Budgeting

What Is Joyful Budgeting and How to Prepare One

Most people have tried a traditional budget at some point in their lives. Most of those budgets failed — not because the maths were wrong, but because they were built around restriction rather than intention. Joyful budgeting, which Essence and Bank of America named a top consumer financial trend for 2026, flips the model: instead of starting with what you must cut, it starts with what genuinely brings you joy — and builds the numbers around that. Intuit's January 2026 research found that joy is now the leading driver of consumer spending at 38%, outranking both convenience and security. This guide explains exactly what joyful budgeting is and how to build one.

Joyful budgeting is the practice of building your financial plan around the spending that genuinely enriches your life, rather than starting with restrictions and working outward. It is sometimes called joy-based budgeting or values-based budgeting, and it was named a top consumer financial trend for 2026 by Essence magazine in partnership with Bank of America in February 2026.

NerdWallet's April 2026 analysis provides the clearest working definition: joyful budgeting is 'the practice of spending money on the things that enrich your life while still meeting your savings goals.' The key distinction from a traditional budget is the starting point. A traditional budget starts with income, subtracts fixed costs and savings targets, and treats what remains as the maximum allowable discretionary spending — typically experienced as a ceiling. A joyful budget starts with a list of what genuinely brings joy, allocates real money to those things first within a responsible framework, and then cuts ruthlessly from the things that bring no real satisfaction.

Bank of America's research team describes the approach to Essence in February 2026 as: 'Instead of cutting everything out, you first identify the spending that brings you real joy — whether that's experiences, time with loved ones, or meaningful hobbies — and then build your budget around those priorities while still saving consistently.' The 'while still saving consistently' is not optional — joyful budgeting is not a licence to spend everything on pleasures and ignore financial stability. It is a reordering of priorities within a responsible financial framework, not an abandonment of one.

Joy-based budgeting can be successful because it includes the fun parts of life, instead of a more limiting style of budgeting that fails almost every time. It is spending on purpose. Spending intentionally.

— ASHLEY BLECKNER, CFP, SAN DIEGO — NERDWALLET, APRIL 2026

CFP Kaylee McClellan, speaking to NerdWallet in April 2026, makes the analogy explicit: 'In much the same way that including some chocolate might help you stick to a diet, including some joyful spending can help you stick to a long-term financial plan.' Diets built on total deprivation fail almost universally. Diets with a structured allowance for enjoyment have dramatically better completion rates. The same logic applies to financial plans — not because people lack discipline, but because the human capacity for sustained self-denial in the face of enjoyable alternatives is finite and predictable.

McClellan describes clients in their thirties who find it 'challenging to want to save all this money for this future date' when the present holds uncertainty. Without building in the travel they value, she says, 'they'd be miserable. And they wouldn't be able to buy into the long-term savings plan.' The joyful budget solves this by making the long-term plan include the things that make current life worth living — not as a compromise, but as an essential design feature. A budget that people will actually follow for years is more valuable than a theoretically optimal budget they abandon in the first month.

The first psychological principle is autonomy. People comply with externally imposed rules, but they commit to self-chosen decisions. A budget experienced as an external constraint ('I have to stick to this budget') generates resistance. A budget experienced as a personal expression of values ('I am choosing to fund the things that matter to me and skip the ones that don't') generates ownership. The spending choices in a joyful budget feel chosen rather than forced — because they genuinely are.

The second principle is what CFP Nick Gertsema describes to NerdWallet as the Red Car Theory: 'If you're thinking about buying a red car, you suddenly notice red cars everywhere.' When you have identified and named what brings you joy — specific experiences, specific relationships, specific activities — you become more attuned to opportunities that serve those values and less reflexively responsive to marketing and social comparison that previously drove spending on things that brought no real satisfaction. The clarity of a joy list is itself a filter on impulsive spending.

Intuit's January 2026 Financial Wellness Survey confirms the cultural shift this psychology is producing: joy has emerged as the leading driver of consumer spending at 38%, outranking convenience, confidence, and security. And 41% of respondents say they feel justified in spending on things that make them happy. This is not irresponsibility — it is the population-level expression of a psychological truth that financial planners have known for years: sustainable financial behaviour must include positive reinforcement, not just restraint.

Brian Ford, head of financial wellness at Truist, frames the essential question: 'One of the keys to finding happiness with money is to stop spending on stuff you don't actually care about in life.' The joy list is the answer to the inverse question: what do you actually care about? It might include specific experiences (coffee from a particular café, weekend hiking, live music), relationships (regular dinners with friends, visits to family), physical wellbeing (a gym class you genuinely enjoy, quality food), creative pursuits (art supplies, photography, writing tools), or comfort (a good mattress, quality clothing you actually wear).

Write the list without editing or judging it. Fifteen to twenty items is a good starting point. Rank them loosely from 'brings the most joy' to 'brings the least joy.' This ranked list becomes the decision-making framework for the entire budget — it determines which spending categories receive more than average allocation and which receive less or nothing.

Most people discover one of three patterns in the audit. The first is a joy gap: the things on their joy list are underfunded — they are not actually spending on the things that matter most to them. The second is joy misalignment: money is flowing to habitual or socially influenced spending rather than the things they identified as genuinely joyful. The third is a combination: some joy-aligned spending is present but competing with a large volume of joyless automatic or habitual expenditure that has never been questioned.

Circle every transaction on the audit that corresponds directly to something on your joy list. These are your joy-aligned expenditures — the spending you want to protect and potentially increase. Everything uncircled is a candidate for reduction or elimination to fund more of what is circled. The audit is not a guilt exercise. It is data collection that reveals the gap between your current financial life and the one you actually want.

Ramit Sethi's 'conscious spending' model, cited in the Nasdaq values-based budgeting analysis, captures the principle: spend lavishly on things you love and cut costs mercilessly on things you don't. The separation exercise makes this practical — it gives you a specific target for merciless cutting (the joyless spending list) and a specific home for the redirected funds (the joy spending list). The discipline is not in restricting joy spending but in ruthlessly eliminating joyless spending that is consuming the budget's capacity for the things that matter.

The joy fund converts aspirational spending from anxiety to anticipation. Deciding in September that you want to attend a festival in July and putting £30 per month into a named 'Festival' savings pot means arriving at the ticket-purchase moment with the money already saved, the decision already made, and zero guilt about spending it. The money was earmarked for this purpose. Spending it is not a financial failure — it is a financial success.

In practice, most joyful budgeters maintain two or three concurrent joy funds: one for a near-term experience (next month or two), one for a medium-term goal (six months to a year), and one for a larger aspiration (one to three years). Each fund has a name that reflects the actual joy it is building toward. Seeing 'Weekend Away with Friends — £120/£400 saved' in your banking app is qualitatively different from seeing 'Savings — £120' — it connects the financial discipline of saving to the specific joy it is creating.

The monthly review has four questions. First: did my joy spending last month actually bring joy, or was it habit or social obligation? Second: is there something new on my joy list that is underfunded? Third: is my savings and financial goals category on track? And fourth: are there any joyless spending categories that have crept back up that need to be cut again? The review takes fifteen to twenty minutes and prevents the most common failure mode of joyful budgeting — the gradual drift back toward habitual spending that is no longer genuinely joyful.

Intuit's January 2026 survey finding that 43% of consumers plan to adopt a balanced expense management mindset — 'consistent tracking that still leaves breathing room' — is the joyful budget in practice. The balance between financial responsibility and genuine enjoyment is not a compromise of both. It is the most sustainable financial approach available, because it is the only one that a human being can follow with genuine enthusiasm rather than grim determination.

The six steps in this guide — write your joy list, complete a spending audit, separate joy from joyless spending, build the framework, create your joy fund, and review monthly — can be completed in a Sunday afternoon. The result is a budget that still funds your emergency savings, still pays down debt, and still builds your long-term financial security — while actively making room for the experiences, relationships, and activities that make your daily life genuinely worth living. That is not a compromise between financial responsibility and personal fulfilment. It is both at once.

Essence / Bank of America — Why Joy-Based Budgeting Is Becoming the New Way People Manage Money in 2026 (February 2026) https://www.essence.com/news/money-career/joy-based-budgeting-financial-trend/

Intuit — 2026 Financial Forecast: Staying Mindful Amid Money Stress (January 2026) https://www.intuit.com/blog/innovative-thinking/2026-financial-forecast-mindful-stress/

Truist — Building a Values-Based Budget: How to Spend Mindfully https://www.truist.com/money-mindset/principles/budgeting-by-values/building-a-values-based-budget

Nasdaq / GOBankingRates — 3 Signs a Values-Based Budget Is Best for Your Money (Ramit Sethi conscious spending) https://www.nasdaq.com/articles/3-signs-values-based-budget-best-your-money

CNBC Select — 5 Best Free Budgeting Tools of 2026 (April 2026) https://www.cnbc.com/select/best-free-budgeting-tools/

Ramsey Solutions — The State of Personal Finance in America Q4 2025 (February 2026) https://www.ramseysolutions.com/budgeting/state-of-personal-finance

Monarch Money — Financial Resolutions for 2026: Tips to Achieve Your Money Goals (February 2026) https://www.monarch.com/blog/personal-finance/financial-resolutions

MoneyHelper (UK) — How to Create a Budget: Official Free Guidance https://www.moneyhelper.org.uk/en/money-troubles/way-forward/how-to-create-a-budget

TABLE OF CONTENTS

- What Is Joyful Budgeting? The Definition

- Why Traditional Budgets Fail (and Why Joyful Budgeting Doesn't)

- The Psychology Behind Joyful Budgeting

- Joyful Budgeting vs Other Budget Methods

- How to Build Your Joyful Budget: A Six-Step Plan

- Step 1 — Write Your Joy List

- Step 2 — Complete a Spending Audit

- Step 3 — Separate Joy Spending from Joyless Spending

- Step 4 — Build Your Joyful Budget Framework

- Step 5 — Set Your Joy Fund

- Step 6 — Review Monthly — Does This Still Bring Joy?

- Common Mistakes When Building a Joyful Budget

- Conclusion

- Frequently Asked Questions

- References

What Is Joyful Budgeting? The Definition

Joyful budgeting is the practice of building your financial plan around the spending that genuinely enriches your life, rather than starting with restrictions and working outward. It is sometimes called joy-based budgeting or values-based budgeting, and it was named a top consumer financial trend for 2026 by Essence magazine in partnership with Bank of America in February 2026.NerdWallet's April 2026 analysis provides the clearest working definition: joyful budgeting is 'the practice of spending money on the things that enrich your life while still meeting your savings goals.' The key distinction from a traditional budget is the starting point. A traditional budget starts with income, subtracts fixed costs and savings targets, and treats what remains as the maximum allowable discretionary spending — typically experienced as a ceiling. A joyful budget starts with a list of what genuinely brings joy, allocates real money to those things first within a responsible framework, and then cuts ruthlessly from the things that bring no real satisfaction.

Bank of America's research team describes the approach to Essence in February 2026 as: 'Instead of cutting everything out, you first identify the spending that brings you real joy — whether that's experiences, time with loved ones, or meaningful hobbies — and then build your budget around those priorities while still saving consistently.' The 'while still saving consistently' is not optional — joyful budgeting is not a licence to spend everything on pleasures and ignore financial stability. It is a reordering of priorities within a responsible financial framework, not an abandonment of one.

Joy-based budgeting can be successful because it includes the fun parts of life, instead of a more limiting style of budgeting that fails almost every time. It is spending on purpose. Spending intentionally.

— ASHLEY BLECKNER, CFP, SAN DIEGO — NERDWALLET, APRIL 2026

Why Traditional Budgets Fail (and Why Joyful Budgeting Doesn't)

The failure rate of traditional budgets is not a secret. Most people who create a strict budget — one built entirely around restriction, with every discretionary category minimised — abandon it within weeks. The reason is not lack of willpower. It is design: a budget that creates a continuous experience of deprivation is competing against every enjoyable thing in daily life, and deprivation reliably loses.CFP Kaylee McClellan, speaking to NerdWallet in April 2026, makes the analogy explicit: 'In much the same way that including some chocolate might help you stick to a diet, including some joyful spending can help you stick to a long-term financial plan.' Diets built on total deprivation fail almost universally. Diets with a structured allowance for enjoyment have dramatically better completion rates. The same logic applies to financial plans — not because people lack discipline, but because the human capacity for sustained self-denial in the face of enjoyable alternatives is finite and predictable.

McClellan describes clients in their thirties who find it 'challenging to want to save all this money for this future date' when the present holds uncertainty. Without building in the travel they value, she says, 'they'd be miserable. And they wouldn't be able to buy into the long-term savings plan.' The joyful budget solves this by making the long-term plan include the things that make current life worth living — not as a compromise, but as an essential design feature. A budget that people will actually follow for years is more valuable than a theoretically optimal budget they abandon in the first month.

The Psychology Behind Joyful Budgeting

Joyful budgeting is grounded in well-established psychological principles around motivation, identity, and behaviour change. Truist's positive psychology expert Bright Dickson describes it: 'Values-based budgeting can help you feel empowered over your financial choices.' The shift from 'I cannot afford this' to 'I choose not to spend here' is not merely semantic — it represents a fundamental change in the relationship between the person and their money.The first psychological principle is autonomy. People comply with externally imposed rules, but they commit to self-chosen decisions. A budget experienced as an external constraint ('I have to stick to this budget') generates resistance. A budget experienced as a personal expression of values ('I am choosing to fund the things that matter to me and skip the ones that don't') generates ownership. The spending choices in a joyful budget feel chosen rather than forced — because they genuinely are.

The second principle is what CFP Nick Gertsema describes to NerdWallet as the Red Car Theory: 'If you're thinking about buying a red car, you suddenly notice red cars everywhere.' When you have identified and named what brings you joy — specific experiences, specific relationships, specific activities — you become more attuned to opportunities that serve those values and less reflexively responsive to marketing and social comparison that previously drove spending on things that brought no real satisfaction. The clarity of a joy list is itself a filter on impulsive spending.

Intuit's January 2026 Financial Wellness Survey confirms the cultural shift this psychology is producing: joy has emerged as the leading driver of consumer spending at 38%, outranking convenience, confidence, and security. And 41% of respondents say they feel justified in spending on things that make them happy. This is not irresponsibility — it is the population-level expression of a psychological truth that financial planners have known for years: sustainable financial behaviour must include positive reinforcement, not just restraint.

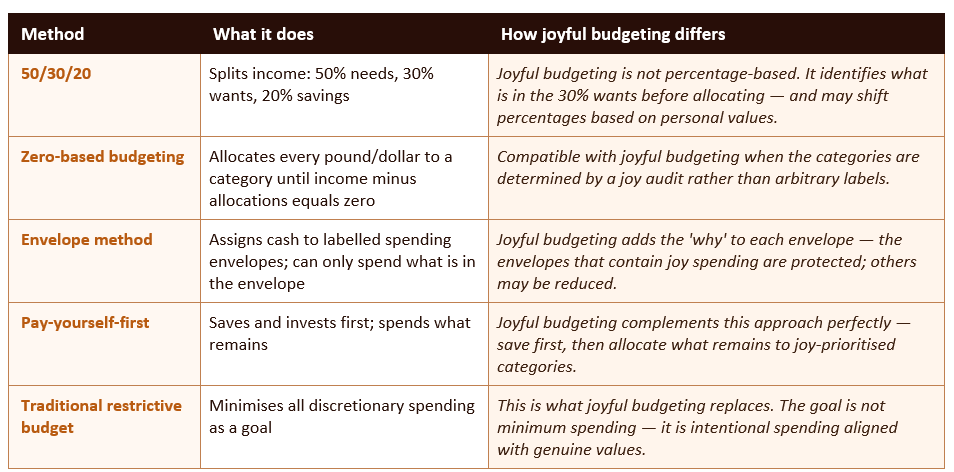

Joyful Budgeting vs Other Budget Methods

How to Build Your Joyful Budget: A Six-Step Plan

The joyful budget is built in six steps that take most people two to three hours on the first pass and twenty minutes per month to maintain. The first three steps are the foundation — discovering what actually brings you joy, what you currently spend, and which spending is aligned with your joy and which is not. The final three steps build the active budget, create your joy fund, and establish the review habit that keeps the budget working over time.Step 1 — Write Your Joy List

Before any numbers, you need one list: the things that genuinely bring you joy in your daily and annual life. Not what you think should bring you joy, not what brings other people joy, and not what you feel guilty for enjoying. What actually makes your day, your week, or your year better?Brian Ford, head of financial wellness at Truist, frames the essential question: 'One of the keys to finding happiness with money is to stop spending on stuff you don't actually care about in life.' The joy list is the answer to the inverse question: what do you actually care about? It might include specific experiences (coffee from a particular café, weekend hiking, live music), relationships (regular dinners with friends, visits to family), physical wellbeing (a gym class you genuinely enjoy, quality food), creative pursuits (art supplies, photography, writing tools), or comfort (a good mattress, quality clothing you actually wear).

Write the list without editing or judging it. Fifteen to twenty items is a good starting point. Rank them loosely from 'brings the most joy' to 'brings the least joy.' This ranked list becomes the decision-making framework for the entire budget — it determines which spending categories receive more than average allocation and which receive less or nothing.

Joy list prompts — questions to help you discover what genuinely matters to you

- When did I last feel genuinely content after spending money on something? What was it? (This reveals what already brings joy when you pay attention.)

- What would I do more of if money were no object? (This reveals desired experiences and activities that may be underfunded in your current budget.)

- What purchases have I regretted in the past six months? (This reveals the joyless spending that could be redirected.)

- What activities make me lose track of time? (This reveals genuine engagement — and the spending that enables those activities is almost always worth prioritising.)

- When I imagine myself thriving financially and personally, what does a typical week look like? (This reveals your vision of a good life — the destination your joyful budget is building toward.)

Step 2 — Complete a Spending Audit

With your joy list in hand, pull your last thirty days of bank and card statements. Categorise every transaction. The goal is not to judge what you have been spending — it is to create the data set that allows you to compare your current spending with your joy list.Most people discover one of three patterns in the audit. The first is a joy gap: the things on their joy list are underfunded — they are not actually spending on the things that matter most to them. The second is joy misalignment: money is flowing to habitual or socially influenced spending rather than the things they identified as genuinely joyful. The third is a combination: some joy-aligned spending is present but competing with a large volume of joyless automatic or habitual expenditure that has never been questioned.

Circle every transaction on the audit that corresponds directly to something on your joy list. These are your joy-aligned expenditures — the spending you want to protect and potentially increase. Everything uncircled is a candidate for reduction or elimination to fund more of what is circled. The audit is not a guilt exercise. It is data collection that reveals the gap between your current financial life and the one you actually want.

Step 3 — Separate Joy Spending from Joyless Spending

With the audit complete, create two lists from your spending categories: joy spending (things that appear on or directly enable your joy list) and joyless spending (things that do not). Joyless spending is not 'bad' spending — it includes necessary fixed costs like rent, utilities, and insurance. But it also includes the discretionary spending that is neither necessary nor joyful: the subscriptions you forgot about, the takeaways that felt automatic rather than chosen, the shopping that provided momentary distraction but no real satisfaction.Ramit Sethi's 'conscious spending' model, cited in the Nasdaq values-based budgeting analysis, captures the principle: spend lavishly on things you love and cut costs mercilessly on things you don't. The separation exercise makes this practical — it gives you a specific target for merciless cutting (the joyless spending list) and a specific home for the redirected funds (the joy spending list). The discipline is not in restricting joy spending but in ruthlessly eliminating joyless spending that is consuming the budget's capacity for the things that matter.

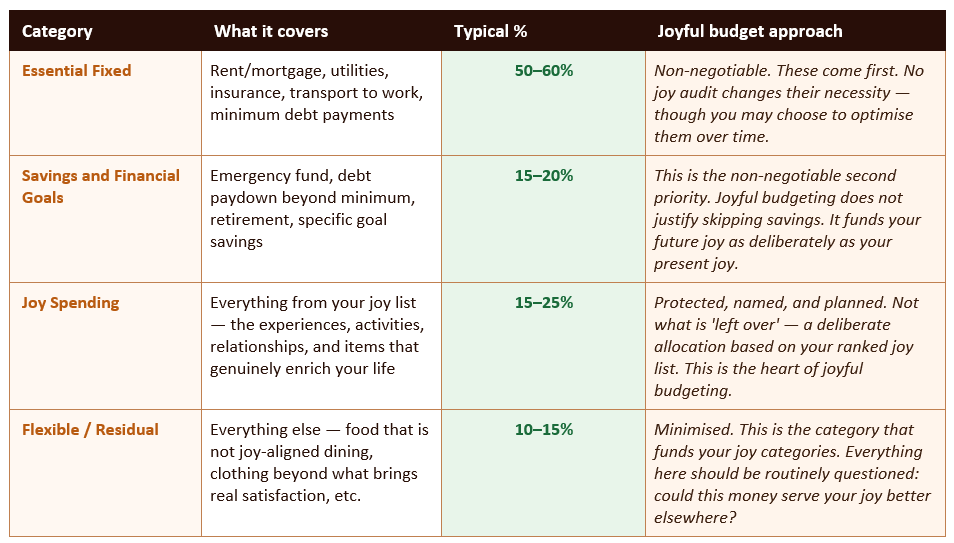

Step 4 — Build Your Joyful Budget Framework

Now build the budget using the foundation from steps one through three. The structure is simple and uses four categories rather than the dozens that make traditional budgets feel overwhelming.Step 5 — Set Your Joy Fund

The joy fund is a dedicated savings pot — separate from your emergency fund — specifically for planned future joy spending. It is the sinking fund principle applied to your joy list: instead of experiencing a concert, a trip, a piece of equipment, or a meaningful experience as a budget-busting event, you save toward it deliberately and then spend it guilt-free when it arrives.The joy fund converts aspirational spending from anxiety to anticipation. Deciding in September that you want to attend a festival in July and putting £30 per month into a named 'Festival' savings pot means arriving at the ticket-purchase moment with the money already saved, the decision already made, and zero guilt about spending it. The money was earmarked for this purpose. Spending it is not a financial failure — it is a financial success.

In practice, most joyful budgeters maintain two or three concurrent joy funds: one for a near-term experience (next month or two), one for a medium-term goal (six months to a year), and one for a larger aspiration (one to three years). Each fund has a name that reflects the actual joy it is building toward. Seeing 'Weekend Away with Friends — £120/£400 saved' in your banking app is qualitatively different from seeing 'Savings — £120' — it connects the financial discipline of saving to the specific joy it is creating.

Step 6 — Review Monthly: Does This Still Bring Joy?

Joyful budgets require one maintenance habit: a monthly review that asks one simple question about each joy allocation — 'did this bring me the joy I expected?' People change. Circumstances change. What brought genuine joy six months ago may feel stale or less compelling now. The monthly review is the mechanism that keeps the budget aligned with current values rather than past assumptions.The monthly review has four questions. First: did my joy spending last month actually bring joy, or was it habit or social obligation? Second: is there something new on my joy list that is underfunded? Third: is my savings and financial goals category on track? And fourth: are there any joyless spending categories that have crept back up that need to be cut again? The review takes fifteen to twenty minutes and prevents the most common failure mode of joyful budgeting — the gradual drift back toward habitual spending that is no longer genuinely joyful.

Intuit's January 2026 survey finding that 43% of consumers plan to adopt a balanced expense management mindset — 'consistent tracking that still leaves breathing room' — is the joyful budget in practice. The balance between financial responsibility and genuine enjoyment is not a compromise of both. It is the most sustainable financial approach available, because it is the only one that a human being can follow with genuine enthusiasm rather than grim determination.

Common Mistakes When Building a Joyful Budget

Five mistakes to avoid when building your joyful budget

- Skipping the savings and financial goals category: Joyful budgeting does not mean living only in the present. The 'while still saving consistently' element is not optional. A budget that funds present joy at the expense of future security is not joyful budgeting — it is financial avoidance. The savings category must be protected before the joy spending category is allocated, using the pay-yourself-first principle.

- Confusing habit spending with joy spending: Not everything that feels normal is actually joyful. Scrolling-to-purchase, stress-shopping, social-obligation spending, and brand loyalty that exists only through inertia are habits, not joys. They appear on the spending audit but should not appear on the joy list. Be honest in the audit: circle only what genuinely brings you life energy, not what is merely familiar.

- Making the joy budget so large it crowds out financial stability: If the joy spending category expands to fill all available discretionary income, the emergency fund goes unfunded and the debt grows. The joyful budget is a reallocation of discretionary spending, not an expansion of it. The total spending across all categories must remain within income. Joy is about where money goes within the budget, not about spending beyond it.

- Letting social comparison define the joy list: What brings you genuine joy is unique to you. If your joy list includes inexpensive things — walking in nature, cooking at home, reading, gardening — that is not a failure of aspiration. It is accurate self-knowledge. The Truist principle applies: 'One of the keys to finding happiness with money is to stop spending on stuff you don't actually care about in life.' That includes expensive things that appear on your joy list because of social comparison rather than genuine resonance.

- Reviewing too infrequently: A joyful budget that is reviewed only annually drifts. Values change, circumstances change, and what brought joy in January may feel different in October. A brief monthly check-in — fifteen to twenty minutes, four simple questions — is the maintenance habit that keeps the budget a living expression of current values rather than a static document from the past.

CONCLUSION

Joyful budgeting is not a soft alternative to real financial planning. It is the recognition that a financial plan people will actually follow for years is more powerful than a theoretically optimal plan they abandon in weeks. Intuit's January 2026 data shows that joy is now the leading driver of consumer spending at 38%. Bank of America named joy-based budgeting a top consumer financial trend for 2026. Three certified financial planners contributing to NerdWallet's April 2026 analysis agree that restrictive budgets 'fail almost every time' — and that the inclusion of joyful spending is what makes long-term financial plans work.The six steps in this guide — write your joy list, complete a spending audit, separate joy from joyless spending, build the framework, create your joy fund, and review monthly — can be completed in a Sunday afternoon. The result is a budget that still funds your emergency savings, still pays down debt, and still builds your long-term financial security — while actively making room for the experiences, relationships, and activities that make your daily life genuinely worth living. That is not a compromise between financial responsibility and personal fulfilment. It is both at once.

Frequently Asked Questions

What exactly is joyful budgeting and is it a real financial approach?

Joyful budgeting — also called joy-based budgeting or values-based budgeting — is a legitimate personal finance approach defined by NerdWallet in April 2026 as 'the practice of spending money on the things that enrich your life while still meeting your savings goals.' It was named a top consumer financial trend for 2026 by Essence magazine in partnership with Bank of America (February 2026), and is actively recommended by certified financial planners including Kaylee McClellan (CFP, Innovative Planning Group), Ashley Bleckner (CFP, San Diego), and Nick Gertsema (CFP, Saint Joseph). It is not a permission to spend without a plan — it is a reordering of how a budget is built: starting with values and joy rather than starting with restrictions, while maintaining savings and financial stability as non-negotiable foundations.Does joyful budgeting mean you can spend whatever you want on fun?

No — and this is the most important clarification about joyful budgeting. It does not mean prioritising present enjoyment over financial stability or savings. Truist's financial wellness team is explicit: 'We are not saying to prioritise your wants over your needs when building a values-based budget. Even if you don't enjoy spending money on bills or saving for emergencies and retirement — those needs must come first.' The joyful budget framework in this guide places essential fixed costs first, savings and financial goals second, and joy spending third — within the remaining budget. Joyful budgeting is about where discretionary spending goes within a financially responsible plan, not about expanding total spending beyond income.How is joyful budgeting different from just spending more on things I enjoy?

The key difference is intentionality and trade-offs. Simply spending more on enjoyment without a framework is likely to create debt, reduce savings, and ultimately undermine the financial security that makes enjoyment sustainable. Joyful budgeting explicitly requires two parallel actions: increasing spending on genuinely joy-aligned categories AND reducing spending on joyless categories by an equivalent amount. The joy list and spending audit exist specifically to identify what joyless spending can be cut to fund what is genuinely joyful. CFP Ashley Bleckner describes it as 'spending on purpose — spending intentionally.' It is not more spending. It is better-directed spending within the same financial constraints.How do I know what genuinely brings me joy versus what I just habit-spend on?

The distinction between genuine joy and habitual spending is one of the most valuable insights the joy list exercise produces. The test is simple: after the purchase or experience, did you feel genuinely enriched, satisfied, or alive — or did you feel neutral, slightly flat, or faintly regretful? Habitual spending typically produces neutrality or mild regret immediately after; genuine joy spending produces a lingering positive feeling. Nick Gertsema's Red Car Theory from NerdWallet's April 2026 analysis applies here: once you name what brings genuine joy, you start noticing it and noticing its absence more clearly. The thirty-day spending audit is the practical data-gathering tool: circle every transaction that you feel genuinely good about in retrospect. The uncircled ones are candidates for reduction.Can I use joyful budgeting if I am on a tight budget or low income?

Yes — and in some ways it is most valuable for people on tighter incomes, because the stakes of misaligned spending are higher. When every pound and dollar counts, directing discretionary spending toward genuinely joyful activities and away from habitual or socially pressured spending produces a disproportionate improvement in both financial position and wellbeing. The Essence / Bank of America February 2026 analysis notes that joy-based budgeting is catching on particularly strongly with Gen Z and lower-income consumers precisely because it provides a way to 'say yes to more plans' without spending more — by spending more intentionally. Joy does not require large amounts of money: it requires that the money you do have goes toward what actually enriches your life. A £5 activity that produces genuine joy is more valuable to your wellbeing than a £50 purchase that produces only mild satisfaction.References

NerdWallet — Joy-Based Budgeting: Does It Actually Work? (April 2026) https://www.nerdwallet.com/finance/learn/joy-based-budgetingEssence / Bank of America — Why Joy-Based Budgeting Is Becoming the New Way People Manage Money in 2026 (February 2026) https://www.essence.com/news/money-career/joy-based-budgeting-financial-trend/

Intuit — 2026 Financial Forecast: Staying Mindful Amid Money Stress (January 2026) https://www.intuit.com/blog/innovative-thinking/2026-financial-forecast-mindful-stress/

Truist — Building a Values-Based Budget: How to Spend Mindfully https://www.truist.com/money-mindset/principles/budgeting-by-values/building-a-values-based-budget

Nasdaq / GOBankingRates — 3 Signs a Values-Based Budget Is Best for Your Money (Ramit Sethi conscious spending) https://www.nasdaq.com/articles/3-signs-values-based-budget-best-your-money

CNBC Select — 5 Best Free Budgeting Tools of 2026 (April 2026) https://www.cnbc.com/select/best-free-budgeting-tools/

Ramsey Solutions — The State of Personal Finance in America Q4 2025 (February 2026) https://www.ramseysolutions.com/budgeting/state-of-personal-finance

Monarch Money — Financial Resolutions for 2026: Tips to Achieve Your Money Goals (February 2026) https://www.monarch.com/blog/personal-finance/financial-resolutions

MoneyHelper (UK) — How to Create a Budget: Official Free Guidance https://www.moneyhelper.org.uk/en/money-troubles/way-forward/how-to-create-a-budget

0 Comments Comments