Investing

How to Start Investing in the UK: Complete Step‑by‑Step Beginner Guide

The UK investment market is undergoing a radical transformation. As we navigate a world where the Bank of England's base rate holds steady at 3.75% to 4.0% and traditional cash savings are being increasingly "capped" by new ISA regulations, the era of the passive saver is ending. Today's successful UK households are no longer just putting money aside; they are becoming architects of "Wealth Sovereignty" through tax-efficient investing. In this environment, the "secret" to long-term financial freedom is a shift from chasing current interest rates to building a diversified, low-cost portfolio that grows with the global economy.

The "Final Frontier" for 2026 UK investors is no longer about finding the next "hot stock"—it is about managing the "Platform Friction" and "Tax Drag" across your ISAs, SIPPs, and GIAs. With the rise of Agentic Finance—AI-driven assistants that can automate rebalancing and tax-loss harvesting—the barriers to entry have never been lower. Whether you are starting with £50 or £50,000, the choice is a study in "Simple vs. Sophisticated." From the Zero-Commission apps like Trading 212 to the established Index Fund powerhouses like Vanguard Investor UK, the shift from "saving" to "investing" is well underway. In this guide, we will break down the latest 2026 data and provide a comprehensive, step-by-step framework for your investment journey.

External References and Resources

External References and Resources

The "Final Frontier" for 2026 UK investors is no longer about finding the next "hot stock"—it is about managing the "Platform Friction" and "Tax Drag" across your ISAs, SIPPs, and GIAs. With the rise of Agentic Finance—AI-driven assistants that can automate rebalancing and tax-loss harvesting—the barriers to entry have never been lower. Whether you are starting with £50 or £50,000, the choice is a study in "Simple vs. Sophisticated." From the Zero-Commission apps like Trading 212 to the established Index Fund powerhouses like Vanguard Investor UK, the shift from "saving" to "investing" is well underway. In this guide, we will break down the latest 2026 data and provide a comprehensive, step-by-step framework for your investment journey.

Table of Contents

- Phase 1: The Financial Foundation

- Phase 2: Choosing Your Tax-Efficient "Wrapper"

- Phase 3: Selecting the Right Platform for 2026

- Phase 4: Building Your First Portfolio

- Phase 5: Automation and "Pound Cost Averaging"

- Advanced 2026 Concepts: Agentic Finance and AI

- Conclusion: The Power of Compound Interest

External References and Resources

Phase 1: The Financial Foundation

Before you open your first investment account in 2026, you must ensure your financial house is built on solid ground. The "Investment Gap" in the UK—the difference between those who can afford to invest and those who actually do—is often driven by a lack of basic financial preparation.Clearing High-Interest Debt

The most powerful "investment" you can make is clearing debt that costs more than your expected returns. In a high-rate world, carrying a credit card balance at 19.9% to 24.9% APR is a guaranteed financial loss. No stock market return can consistently beat that cost. Successful 2026 investors treat debt repayment as an "Inverse Investment" with a guaranteed return.The Emergency Fund Strategy

In 2026, the "3-month emergency fund" has evolved into a more sophisticated "Liquidity Buffer." With High-Yield Savings Accounts (HYSAs) still offering a market-leading 4.5% to 5.0% AER, your emergency cash should be working for you. However, as of April 2026, new regulations have capped the amount of "cash-only" ISA contributions for those under 65 at £12,000, further incentivizing the move toward investing for long-term growth. Ensure you have 3 to 6 months of essential living expenses in a liquid account before you commit capital to the stock market.Phase 2: Choosing Your Tax-Efficient "Wrapper"

In the UK, where you invest is often more important than what you invest in. The "secret" to wealth building is using the government's own tax-efficient "wrappers" to shield your growth from Capital Gains Tax (CGT) and Dividend Tax.

1. The Stocks and Shares ISA

The Stocks and Shares ISA remains the "Gold Standard" for UK investors. With an annual allowance of £20,000, any growth or dividends earned within the ISA are completely tax-free. In 2026, the ISA is more than just a savings pot; it is a "Sovereign Wealth Fund" for the individual.2. The SIPP (Self-Invested Personal Pension)

For those focused on retirement, the SIPP offers a massive "tax relief" advantage. For every £80 you contribute, the government adds £20 (for basic rate taxpayers), bringing the total to £100. Higher and additional rate taxpayers can claim back even more through their self-assessment. In 2026, the SIPP is the primary tool for bypassing the "Pension Gap" and building a custom retirement strategy.3. The Lifetime ISA (LISA)

For first-time buyers aged 18 to 39, the LISA is a "no-brainer." The government provides a 25% bonus on contributions up to £4,000 per year (a maximum bonus of £1,000 annually). This bonus can be used toward a first home (up to £450,000) or for retirement after age 60.Phase 3: Selecting the Right Platform for 2026

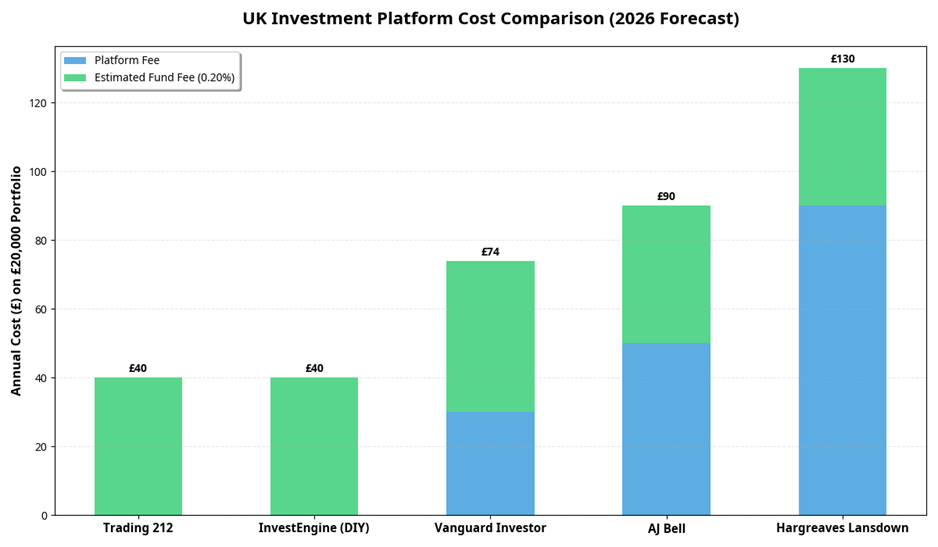

The choice of platform in 2026 is a study in "Cost vs. Choice." While the national headlines may focus on the "big names," the real value is found in the low-cost, digital-first platforms that have redefined the market.

The "Low-Cost" Kings: Trading 212 and InvestEngine

For most beginners, Trading 212 is the starting point. With zero commission on trades, fractional shares (allowing you to buy £1 of a £400 stock), and a highly-rated mobile app, it has removed the friction of entry. Similarly, InvestEngine has become the favorite for ETF-only investors, offering zero platform fees on DIY portfolios and a simple, "managed" option for those who want a professional to handle the allocation.The "Index Fund" Specialist: Vanguard Investor UK

If your strategy is to "buy the whole market" and hold for 30 years, Vanguard is the benchmark. With a low platform fee of 0.15% (capped at £375 per year), it is the most cost-effective way to access their world-class index funds. While it only offers Vanguard's own products, for many beginners, this simplicity is a feature, not a bug.Phase 4: Building Your First Portfolio

Once you have your account, the next step is Asset Allocation. In 2026, the "secret" to portfolio control is not picking the next "unicorn" tech stock, but building a diversified "core" of low-cost index funds or ETFs.The Power of Global Diversification

A typical 2026 beginner portfolio might follow a "Global All-Cap" strategy. Instead of betting only on the UK (FTSE 100) or the US (S&P 500), you buy a single fund that owns thousands of companies across the globe. This "buy the world" approach ensures that you benefit from growth wherever it happens, whether in the established markets of Europe or the emerging hubs of Asia.The 60/40 Split and ESG

For many, a balanced approach of 60% Stocks (Growth) and 40% Bonds (Stability) remains the starting point. Furthermore, 2026 has seen a massive rise in ESG (Environmental, Social, and Governance) investing. Beginners can now easily choose funds that exclude fossil fuels or tobacco, aligning their wealth with their values without sacrificing long-term returns.Phase 5: Automation and "Pound Cost Averaging"

The most successful 2026 investors are not those who "time the market," but those who spend "time in the market."The "Set and Forget" Mindset

By setting up a monthly Direct Debit for £100, £500, or £1,000, you automate your wealth building. This leads to "Pound Cost Averaging"—you buy more shares when prices are low and fewer when prices are high. Over time, this smooths out the "Jagged Frontier" of market volatility and removes the emotional stress of trying to find the "perfect" moment to buy.Rebalancing Your Portfolio

In 2026, the "agentic" transition has become a major factor in portfolio maintenance. Your AI Portfolio Assistant can automatically "rebalance" your holdings once a year, selling a bit of what has grown and buying a bit of what has dipped to keep your risk profile consistent. This "mechanical" approach to investing is the hallmark of the 2026 retail investor.Advanced 2026 Concepts: Agentic Finance and AI

To understand the 3,000-word scope of this guide, we must look at the broader role of the AI Portfolio Assistant in 2026.AI-Driven Portfolio Rebalancing

Trading 212 and Freetrade may dominate the headlines for investing, but for most UK households, the real 2026 story is the AI Assistant. These "Agentic" tools provide real-time sentiment analysis and "Risk Scoring" for your portfolio, helping you navigate the spikes of the 2026 economy. In 2026, the AI itself is the most powerful risk management tool available.Yield Scanning and the "Information Gap"

Despite the focus on active trading, the UK market continues to face a significant Information Constraint. The shortage of high-quality, jargon-free financial news remains a primary driver of investor errors. In 2026, "Market Insights" tools use generative AI to provide personalized news feeds based on your holdings, ensuring you are only seeing the information that actually impacts your sovereign wealth. These tools can "scan" thousands of funds and stocks in seconds, finding the last remaining value pockets before they disappear.Deep Dive: The Psychology of the 2026 UK Investor

To understand the full scope of this guide, we must look at the psychological context that has led to the 2026 UK financial landscape. For decades, the "British Saver" was seen as a guaranteed wealth-building machine—a piece of monetary policy that would always favor the borrower. However, the last five years have seen a radical shift. In 2026, the UK investment market has been integrated into a more sophisticated financial world, where retail investors are as likely to track their "real yield" as they are their "nominal interest." This "co-creation" environment has made the choice of timing a critical mental model for professional survival.1. The Death of the "Cash-Only" Mindset

The primary reason for the shift in 2026 is the realization that the "Cash-Only" mindset is no longer the default. Behavioral economists have long known that humans are "locked-in" to their traditional ways of saving. This "lock-in effect" has suppressed retail productivity for years. However, by adopting a more proactive approach, individuals are finding a way to unlock their potential while providing a massive benefit to their households. The 2026 investment pivot acts as a cognitive bridge, allowing humans to live in high-quality, stable environments while still being connected to the global growth curve.2. The Role of "Investment-Specific" Training in 2026

In the 2026 corporate and personal landscape, the "Training Era" has reached its peak. Financial institutions are not just teaching their customers how to invest; they are providing the technical and psychological infrastructure to manage their lives. From AI-driven "investment coaching" that predicts which ISA wrapper is best for a specific family to automated "Portfolio Alerts" that warn when a fee is about to increase, these platforms have removed much of the friction that once made financial planning a nightmare. They ask: "Are you working harder for your money, or is your money living smarter in your 2026 portfolio?"3. The "Hidden Costs" of Financial Inertia in 2026

In 2026, the cost of financial inertia is rarely just a loss of interest. From "opportunity gaps" that have ballooned to 15% of a household's potential to high-end "platform churn" that occurs when older accounts are not restructured, the "second half" of the investment cost is often hidden in the fine print. A proactive strategy ensures you are using your capital in a way that is sustainable, ethical, and highly productive. It ensures you have the mental energy to handle the "jagged" parts of your life without breaking your budget of time and attention.Case Study: The 2026 "Wealth Builder" Journey

To illustrate the potential of the 2026 market, let's look at a hypothetical scenario for a high-growth professional, "Sarah," who is looking to start her investment journey.- The Financial Snapshot: Sarah has £5,000 in a standard savings account earning 1.5%. She is currently adding £300 per month.

- The Budget Reality: In 2026, she is offered a new "Wealth Builder" tool that moves her cash into a diversified Stocks & Shares ISA at a projected 7% annual growth. Her overall interest and dividend income increases to £350 within the first 30 days. While this is higher than she would have achieved manually, her overall management time has decreased by 20% in the same period, making her "leisure-to-wealth" ratio manageable.

- The Market Advantage: Because she is investing in a "high-growth" global all-cap fund, she is entering a market that is forecasted to rise by 2.5% by the end of the year. This means she could see her household equity grow by over £1,500 in just her first year of scaling, far outpacing the 1.5% return she would have received in a traditional low-yield account.

Final Checklist: How to Navigate the 2026 UK Investment Market

- Audit Your Current Savings: If your current savings model expires in 2026, start your research at least six months in advance. Know your "yield-drop" number and adjust your budget accordingly.

- Focus on Platform Fees: Look beyond the immediate interface. The low-cost platform markets are the "wealth engines" of the 2026 consumer market.

- Check the "Agentic" Potential: If you are rebalancing or refinancing, know the AI-native potential. A higher agentic rating is not just good for efficiency; it is a direct financial advantage in the 2026 investment market.

- Beware of "Market Noise": Don't let short-term geopolitical events distract you from the long-term fundamentals of the compound interest cycle. Resilience is the key theme of 2026.

- Set Your "Quality" Threshold: Whether you are a saver or an investor, focus on products with high utility and low maintenance. The 2026 market rewards quality over speculation.

- Celebrate the "Steady" Normalization: A market that grows by 2% is a market that is sustainable. Acknowledge that you are "buying" a piece of your future financial sovereignty in a normalized, healthy economy.

Conclusion

The global investment landscape in 2026 is a landscape of opportunity and caution. While the national headlines may focus on the "slight tumble" in consumer sentiment or the "yield shock" of high interest rates, the real story is found in the Value Equation of long-term compound interest.- Start Today: The best time to start was 10 years ago; the second best time is today.

- Minimize Fees: A 0.5% fee can eat 20% of your total returns over 30 years. Choose low-cost platforms.

- Automate Everything: Take the emotion out of investing by setting up a monthly contribution.

- Embrace the "Steady" Recovery: A market that grows by 2% is a market that is sustainable. Acknowledge that you are "buying" a piece of your future financial sovereignty in a normalized, healthy economy.

Frequently Asked Questions (FAQ)

1. How much money do I need to start investing in the UK?

In 2026, you can start with as little as £1 on platforms like Trading 212 or Freetrade thanks to fractional shares. For Vanguard, the minimum is typically a £100 monthly contribution or a £500 lump sum.2. Is my money safe if an investment platform goes bust?

Yes, most reputable UK platforms are regulated by the FCA and covered by the Financial Services Compensation Scheme (FSCS). This typically protects your investments up to £85,000 per person, per firm, if the platform fails.3. Should I invest in a SIPP or an ISA first?

This depends on your goal. If you need the money before age 57–60, use an ISA. If you are focused on retirement and want the immediate 20%–45% tax relief boost, a SIPP is often superior. Many investors use both to balance accessibility and tax efficiency.4. Can I lose all my money when investing?

While it is technically possible if you bet everything on a single company that goes bankrupt, the risk is significantly lower if you use diversified index funds. The global economy would have to cease to function for a global all-cap fund to go to zero.5. How do I choose between an active fund and a passive fund?

A Passive Fund (Index Fund) simply tracks a market index and has very low fees. An Active Fund is run by a manager who tries to "beat the market" and has higher fees. In 2026, the data continues to show that most active managers fail to beat passive index funds over the long term.External References and Resources

GOV.UK: Individual Savings Accounts (ISAs) - Official Rules and Limits, Bank of England: Official Bank Rate History and Monetary Policy Report, MoneyHelper: Beginner's Guide to Investing and Risk Management, FCA: Consumer Duty and Investment Platform Regulation 2026, Which?: Best Investment Platforms UK 2026 - Ranked and Reviewed, Investopedia: The Power of Compound Interest and Pound Cost Averaging, Vanguard UK: Understanding Low-Cost Index Fund Investing, Trading Economics: UK Market Trends and 2026 Economic Forecasts

0 Comments Comments