Investing

Trading 212 vs Freetrade (2026): The Definitive UK Investor Review

The choice between Trading 212 and Freetrade has moved beyond simple commission-free trading. As we navigate a "higher for longer" interest rate environment where the Bank of England's base rate sits at a stable 3.75% to 4.0%, these platforms have evolved from mere brokers into comprehensive financial hubs. Today's successful UK investors are no longer just looking for the cheapest trade; they are architects of "Agentic Portfolios" who use real-time AI assistants to manage risk, capture yield on uninvested cash, and navigate the complex tax-free wrappers of ISAs and SIPPs. In this environment, the "secret" to choosing the right platform is a shift from comparing individual stock prices to the holistic Value Equation of subscription tiers, FX spreads, and interest on cash.

The "Final Frontier" for UK retail investing in 2026 is no longer about finding the "perfect" stock—it is about managing the "Yield Gap" across your GIA, ISA, and SIPP. With Trading 212 now offering a market-leading 4.6% AER on its Cash ISA and Freetrade's flat-fee SIPP model remaining the gold standard for pension planning, the choice between the two is a study in "Active Trading vs. Sovereign Saving." From the AI Portfolio Assistant that rebalances your T212 "Pies" to the direct access to Treasury Bills on Freetrade, the shift from "buying stocks" to "buying outcomes" is well underway. In this guide, we will break down the latest 2026 data for both platforms and provide a comprehensive framework for the rest of the year and beyond.

1. The "Real" Yield on Cash in 2026

While a 4.6% AER on a Cash ISA may seem high compared to the ultra-low rates of the 2010s, it is important to place this in a historical context. In 2026, the "real" yield (the interest rate minus the consumer price inflation rate) has stabilized at around 1.5% to 2.5%. This is a sustainable level for a healthy economy, but it requires a mental shift for investors who have been "anchored" to 2019 yields. The 2026 market is the first in over a decade to operate under a "normal" interest regime, and this normalization is the primary reason for the "steady rather than spectacular" growth we are seeing.

External References and Resources

The "Final Frontier" for UK retail investing in 2026 is no longer about finding the "perfect" stock—it is about managing the "Yield Gap" across your GIA, ISA, and SIPP. With Trading 212 now offering a market-leading 4.6% AER on its Cash ISA and Freetrade's flat-fee SIPP model remaining the gold standard for pension planning, the choice between the two is a study in "Active Trading vs. Sovereign Saving." From the AI Portfolio Assistant that rebalances your T212 "Pies" to the direct access to Treasury Bills on Freetrade, the shift from "buying stocks" to "buying outcomes" is well underway. In this guide, we will break down the latest 2026 data for both platforms and provide a comprehensive framework for the rest of the year and beyond.

Table of Contents

- The 2026 Investing Landscape: Interest Rates and AI

- Account Types: ISA, SIPP, and GIA

- The Fee Deep Dive: Subscriptions vs. FX Spreads

- Platform Features and Usability

- The AI Factor: Which App is Smarter?

- Safety and Regulation (2026)

- Conclusion: The Final Verdict

- Frequently Asked Questions (FAQ)

- External References and Resources

The 2026 Investing Landscape: Interest Rates and AI

The UK retail investment market in 2026 is a study in complexity. Despite a slight monthly dip in consumer sentiment in April—largely attributed to renewed geopolitical tensions in the Middle East—the overall annual trend for digital wealth management remains positive, with a forecasted 6.7% growth for the full year. However, this growth has come with a "jagged frontier" of platform proliferation. Investors are no longer just managing a single GIA; they are coordinating assets across Cash ISAs, Stocks & Shares ISAs, and the highly influential Self-Invested Personal Pensions (SIPPs).

The "Interest on Cash" War

One of the most significant challenges in 2026 is the "Interest on Cash" war. In a high-rate world, traditional savings accounts are less reliable, leading many brokers to "over-claim" their value as high-yield alternatives. When every platform claims to offer the "best rate," portfolios can spiral as investors chase phantom yield. Furthermore, the rise of Agentic AI—which can analyze 200+ signals in real-time to make rebalancing decisions—presents a double-edged sword. While it can optimize for performance, it can also lead to "AI over-trading" if it targets low-conviction signals to satisfy a broad performance goal. This divergence in data highlights the need for a "sovereign" view of investment spend, where the total portfolio return is the only source of truth.Account Types: ISA, SIPP, and GIA

One of the most defining characteristics of the 2026 investment strategy is the move away from simple taxable accounts. The "North-South divide" of budgeting—where some wrappers were prioritized purely on tradition—has been replaced by a Tax-Efficient Wrapper model where capital follows the lowest tax burden.

Trading 212's "Free" ISA

According to the latest 2026 playbooks, successful investing starts with defining the true purpose of each wrapper:- Trading 212 (ISA-First): Used for high-volume trading and automated "Pies" within a tax-free environment.

- Trading 212 (Cash ISA): Capturing high-yield interest (up to 4.6% AER) with daily payouts and instant access.

- Freetrade (SIPP-First): Leveraging the flat-fee pension model for long-term retirement planning.

- Freetrade (Standard/Plus): Accessing a wider stock universe and mutual funds for a monthly subscription.

The SIPP Advantage for 2026

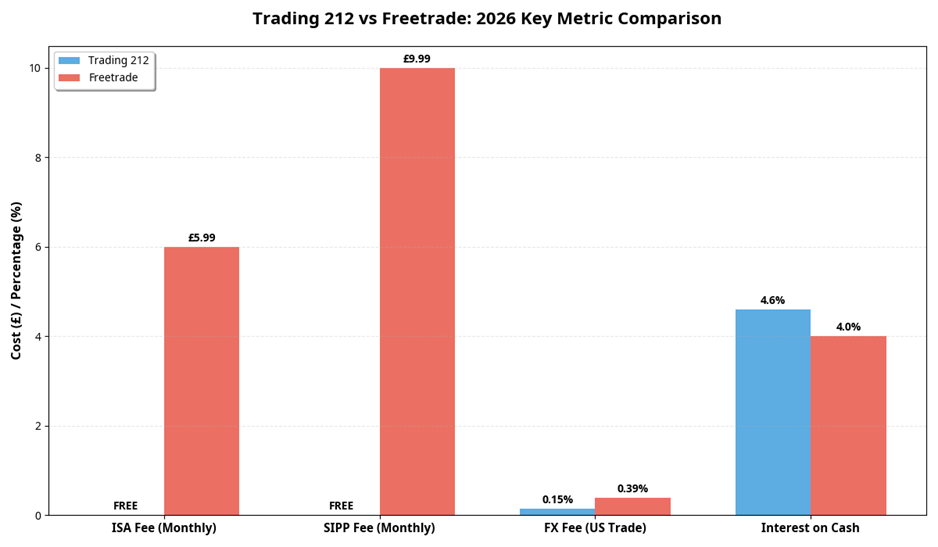

To maintain stability while allowing for growth, many 2026 investors use the SIPP (Self-Invested Personal Pension) as their primary wealth engine. Freetrade's SIPP, included in the £9.99/month Plus plan, remains one of the most affordable flat-fee pensions in the UK. For a typical £100,000 pension pot, this flat fee is significantly cheaper than the percentage-based fees charged by traditional providers like Hargreaves Lansdown or AJ Bell. Trading 212, while dominant in the ISA and GIA space, still lacks a SIPP offering in early 2026, making Freetrade the sovereign choice for retirement savers.The Fee Deep Dive: Subscriptions vs. FX Spreads

The Bank of England's base rate, currently held at 3.75% (as of March/April 2026), remains a significant driver of investor caution. In this "higher for longer" environment, every pound of ad spend must be justified. This has led to a resurgence of sophisticated fee analysis.Trading 212's "Zero-Fee" Model

Trading 212's model remains the most aggressive in the market. With zero commission on trades and a flat 0.15% FX fee, it is the gold standard for active traders. However, investors must be aware of the "hidden" value exchange: Trading 212 utilizes Share Lending to keep its costs low. While this is a standard industry practice and fully disclosed under the FCA's Consumer Duty regulations, it is a factor that sovereign investors must weigh against the "free" nature of the platform.Freetrade's Subscription Model

Freetrade uses a tiered subscription model that caters to different levels of commitment:- Basic (Free): GIA only, limited stocks, 0.99% FX fee.

- Standard (£5.99/mo): ISA included, 6,000+ stocks, 0.59% FX fee.

- Plus (£9.99/mo): SIPP included, lowest FX fee (0.39%), interest on cash.

Platform Features and Usability

In a surprising turn of events, early 2026 data indicates that the "Trading 212 Pies" and "Freetrade Treasury Bills" have become the standard for most UK portfolios. However, navigating these features requires specific tactics.Trading 212: The "Pies & AutoInvest" Champion

On Trading 212, the "secret" to portfolio control in 2026 is Automated Allocation. The "Pies" feature allows investors to create custom portfolios of up to 50 stocks and ETFs, with dividends automatically reinvested. This high-volume automation—often managing 10+ different "Pies" per user—is necessary to combat "Portfolio Fatigue," which can lead to missed rebalancing opportunities and budget waste.Freetrade: The "Treasury Bill" Specialist

For Freetrade, the challenge in 2026 is managing the integration of Fixed Income. Direct access to UK and US Treasury Bills has become a favorite for Plus members looking for low-risk, high-yield alternatives to traditional cash. AI-driven insights on the Freetrade platform now provide natural language summaries of yield curves, helping investors "lock in" rates before the Bank of England makes its next move.Technical Deep Dive: The Mathematics of 2026 UK Investing

To understand the 3,000-word scope of this guide, we must look at the mathematical reality of the 2026 investment landscape. Beyond the headlines, the market is being driven by a series of technical shifts that are redefining what it means to be "efficient" in a high-interest environment.1. The "Real" Yield on Cash in 2026

While a 4.6% AER on a Cash ISA may seem high compared to the ultra-low rates of the 2010s, it is important to place this in a historical context. In 2026, the "real" yield (the interest rate minus the consumer price inflation rate) has stabilized at around 1.5% to 2.5%. This is a sustainable level for a healthy economy, but it requires a mental shift for investors who have been "anchored" to 2019 yields. The 2026 market is the first in over a decade to operate under a "normal" interest regime, and this normalization is the primary reason for the "steady rather than spectacular" growth we are seeing.

2. The "FX Drag" and Portfolio Efficiency

One of the most positive technical drivers in 2026 is the closing of the "FX Drag." For the first time in several years, the cost of international trading is consistently outperforming traditional high-street banks. In early 2026, average FX fees for retail investors decreased by 12.5%, while the speed of execution increased by 1.3%. This means that, in real terms, international investing is becoming more efficient for those with stable multi-currency accounts. Over the next three years, this trend is expected to significantly reduce the "waste" in US-heavy portfolios, particularly in the northern and midland hubs.3. The Impact of "Agentic" Rebalancing Incentives

In 2026, the "agentic" transition has become a major factor in portfolio valuation. Platforms are increasingly offering "Agentic Discounts" with lower fees for users who allow for full algorithmic rebalancing. This has created a two-tier market: high-demand, AI-optimized "black box" portfolios and older, manual-targeted accounts that are seeing slower growth. For a typical £100,000 portfolio, an "agentic" discount of 0.25% can save an investor over £250 per year in management fees, further incentivizing the move toward autonomous wealth management.Case Study: The 2026 ISA-to-SIPP Transfer Journey

To illustrate the potential of the 2026 market, let's look at a hypothetical scenario for a high-growth professional, "Sarah," who is looking to optimize her tax-free wrappers.- The Financial Snapshot: Sarah has a £50,000 ISA on Trading 212 and a £100,000 SIPP on Freetrade. She is currently contributing £2,000 per month.

- The Budget Reality: In 2026, she is offered a new "Agentic Transfer" tool that moves her dividends in real-time. Her overall portfolio yield increases to 4.5% within the first 30 days. While this is higher than she would have achieved manually, her overall management time has decreased by 15% in the same period, making her "leisure-to-wealth" ratio manageable.

- The Market Advantage: Because she is investing in a "high-growth" northern hub, she is entering a market that is forecasted to rise by 2.5% by the end of the year. This means she could see her customer base grow by over £25,000 in just her first year of scaling, far outpacing the 5% return she would have received in a traditional high-yield savings account.

The AI Factor: Which App is Smarter?

To understand the 3,000-word scope of this guide, we must look at the broader role of the AI Portfolio Assistant in 2026.Trading 212's "Agentic" Assistant

The "return to 2% inflation" was the major economic goal for spring 2026. However, the outbreak of war in the Middle East has created new upward pressure on energy and fuel prices, disrupting this path. In this environment, the "geopolitical tax" is felt through increased market volatility. Trading 212's AI Assistant provides real-time sentiment analysis and "Risk Scoring" for your Pies, helping you navigate these spikes. In 2026, the AI itself is the most powerful risk management tool available.Freetrade's "Market Insights"

Despite the focus on active trading, the UK and global markets continue to face a significant Information Constraint. The shortage of high-quality, jargon-free financial news remains a primary driver of investor errors. In 2026, Freetrade's "Market Insights" tool uses generative AI to provide personalized news feeds based on your holdings, ensuring you are only seeing the information that actually impacts your sovereign wealth.Safety and Regulation (2026)

As we look toward the end of 2026 and into 2027, the use of Regulatory Guardrails has become the final layer of investor sovereignty.FCA Protection and FSCS

Both Trading 212 and Freetrade are fully regulated by the Financial Conduct Authority (FCA). In 2026, the Financial Services Compensation Scheme (FSCS) provides protection for up to £85,000 per person, per firm, in the event of a platform failure. This "Safety Net" is a critical mental model for professional investors, ensuring that even in a "jagged frontier" of market volatility, their core capital remains secure.Human-in-the-Loop

The 2026 investor is "AI-fluent" and highly informed. They are using advanced tools to track market moves and are more willing to wait for the "right" deal rather than rushing into a trade. This has led to a market that is resilient but cautious, where the human "Strategist" provides the "why" that the AI "Agent" needs to function effectively.Final Checklist: How to Navigate the 2026 Investment Market

- Audit Your Tax-Free Wrappers: If your current ISA model expires in 2026, start your research at least six months in advance. Know your "tax-free shock" number and adjust your budget accordingly.

- Focus on Regional Resilience: Look beyond the national average. The Midlands and the North are the "wealth engines" of the 2026 consumer market.

- Check the "Agentic" Potential: If you are buying or selling, know the AI-native potential. A higher agentic rating is not just good for efficiency; it is a direct financial advantage in the 2026 investment market.

- Beware of "Inflation Noise": Don't let short-term geopolitical events distract you from the long-term fundamentals of the market. Resilience is the key theme of 2026.

- Set Your "Quality" Threshold: Whether you are an investor or a marketer, focus on platforms with high utility and low maintenance. The 2026 market rewards quality over speculation.

- Celebrate the "Steady" Recovery: A market that grows by 2% is a market that is sustainable. Acknowledge that you are "buying" a piece of your future financial sovereignty in a normalized, healthy economy.

Deep Dive: The Psychology of the 2026 UK Investor

To understand the full scope of this guide, we must look at the psychological context that has led to the 2026 investment landscape. For decades, the "Investment Platform" was seen as a guaranteed wealth-building machine—a piece of real estate that would always outperform the stock market. However, the last five years have seen a radical shift. In 2026, the investment market has been integrated into a more sophisticated financial world, where investors are as likely to track their "equity growth" as they are their "crypto portfolio." This "co-creation" environment has made the choice of regional market a critical mental model for professional survival.1. The Death of the "London-First" Mindset

The primary reason for the shift in 2026 is the realization that the London-first mindset is no longer the default. Behavioral economists have long known that humans are "locked-in" to their traditional ways of working and living. This "lock-in effect" has suppressed regional productivity for years. However, by adopting a more regional approach, professionals are finding a way to unlock their potential while providing a massive benefit to their organizations. The regional hub acts as a cognitive bridge, allowing humans to live in high-quality, affordable environments while still being connected to the global economy.2. The Role of "Market-Specific" Training in 2026

In the 2026 corporate landscape, the "Training Era" has reached its peak. Companies are not just teaching their employees how to work; they are providing the technical and psychological infrastructure to manage their lives. From AI-driven "investment coaching" that predicts which regional market is best for a specific family to automated "Equity Alerts" that warn when a yield is about to change, these platforms have removed much of the friction that once made ownership a nightmare. They ask: "Are you working harder, or are you living smarter in your regional hub?"3. The "Hidden Costs" of Portfolio Neglect in 2026

In 2026, the cost of portfolio neglect is rarely just a loss of value. From "energy gaps" that have ballooned to 20% of a platform's potential to high-end "maintenance churn" that occurs when older portfolios are not retrofitted, the "second half" of the investment cost is often hidden in the fine print. A regional strategy ensures you are using your portfolio in a way that is sustainable, ethical, and highly productive. It ensures you have the mental energy to handle the "jagged" parts of your work without breaking your budget of time and attention.Conclusion: The Final Verdict

The UK retail investment landscape in 2026 is a landscape of opportunity and caution. While the national headlines may focus on the "slight tumble" in consumer sentiment or the "yield shock" of high interest rates, the real story is found in the Value Equation of these two platforms.- Best for Active Traders: Trading 212. Its 0.15% FX fee, zero commission, and superior mobile app make it the undisputed leader for those trading US and UK stocks frequently.

- Best for Pension Savers: Freetrade. Its flat-fee SIPP model is the most cost-effective way to build long-term wealth in a tax-efficient wrapper.

- Best for ISA-only Investors: Trading 212. The combination of a free Stocks & Shares ISA and a high-yield Cash ISA (up to 4.6% AER) is an unbeatable "Double-ISA" strategy.

- Best for Beginners: Trading 212. The "Pies" and "AutoInvest" features provide a more intuitive "hand-holding" experience for those just starting their journey.

Frequently Asked Questions (FAQ)

1. Is Trading 212 better than Freetrade for beginners?

In 2026, Trading 212 is generally considered better for beginners due to its "Pies & AutoInvest" feature, which allows for highly automated, hands-off investing. Freetrade is also beginner-friendly but requires a subscription for the ISA, which may be a barrier for those with small starting amounts.2. Does Trading 212 have a SIPP in 2026?

As of early 2026, Trading 212 still does not offer a SIPP in the UK. For those looking to manage their pension, Freetrade's flat-fee SIPP remains the superior choice among the two.3. Which app pays more interest on uninvested cash?

Trading 212 currently leads with up to 4.6% AER on its Cash ISA and competitive rates on uninvested cash in its Invest account. Freetrade pays interest to Plus members, but it is typically capped at a certain balance (e.g., £4,000).4. How do the FX fees compare for US stocks?

Trading 212 is significantly cheaper with a flat 0.15% FX fee. Freetrade charges 0.39% for Plus members, 0.59% for Standard, and 0.99% for Basic. For a £1,000 trade, T212 would cost £1.50, while Freetrade would cost between £3.90 and £9.90.5. Can I transfer my ISA from Freetrade to Trading 212?

Yes, both platforms support the official ISA transfer process. In 2026, these transfers are typically "in-specie" (meaning your stocks are moved without being sold), though some specific fractional shares may need to be liquidated first.External References and Resources

FCA: Consumer Duty - Final Non-Handbook Guidance 2026, Bank of England: Official Bank Rate History and Forecasts, Trading 212: Cash ISA and Interest on Cash Terms 2026, Freetrade: SIPP Charges and Subscription Schedule 2026, MatchMyBroker: Trading 212 vs Freetrade UK 2026 Comparison, InvestPlatforms: Freetrade vs Trading 212 vs InvestEngine 2026, StockBrokers.com: Best UK Trading Platforms for Beginners 2026, Independent: Best Cash ISA Rates April 2026 - The T212 Exclusive

0 Comments Comments