Savings

How to Save $5,000 in 6 Months: Step-by-Step Guide

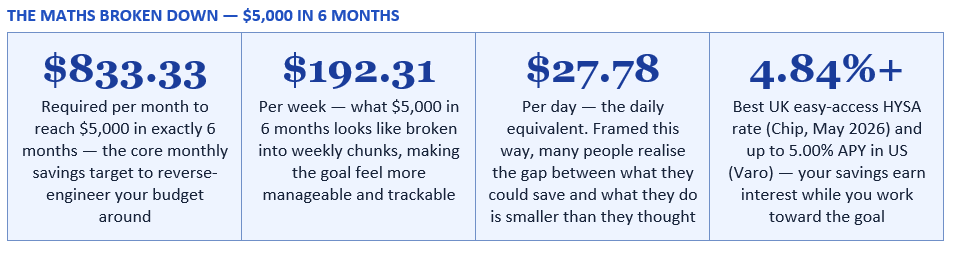

$5,000 in six months is $833.33 per month. That is $192.31 per week, or $27.78 per day. Written as a daily figure, it stops sounding impossible and starts sounding like a decision. This guide breaks the $5,000 target into a concrete six-month plan with specific monthly actions, the biggest expense levers to pull first, the automation strategies that make saving feel effortless, and the motivational systems that keep people going past month two when enthusiasm fades.

The reason most people do not save $5,000 in six months is not that they cannot — it is that they have never built a specific plan to do it. Without a plan, saving is passive: whatever is left at the end of the month goes to savings, which is typically nothing. With a specific plan, saving becomes active: a defined amount leaves for savings first, and the rest is spent.

Fidelity's March 2026 savings guide makes this arithmetic clear: saving $5,000 in one year requires $417 per month or $14 per day. At the six-month target, the figure doubles to $833 per month — still achievable for many households when the specific steps in this guide are applied. The Hustle Scientist's January 2026 first-person account of saving $5,000 in six months demonstrates that it is possible without a six-figure salary: 'I wasn't earning a six-figure salary or living rent-free with my parents. I had bills, responsibilities, and temptations like everyone else. But with a bit of strategy and a lot of motivation, I made it happen.'

The three levers that make it achievable are spending reduction (cutting the expenses that are not serving you without cutting the life you enjoy), income increase (adding even one modest side income stream), and automation (removing the decision from the process entirely by making the saving happen automatically). None of these requires exceptional income, exceptional discipline, or exceptional sacrifice. They require a plan — and this is the plan.

I concentrated on the 'Big Three' expenses where you can save hundreds of dollars all at once rather than becoming fixated on a $5 coffee. I saved $300 a month just from meal planning alone.

— THE HUSTLE SCIENTIST — HOW I SAVED $5,000 IN 6 MONTHS WITHOUT GIVING UP COFFEE (MEDIUM, JANUARY 2026)

A worked example: take-home income of $3,200 per month. Current saving: $0 (spending everything each month). Savings gap: $833. The goal is to find $833 per month from a combination of (a) spending that can be cut — subscriptions, dining out, discretionary shopping, impulse purchases — and (b) additional income. The steps below show where the money most commonly comes from.

The Medium/Hustle Scientist's January 2026 account makes the HYSA case emphatically: 'A High-Yield Savings Account was the main factor in my success. My money actually increased while it was there due to interest rates in 2026.' At the best available rates in May 2026 — up to 5.00% APY in the US (Varo Money) and 4.84% easy-access AER in the UK (Chip) — a growing $5,000 balance earns meaningful interest during the accumulation period. By month five with $4,167 already saved, the account is earning approximately $17 per month in interest — which is the equivalent of two no-spend evenings in or a week of packed lunches.

The separation principle is as important as the interest rate. Money sitting in the same account as your spending money is money that will be spent. A separate account — ideally at a different bank from your main current account, with a slight transfer delay — creates the friction that prevents casual raiding of the savings balance. Name the account explicitly: '6-Month Challenge' or 'Emergency Fund Goal' — the named destination makes the money psychologically unavailable for spending in a way that a generic savings account does not.

The Hustle Scientist's January 2026 account describes exactly how this worked: 'Every Monday, my bank set up an automatic transfer of $210 from my checking account to my savings account. Out of sight, out of mind. The money was already moved, even when I was tempted to spend. It forced me to live on what was left — and surprisingly, I managed just fine.' This is the experience of most people who implement automated savings for the first time: the adjustment to the reduced available balance happens within two to three pay cycles, and the savings accumulate without requiring any active willpower.

For the $5,000/six-month target, the automatic transfer should be set to $833.33 if paid monthly, or $416.67 if paid bi-weekly. Set this up on the first payday of the challenge. Do not set it up next week or when things calm down — set it up today, before any other step. Money Bliss's practical savings guide confirms: 'Paying yourself first means putting money into savings before you spend it. Instead of waiting to see what's left, you save right away. This helps you treat saving like a bill that has to be paid.'

The Vocal Media $5,000 account describes using a progress tracker to stay motivated: 'I developed a small progress monitor. Every $500 I saved, I'd colour in a square. It made the goal feel real and satisfying.' Applying the same visual progress approach to no-spend days — tracking them on a calendar or app — creates a game-like motivation that makes the habit more sustainable. Money Bliss's savings guide identifies the 7-day no-spend challenge as a particularly effective entry point for those new to structured saving.

Aim for two to three no-spend days per week throughout the six-month challenge. At an average of $25 to $40 in daily discretionary spending, two no-spend days per week saves $200 to $320 per month — a significant contribution toward the $833 monthly target. The cumulative six-month saving from this habit alone is $1,200 to $1,920.

The windfall rule is simple: when unexpected money arrives, the first question is not 'what shall I buy?' but 'how much of this can go straight to my $5,000 goal?' A $500 tax refund applied in month two means month two requires only $333 in regular monthly saving rather than $833 — relieving pressure and accelerating the timeline. Fidelity's March 2026 guidance specifically identifies tax refunds as one of the most impactful windfall opportunities: checking your tax withholding (W-4) and ensuring you are capturing all tax credits you are eligible for can produce a meaningful refund that, applied to a savings goal, is the equivalent of several months of disciplined monthly saving in a single deposit.

The psychological principle behind the windfall rule is pre-commitment. By establishing the rule before any windfall arrives — 'any unexpected money goes to the savings account first' — you remove the in-the-moment decision about whether to spend or save it. Pre-commitment beats willpower every time.

The principle from SmartMoneyTrek and InCharge's budgeting guidance applies directly here: a budget that requires revision is not a failed budget. It is a living plan that responds to reality. If month three produces only $500 rather than $833, the response is not abandonment — it is recalibration. Add the $333 shortfall to month four's target. Identify what caused the shortfall (a specific unexpected expense? a discipline failure in a specific category?) and address it before month four. A bad month slightly extends the timeline. Quitting ends it entirely.

The easiest tactical response to a shortfall month is to increase the following month's side income target. If selling $200 of items in month three was the plan but only $100 was achieved, listing $300 worth of items for month four recovers the difference. The side income stream is the most flexible component of the plan — it can be increased or decreased depending on what the month requires.

The person who reaches $5,000 in six months has not just saved $5,000. They have built a set of financial habits — automation, intentional spending, side income awareness, progress tracking, accountability — that are now available to every subsequent financial goal. The emergency fund becomes the house deposit. The house deposit becomes the investment account. The six-month challenge is the beginning of a relationship with money that compounds long beyond the target date.

Medium / The Hustle Scientist — How I Saved $5,000 in 6 Months Without Giving Up Coffee (January 2026) https://medium.com/@maqsoodfareed41/how-i-saved-5-000-in-6-months-without-giving-up-coffee-3adde4e2ffda

Vocal Media — How I Saved $5,000 in 6 Months: A Real-Life Guide to Reaching Your Savings Goal https://vocal.media/education/how-i-saved-5-000-in-6-months

Money Bliss — Smart Tips to Reach $5,000 in Savings in 6 Months (July 2025) https://moneybliss.org/tips-to-save-5000-in-6-months/

Stash — How to Save $5,000 in 6 Months: Actionable Strategies https://www.stash.com/learn/how-to-save-5000-in-6-months/

Bankrate — Save Money Calculator: How Much to Save Each Month https://www.bankrate.com/banking/savings/save-money-calculator/

DollarWiseLiving — How to Save $5,000 in Just 6 Months: A Step-by-Step Guide (February 2025) https://dollarwiseliving.wordpress.com/2025/02/25/how-to-save-5000-in-just-6-months-a-step-by-step-guide/

SmartMoneyTrek — How to Budget on a Low Income: 10 Practical Strategies (March 2026) https://smartmoneytrek.com/how-to-budget-on-a-low-income

Makeheadway — How to Save Money Fast on a Low Income (2025) https://makeheadway.com/blog/how-to-save-money-fast-on-low-income/

TABLE OF CONTENTS

- Why $5,000 in 6 Months Is Achievable for Most People

- Before You Start: The Two Non-Negotiables

- Step 1 — Calculate Your Real Savings Gap

- Step 2 — Open a Dedicated High-Yield Savings Account

- Step 3 — Automate the Transfer Before You Can Spend It

- Step 4 — Attack the Big Three Expenses First

- Step 5 — Build Weekly No-Spend Habits

- Step 6 — Add a Side Income Stream

- Step 7 — Use Windfalls Strategically

- The Month-by-Month Milestone Plan

- Staying Accountable: The Two Tools That Actually Work

- What to Do When You Have a Bad Month

- Conclusion

- Frequently Asked Questions

- References

Why $5,000 in 6 Months Is Achievable for Most People

The reason most people do not save $5,000 in six months is not that they cannot — it is that they have never built a specific plan to do it. Without a plan, saving is passive: whatever is left at the end of the month goes to savings, which is typically nothing. With a specific plan, saving becomes active: a defined amount leaves for savings first, and the rest is spent.Fidelity's March 2026 savings guide makes this arithmetic clear: saving $5,000 in one year requires $417 per month or $14 per day. At the six-month target, the figure doubles to $833 per month — still achievable for many households when the specific steps in this guide are applied. The Hustle Scientist's January 2026 first-person account of saving $5,000 in six months demonstrates that it is possible without a six-figure salary: 'I wasn't earning a six-figure salary or living rent-free with my parents. I had bills, responsibilities, and temptations like everyone else. But with a bit of strategy and a lot of motivation, I made it happen.'

The three levers that make it achievable are spending reduction (cutting the expenses that are not serving you without cutting the life you enjoy), income increase (adding even one modest side income stream), and automation (removing the decision from the process entirely by making the saving happen automatically). None of these requires exceptional income, exceptional discipline, or exceptional sacrifice. They require a plan — and this is the plan.

I concentrated on the 'Big Three' expenses where you can save hundreds of dollars all at once rather than becoming fixated on a $5 coffee. I saved $300 a month just from meal planning alone.

— THE HUSTLE SCIENTIST — HOW I SAVED $5,000 IN 6 MONTHS WITHOUT GIVING UP COFFEE (MEDIUM, JANUARY 2026)

Before You Start: The Two Non-Negotiables

Two things must be in place before the six-month plan begins. Without them, the plan will stall within weeks.Non-negotiable 1: A specific written reason

Vocal Media's first-person $5,000 savings account identifies this as the first and most important action: 'I needed to really think about the reasons why I wanted to save money before I could save anything. Having that goal in mind kept me motivated. I wrote it on a sticky note and placed it on my laptop: $5,000 by [target date] — You Got This!' The reason does not have to be grand. It can be an emergency fund, a down payment, a car repair buffer, a holiday, or simply the experience of having $5,000 in a bank account for the first time. What matters is that it is specific, written down, and visible.Non-negotiable 2: A 30-day spending audit before Month 1

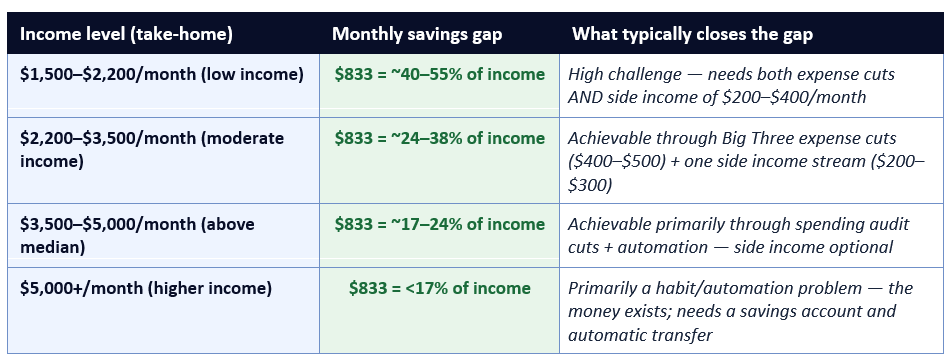

You cannot make a $833/month savings plan work if you do not know where your current money is going. Before starting the plan, pull 30 days of bank and card statements, categorise every transaction, and total each category. This single step reveals the specific expense categories where the savings gap can be found. Most people who do this exercise find three to five categories where spending is higher than they assumed and where reductions are possible without meaningful impact on quality of life.Step 1 — Calculate Your Real Savings Gap

Once you have your 30-day spending data, the maths of the plan become specific to your situation. Subtract your current monthly saving from $833. The result is your savings gap — the additional monthly saving you need to find. This gap is then closed through the combination of spending reductions and income additions that follow.A worked example: take-home income of $3,200 per month. Current saving: $0 (spending everything each month). Savings gap: $833. The goal is to find $833 per month from a combination of (a) spending that can be cut — subscriptions, dining out, discretionary shopping, impulse purchases — and (b) additional income. The steps below show where the money most commonly comes from.

Step 2 — Open a Dedicated High-Yield Savings Account

The account where your $5,000 lives during the six-month journey matters. There are two requirements: the account must be separate from your everyday checking/current account, so the balance is not visible or easily spent; and it must pay a competitive interest rate, so your savings earn something while you are accumulating.The Medium/Hustle Scientist's January 2026 account makes the HYSA case emphatically: 'A High-Yield Savings Account was the main factor in my success. My money actually increased while it was there due to interest rates in 2026.' At the best available rates in May 2026 — up to 5.00% APY in the US (Varo Money) and 4.84% easy-access AER in the UK (Chip) — a growing $5,000 balance earns meaningful interest during the accumulation period. By month five with $4,167 already saved, the account is earning approximately $17 per month in interest — which is the equivalent of two no-spend evenings in or a week of packed lunches.

The separation principle is as important as the interest rate. Money sitting in the same account as your spending money is money that will be spent. A separate account — ideally at a different bank from your main current account, with a slight transfer delay — creates the friction that prevents casual raiding of the savings balance. Name the account explicitly: '6-Month Challenge' or 'Emergency Fund Goal' — the named destination makes the money psychologically unavailable for spending in a way that a generic savings account does not.

Step 3 — Automate the Transfer Before You Can Spend It

The single most effective action in this entire guide is setting up an automatic transfer from your checking account to your dedicated savings account on payday — before any discretionary spending occurs. This is the financial principle of paying yourself first, and it is the mechanism that distinguishes people who achieve savings goals from those who perpetually intend to.The Hustle Scientist's January 2026 account describes exactly how this worked: 'Every Monday, my bank set up an automatic transfer of $210 from my checking account to my savings account. Out of sight, out of mind. The money was already moved, even when I was tempted to spend. It forced me to live on what was left — and surprisingly, I managed just fine.' This is the experience of most people who implement automated savings for the first time: the adjustment to the reduced available balance happens within two to three pay cycles, and the savings accumulate without requiring any active willpower.

For the $5,000/six-month target, the automatic transfer should be set to $833.33 if paid monthly, or $416.67 if paid bi-weekly. Set this up on the first payday of the challenge. Do not set it up next week or when things calm down — set it up today, before any other step. Money Bliss's practical savings guide confirms: 'Paying yourself first means putting money into savings before you spend it. Instead of waiting to see what's left, you save right away. This helps you treat saving like a bill that has to be paid.'

Step 4 — Attack the Big Three Expenses First

Rather than trying to squeeze savings from dozens of small spending categories simultaneously, focus first on the three expense categories where meaningful reductions produce the largest cash savings per unit of effort. These are housing and utilities, transportation, and food.Food: the biggest single controllable household expense

The Hustle Scientist's January 2026 account documents that meal planning alone saved $300 per month: 'I adopted a rigorous meal planning schedule in place of boredom shopping. I saved $300 a month just from this.' This is a consistently achievable reduction for households that shift from reactive grocery shopping (buying what feels right in the moment) to planned shopping (buying specifically what a weekly meal plan requires). The practical actions are straightforward: plan seven dinners before the weekly shop, write a precise list, shop from the list, and batch cook where possible. Carrying packed lunches to work rather than buying lunch out saves $50 to $150 per month for most full-time workers.Housing and utilities

The Hustle Scientist also negotiated their internet bill and installed a smart thermostat, reducing electricity by 15%. On a $150/month electricity bill, 15% is $22.50 per month — or $270 over the six-month challenge. Contacting your internet provider to ask for a retention deal, comparison-shopping home insurance at renewal, and switching energy tariffs if available in your market are all one-time actions with multi-month payoffs.Transportation

Carpooling twice a week with a colleague or neighbour can reduce fuel costs by 30% to 40% for those commutes. Switching car insurance providers at renewal — which takes 30 minutes of comparison shopping — typically saves $100 to $400 per year. Using public transport for some journeys, or consolidating errands into single trips, reduces both fuel and vehicle wear costs. The transportation category is often the second-largest household expense after housing, and it is frequently overlooked in savings plans.Step 5 — Build Weekly No-Spend Habits

A no-spend day is a day when you make no discretionary purchases — no coffee, no takeaway, no impulse online orders, no non-essential shopping. A no-spend week is seven consecutive days with the same commitment. These structured pauses in discretionary spending serve two purposes: they produce direct savings, and they reveal which spending is habitual rather than genuinely desired.The Vocal Media $5,000 account describes using a progress tracker to stay motivated: 'I developed a small progress monitor. Every $500 I saved, I'd colour in a square. It made the goal feel real and satisfying.' Applying the same visual progress approach to no-spend days — tracking them on a calendar or app — creates a game-like motivation that makes the habit more sustainable. Money Bliss's savings guide identifies the 7-day no-spend challenge as a particularly effective entry point for those new to structured saving.

Aim for two to three no-spend days per week throughout the six-month challenge. At an average of $25 to $40 in daily discretionary spending, two no-spend days per week saves $200 to $320 per month — a significant contribution toward the $833 monthly target. The cumulative six-month saving from this habit alone is $1,200 to $1,920.

Step 6 — Add a Side Income Stream

Expense cuts have a ceiling — there is a floor below which you cannot reduce spending without genuine hardship. Income increases have no ceiling. Adding even one modest side income stream shifts the maths of the challenge significantly, particularly for those at lower income levels where the savings gap represents a large share of take-home pay.Six realistic side income options for the 6-month challenge — earning $100–$500/month

- Sell unused items: Every household has items of value sitting unused — electronics, clothing, furniture, sports equipment, instruments. Selling through eBay, Facebook Marketplace, or Depop typically generates $200 to $600 in the first month of a clearout, with no time commitment beyond photographing and listing. The Vocal Media account notes side hustles and one-time sales generated an additional $300 per month on average during the challenge.

- Freelance your existing skills: If you have any professional skill — writing, design, spreadsheets, social media, translation, photography, coding — there is demand for it on Fiverr, Upwork, or through direct client acquisition. Even two or three small projects per month at $50 to $100 each adds $100 to $300 per month. The key is to start with what you already know, not to learn something new.

- Food delivery or ride-sharing: Platforms like DoorDash, Uber Eats, Deliveroo, or Uber operate in most cities and allow flexible hours around existing work commitments. Two evenings or one weekend day per week typically generates $100 to $200 per week in additional income, with control over hours.

- Tutoring: If you have expertise in any school or university subject, tutoring in your area or online generates $20 to $50 per hour in most markets. One student for two hours per week is $160 to $400 per month of additional income. Advertising on local Facebook groups, Nextdoor, or tutoring platforms takes less than an hour to set up.

- Cashback and rewards optimisation: Using a cashback credit card (paid in full every month) for all regular spending — groceries, petrol, utilities — and redirecting the cashback directly to the savings account generates passive additional income of $20 to $80 per month depending on spending volume. The Vocal Media account notes: 'I strategically utilised cashback apps and credit card rewards. It wasn't huge money, but every bit helped.'

- Rent what you own: A spare room on Airbnb (even just for occasional weekends), a car via platforms like Turo, a driveway or storage space, or tools and equipment can generate passive income from assets already owned. Even one Airbnb weekend per month at $80 to $120 is $480 to $720 over six months — a meaningful contribution to the goal.

Step 7 — Use Windfalls Strategically

A windfall is any money that arrives outside your regular income — a tax refund, a work bonus, a birthday gift in cash, a side income payment that exceeds expectation, proceeds from selling items, or a rebate. During a six-month savings challenge, every windfall should be directed to the savings account before it is spent.The windfall rule is simple: when unexpected money arrives, the first question is not 'what shall I buy?' but 'how much of this can go straight to my $5,000 goal?' A $500 tax refund applied in month two means month two requires only $333 in regular monthly saving rather than $833 — relieving pressure and accelerating the timeline. Fidelity's March 2026 guidance specifically identifies tax refunds as one of the most impactful windfall opportunities: checking your tax withholding (W-4) and ensuring you are capturing all tax credits you are eligible for can produce a meaningful refund that, applied to a savings goal, is the equivalent of several months of disciplined monthly saving in a single deposit.

The psychological principle behind the windfall rule is pre-commitment. By establishing the rule before any windfall arrives — 'any unexpected money goes to the savings account first' — you remove the in-the-moment decision about whether to spend or save it. Pre-commitment beats willpower every time.

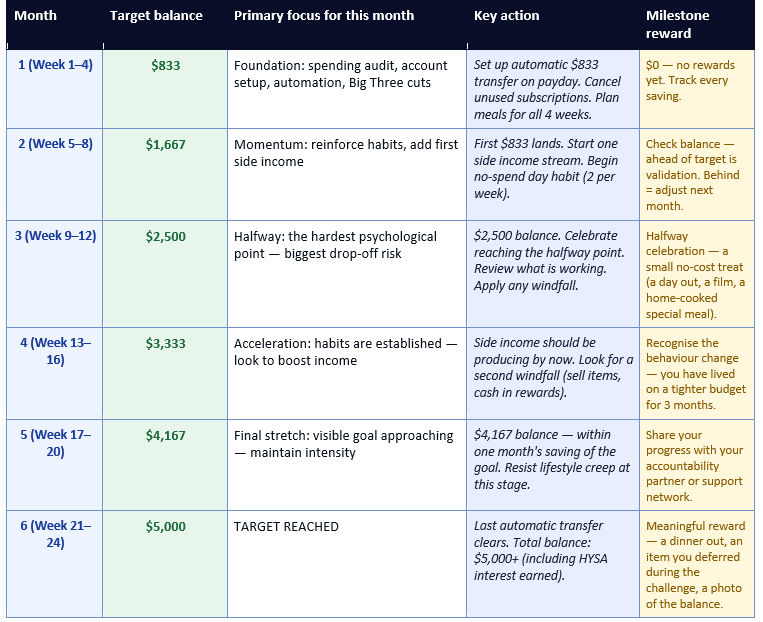

The Month-by-Month Milestone Plan

Staying Accountable: The Two Tools That Actually Work

Motivation is highest at the start of any savings challenge and lowest around months two and three — when the novelty has worn off, the goal still feels distant, and the sacrifices of month one feel fatiguing. Two specific tools significantly improve completion rates.An accountability partner

The Vocal Media $5,000 account identifies this as a turning point: 'I mentioned my goal of saving money to a close friend. Every month, we'd check in. Having someone to hold me accountable made me think twice about impulse purchases.' An accountability partner does not need to be doing the same challenge. They simply need to know your goal, be willing to ask about it once a month, and give honest encouragement rather than empty validation. The knowledge that someone else is aware of your commitment changes the psychological calculus of impulsive spending.A visual progress tracker

The same Vocal Media account describes a physical progress tracker — colouring in a square every $500 saved. Money Bliss's savings guide recommends similar visual goal-tracking: 'Saving money can feel slow, so it helps to celebrate small wins.' The tracker converts an abstract number into a visible, satisfying record of progress. Print a simple six-bar chart with $833 milestones, pin it somewhere you see daily (bathroom mirror, laptop screen, fridge), and mark each milestone as it is reached. The act of marking progress is a small but genuinely effective motivational reinforcement.What to Do When You Have a Bad Month

Every six-month savings challenge will have at least one difficult month — an unexpected bill, a social event that costs more than planned, a slow month for side income, or simply a week where discipline failed. The challenge is not destroyed by a bad month. It is destroyed by quitting after a bad month.The principle from SmartMoneyTrek and InCharge's budgeting guidance applies directly here: a budget that requires revision is not a failed budget. It is a living plan that responds to reality. If month three produces only $500 rather than $833, the response is not abandonment — it is recalibration. Add the $333 shortfall to month four's target. Identify what caused the shortfall (a specific unexpected expense? a discipline failure in a specific category?) and address it before month four. A bad month slightly extends the timeline. Quitting ends it entirely.

The easiest tactical response to a shortfall month is to increase the following month's side income target. If selling $200 of items in month three was the plan but only $100 was achieved, listing $300 worth of items for month four recovers the difference. The side income stream is the most flexible component of the plan — it can be increased or decreased depending on what the month requires.

CONCLUSION

Saving $5,000 in six months is $27.78 per day. Stated as a daily number, it is clearly not a mystery of finance or a privilege of high incomes. It is a decision, an automatic transfer, and a series of weekly habits that compound into a meaningful amount in less time than most people expect. The steps in this guide — spending audit, dedicated HYSA account, automated transfer, Big Three expense cuts, no-spend days, side income, windfall rule, accountability partner, visual tracker — are not individually complex. What makes them powerful is applying them simultaneously, consistently, for six months.The person who reaches $5,000 in six months has not just saved $5,000. They have built a set of financial habits — automation, intentional spending, side income awareness, progress tracking, accountability — that are now available to every subsequent financial goal. The emergency fund becomes the house deposit. The house deposit becomes the investment account. The six-month challenge is the beginning of a relationship with money that compounds long beyond the target date.

Frequently Asked Questions

Is saving $5,000 in 6 months realistic on an average income?

Yes, for most people earning above $2,200 per month take-home, though the difficulty varies significantly with income level. The table in Step 1 of this guide breaks down the challenge by income bracket. At $2,200 to $3,500 per month, it typically requires a combination of Big Three expense cuts ($400 to $500 per month) and one modest side income stream ($200 to $300 per month). At $3,500 to $5,000 per month, it is achievable primarily through a spending audit and automation. The most common reason people on average incomes do not reach the goal is not that the money is unavailable — it is that it is not directed to savings before being spent. The automated transfer in Step 3 is the single most important action to change this.What should I do with $5,000 once I have saved it?

The answer depends on what the savings goal was. If it was an emergency fund: your money belongs in the high-yield savings account you already opened, earning interest and available for genuine emergencies. If it was a specific purchase or goal: spend it for the purpose it was saved for, guilt-free — you earned it through six months of deliberate effort. If you are now motivated to continue: set the next goal immediately and repeat the process. The habits you have built — automated savings, spending awareness, side income — are now established and can be pointed at any subsequent financial goal. Fidelity's guidance recommends that once a $5,000 emergency fund is established, the next step is ensuring you are capturing your employer's pension or 401(k) match (a guaranteed 50% to 100% return) before any other savings or investment goal.What is the best savings account for a $5,000 savings challenge?

In the US, the best easy-access high-yield savings accounts in May 2026 pay up to 5.00% APY (Varo Money) and 4.50% APY (SoFi with direct deposit). These accounts are FDIC-insured, have no monthly fees, and allow instant access if needed. The Hustle Scientist's January 2026 account specifically identifies the HYSA as 'the main factor in my success,' noting that 'my money actually increased while it was there due to interest rates in 2026.' In the UK, the best easy-access rates are up to 4.84% AER (Chip) and 4.68% AER (Plum Cash ISA). For a six-month savings challenge, easy-access is more important than maximum rate — you need the flexibility to add to it monthly — so prioritise a no-fee, high-rate easy-access account over a fixed-term product.How do I stay motivated past month 2 when the novelty wears off?

The two tools identified consistently in first-person savings accounts are an accountability partner and a visual progress tracker. Vocal Media's $5,000 account documents both: a monthly check-in with a trusted friend ('having someone to hold me accountable made me think twice about impulse purchases') and a physical progress chart ('every $500 I saved, I'd colour in a square — it made the goal feel real and satisfying'). Additionally, the halfway milestone at month three — $2,500 — should be acknowledged with a specific, no-cost celebration. The goal-visibility principle is also important: keeping a written statement of why you are saving (sticky note on laptop, phone lock screen wallpaper) maintains the emotional connection to the goal during the weeks when motivation is low.How do I handle an unexpected expense during the six-month challenge?

Unexpected expenses are the most common reason savings challenges fail — not because the expense is unmanageable, but because it leads to abandonment of the plan rather than adjustment. The correct response to an unexpected expense during the challenge is to treat it as a month-specific shortfall, not a plan failure. If an unexpected $400 car repair arises in month two: pay it, acknowledge that month two's savings will be short, and add $100 to each of the next four months to recover the shortfall. Do not withdraw from the savings account unless the emergency fund specifically exists for this purpose — the separation principle protects the savings balance. The side income stream in Step 6 is specifically designed to be flexible: it can be temporarily boosted (more items sold, more side work taken on) in recovery months to compensate for shortfall months.References

Fidelity — How to Save $5,000 This Year: Practical Strategies and Calculator (March 2026) https://www.fidelity.com/learning-center/personal-finance/how-to-save-5000Medium / The Hustle Scientist — How I Saved $5,000 in 6 Months Without Giving Up Coffee (January 2026) https://medium.com/@maqsoodfareed41/how-i-saved-5-000-in-6-months-without-giving-up-coffee-3adde4e2ffda

Vocal Media — How I Saved $5,000 in 6 Months: A Real-Life Guide to Reaching Your Savings Goal https://vocal.media/education/how-i-saved-5-000-in-6-months

Money Bliss — Smart Tips to Reach $5,000 in Savings in 6 Months (July 2025) https://moneybliss.org/tips-to-save-5000-in-6-months/

Stash — How to Save $5,000 in 6 Months: Actionable Strategies https://www.stash.com/learn/how-to-save-5000-in-6-months/

Bankrate — Save Money Calculator: How Much to Save Each Month https://www.bankrate.com/banking/savings/save-money-calculator/

DollarWiseLiving — How to Save $5,000 in Just 6 Months: A Step-by-Step Guide (February 2025) https://dollarwiseliving.wordpress.com/2025/02/25/how-to-save-5000-in-just-6-months-a-step-by-step-guide/

SmartMoneyTrek — How to Budget on a Low Income: 10 Practical Strategies (March 2026) https://smartmoneytrek.com/how-to-budget-on-a-low-income

Makeheadway — How to Save Money Fast on a Low Income (2025) https://makeheadway.com/blog/how-to-save-money-fast-on-low-income/

0 Comments Comments