Budgeting

How to Create a Simple Money System That Runs Automatically

In 2026, the most valuable asset you have isn't just your income—it's your time. For many, the monthly ritual of paying bills, checking balances, and manually moving money into savings is a source of stress and "decision fatigue." But what if your finances could manage themselves? What if you could build a "financial engine" that ensures your bills are paid, your savings are growing, and your investments are compounding, all while you sleep?

This is the power of an Automated Money System. In this comprehensive guide, we reveal how to move beyond manual budgeting and into a world of automated wealth. By leveraging the latest 2026 fintech tools and banking features, you can create a system that not only saves you thousands of hours over your lifetime but also eliminates the emotional friction that often leads to poor financial decisions.

2 Fixed Costs (Rent, Utilities, Insurance) are paid via Auto-Pay or Direct Debit.

3 Savings & Investments are swept into high-yield accounts or brokerage platforms immediately.

4 Spending Money is what remains, allowing you to spend without guilt or the need to track every penny.

6 What an Automated Money System Is: The Philosophy of Automation

7 The Benefits of Automation: Why Manual Budgeting is Dead in 2026

8 Step-by-Step Setup: Building Your Financial Engine

11 Common Pitfalls: What to Watch Out For

Conclusion: Reclaiming Your Time and Wealth

Frequently Asked Questions (FAQ)

External References and Resources

We are living in the era of "Set-and-Forget" Finance. The goal of an automated money system is not just to pay your bills on time; it's to create a psychological environment where "doing the right thing" is the default behavior. By removing the need for willpower, you ensure that your financial goals are met consistently, month after month, regardless of your mood or schedule.

In this guide, we won't just tell you to "save more." We will show you exactly how to wire your financial life so that saving happens automatically, leaving you free to focus on what truly matters.

By understanding the "loyalty penalty" and the "Big Three" expenses, you can build a more accurate and sustainable budget for your household. In 2026, with the widespread adoption of AI-driven energy management and community-led food exchanges, households are increasingly able to "stack" their energy-intensive activities to maximize efficiency.

As you look toward the future, remember that technology and data are your best allies. By staying informed and prepared, you can build a more secure and stable home for yourself and your family.

By starting your automated money system today, you aren't just simplifying your life in 2026; you are preparing yourself for the next generation of wealth-building technology.

This is the power of an Automated Money System. In this comprehensive guide, we reveal how to move beyond manual budgeting and into a world of automated wealth. By leveraging the latest 2026 fintech tools and banking features, you can create a system that not only saves you thousands of hours over your lifetime but also eliminates the emotional friction that often leads to poor financial decisions.

The Automated Money System

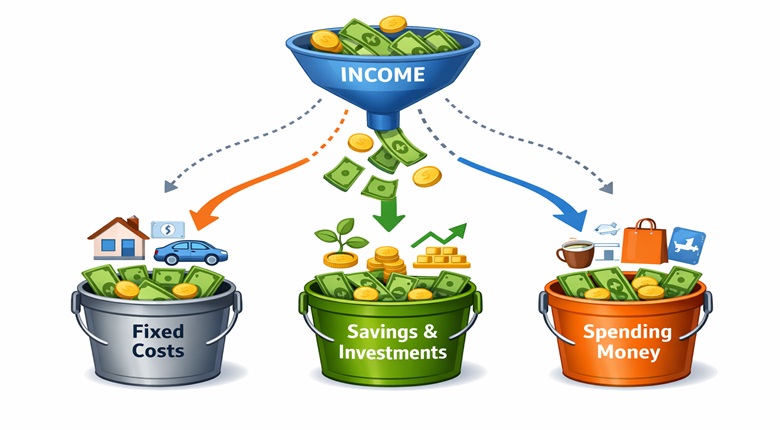

An automated money system is a series of pre-set instructions (rules) that move your income through various "buckets"—Fixed Costs, Savings, Investments, and Guilt-Free Spending—without manual intervention.The Core Framework:

1 Income hits your primary checking account.2 Fixed Costs (Rent, Utilities, Insurance) are paid via Auto-Pay or Direct Debit.

3 Savings & Investments are swept into high-yield accounts or brokerage platforms immediately.

4 Spending Money is what remains, allowing you to spend without guilt or the need to track every penny.

Table of Contents

5 Introduction: The Era of "Set-and-Forget" Finance6 What an Automated Money System Is: The Philosophy of Automation

7 The Benefits of Automation: Why Manual Budgeting is Dead in 2026

8 Step-by-Step Setup: Building Your Financial Engine

- Step 1: The "Income Hub" (Primary Checking)

- Step 2: Automating the "Big Three" (Fixed Costs)

- Step 3: The "Pay Yourself First" Sweep (Savings & Investments)

- Step 4: The "Guilt-Free" Buffer (Spending Account)

- AI-Driven Budgeting Apps (Monarch, YNAB, Copilot)

- Automated Investment Platforms (Acorns, Betterment, Vanguard)

- High-Yield "Sweep" Accounts (Wealthfront, Marcus)

11 Common Pitfalls: What to Watch Out For

Conclusion: Reclaiming Your Time and Wealth

Frequently Asked Questions (FAQ)

External References and Resources

The Era of "Set-and-Forget" Finance

As we navigate through 2026, the complexity of personal finance has reached a tipping point. With multiple bank accounts, credit cards, investment platforms, and a myriad of subscription services, the cognitive load of "managing money" has never been higher. Yet, ironically, the tools to simplify this complexity have also never been more powerful.We are living in the era of "Set-and-Forget" Finance. The goal of an automated money system is not just to pay your bills on time; it's to create a psychological environment where "doing the right thing" is the default behavior. By removing the need for willpower, you ensure that your financial goals are met consistently, month after month, regardless of your mood or schedule.

In this guide, we won't just tell you to "save more." We will show you exactly how to wire your financial life so that saving happens automatically, leaving you free to focus on what truly matters.

What an Automated Money System Is: The Philosophy of Automation

An automated money system is more than just a series of scheduled transfers; it is a financial ecosystem designed to manage your cash flow without your constant input. It is built on the principle that humans are naturally prone to "decision fatigue" and "emotional spending." By pre-committing to your financial goals and setting up a system to execute them, you remove the need for willpower.The Core Components of an Automated System

-

The Hub (Checking Account): This is where all your income (salary, dividends, side hustles) lands first. It acts as the "clearinghouse" for your money.

-

The "Big Three" (Fixed Costs): These are the non-negotiable bills—rent/mortgage, utilities, insurance, and debt payments. In an automated system, these are paid via Auto-Pay or Direct Debit.

- The "Pay Yourself First" Sweep (Savings & Investments): This is the most critical part of the system. Immediately after your income lands, a portion is swept into your emergency fund, retirement accounts (401k, IRA, ISA), and brokerage platforms.

- The "Guilt-Free" Buffer (Spending Account): This is the money that remains after your fixed costs and savings are taken care of. This is your spending money for dining out, hobbies, and travel.

The "Default Behavior" Advantage

In 2026, the power of "default behavior" is well-documented. If your default is to save 20% of your income before you even see it, you will naturally adjust your lifestyle to live on the remaining 80%. An automated system makes "saving" the default, while "spending" becomes a conscious choice.Step‑by‑Step Setup: Building Your Financial Engine

Building an automated money system doesn't happen overnight, but it can be done in four simple phases.Step 1: The "Income Hub" (Primary Checking)

Your primary checking account is the heart of your system. Choose an account with no monthly fees and real-time transaction alerts. In 2026, many "neo-banks" like Monzo, Revolut, and Chime offer "virtual cards" and "pots" that can help you segment your money within a single account.- Action Item: Set up your direct deposit to land in this account. If you have multiple income sources, ensure they all point to this single "hub."

Step 2: Automating the "Big Three" (Fixed Costs)

List all your recurring monthly bills. This includes rent/mortgage, utilities, insurance, and minimum debt payments.- Action Item: For every bill that allows it, set up Auto-Pay. For bills that vary (like utilities), use a "bill-smoothing" service or set your Auto-Pay to a slightly higher amount to build a small credit on the account.

- Pro Tip: Use a dedicated credit card for all your recurring bills to earn rewards, then set that credit card to Auto-Pay the full balance from your "Income Hub" every month.

Step 3: The "Pay Yourself First" Sweep (Savings & Investments)

This is where the magic happens. You must move your savings and investment contributions out of your checking account as soon as your salary hits.- Action Item: Set up an automatic transfer from your "Income Hub" to your High-Yield Savings Account (HYSA) for your emergency fund.

- Action Item: Set up automatic contributions to your retirement accounts (401k, IRA, ISA) and brokerage platforms (Vanguard, Fidelity, Betterment).

- Pro Tip: Aim for at least 15-20% of your gross income to be automated into these "wealth-building" buckets.

Step 4: The "Guilt-Free" Buffer (Spending Account)

Once your fixed costs and savings are automated, what remains in your checking account is your "guilt-free" spending money.- Action Item: Calculate your "Safe-to-Spend" amount by subtracting your automated fixed costs and savings from your total income.

- Pro Tip: In 2026, many banks offer a "Safe-to-Spend" feature that automatically calculates this for you in real-time, helping you avoid overspending without the need for a manual spreadsheet.

H2: Tools of the Trade: The Best Fintech for 2026

In 2026, the best tools for an automated money system are those that integrate seamlessly with your existing banking and investment platforms. From AI-driven budgeting apps to automated investment platforms, these tools are designed to simplify your financial life.1. AI-Driven Budgeting Apps (Monarch, YNAB, Copilot)

These apps have evolved into sophisticated financial managers. In 2026, they use AI to analyze your bank statements and identify areas where you can save. They can automatically categorize your spending, identify "subscription creep," and even set aside small amounts of money each week into a high-interest savings account.- Monarch Money: Known for its "household-level" view and customizable categories.

- YNAB (You Need A Budget): A classic for its "zero-based" budgeting philosophy, now with enhanced automation features.

- Copilot Money: A favorite for its sleek interface and AI-driven spending insights.

2. Automated Investment Platforms (Acorns, Betterment, Vanguard)

For those who want to automate their wealth-building, these platforms offer a "set-and-forget" approach to investing.- Acorns: Known for its "round-ups" feature, which automatically invests the change from your daily purchases.

- Betterment: A "robo-advisor" that automatically rebalances your portfolio and optimizes for tax-efficiency.

- Vanguard: A classic for its low-cost index funds and automated "Target Retirement" funds.

3. High-Yield "Sweep" Accounts (Wealthfront, Marcus)

In 2026, many banks offer "sweep" accounts that automatically move excess cash from your checking account into a high-interest savings account.- Wealthfront: Offers a "Cash Account" with a high interest rate and automated "sweep" features.

- Marcus by Goldman Sachs: A classic for its competitive interest rates and easy-to-use interface.

Advanced Automation: Using AI to Optimize Your Cash Flow

In 2026, the next level of financial automation is driven by AI. These advanced tools can not only automate your transfers but also optimize your cash flow in real-time.1. AI-Driven "Smart-Transfers"

Some neo-banks and fintech apps now offer "Smart-Transfers" that use AI to predict your upcoming bills and adjust your automated transfers accordingly. If you have a particularly expensive month coming up, the AI will automatically reduce your savings contribution to ensure you have enough for your fixed costs.2. "Micro-Savings" and "Micro-Investing"

Apps like Plum and Chip use AI to analyze your spending and identify small amounts of money that you "won't miss." These apps then automatically move these "micro-savings" into a high-interest account or an investment fund. Over time, these small amounts can add up to thousands of pounds/dollars.3. Automated Debt Paydown

For those with high-interest debt, AI-driven debt paydown tools can automatically prioritize your highest-interest balances. By using the "Debt Avalanche" or "Debt Snowball" method, these tools can help you pay off your debt faster and save thousands in interest.Common Pitfalls: What to Watch Out For

While an automated money system is a powerful tool for financial success, there are some common pitfalls to watch out for.1. "Set-and-Forget" Doesn't Mean "Ignore"

While an automated system is designed to run without your constant input, you should still check in on your finances at least once a month. This is particularly important for your "Income Hub" and your "Fixed Costs" to ensure all your bills are being paid correctly.2. The "Subscription Creep"

In 2026, many of us have multiple digital subscriptions that we don't even use. By conducting a "subscription audit" and canceling any service you haven't used in the last 30 days, you can save an immediate £50–£100 per month.3. Over-Automation

It's possible to over-automate your finances. If you automate too much of your income into savings and investments, you may find yourself short of cash for your fixed costs or spending money. Ensure you have a "buffer" in your "Income Hub" to account for any unexpected expenses.The 2026 "Set-and-Forget" Strategy: A Deeper Look at Setup

In 2026, the "set-and-forget" strategy is no longer just about paying your bills on time; it’s about a fundamental shift in how we manage our wealth. The introduction of smart-home ecosystems has made it possible to manage your energy usage at a granular level, and your financial life is no different.1. The Impact of Smart-Home Ecosystems

By integrating your smart meter, smart thermostat, and smart appliances into a single ecosystem, you can achieve a level of energy optimization that was previously impossible. For example, your smart dishwasher can now be programmed to run only during off-peak hours when electricity is cheapest. This "load-shifting" strategy can save a typical household an additional £50–£75 ($65–$100) per year on their electricity bill.2. The Rise of "Time-of-Use" Tariffs

With the widespread adoption of smart meters, more energy suppliers are offering Time-of-Use (ToU) Tariffs. These tariffs offer cheaper electricity during periods of low demand (e.g., overnight) and higher prices during peak periods (e.g., 4:00 PM to 7:00 PM). By shifting your most energy-intensive tasks—like laundry and dishwashing—to off-peak hours, you can save an additional 10-15% on your electricity bill.3. The Energy Efficiency "Upgrade"

If you have the budget for it, upgrading your home’s energy efficiency can lead to significant long-term savings. In 2026, the cost of solar panels and battery storage has fallen by over 30% compared to 2021 levels. By generating your own electricity and storing it for use during peak hours, you can reduce your reliance on the grid by 50-70%.The 2026 "Smart-Shopping" Strategy: A Deeper Look at Tools

While the "own-brand" switch is a great start, there are other data-driven ways to reduce your food bill in 2026.1. The "Zero-Waste" Kitchen

In 2026, food waste is no longer just an environmental issue; it’s a financial one. The average UK/US household throws away over £700 ($900) per year in food that could have been eaten [14]. By using "zero-waste" kitchen apps that suggest recipes based on what you already have in your fridge, you can significantly reduce your grocery bill while also helping the environment.2. The "Direct-to-Consumer" Advantage

Many food producers are now selling their products directly to consumers through online marketplaces. By cutting out the "middle-man" (the supermarket), you can often save 10-20% on the shelf price of high-quality produce. This is particularly effective for meat, dairy, and organic vegetables.3. The "Batch-Cooking" Economy

Batch-cooking has become a popular way for busy households to save time and money in 2026. By cooking large quantities of food at once and freezing individual portions, you can reduce your energy usage and avoid the temptation of expensive takeaways.Conclusion: Reclaiming Your Time and Wealth

As we look toward the future, the automated money system will continue to evolve. For many, the key to financial success in 2026 is to be proactive and adaptable. Whether you are a single person in a city flat or a family of four in a suburban semi-detached, understanding the true cost of living is the first step toward effective financial optimization.By understanding the "loyalty penalty" and the "Big Three" expenses, you can build a more accurate and sustainable budget for your household. In 2026, with the widespread adoption of AI-driven energy management and community-led food exchanges, households are increasingly able to "stack" their energy-intensive activities to maximize efficiency.

As you look toward the future, remember that technology and data are your best allies. By staying informed and prepared, you can build a more secure and stable home for yourself and your family.

The Future of Financial Automation: Beyond 2026

As we look toward the future, the integration of AI and personal finance will only deepen. We are moving toward a world of "Autonomous Finance," where your money system doesn't just follow rules but actively makes decisions on your behalf.1. Predictive Wealth Building

Imagine an AI that doesn't just save a fixed percentage of your income but predicts your future income and expenses to optimize your savings in real-time. If the AI sees a high-yield opportunity or a market dip, it could automatically adjust your contributions to maximize your long-term wealth.2. Global Arbitrage for the Average Household

In a more connected digital economy, AI tools may soon allow average households to engage in "global arbitrage"—automatically moving their cash into the highest-yielding currencies or investment vehicles across the globe, a strategy previously reserved for the ultra-wealthy.3. The "Financial Twin" Concept

In the coming years, you may have a "Financial Twin"—a digital model of your entire financial life that allows you to run "what-if" scenarios. Want to know the impact of buying a house in five years or retiring at 50? Your Financial Twin will simulate thousands of possibilities to give you the most accurate roadmap to your goals.By starting your automated money system today, you aren't just simplifying your life in 2026; you are preparing yourself for the next generation of wealth-building technology.

0 Comments Comments