Retirement

The High-Stakes Effort to Repair American Retirement

Table of Contents

What the 2026 Trustees Report Actually FoundThe Bicentennial Echo: A Strikingly Similar Crisis in 1976

Why This Reckoning Carries Even Higher Stakes

The High-Stakes Policy Options Now on the Table

What This Means for Your Own Retirement Planning

Conclusion

Frequently Asked Questions (FAQ)

External References & Further Reading

As the United States marks its 250th anniversary in 2026, major news organizations have launched ambitious retrospective series examining the institutions that built what is still, by most measures, the world's largest economy. The Wall Street Journal's year-long project, titled "USA250: The Story of the World's Greatest Economy," is exploring the triumphs, trials, and innovations that shaped American economic life across two and a half centuries. Few stories fit that frame more urgently than the one unfolding right now inside the Social Security Administration.

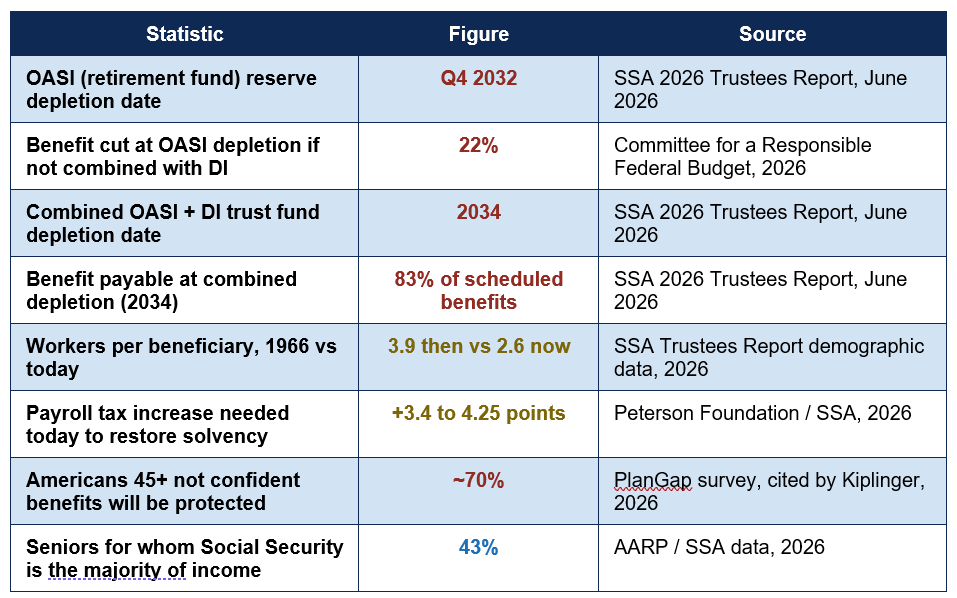

In June 2026, the Social Security Board of Trustees released its annual report, and the news was sobering: the program's primary retirement trust fund is now projected to deplete its reserves in the fourth quarter of 2032 — one quarter sooner than projected just a year earlier. If Congress allows the retirement and disability trust funds to be combined, as is standard practice, the depletion date extends to 2034, at which point the system would only be able to pay 83% of scheduled benefits using ongoing payroll tax revenue alone. Roughly 71 million Americans currently receive Social Security benefits, and for 43% of seniors, those payments represent the majority of their income.

This is not a new crisis manufactured for an anniversary news cycle — it is a structural problem more than five decades in the making, one with an eerie historical parallel to the very Bicentennial era the 250th anniversary now echoes. This piece examines exactly what the 2026 Trustees Report found, draws out the striking parallel to a nearly identical crisis the system faced fifty years ago, and lays out the high-stakes policy options now on the table as America's retirement system approaches what may be its most consequential reckoning in over forty years.

What the 2026 Trustees Report Actually Found

Released on June 9, 2026, the Social Security Board of Trustees' annual report is the authoritative, legally mandated assessment of the program's financial health, prepared jointly by the Treasury Secretary, Labor Secretary, Health and Human Services Secretary, and the Social Security Commissioner. The key findings paint a picture of a system whose finances have deteriorated meaningfully even compared to the already-concerning projections of recent years:

This year's shortfall vs. 2010 projections: 2.3 times larger — the Committee for a Responsible Federal Budget found this year's projected payroll shortfall of 4.42% is the largest in nearly half a century, and more than double the shortfall projected back in 2010 — illustrating how the problem has compounded through years of congressional inaction.

Why the date moved up: the Trustees attributed much of the year-over-year worsening to revised demographic assumptions, particularly a downward revision to the projected long-term fertility rate, from 1.9 to 1.75 children per woman. Fewer future workers paying into the system, combined with a growing population of retirees drawing from it, is the structural engine behind nearly every version of this crisis the program has faced since the 1970s.

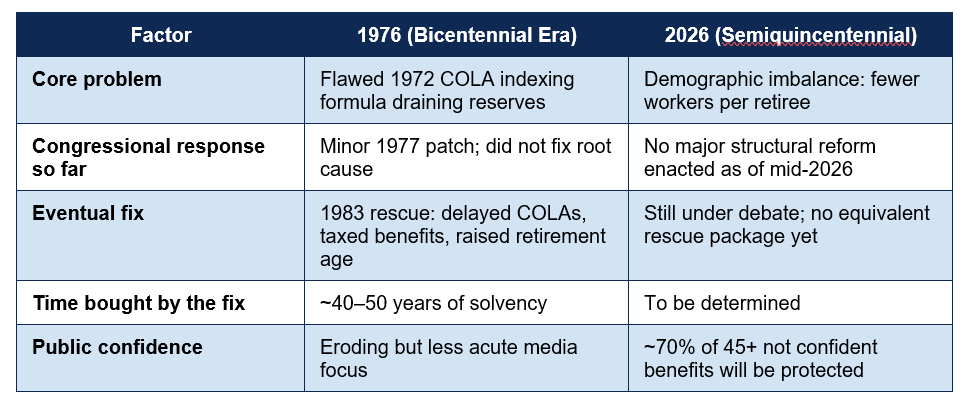

The Bicentennial Echo: A Strikingly Similar Crisis in 1976

One of the more remarkable threads running through this year's retrospective economic coverage, highlighted specifically by Kiplinger's contribution to the America at 250 series, is just how closely today's Social Security predicament echoes the situation the program faced exactly fifty years earlier, during the nation's Bicentennial celebrations in 1976.In 1976, a flawed benefit-indexing formula enacted in 1972 — designed to protect retirees from inflation through cost-of-living adjustments — was inadvertently over-indexing benefits, quietly draining the trust funds faster than policymakers had anticipated. Rather than confronting the structural problem directly, Congress passed only a minor technical patch in 1977 that left the deeper imbalance unresolved. By 1982, the Trustees were warning that the system was mere months away from outright insolvency.

The resolution came in 1983, through a sweeping, bipartisan legislative rescue package: cost-of-living adjustments were delayed, a portion of benefits became subject to federal income tax for the first time, and the retirement age was gradually raised. Crucially, that package was explicitly designed by its architects to buy the system 40 to 50 years of breathing room — a runway that, by the program's own arithmetic, is now expiring almost exactly on schedule, just as the nation reaches its 250th year.

Why This Reckoning Carries Even Higher Stakes

While the structural pattern echoes 1976, several factors make the current moment arguably more urgent than its Bicentennial-era predecessor. The worker-to-beneficiary ratio — the number of active workers supporting each person drawing benefits — has fallen from 3.9 workers per beneficiary in 1966 to just 2.6 today, and the Trustees project it will fall further still, to 2.2, by 2046. This is the single most important demographic fact underlying the entire crisis: a pay-as-you-go system designed when several workers supported each retiree is straining under a ratio that has nearly halved.The cost of delay is also compounding in a measurable, well-documented way. The Committee for a Responsible Federal Budget calculates that restoring full long-term solvency today would require an immediate, permanent payroll tax increase of roughly 3.4 to 4.25 percentage points, or an equivalent reduction in benefits of around 25%. Waiting until the trust fund actually depletes in 2034 would require a larger 4.9 percentage point tax increase, or a steeper 29% benefit cut — meaning every year of further congressional inaction makes the eventual fix measurably more painful, a dynamic the Trustees themselves have flagged explicitly in their official recommendations.

- The human stakes in concrete terms: the Committee for a Responsible Federal Budget estimates that a typical couple retiring in 2033, facing the unmitigated benefit cut at that time, would see an $18,400 annual reduction in their combined Social Security income — a figure that makes the abstract policy debate over trust fund mathematics into a very real household budgeting problem for tens of millions of future retirees.

The High-Stakes Policy Options Now on the Table

Much as the 1983 rescue combined several distinct levers rather than relying on a single fix, the current policy conversation around restoring Social Security's solvency centers on a small number of well-understood mechanisms, each carrying distinct trade-offs:- Raising the payroll tax rate: The current combined Social Security payroll tax rate is 12.4% (6.2% paid by employees, 6.2% by employers). The Social Security Administration's own modeling suggests a 4.25 percentage point increase enacted in 2026 could restore long-term solvency, though this would represent a substantial increase in the tax burden on working Americans and their employers.

- Raising or eliminating the payroll tax wage cap: Earnings above a certain annual threshold (adjusted yearly) are not currently subject to Social Security payroll tax. Raising or eliminating this cap, so that higher earners contribute on a larger share of their income, is among the policy options most frequently discussed as a way to raise revenue without increasing the rate paid by lower and middle-income workers.

- Gradually raising the full retirement age: Mirroring the approach taken in 1983, a further gradual increase in the age at which full benefits become available is sometimes proposed to reflect increased life expectancy since the program's last major retirement-age adjustment, though this approach is also criticized for disproportionately affecting workers in physically demanding occupations with shorter healthy life expectancies.

- Adjusting the benefit formula or cost-of-living calculation: Various proposals would adjust how initial benefits are calculated or how annual cost-of-living adjustments are determined, generally aiming to slow the growth rate of future benefits, particularly for higher earners, while preserving benefit levels for lower-income retirees who rely most heavily on the program.

- A combination approach, as in 1983: Most nonpartisan analyses, including from the Committee for a Responsible Federal Budget, conclude that no single lever alone is likely to be politically or economically palatable at the scale required, and that the eventual solution — much like the 1983 rescue — will likely combine smaller adjustments to several of these mechanisms simultaneously, phased in gradually to give workers and retirees time to plan.

As of mid-2026, no comprehensive legislative package addressing the core structural shortfall has been enacted, despite the consistent and increasingly urgent warnings issued in successive Trustees Reports over more than a decade. AARP's CEO, in response to this year's report, called the findings "a wake-up call," stating plainly that "Congress needs to act," while explicitly opposing any approach that reduces benefits, raises the retirement age, or moves toward privatization — illustrating the genuine political difficulty of assembling the kind of bipartisan coalition that made the 1983 rescue possible.

What This Means for Your Own Retirement Planning

Regardless of how the policy debate ultimately resolves, individuals planning for their own retirement can take several concrete steps in response to the genuine uncertainty the Trustees Report highlights:- Avoid assuming benefits will be eliminated entirely: Even in the unmitigated scenario where no congressional action occurs, the Trustees project Social Security would still be able to pay 83% of scheduled benefits indefinitely using ongoing payroll tax revenue — a meaningful reduction, but not the complete disappearance of the program that some popular commentary suggests.

- Build retirement plans that are resilient to a benefit reduction scenario: Financial planners increasingly recommend stress-testing retirement projections against a scenario where Social Security benefits are reduced by 15-20%, ensuring that personal savings and other income sources provide a meaningful cushion even under a less favorable outcome.

- Maximize personal retirement savings vehicles regardless of the Social Security outlook: 401(k), IRA, and other tax-advantaged retirement accounts remain entirely within an individual's own control, unaffected by the political outcome of the Social Security solvency debate, making consistent personal contribution one of the most reliable hedges available.

- Stay informed through official sources rather than secondhand commentary: The Social Security Administration publishes its full Trustees Report and a clear summary annually at ssa.gov, providing the most accurate and current information directly, rather than relying on potentially outdated or politically filtered secondary coverage.

Conclusion

As America's 250th anniversary retrospectives — from the Wall Street Journal's USA250 series to similar projects across television, print, and digital media — look back across two and a half centuries of economic triumphs and trials, the story of Social Security's repeated brushes with insolvency stands out as a particularly instructive thread. The program has faced this exact kind of structural reckoning before, almost precisely fifty years ago during the nation's Bicentennial, and it was rescued then through difficult but ultimately bipartisan legislative action that bought the system decades of additional life.The 2026 Trustees Report makes clear that the clock purchased by that 1983 rescue is now running out, with the retirement trust fund's reserves projected to deplete in 2032 and the combined system's reserves following in 2034. The choices facing Congress — some combination of higher payroll taxes, a higher retirement age, an adjusted wage cap, or a modified benefit formula — are not fundamentally different in kind from the choices made in 1983, even if the specific numbers and political environment have changed.

What is different, and what makes this moment genuinely high-stakes rather than simply another recurring headline, is the shrinking runway: every year without action makes the eventual fix measurably more expensive and more painful, both for the federal budget and for the tens of millions of Americans whose retirement security depends on the outcome. As the nation marks 250 years and tells the story of the world's greatest economy, the resolution of this particular chapter — still being written in real time — will shape the retirement security of nearly every American currently working toward that milestone themselves.

Frequently Asked Questions (FAQ)

Is Social Security really going to run out of money completely?

No. Even if Congress takes no action at all, Social Security would not disappear or stop paying benefits entirely. The 2026 Trustees Report projects that after the combined trust funds deplete their reserves in 2034, ongoing payroll tax revenue would still cover approximately 83% of scheduled benefits indefinitely. This represents a meaningful, painful cut for retirees, but not the complete elimination of the program that some discussions of 'Social Security running out' can imply.What's the difference between the OASI trust fund and the combined trust fund dates?

The Old-Age and Survivors Insurance (OASI) trust fund specifically covers retirement and survivor benefits, and is projected to deplete its own reserves in the fourth quarter of 2032. The Disability Insurance (DI) trust fund, which covers disability benefits, remains healthier and is not projected to deplete during the 75-year projection period on its own. If Congress permits reallocation between the two funds, as has been done before, the combined reserves extend the depletion date to 2034. Without that reallocation, OASI alone would face a steeper, earlier cut to retirement benefits specifically.Why does Congress keep delaying action on this well-known problem?

Social Security reform has long been considered one of the most politically difficult issues in American policy, since every available solution — tax increases, benefit reductions, or a higher retirement age — imposes a direct, visible cost on a specific group of voters. As one retirement researcher noted in coverage of the 2026 report, lawmakers have known about the underlying demographic problem for decades but have repeatedly avoided the political cost of addressing it directly, a pattern that mirrors the original delay between the 1976 warning signs and the eventual 1983 rescue package.How does the 2025 tax law (OBBBA) affect Social Security's finances?

The One Big Beautiful Bill Act (OBBBA), enacted in July 2025, made the lower individual income tax rates from the 2017 Tax Cuts and Jobs Act permanent and expanded the standard deduction, including a larger deduction specifically for seniors. According to analysis from the Tax Policy Center and the Peter G. Peterson Foundation, these changes are projected to reduce Social Security trust fund revenues by roughly $170 billion between 2025 and 2034, contributing to the acceleration of the OASI depletion date from early 2033 in the prior year's report to late 2032 in the 2026 report.What should I do personally to prepare for possible Social Security benefit changes?

Financial planners generally recommend continuing to maximize personal retirement savings through 401(k)s, IRAs, and other tax-advantaged accounts regardless of the Social Security policy outcome, since these remain fully within your own control. It can also be useful to model your retirement plan under a conservative scenario assuming a 15-20% reduction in projected Social Security benefits, to ensure your broader plan remains resilient even if Congress does not act before the relevant depletion dates. Staying informed through the Social Security Administration's own published Trustees Report summaries at ssa.gov is the most reliable way to track how the policy situation develops over the coming years.External References

The following official and authoritative sources were used in researching this article and are recommended for further reading:1. Social Security Administration — 2026 Trustees Report Summary

https://www.ssa.gov/oact/trsum/

2. Social Security Administration — Official 2026 Trustees Report Press Release

https://www.ssa.gov/news/en/press/releases/2026-06-09.html

3. Committee for a Responsible Federal Budget — Analysis of the 2026 Social Security Trustees' Report

https://www.crfb.org/papers/analysis-2026-social-security-trustees-report

4. Kiplinger — America at 250: 3 Economic Headaches That Haven't Changed Since 1976

https://www.kiplinger.com/retirement/social-security/america-at-250-3-economic-issues-that-remain-since-1976

5. AARP — 2026 Social Security Trust Fund Report Analysis

https://www.aarp.org/social-security/trust-fund-report-2026/

6. PBS NewsHour — Social Security's Retirement Trust Fund Faces Projected Shortfall in 2032

https://www.pbs.org/newshour/politics/social-securitys-retirement-trust-fund-faces-a-projected-funding-shortfall-in-2032-a-year-earlier-than-expected

7. Wall Street Journal — USA250: The Story of the World's Greatest Economy (Series Overview)

https://www.wsj.com/economy

8. RBC Wealth Management — American Economic Milestones: A Look Back at 250 Years of US Financial History

https://www.rbcwealthmanagement.com/en-us/insights/american-economic-milestones-a-look-back-at-250-years-of-us-financial-history

0 Comments Comments