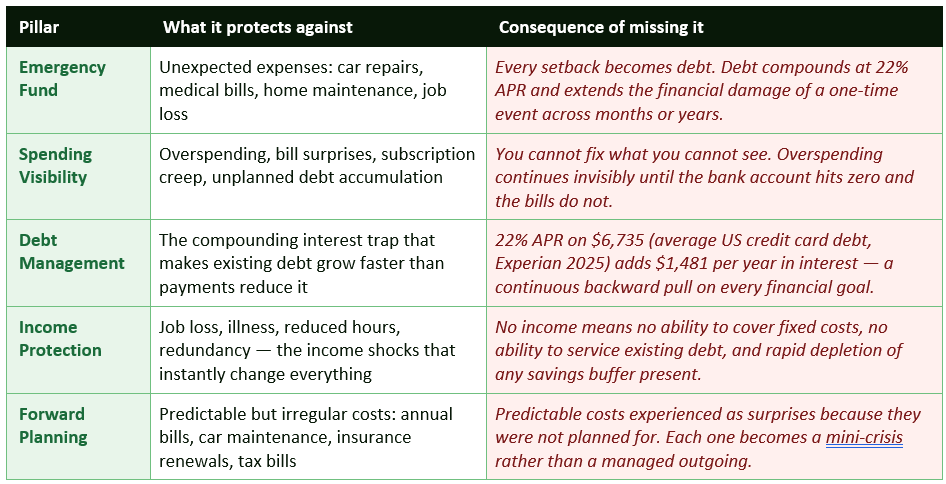

The Five Pillars of Financial Resilience

Avoiding falling behind financially is not achieved through a single action or a single habit. It is achieved through a set of interlocking protections — five pillars that together create the financial resilience to absorb the setbacks that NEFE's data shows 77% of households experienced in 2025.Pillar 1: The Emergency Fund — Your First Line of Defence

The emergency fund is the single most important financial protection available to any household. Its purpose is specific: to absorb unexpected, unavoidable expenses without recourse to high-interest debt. When a car repair costs $700, a household with a $1,000 emergency fund pays $700 and replenishes the fund over the following weeks. A household without one puts $700 on a credit card at 22% APR and begins paying interest on a car repair for months or years.NEFE's January 2026 data shows the top two financial setbacks of 2025 were unexpected transportation expenses (25%) and unexpected home repairs (24%). Both are predictable in category — everyone with a car knows it will need repairs; everyone with a home knows it will need maintenance — and both are manageable in amount for most households if an emergency fund is present. Without one, both become debt events.

The target for most financial guidance, including Fidelity's 2025 Financial Resolutions Study, is three to six months of essential living expenses held in a high-yield savings account. In the US in 2026, the best easy-access HYSA rates are up to 5.00% APY (Varo Money), meaning the emergency fund itself earns meaningful interest while providing the buffer function.

For households starting from zero, the initial target is a micro emergency fund of $500 to $1,000 — enough to cover the most common setbacks (a car repair, a medical copay, a utility bill when an account runs short) without credit card debt. Kiplinger's December 2025 financial planning guide confirms: 'According to Fidelity's 2025 Financial Resolutions Study, 80% of respondents say having a plan and structure in place helps them deal with surprise events.' The emergency fund is the structural protection that makes that plan work.

Build the emergency fund in a separate account from your everyday checking — the separation prevents it from being spent on non-emergencies. Name the account explicitly: 'Emergency Fund' or 'Shield Account.' Automate a fixed transfer on payday, even if it is only $25 per week. At $25 per week, the $1,000 micro emergency fund is fully funded in 40 weeks. Every setback absorbed without credit card debt prevents the compounding spiral that makes financial recovery so slow.

Pillar 2: Spending Visibility — Knowing Before You Overspend

You cannot avoid falling behind on something you cannot see. The most consistent finding across financial wellbeing research is that people's mental model of their spending is systematically inaccurate — they underestimate discretionary spending, forget recurring subscriptions, and do not account for irregular costs. Intuit's January 2026 research found that 45% of consumers admit impulse spending has derailed their financial progress, and 61% identify money as their primary life stressor. Both problems are significantly worse when spending is invisible.Spending visibility does not require a complex budgeting system. It requires one thing: knowing, in real time or near-real time, what you have spent this week against what you planned to spend. Three tools make this accessible for any budget in 2026. In the US, Empower Personal Dashboard (free), Rocket Money (free for subscription tracking), and SoFi Relay (free, links all accounts) all provide automatic categorisation of spending across linked accounts. In the UK, Monzo and Starling current accounts provide real-time spending categorisation with no additional tools required. For anyone who prefers not to link financial accounts to a third-party app, a simple weekly total in a notes app or spreadsheet, updated every two or three days, is sufficient.

The specific spending visibility practice that most consistently prevents falling behind is the weekly review: once a week, total your spending by category and compare it to your target allocations. This review — the thirty-minute weekly money review described in the companion guide in this series — allows course corrections in real time rather than end-of-month shock. A household that discovers on Thursday that it has already spent its full food budget for the week can make adjustments on Thursday. A household that discovers the same thing in the bank statement at the end of the month has already done the damage.

Pillar 3: Debt Management — Stopping the Compounding Trap

Existing high-interest debt is the structural drag that makes every other financial goal harder and every financial setback worse. The average American carried $6,735 in credit card debt in 2025, according to Experian data cited by Monarch's February 2026 financial resolutions guide. At 22% APR — the current national average, per Federal Reserve data cited by FiTHMedia's April 2026 guide — that $6,735 generates approximately $1,481 in annual interest, or approximately $123 per month that goes to the bank before any actual debt reduction occurs.Northwestern Mutual's January 2026 data found that for the third consecutive year, reducing debt was Americans' highest financial priority — ahead of saving. This prioritisation is correct for anyone paying 22% interest: the guaranteed, risk-free return from eliminating credit card debt is 22% — higher than any investment reliably available to most retail investors. But the prioritisation must not come at the expense of the emergency fund, because eliminating debt without a buffer means the next unexpected expense immediately creates new debt, resetting the paydown to zero.

The correct sequencing is: emergency fund to at least $500 first, then debt paydown. The most efficient paydown method for multiple debts is the debt avalanche — directing all extra payments to the highest-APR debt while maintaining minimum payments on all others. This saves the most in total interest. For those who need motivational wins to sustain the effort, the debt snowball (paying off the smallest balance first, then rolling that payment to the next) generates faster visible progress at a slightly higher total interest cost. Either method — consistently applied — eliminates the compounding drag that keeps millions of households financially behind year after year.

Pillar 4: Income Protection — Defending What You Earn

NEFE's January 2026 data shows that job loss or significant income reduction affected 20% of households as a financial setback in 2025. This is not a fringe risk — it is a one-in-five annual probability at the population level. The financial consequence of income loss is immediate and severe for households without buffers: fixed costs continue, debt service continues, and the income to cover them has disappeared.Income protection insurance (UK)

In the UK, income protection insurance pays a monthly benefit (typically 50–70% of gross income) if you are unable to work due to illness or injury, for periods from one year to the point of retirement. It is one of the most undersold and most valuable personal finance products available. A non-smoker in their thirties can secure meaningful income protection for £20 to £50 per month. For self-employed workers without sick pay entitlement, it is particularly critical — the self-employed have no Statutory Sick Pay and no employer-funded sick pay, making them entirely dependent on savings during any period of inability to work.Disability insurance (US)

In the US, employer-provided short-term and long-term disability insurance covers income replacement in illness and injury scenarios. Many employer plans cover only 60% of salary, and many self-employed workers have no coverage at all. Reviewing your employer's disability benefits and considering supplemental coverage where the existing policy leaves a significant income gap is a meaningful risk management action. The Social Security Disability Insurance (SSDI) system provides a backstop but is difficult to access and provides modest payments that rarely cover all living expenses.Building multiple income streams

The most accessible income resilience strategy for most households is developing at least one income source beyond a single primary employer. This does not require a full second job — a freelance skill, a side income from selling items, tutoring, or any activity that generates $200 to $500 per month provides meaningful protection against total income loss from a single employer. When the primary income is disrupted, the secondary income provides time to respond without immediately depleting savings or creating debt.Pillar 5: Forward Planning — Preparing for the Predictable

The most avoidable financial setbacks are the predictable ones that arrive as surprises because nobody planned for them. Annual car insurance renewals, vehicle MOT and service costs, household appliance replacements, dental check-ups, school costs at the start of term, Christmas, birthdays, and tax bills — none of these is genuinely unexpected. All of them are known in category, if not exact amount, well in advance. Yet they are cited as financial crises in household after household, year after year.The tool that converts predictable setbacks into managed expenditures is the sinking fund — a named savings pot dedicated to a specific planned cost, funded in small weekly or monthly amounts well in advance of the expense. As covered in our companion guides, a Christmas fund that saves £40 per month from January means Christmas costs nothing extra in December. An annual car insurance fund that saves one-twelfth of the annual premium each month means the renewal is a zero-drama non-event. The annual insurance renewal that triggers a panic in November would have been £50 per month from January.

The annual events most households should have sinking funds for

- Car maintenance and MOT/service: Budget £500–£800/$500–$800 per year for routine maintenance, tyres, and MOT (UK). Create a monthly sinking fund of £60–£70/$60–$70. Any repair above this is absorbed by the emergency fund — this sinking fund covers the predictable, the emergency fund covers the unpredictable.

- Home maintenance: Budget 1–2% of your home's value per year for routine maintenance and repairs. On a £200,000/$250,000 home, that is £2,000–$2,500 per year, or £170–$210 per month. Without this fund, every boiler repair, roof issue, or appliance failure becomes a crisis.

- Annual insurance renewals (car, home, life): Calculate the annual total of all insurance premiums, divide by 12, and save that amount each month. When each renewal arrives, the money is already there. This also creates the time to compare and switch providers rather than auto-renewing under financial pressure.

- Annual tax bill (self-employed / freelance): Set aside 20–30% of every payment received into a dedicated tax pot. HMRC (UK) and the IRS (US) do not accept 'I forgot to save for it' as a tax deferral. A self-employed person without a tax sinking fund is building a future financial crisis with every invoice they receive.

- Christmas and gifts: The average UK household spends £500–£800 on Christmas. Divide by 12 and save from January. The average US household spends $1,000–$1,400. Both are entirely manageable as a monthly sinking fund. Both are financially disruptive as a December credit card event.

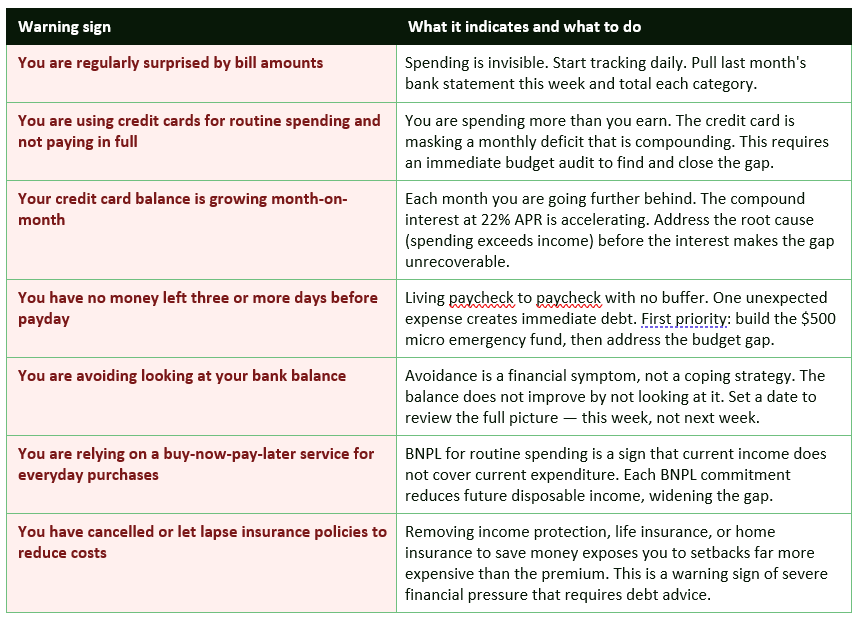

Warning Signs You Are Starting to Fall Behind

Financial decline is rarely sudden. It has warning signs — specific patterns in spending and financial behaviour that indicate the five pillars are weakening before a crisis makes it obvious. Recognising these patterns early allows correction while the options are still wide.What to Do If You Are Already Behind

If one or more of the warning signs above describes your current situation, the response is action — not anxiety. NEFE's January 2026 data shows 77% of households experienced a financial setback in 2025, which means falling behind is common. It is also recoverable. The Credit Karma research found 93% of people with financial regrets from 2025 plan to change how they manage their money in 2026 — which confirms that the period immediately after identifying a problem is the highest-motivation moment to act.The triage sequence for someone who is already behind is: first, stop the active bleeding — if you are adding to credit card debt every month, identify the specific gap between income and spending and address it before anything else. Second, contact creditors early — if you are at risk of missing bill payments, contacting creditors before missing a payment consistently produces better outcomes (payment plans, reduced interest, temporary payment deferrals) than waiting until a missed payment triggers penalties and credit damage. Third, seek free debt advice if the situation is serious — in the UK, StepChange provides free, non-judgmental professional debt counselling online and by phone; in the US, the National Foundation for Credit Counseling (NFCC) provides the equivalent service. Both are entirely free.

Kiplinger's December 2025 year-end financial planning guide captures the right mindset for recovery: 'Successful financial planning is not necessarily about perfection, but consistency. Small, deliberate actions taken regularly can compound into significant results over time.' The person who is behind today and takes two specific actions this week is better off than the person who waits for the perfect moment to start a comprehensive plan. The emergency fund, the budget, the debt paydown — all of them start with a single first action, not a perfect plan.

CONCLUSION

Seventy-seven per cent of Americans had a financial setback in 2025. The setbacks themselves were not unusual — car repairs, medical bills, home maintenance, reduced income. What made them financially damaging was the absence of the five pillars that absorb such shocks: an emergency fund, spending visibility, debt management, income protection, and forward planning. With all five in place, the same events would have been inconveniences. Without them, they became crises.The goal of this guide is not a perfect financial life — NEFE's data shows that financial setbacks are a normal part of life at the population level. The goal is a financially resilient one, in which setbacks are absorbed rather than amplified by the compounding of high-interest debt. Each pillar in this guide is buildable in weeks rather than years. Start with the emergency fund. Build $500 before the next car repair, medical bill, or home maintenance issue arrives and converts a manageable expense into a debt spiral. From there, each additional pillar strengthens the system. The 93% of people who entered 2026 planning to change how they manage their money are right to prioritise it. This guide is how.

Frequently Asked Questions

What is the number one cause of people falling behind financially?

The number one structural cause of falling behind financially is the absence of an emergency fund combined with existing high-interest debt. When a setback occurs — and NEFE's January 2026 data shows 77% of households experienced at least one in 2025 — a household with no savings buffer must cover the expense with credit card debt at 22% APR. The debt then compounds month by month, reducing the amount available for other bills and goals, making the next setback even harder to absorb. The top five setbacks that sent households behind in 2025 were unexpected transportation costs (25%), home repairs (24%), falling behind on bill payments (22%), medical expenses (21%), and job loss or income reduction (20%). All five are predictable in category — it is not the unpredictability of the events that causes the financial damage, it is the absence of preparation.How much emergency fund do I need to avoid falling behind?

The standard financial guidance is three to six months of essential living expenses in a high-yield savings account. In practice, the most critical threshold is the first $500 to $1,000 — enough to cover the most common setbacks without recourse to credit card debt. At $25 per week automated, the $1,000 micro emergency fund is fully funded in 40 weeks. Once that initial buffer is in place, building toward one month and then three months of expenses provides progressively stronger protection against income disruption as well as individual expense shocks. Fidelity's 2025 Financial Resolutions Study found that 80% of respondents say having a plan and structure in place helps them deal with surprise events — the emergency fund is the structural element of that plan. In 2026, the best easy-access savings accounts in the US pay up to 5.00% APY (Varo Money), making the emergency fund an interest-earning asset rather than idle cash.How do I stop spending more than I earn?

The first step is establishing exactly how much you earn and exactly how much you currently spend — which requires pulling 30 days of bank and card statements and totalling spending by category. Most people who spend more than they earn are not aware of the exact gap because spending is invisible without this data. Credit Karma's Qualtrics research found that the top financial regret from 2025 was not saving enough, but the underlying cause in most cases is that the gap between income and spending was not visible in time to close it. Once the gap is quantified, close it through a combination of spending reductions (subscriptions, discretionary categories, habitual spending that brings no real satisfaction) and, where possible, income increases. The Intuit January 2026 survey found 43% of consumers plan to adopt a balanced expense management mindset in 2026 — consistent tracking with breathing room, rather than a rigid zero-tolerance budget that leads to abandonment.What should I do if I have already fallen behind on bills?

Contact your creditors before the situation deteriorates further — proactive contact consistently produces better outcomes than waiting until payments are missed. Most creditors offer hardship plans, payment deferrals, or reduced-interest arrangements that are not automatically offered but are available when requested. If you are in the UK, contact StepChange (stepchange.org) for free professional debt advice — they can assess your full situation and recommend the most effective approach, including debt management plans, Individual Voluntary Arrangements (IVAs), or bankruptcy where appropriate. In the US, contact the National Foundation for Credit Counseling (nfcc.org), which provides the equivalent free, non-profit debt counselling service. Do not take out a payday loan or high-interest short-term loan to cover missed payments — this is the most consistently damaging financial response to a cash shortfall and reliably makes the situation worse.How do I protect myself financially from job loss?

Income protection against job loss has three layers. The first is the emergency fund: three to six months of essential living expenses held in a high-yield savings account provides the time to find new employment without immediately defaulting on bills or running up credit card debt. The second is income protection insurance (UK) or supplemental disability insurance (US), which replaces a portion of income if you cannot work due to illness or injury — covering the scenario where job loss is caused by a health event rather than redundancy. The third is income diversification: having at least one income source beyond a single employer — a freelance skill, rental income, a side business, or any reliable additional income stream — means total income loss from one employer does not mean total income loss. The NEFE January 2026 poll found job loss and significant income reduction affected 20% of households in 2025. Each of the three layers above reduces both the probability and the financial impact of that event.References

NEFE — Poll: Americans Feeling Financial Stress to Begin 2026 (January 2026) https://www.nefe.org/news/2026/01/poll-americans-feeling-stressed-to-begin-2026.aspxIntuit — 2026 Financial Forecast: Staying Mindful Amid Money Stress (January 2026) https://www.intuit.com/blog/innovative-thinking/2026-financial-forecast-mindful-stress/

Credit Karma / Qualtrics — Nearly Half of Americans Say Their Finances Worsened in 2025 (December 2025) https://www.creditkarma.com/about/commentary/nearly-half-of-americans-say-their-finances-worsened-in-2025-but-most-are-planning-a-reset-in-the-new-year

Northwestern Mutual — Simple Resolutions to Unlock Your Financial Potential in 2026 (January 2026) https://www.northwesternmutual.com/life-and-money/simple-resolutions-to-unlock-your-financial-potential-in-2026/

FiTHMedia — Financial Resilience 2026: U.S. Guide to Thriving Change (April 2026) https://fithmedia.com/timeless-finance/financial-resilience-2026-u-s-guide-to-thriving-change/

Kiplinger — Financial To-Dos to Finish 2025 Strong and Start 2026 Stronger (December 2025) https://www.kiplinger.com/personal-finance/financial-to-dos-to-finish-2025-strong-and-start-2026-stronger

Monarch Money — Financial Resolutions for 2026: Tips to Achieve Your Money Goals (February 2026) https://www.monarch.com/blog/personal-finance/financial-resolutions

StepChange — Free Debt Advice (UK) https://www.stepchange.org

0 Comments Comments