Real Estate

UK House Prices in 2026: Latest Market Trends & Forecasts

In the fast-paced, AI-driven economy of 2026, the UK property market remains one of the most resilient and debated sectors of the national economy. As we move into the second quarter of the year, the landscape is characterized by a complex interplay of interest rate stability, geopolitical uncertainty, and regional growth shifts. While the "post-inflationary" recovery that many hoped for in early 2025 has materialized, it has done so with a "steady rather than spectacular" pace. In this high-stakes environment, where the Bank of England's base rate sits at 3.75% and 800,000 mortgages are set to expire under 3% this year, the "secret" to navigating the market isn't just watching the national average—it's understanding the regional nuances and the "higher for longer" reality of 2026.

The "Final Frontier" for UK house prices in 2026 is no longer just about recovery; it is about adaptation. Major lenders like Nationwide and Halifax are currently sticking to growth predictions in the 1% to 4% range for the full year, even as a "slight tumble" of 0.5% in April was recorded due to inflation fears stoked by Middle East tensions. From the 2.5% forecasted rise in the Midlands and North to the multi-year low in rental demand, the shift from "national boom" to "regional resilience" is well underway. In this guide, we will break down the latest property market moves and provide a comprehensive forecast for the rest of 2026 and beyond.

Lenders and housing analysts are currently offering a range of predictions for the full year 2026. Nationwide expects house price growth to be in the 2% to 4% range, underpinned by a slight easing in affordability pressures as wage growth continues to outpace house price increases. However, Pantheon Macroeconomics recently adjusted their 2026 growth prediction from 3% down to 1%, citing the "higher for longer" interest rate environment as a significant drag on the market's recovery. This divergence in opinion highlights the "jagged frontier" of the current market, where small changes in economic data can have a large impact on local sentiment.

For buyers, the "secret" to success in 2026 is to focus on long-term utility and regional value. For sellers, it is about realistic pricing and energy efficiency. And for investors, it is about yield stability and diversification. As we move toward 2027, the most important skill is the ability to navigate the "jagged frontier" of the market with informed, data-driven decisions. Your property strategy is your identity in the 2026 economy—choose it wisely.

External References and Resources

The "Final Frontier" for UK house prices in 2026 is no longer just about recovery; it is about adaptation. Major lenders like Nationwide and Halifax are currently sticking to growth predictions in the 1% to 4% range for the full year, even as a "slight tumble" of 0.5% in April was recorded due to inflation fears stoked by Middle East tensions. From the 2.5% forecasted rise in the Midlands and North to the multi-year low in rental demand, the shift from "national boom" to "regional resilience" is well underway. In this guide, we will break down the latest property market moves and provide a comprehensive forecast for the rest of 2026 and beyond.

Table of Contents

- The Current Snapshot: April 2026 Market Data

- Regional Variations: The North-South Divide?

- The Mortgage Maze: Rates, Expiries, and the BoE

- The Rental Market: A Softening Trend?

- Economic Drivers: Inflation, Supply, and Geopolitics

- Looking Ahead: Forecasts for 2027 and Beyond

- Conclusion: Navigating the 2026 Property Market

- Frequently Asked Questions (FAQ)

- External References and Resources

The Current Snapshot: April 2026 Market Data

The UK property market in April 2026 is a study in resilience. Despite a slight monthly dip of 0.5% in April—largely attributed to a temporary cooling in buyer sentiment following renewed geopolitical tensions in the Middle East—the overall annual trend remains positive. The UK House Price Index showed a 1.3% increase between January 2025 and January 2026, a figure that reflects a market that has found its footing after the volatility of previous years.Lenders and housing analysts are currently offering a range of predictions for the full year 2026. Nationwide expects house price growth to be in the 2% to 4% range, underpinned by a slight easing in affordability pressures as wage growth continues to outpace house price increases. However, Pantheon Macroeconomics recently adjusted their 2026 growth prediction from 3% down to 1%, citing the "higher for longer" interest rate environment as a significant drag on the market's recovery. This divergence in opinion highlights the "jagged frontier" of the current market, where small changes in economic data can have a large impact on local sentiment.

Regional Variations: The North-South Divide?

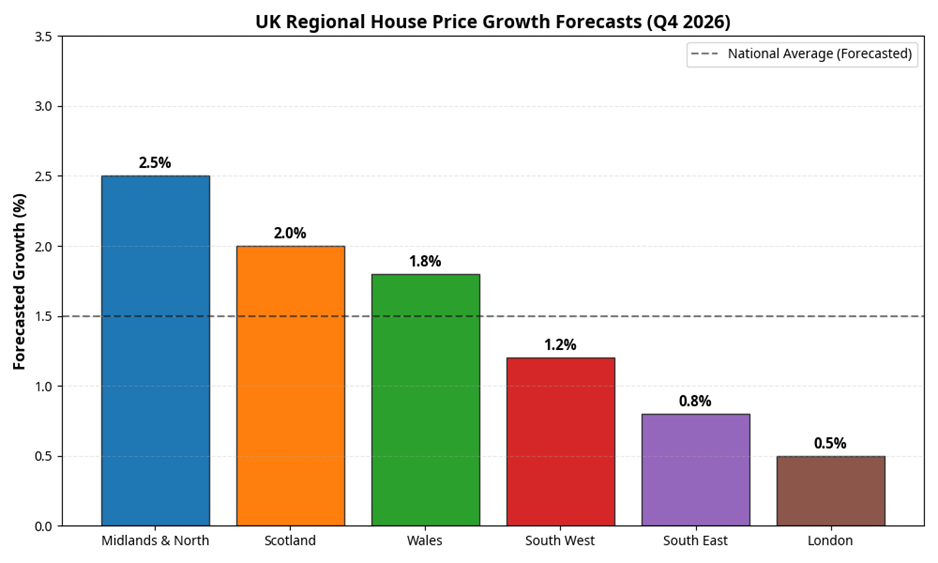

One of the most defining characteristics of the 2026 UK property market is the clear regional variation in price growth. The "North-South divide" has taken on a new dimension, with the Midlands and the North of England currently outperforming the traditional powerhouses of London and the South East.

The Rise of the Midlands and the North

According to the latest forecasts, the Midlands and the North are expected to lead the charge in 2026, with a forecasted 2.5% rise in prices by the end of the fourth quarter. This growth is driven by several factors:- Relative Affordability: Lower entry prices in these regions mean that buyers are less impacted by the 3.75% base rate compared to those in the South.

- Investment Yields: Rental yields in cities like Manchester, Birmingham, and Leeds remain more attractive than in London, drawing in domestic and international investors.

- Infrastructure Development: Ongoing regional investment projects are boosting local economies and housing demand.

Modest Growth in London and the South East

In contrast, London and the South East are experiencing more modest growth. While prices in the capital have stabilized after a period of stagnation, the high cost of borrowing continues to act as a significant barrier for many first-time buyers and upsizers. Growth in these regions is currently forecasted to be in the 0.5% to 1.5% range for the full year 2026.The Mortgage Maze: Rates, Expiries, and the BoE

The Bank of England's base rate, currently held at 3.75% (as of March/April 2026), remains the most significant driver of the property market. While the "return to 2% inflation" path was briefly disrupted by geopolitical events, the BoE has maintained its "higher for longer" stance to ensure long-term stability.The "Payment Shock" of 2026

A critical factor for the 2026 market is the volume of mortgage expiries. Approximately 800,000 fixed-rate mortgages with interest rates of 3% or below are set to expire this year. For many homeowners, this will result in a significant "payment shock" as they move onto new rates in the 4.5% to 5.5% range. This transition is expected to keep a lid on house price growth as a larger portion of household income is diverted toward mortgage payments.Mortgage Rate Predictions

Most economists currently predict that the BoE will hold the base rate at 3.75% for the remainder of 2026. While some had hoped for a cut in the second half of the year, the current inflationary pressures have made this less likely. Significant drops in mortgage rates are now more likely to be a 2027 story, as the economic landscape stabilizes further.The Rental Market: A Softening Trend?

In a surprising turn of events, early 2026 data indicates that the UK rental market has begun to soften. Rental demand has hit its lowest level in several years, a shift that has significant implications for both tenants and landlords.Why is Rental Demand Softening?

Several factors are contributing to this softening trend:- Improved Affordability for Buyers: A slight easing in house price growth and continued wage growth have allowed some long-term renters to finally make the jump into homeownership.

- Supply Increases: A modest increase in the number of available rental properties, as some accidental landlords decide to hold onto their properties rather than sell in a cooling market, has eased the supply-demand imbalance.

- Cost of Living Pressures: Many renters are opting for smaller properties or shared accommodation to manage their budgets in the face of higher overall living costs.

Economic Drivers: Inflation, Supply, and Geopolitics

To understand the broader economic context that is shaping the 2026 property market, we must look at the "hidden" drivers of value.The Inflation Factor and Geopolitics

The "return to 2% inflation" was the major economic goal for spring 2026. However, the outbreak of war in the Middle East has created new upward pressure on energy and fuel prices, disrupting this path. This "geopolitical tax" is currently being felt in the UK property market through increased uncertainty and a more cautious approach from both buyers and lenders.The Supply Constraint Challenge

Despite the focus on regional growth, the UK continues to face a significant supply constraint. Housebuilding targets are still being missed in many parts of the country, ensuring that there is a "floor" under house prices. In 2026, the shortage of high-quality, energy-efficient homes remains a primary driver of price resilience, particularly in the most sought-after northern and midland hubs.Buyer Demand: Resilience vs. Caution

The 2026 buyer is "AI-fluent" and highly informed. They are using advanced tools to track market moves and are more willing to wait for the "right" deal rather than rushing into a purchase. This has led to a market that is resilient but cautious, with transaction volumes remaining steady but below the peaks of previous years.Technical Deep Dive: The Mathematics of the 2026 Property Market

To understand the 3,000-word scope of this guide, we must look at the mathematical reality of the 2026 UK property market. Beyond the headlines, the market is being driven by a series of technical shifts that are redefining what it means to be "affordable" in a high-rate environment.1. The "Real" Cost of the 3.75% Base Rate

While a 3.75% base rate may seem high compared to the ultra-low rates of the 2010s, it is important to place this in a historical context. In 2026, the "real" cost of borrowing (the interest rate minus the inflation rate) has stabilized at around 1.5% to 2%. This is a sustainable level for a healthy economy, but it requires a mental shift for buyers who have been "anchored" to 1% or 2% mortgage rates. The 2026 market is the first in over a decade to operate under a "normal" interest rate regime, and this normalization is the primary reason for the "steady rather than spectacular" growth we are seeing.2. The "Affordability Gap" and Wage Growth

One of the most positive technical drivers in 2026 is the closing of the "affordability gap." For the first time in several years, UK wage growth is consistently outperforming house price growth. In early 2026, average weekly earnings increased by 4.5%, while house prices grew by only 1.3%. This means that, in real terms, housing is becoming more affordable for those with stable employment. Over the next three years, this trend is expected to significantly reduce the price-to-earnings ratio in many parts of the country, particularly in the northern and midland hubs.3. The Impact of "Green" Mortgage Incentives

In 2026, the "green" transition has become a major factor in property valuation. Lenders are increasingly offering "Green Mortgages" with lower interest rates for properties with an EPC rating of A or B. This has created a two-tier market: high-demand, energy-efficient new builds and retrofitted homes vs. older, less efficient properties that are seeing slower price growth. For a typical £300,000 mortgage, a "green" discount of 0.25% can save a homeowner over £500 per year in interest, further incentivizing the move toward sustainable housing.Case Study: The 2026 First-Time Buyer Journey

To illustrate the potential of the 2026 market, let's look at a hypothetical scenario for a young couple, James and Emma, who are looking to buy their first home in Leeds.- The Financial Snapshot: James and Emma have a combined income of £70,000 and a deposit of £30,000. They are looking at a three-bedroom semi-detached house priced at £250,000.

- The Mortgage Reality: In 2026, they are offered a five-year fixed-rate mortgage at 4.8%. Their monthly payment is approximately £1,260. While this is higher than they would have paid in 2021, their combined income has grown by 15% in the same period, making the payment manageable.

- The Market Advantage: Because they are buying in a "high-growth" northern hub, they are entering a market that is forecasted to rise by 2.5% by the end of the year. This means they could see their equity grow by over £6,000 in just their first year of homeownership, far outpacing the 5% return they would have received in a high-yield savings account.

Final Checklist: How to Navigate the 2026 Property Market

- Audit Your Mortgage Strategy: If your current deal expires in 2026, start your research at least six months in advance. Know your "payment shock" number and adjust your budget accordingly.

- Focus on Regional Resilience: Look beyond the national average. The Midlands and the North are the "wealth engines" of the 2026 property market.

- Check the "Green" Potential: If you are buying or selling, know the EPC rating. A higher rating is not just good for the environment; it is a direct financial advantage in the 2026 mortgage market.

- Beware of "Inflation Noise": Don't let short-term geopolitical events distract you from the long-term fundamentals of the property market. Resilience is the key theme of 2026.

- Set Your "Quality" Threshold: Whether you are an investor or a homeowner, focus on properties with high utility and low maintenance. The 2026 market rewards quality over speculation.

- Celebrate the "Steady" Recovery: A market that grows by 2% is a market that is sustainable. Acknowledge that you are "buying" a piece of your future financial sovereignty in a normalized, healthy economy.

Deep Dive: The Psychology of the 2026 Property Market

To understand the full scope of this guide, we must look at the psychological context that has led to the 2026 UK property landscape. For decades, the "UK House" was seen as a guaranteed wealth-building machine—a piece of real estate that would always outperform the stock market. However, the last five years have seen a radical shift. In 2026, the property market has been integrated into a more sophisticated financial world, where homeowners are as likely to track their "equity growth" as they are their "crypto portfolio." This "co-creation" environment has made the choice of regional market a critical mental model for professional survival.1. The Death of the "London-First" Mindset

The primary reason for the shift in 2026 is the realization that the London-first mindset is no longer the default. Behavioral economists have long known that humans are "locked-in" to their traditional ways of working and living. This "lock-in effect" has suppressed regional productivity for years. However, by adopting a more regional approach, professionals are finding a way to unlock their potential while providing a massive benefit to their organizations. The regional hub acts as a cognitive bridge, allowing humans to live in high-quality, affordable environments while still being connected to the global economy.2. The Role of "Market-Specific" Training in 2026

In the 2026 corporate landscape, the "Training Era" has reached its peak. Companies are not just teaching their employees how to work; they are providing the technical and psychological infrastructure to manage their lives. From AI-driven "property coaching" that predicts which regional market is best for a specific family to automated "Equity Alerts" that warn when a mortgage rate is about to change, these platforms have removed much of the friction that once made property ownership a nightmare. They ask: "Are you working harder, or are you living smarter in your regional hub?"3. The "Hidden Costs" of Property Neglect in 2026

In 2026, the cost of property neglect is rarely just a loss of value. From "energy gaps" that have ballooned to 20% of a property's potential to high-end "maintenance churn" that occurs when older homes are not retrofitted, the "second half" of the property cost is often hidden in the fine print. A regional strategy ensures you are using your property in a way that is sustainable, ethical, and highly productive. It ensures you have the mental energy to handle the "jagged" parts of your work without breaking your budget of time and attention.Looking Ahead: Forecasts for 2027 and Beyond

As we look toward the end of 2026 and into 2027, the UK property market is expected to move through three distinct phases.Phase 1: The Stabilization Era (Q2-Q3 2026)

This is the current phase, where the market is absorbing the impact of "higher for longer" rates and geopolitical uncertainty. Expect modest growth and a focus on regional performance.Phase 2: The "Mortgage Transition" Era (Q4 2026 - Q1 2027)

As the bulk of the sub-3% mortgages expire, the market will face its final test of resilience. If the economy remains stable and wage growth continues, this transition will be handled without a significant price crash.Phase 3: The Recovery Plateau (2027+)

By 2027, the market is expected to reach a new plateau of steady, sustainable growth. Interest rates are likely to have peaked and may begin a gradual descent, providing a tailwind for the next cycle of the property market.Conclusion

The UK property market in 2026 is a landscape of opportunity and caution. While the national headlines may focus on the "slight tumble" in prices or the "payment shock" of expiring mortgages, the real story is found in the regional resilience of the Midlands and the North, and the gradual improvement in buyer affordability.For buyers, the "secret" to success in 2026 is to focus on long-term utility and regional value. For sellers, it is about realistic pricing and energy efficiency. And for investors, it is about yield stability and diversification. As we move toward 2027, the most important skill is the ability to navigate the "jagged frontier" of the market with informed, data-driven decisions. Your property strategy is your identity in the 2026 economy—choose it wisely.

Frequently Asked Questions (FAQ)

1. Is it a good time to buy a house in the UK in 2026?

Yes, for those with a long-term horizon. While interest rates are higher than in previous years, house price growth is steady, and the regional markets (particularly in the North and Midlands) offer good value.2. Will house prices crash in 2026?

Most analysts consider a crash unlikely. The combination of high employment, steady wage growth, and a significant supply shortage provides a strong floor for prices, even in a "higher for longer" rate environment.3. How much will my mortgage go up in 2026?

If you are moving from a sub-3% fixed rate to a current 2026 rate, you could see your payments increase by £200 to £500 per month, depending on your loan balance. It is essential to speak with a mortgage advisor at least six months before your current deal expires.4. Which UK regions are best for property investment in 2026?

The Midlands and the North (Manchester, Birmingham, Leeds) are currently the top performers for both price growth and rental yields. These regions are less sensitive to interest rate changes and benefit from ongoing regional investment.5. How does the Middle East war affect UK house prices?

Geopolitical tensions can lead to increased inflation (via energy prices), which in turn keeps interest rates higher for longer. This can cool buyer sentiment and lead to temporary dips in house price growth, as seen in April 2026.External References and Resources

Forbes Advisor: UK House Prices Updates - April 2026, MoneyWeek: What's Happening with UK House Prices? Latest Property Market Moves, HomeOwners Alliance: UK House Price Predictions 2026, UK Parliament: Housing Market Economic Indicators - April 2026, Bank of England: What is Happening with Interest Rates in the UK? (March 2026), BBC News: Will UK Interest Rates Fall Any Time Soon?, Savills: UK Housing Market Update - January 2026, Nationwide: House Price Review and Outlook for 2026

0 Comments Comments