Budgeting

How to Manage a Family of 4 on a Low Income

Managing a household of four people on a tight budget takes planning, not miracles. This guide covers every area of family spending — food, housing, childcare, utilities, and savings — with practical, real-world strategies that actually work in 2026.

Start by writing down every source of income: wages, tax credits, child benefit, Universal Credit (UK) or food stamps/SNAP (US), and anything else. Then list every outgoing, broken down into three types: fixed costs that are the same every month (rent, mortgage, loan repayments, phone contracts), variable essential costs (food, fuel, utilities), and discretionary spending (takeaways, streaming, clothing beyond basics).

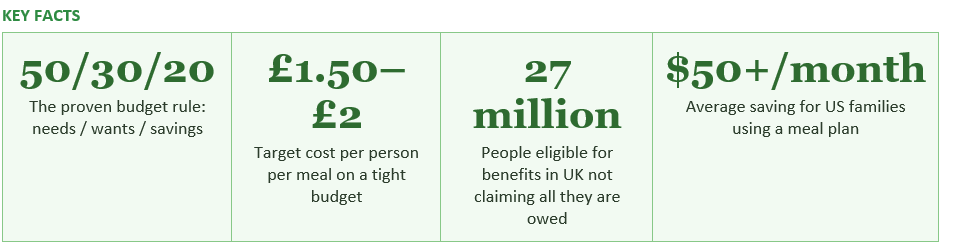

A widely recommended framework for families on tight budgets is the 50/30/20 rule: allocate 50% of net income to needs (housing, food, utilities, transport to work), 30% to wants (entertainment, eating out, non-essential clothing), and 20% to savings and debt repayment. On a low income, you may find this ratio needs adjusting — perhaps 70/15/15 — but having any structure is better than none. Most families who track their spending carefully discover at least one or two areas where small reductions are possible without any meaningful impact on quality of life.

Never assume you do not qualify for support. Benefits systems are designed to help families who are working, not just those who are not. Use an online benefits calculator every six months — your circumstances change, and so do the rules.

— CITIZENS ADVICE / TURN2US (UK, 2026)

A good meal plan for a family of four on a tight budget prioritises ingredients that do double duty across multiple meals. A whole chicken can provide a roast dinner, sandwiches, and a soup or stew. A batch of bolognese sauce can go over pasta on Monday and with rice or baked potatoes on Wednesday. Eggs are one of the best-value sources of protein available — at around 20 to 25p each in the UK and 20 to 30 cents in the US, they are cheaper per gramme of protein than most meats.

Batch cooking and freezing is another strategy that saves both money and time. Making a large pot of soup, a batch of curries, or a tray of muffins and freezing portions means you always have a cheap, ready-made meal available — reducing the temptation to order a takeaway when you are tired and unprepared.

If you are a homeowner with a mortgage, contact your lender to discuss any available mortgage support if you are struggling with payments. Most UK lenders now have a mortgage support charter offering options including payment deferrals, interest-only switches, and extended terms. In the US, contact your loan servicer about forbearance options or income-driven repayment plans if applicable.

In the US, LIHEAP provides energy bill assistance for qualifying families, and many utility companies offer low-income rate programmes — contact your energy provider directly to ask what is available. Energy efficiency measures such as sealing draughts, using programmable thermostats, and washing clothes in cold water all reduce bills meaningfully over the year.

In both countries, cycling is one of the most cost-effective commuting options available. The UK's Cycle to Work scheme allows employees to purchase a bicycle and equipment tax-free through salary sacrifice, saving 32% to 42% on the cost. Children who cycle to school also eliminate the need for school transport costs entirely in many cases.

The most important step for any family with a child under five is to check their entitlement to free childcare hours. As of September 2025, working parents of children aged 9 months to 4 years in England can access 15 to 30 hours per week of government-funded childcare, depending on their working hours and income. This can save families thousands of pounds per year and represents one of the most valuable benefits available to low-income working families.

Tax-Free Childcare (UK) is another underused benefit. For every £8 you deposit into an online Tax-Free Childcare account, the government adds £2 — effectively a 25% top-up on childcare costs up to a maximum government contribution of £2,000 per child per year (£4,000 for disabled children). In the US, the Dependent Care FSA allows families to pay up to $5,000 of dependent care costs from pre-tax earnings, saving federal income tax on that amount.

If formal childcare is not available or affordable, explore whether informal arrangements with family members, mutual childcare swaps with other parents, or community childminder networks can reduce costs. Many areas also have subsidised childcare available through charities, housing associations, or local authority schemes — your health visitor or children's centre can often point you toward what is available locally.

The most effective approach is to automate any saving, however small. Setting up a standing order or automatic transfer that moves even a small amount into a separate savings account on the day you are paid means the money is gone before you have a chance to spend it. Several UK banks and apps — including Monzo, Starling, and Chip — offer round-up features that save the spare change from every transaction automatically. Over a month, this can quietly accumulate £15 to £30 without any conscious effort.

In the UK, a Help to Save account is available to people receiving Universal Credit or Working Tax Credit. The government adds a 50p bonus for every £1 saved, with a maximum government bonus of £1,200 over four years. This is one of the best risk-free returns available anywhere in the financial system and is available specifically to low-income savers. In the US, the Saver's Match programme — launching in 2027 under SECURE 2.0 — will provide a 50% federal match on retirement savings contributions for lower-income workers, worth up to $1,000 per year.

The standard advice to have three to six months of expenses saved is not realistic for most low-income families in the short term. A more achievable goal is to build a starter emergency fund of £500 to £1,000 (or $500 to $1,000) over the next six to twelve months. That modest sum covers the majority of the unexpected costs that derail low-income family budgets most frequently.

If you are building an emergency fund while also paying off debt — particularly high-interest debt — a common strategy is to pause debt overpayments temporarily to build the emergency fund first, then resume overpayments once the fund is established. Without an emergency fund, any unexpected cost will simply create more debt, negating any progress you have made.

Avoid keeping your emergency fund in your regular current account, where it is too easy to spend. A separate instant-access savings account — ideally with a different bank or building society from your main account — adds a small psychological barrier that helps preserve the money for genuine emergencies.

The good news is that some of the most consistently enjoyable family activities cost very little or nothing at all. Libraries remain one of the greatest free family resources in both the UK and US — most offer free books, DVDs, online resources, and regular children's events including reading groups, craft sessions, and holiday activities. In the UK, many museums — including all the national museums in London and many regional ones — are free to enter. The National Trust and English Heritage offer free membership to children under 5, and discounted family memberships that cover multiple visits throughout the year.

Outdoor activities cost nothing. Exploring local parks, walking trails, beaches, and nature reserves provides excellent family time at zero cost. In the UK, Holiday Activities and Food (HAF) programmes provide free activities and hot meals for children on free school meals during school holidays — contact your local council to find out what is available in your area. In the US, the Summer EBT programme (launched 2024) provides food assistance for eligible children during the summer when school meals are unavailable.

For birthdays and Christmas, setting clear, honest expectations with your children early — and redirecting focus from expensive gifts toward experiences, family activities, and handmade or second-hand presents — can dramatically reduce the cost of these occasions without reducing the joy. Children consistently report that time and attention from their parents matter far more to them than the value of presents.

What the evidence does show is that the families who manage best on limited incomes share a few key habits: they know where their money goes, they claim every penny of support they are entitled to, they plan their meals and shopping rather than improvising, and they put even a small amount of money aside for emergencies before spending on anything discretionary. None of these require large sums to start. All of them compound over time. And the sense of control that comes from having a plan — however modest — is one of the most valuable things money can provide.

TABLE OF CONTENTS

- Know Where Your Money Actually Goes: Build a Family Budget

- Benefits and Support You May Be Missing

- Feeding a Family of Four Without Breaking the Bank

- Cutting Your Biggest Bills: Housing, Energy and Transport

- Childcare Costs: Getting Help and Cutting Costs

- Saving When Money Is Tight

- Building an Emergency Fund on a Low Income

- Free and Low-Cost Activities for Families

- Protecting Your Family's Financial Future

- Conclusion

- Frequently Asked Questions

- References

Know Where Your Money Actually Goes: Build a Family Budget

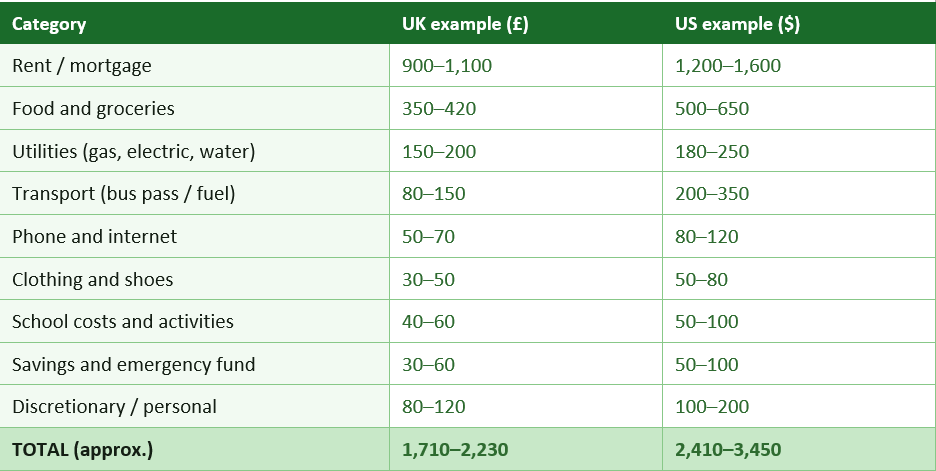

The single most powerful thing a low-income family of four can do is understand exactly where every pound or dollar goes each month. This sounds obvious, but research consistently shows that most households — at all income levels — significantly underestimate what they spend in several categories, particularly food, small daily purchases, and subscriptions.Start by writing down every source of income: wages, tax credits, child benefit, Universal Credit (UK) or food stamps/SNAP (US), and anything else. Then list every outgoing, broken down into three types: fixed costs that are the same every month (rent, mortgage, loan repayments, phone contracts), variable essential costs (food, fuel, utilities), and discretionary spending (takeaways, streaming, clothing beyond basics).

A widely recommended framework for families on tight budgets is the 50/30/20 rule: allocate 50% of net income to needs (housing, food, utilities, transport to work), 30% to wants (entertainment, eating out, non-essential clothing), and 20% to savings and debt repayment. On a low income, you may find this ratio needs adjusting — perhaps 70/15/15 — but having any structure is better than none. Most families who track their spending carefully discover at least one or two areas where small reductions are possible without any meaningful impact on quality of life.

A simple monthly budget template for a family of four

Benefits and Support You May Be Missing

One of the most important and underused tools for low-income families is the benefits system. An estimated 27 million people in the UK are eligible for at least some support they are not currently claiming, including benefits, grants, and discounts they are entitled to by law but may not know about. In the US, the picture is similar: the Urban Institute estimates that only about 80% of eligible families claim SNAP benefits, and participation rates for other programmes are even lower.UK: Benefits and support for families

UK benefits and support to check for 2026

- Universal Credit: The main benefit for working-age families on low incomes. If you have children and are working, you can still claim — many working families do not realise they qualify. Use entitledto.co.uk or Turn2Us to check your eligibility.

- Child Benefit: £26.05 per week for the first child and £17.25 per week for each additional child in 2026/27. Paid regardless of income below the High Income Child Benefit Charge threshold.

- Free School Meals: Children in Reception to Year 2 qualify automatically. Beyond that, eligibility is means-tested — your child qualifies if you receive Universal Credit with net earnings below £7,400, or certain other benefits.

- Healthy Start vouchers: If you are more than 10 weeks pregnant or have a child under 4 and receive qualifying benefits, you get £4.25 per week to spend on milk, fruit, and vegetables.

- Council Tax Reduction: Apply to your local council — up to 100% reduction is available depending on income and household size.

- Help with NHS costs: Low-income families may qualify for free prescriptions, dental treatment, eye tests, and glasses through the NHS Low Income Scheme (HC1 form).

- Warm Home Discount: A one-off £150 annual discount on electricity bills for eligible low-income households.

- Free childcare hours: From September 2025, eligible working parents of children aged 9 months to 4 years can access up to 30 hours per week of free childcare.

US: Federal and state support programmes

US benefits and support to check for 2026

- SNAP (Supplemental Nutrition Assistance Program): A family of 4 with a gross monthly income at or below 130% of the poverty line ($3,250/month in 2026) may be eligible for food assistance averaging $700+ per month.

- Medicaid and CHIP: Low-income families may qualify for free or very low-cost health coverage through Medicaid. Children may be eligible for CHIP even if parents are not on Medicaid.

- Child Tax Credit: Up to $2,000 per qualifying child under 17 in 2026, with up to $1,700 refundable per child. Income phase-outs apply above $200,000 (single) / $400,000 (married).

- Earned Income Tax Credit (EITC): A refundable tax credit worth up to $7,830 in 2026 for a family with three or more qualifying children. Many eligible families do not claim it.

- WIC (Women, Infants and Children): Free nutritious food, baby formula, and health services for pregnant women, new mothers, and children under 5 who qualify on income grounds.

- LIHEAP (Low Income Home Energy Assistance Program): Helps pay for heating and cooling costs. Apply through your state agency.

- Head Start and Early Head Start: Free early childhood education programmes for low-income children from birth to 5.

- School breakfast and lunch programmes: Children from families earning up to 185% of the poverty line qualify for reduced-price meals; those below 130% qualify for free meals.

Never assume you do not qualify for support. Benefits systems are designed to help families who are working, not just those who are not. Use an online benefits calculator every six months — your circumstances change, and so do the rules.

— CITIZENS ADVICE / TURN2US (UK, 2026)

Feeding a Family of Four Without Breaking the Bank

Food is often the biggest area where a low-income family can make meaningful savings without feeling deprived. The average family spends significantly more on food than they need to simply because of the way they shop — without a plan, without a list, and with a tendency to pick up extra items or expensive branded goods out of habit.Meal planning: the single biggest food saving

Meal planning — deciding in advance what you will eat for the week and shopping only for those ingredients — is the most consistently effective way to reduce a family food bill. Research from the USDA and various UK consumer studies suggests that families who meal plan save between 20% and 30% on their weekly food spend compared with those who shop without a plan. For a family spending £100 per week on food, that is £20 to £30 saved per week, or £1,000 to £1,500 per year.A good meal plan for a family of four on a tight budget prioritises ingredients that do double duty across multiple meals. A whole chicken can provide a roast dinner, sandwiches, and a soup or stew. A batch of bolognese sauce can go over pasta on Monday and with rice or baked potatoes on Wednesday. Eggs are one of the best-value sources of protein available — at around 20 to 25p each in the UK and 20 to 30 cents in the US, they are cheaper per gramme of protein than most meats.

Shopping smarter

Where you shop matters as much as what you buy. In the UK, Aldi and Lidl consistently offer the lowest overall basket prices — typically 20% to 30% cheaper than major supermarkets for equivalent items. In the US, Aldi, Walmart Neighborhood Market, and discount grocers like WinCo or Save-A-Lot offer similar value. Buying own-brand or store-brand products instead of branded equivalents can cut your food bill by a further 20% to 40% on most categories, with no meaningful difference in quality for staples like pasta, rice, tinned tomatoes, and cereals.Batch cooking and freezing is another strategy that saves both money and time. Making a large pot of soup, a batch of curries, or a tray of muffins and freezing portions means you always have a cheap, ready-made meal available — reducing the temptation to order a takeaway when you are tired and unprepared.

30 cheap, nutritious family meals under £2 per person (UK) / $3 per person (US)

- Pasta with homemade tomato and vegetable sauce

- Rice and lentil dhal with flatbread

- Baked potatoes with beans and grated cheese

- Egg fried rice with frozen vegetables

- Bean and vegetable soup with crusty bread

- Chicken thigh casserole (thighs are far cheaper than breasts)

- Overnight oats with banana and honey for breakfast

- Homemade pizza on pitta or flatbread with whatever topping you have

- Tuna pasta bake with tinned tuna and cream of mushroom soup

- Chilli con carne stretched with extra kidney beans and served with rice

Cutting Your Biggest Bills: Housing, Energy and Transport

Housing

Housing is typically the largest single item in any family budget. If you rent privately, the most direct way to reduce this cost is to negotiate your rent when your tenancy comes up for renewal, particularly if you have been a reliable, long-term tenant. Landlords often prefer to keep good tenants at a slightly lower rent than face the cost and inconvenience of finding new ones. If your rent is unaffordable, it may also be worth contacting your local council to go on the housing register for social housing, or checking whether you qualify for Local Housing Allowance through Universal Credit.If you are a homeowner with a mortgage, contact your lender to discuss any available mortgage support if you are struggling with payments. Most UK lenders now have a mortgage support charter offering options including payment deferrals, interest-only switches, and extended terms. In the US, contact your loan servicer about forbearance options or income-driven repayment plans if applicable.

Energy

In the UK, you can reduce your energy bills by switching to a cheaper tariff — use comparison sites like Uswitch or MoneySuperMarket — and by claiming the Warm Home Discount (£150 off your electricity bill for eligible households). Simple behavioural changes also make a measurable difference: turning down your thermostat by 1 degree Celsius saves approximately 10% on heating bills, draught-proofing doors and windows reduces heat loss significantly, and switching to LED bulbs can save around £65 per year on electricity for an average UK household.In the US, LIHEAP provides energy bill assistance for qualifying families, and many utility companies offer low-income rate programmes — contact your energy provider directly to ask what is available. Energy efficiency measures such as sealing draughts, using programmable thermostats, and washing clothes in cold water all reduce bills meaningfully over the year.

Transport

Car ownership is often a major but hidden expense for low-income families — when you add up finance payments, insurance, fuel, servicing, and road tax or registration, a car can cost £4,000 to £8,000 per year to run in the UK. If public transport can meet most of your family's travel needs, switching from car ownership to a combination of buses, trains, and occasional car hire may save thousands of pounds per year. If a car is essential, compare insurance quotes annually, consider telematics insurance for younger drivers, and keep up with servicing to avoid expensive repairs.In both countries, cycling is one of the most cost-effective commuting options available. The UK's Cycle to Work scheme allows employees to purchase a bicycle and equipment tax-free through salary sacrifice, saving 32% to 42% on the cost. Children who cycle to school also eliminate the need for school transport costs entirely in many cases.

Childcare Costs: Getting Help and Cutting Costs

For families with young children, childcare is often the second-largest cost after housing — and in many cases it exceeds housing. A full-time nursery place in England costs an average of £14,000 to £17,000 per year for a child under two, according to the Coram Family and Childcare survey. In the US, the average annual cost of full-time childcare for an infant ranges from $8,000 in Mississippi to over $25,000 in Washington DC.The most important step for any family with a child under five is to check their entitlement to free childcare hours. As of September 2025, working parents of children aged 9 months to 4 years in England can access 15 to 30 hours per week of government-funded childcare, depending on their working hours and income. This can save families thousands of pounds per year and represents one of the most valuable benefits available to low-income working families.

Tax-Free Childcare (UK) is another underused benefit. For every £8 you deposit into an online Tax-Free Childcare account, the government adds £2 — effectively a 25% top-up on childcare costs up to a maximum government contribution of £2,000 per child per year (£4,000 for disabled children). In the US, the Dependent Care FSA allows families to pay up to $5,000 of dependent care costs from pre-tax earnings, saving federal income tax on that amount.

If formal childcare is not available or affordable, explore whether informal arrangements with family members, mutual childcare swaps with other parents, or community childminder networks can reduce costs. Many areas also have subsidised childcare available through charities, housing associations, or local authority schemes — your health visitor or children's centre can often point you toward what is available locally.

Saving When Money Is Tight

Telling a family on a low income to save money can feel tone-deaf — if money is tight, what exactly is there to save? The honest answer is that for many families, even small regular savings — as little as £5 or $5 per week — can make a transformative difference over time, and the act of saving, however modestly, provides a psychological buffer against the anxiety of financial insecurity.The most effective approach is to automate any saving, however small. Setting up a standing order or automatic transfer that moves even a small amount into a separate savings account on the day you are paid means the money is gone before you have a chance to spend it. Several UK banks and apps — including Monzo, Starling, and Chip — offer round-up features that save the spare change from every transaction automatically. Over a month, this can quietly accumulate £15 to £30 without any conscious effort.

In the UK, a Help to Save account is available to people receiving Universal Credit or Working Tax Credit. The government adds a 50p bonus for every £1 saved, with a maximum government bonus of £1,200 over four years. This is one of the best risk-free returns available anywhere in the financial system and is available specifically to low-income savers. In the US, the Saver's Match programme — launching in 2027 under SECURE 2.0 — will provide a 50% federal match on retirement savings contributions for lower-income workers, worth up to $1,000 per year.

Building an Emergency Fund on a Low Income

An emergency fund — a pot of money set aside to cover unexpected costs without needing to borrow — is the difference between a financial shock and a financial crisis. When your car breaks down, a child needs new glasses, or a household appliance fails, having even £500 or $500 saved means you can cover it without resorting to a credit card, payday loan, or buy-now-pay-later debt that could cost many times more in interest.The standard advice to have three to six months of expenses saved is not realistic for most low-income families in the short term. A more achievable goal is to build a starter emergency fund of £500 to £1,000 (or $500 to $1,000) over the next six to twelve months. That modest sum covers the majority of the unexpected costs that derail low-income family budgets most frequently.

If you are building an emergency fund while also paying off debt — particularly high-interest debt — a common strategy is to pause debt overpayments temporarily to build the emergency fund first, then resume overpayments once the fund is established. Without an emergency fund, any unexpected cost will simply create more debt, negating any progress you have made.

Avoid keeping your emergency fund in your regular current account, where it is too easy to spend. A separate instant-access savings account — ideally with a different bank or building society from your main account — adds a small psychological barrier that helps preserve the money for genuine emergencies.

Free and Low-Cost Activities for Families

One of the greatest sources of pressure on low-income family budgets is the cost of keeping children entertained and occupied, particularly during school holidays. Birthday parties, days out, sports clubs, and school trips can all add up to significant sums that many families feel unable to say no to without their children missing out.The good news is that some of the most consistently enjoyable family activities cost very little or nothing at all. Libraries remain one of the greatest free family resources in both the UK and US — most offer free books, DVDs, online resources, and regular children's events including reading groups, craft sessions, and holiday activities. In the UK, many museums — including all the national museums in London and many regional ones — are free to enter. The National Trust and English Heritage offer free membership to children under 5, and discounted family memberships that cover multiple visits throughout the year.

Outdoor activities cost nothing. Exploring local parks, walking trails, beaches, and nature reserves provides excellent family time at zero cost. In the UK, Holiday Activities and Food (HAF) programmes provide free activities and hot meals for children on free school meals during school holidays — contact your local council to find out what is available in your area. In the US, the Summer EBT programme (launched 2024) provides food assistance for eligible children during the summer when school meals are unavailable.

For birthdays and Christmas, setting clear, honest expectations with your children early — and redirecting focus from expensive gifts toward experiences, family activities, and handmade or second-hand presents — can dramatically reduce the cost of these occasions without reducing the joy. Children consistently report that time and attention from their parents matter far more to them than the value of presents.

Protecting Your Family's Financial Future

When money is tight, thinking about the future can feel like a luxury. But a few low-cost or free protective steps can make an enormous difference if things go wrong.Low-cost steps to protect your family financially

- Make a will: In the UK, dying without a will (intestate) means your estate is distributed according to fixed rules that may not reflect your wishes, and can cause serious hardship for surviving partners who are not married. Basic wills can be made for free during national will-writing campaigns (usually October) run by organisations including the National Free Wills Network.

- Check your life insurance: If you have dependants, a basic level of life insurance is essential. Many people are surprised how cheap term life insurance is for younger, non-smoking adults — a 20-year level term policy for £100,000 cover can cost as little as £5 to £8 per month.

- Build your credit score: A good credit score means cheaper borrowing if you ever need it. Registering on the electoral roll, paying all bills on time, and keeping credit card balances below 30% of your limit all improve your score over time.

- Know your rights at work: Ensure you are receiving the National Living Wage (£12.21 per hour from April 2026 for over-21s in UK), statutory sick pay, and all statutory entitlements. ACAS (UK) and the Department of Labor (US) both provide free guidance on workers' rights.

- Get debt help early: If debt is becoming unmanageable, seek free advice sooner rather than later. StepChange (UK) and the NFCC (US) both offer free, confidential debt advice with no pressure and no fees.

CONCLUSION

Managing a family of four on a low income is genuinely hard. The cost pressures are real, the margins are thin, and the emotional weight of trying to provide for your family on a tight budget is something that only people who have lived it truly understand. This guide does not pretend otherwise.What the evidence does show is that the families who manage best on limited incomes share a few key habits: they know where their money goes, they claim every penny of support they are entitled to, they plan their meals and shopping rather than improvising, and they put even a small amount of money aside for emergencies before spending on anything discretionary. None of these require large sums to start. All of them compound over time. And the sense of control that comes from having a plan — however modest — is one of the most valuable things money can provide.

0 Comments Comments