Insurance

What Is Travel Insurance? UK Complete Guide

Table of Contents

- Why Travel Insurance Matters

- What Is Travel Insurance?

- What Does Travel Insurance Cover?

- What Travel Insurance Does NOT Cover: Key Exclusions

- The GHIC and Travel Insurance: Why You Need Both

- Types of Travel Insurance: Which Policy Is Right for You?

- Single-Trip Insurance

- Annual Multi-Trip Insurance

- Backpacker and Long-Stay Insurance

- Specialist Policies: Cruise, Winter Sports, and Business

- How Much Does Travel Insurance Cost in 2026?

- How to Find and Buy the Best Travel Insurance

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why Travel Insurance Matters

Travel insurance is one of the most straightforward and most consistently undervalued financial products available to UK holidaymakers. In 2024, the Association of British Insurers (ABI) estimates that insurers paid out £472 million to UK travellers across more than 500,000 claims — covering medical emergencies, cancelled trips, lost luggage, travel delays, and a range of other unexpected events that can turn a holiday into a financial disaster without adequate protection. The average emergency medical treatment claim paid in 2024 was £1,528. But medical bills abroad can reach tens of thousands of pounds for serious illness, surgery, or repatriation — costs that no savings account is typically prepared for.Despite this, many UK travellers either do not buy travel insurance at all or buy it as an afterthought at the airport — the most expensive and often least well-considered point in the buying process. Money Saving Expert founder Martin Lewis has repeatedly recommended buying travel insurance 'as soon as you book' (ASAB), not because it is required but because the trip cancellation protection it provides starts the moment you purchase the policy, not the moment you depart. Book a holiday in January for a June trip, develop a health issue in March that prevents you from going, and only the traveller who bought insurance in January — not the one who planned to buy it at the airport in June — will be covered for the cancellation cost.

This guide answers every core question about travel insurance for UK travellers in 2026: what it is, what it covers, what it does not cover, how much it costs across every major policy type and destination, what the difference between single-trip and annual policies is, how pre-existing medical conditions are handled, what the GHIC does and does not replace, and how to find the best policy for your specific trip. Whether you are planning a weekend in Paris, a family fortnight in the Caribbean, or a long-haul adventure, this guide provides everything you need to travel with genuine financial protection.

What Is Travel Insurance?

Travel insurance is a type of insurance policy that protects you against financial losses arising from unexpected events before, during, and in some cases after a trip. It is sold by insurance companies, comparison sites, banks, travel companies, and specialist brokers, and is available for individual trips (single-trip policies), for an entire year of travel (annual multi-trip policies), and for specialist situations such as long-stay backpacker travel, cruise holidays, or winter sports.Unlike car or home insurance, travel insurance is not a legal requirement in the UK — but it is widely considered a financial necessity for anyone travelling abroad, and many travel companies, package holiday operators, and cruise lines recommend or require it as a condition of booking. The Financial Conduct Authority (FCA) regulates travel insurance in the UK, which means that all policies sold must meet defined standards, and that you have access to the Financial Ombudsman Service if a claim is handled unfairly.

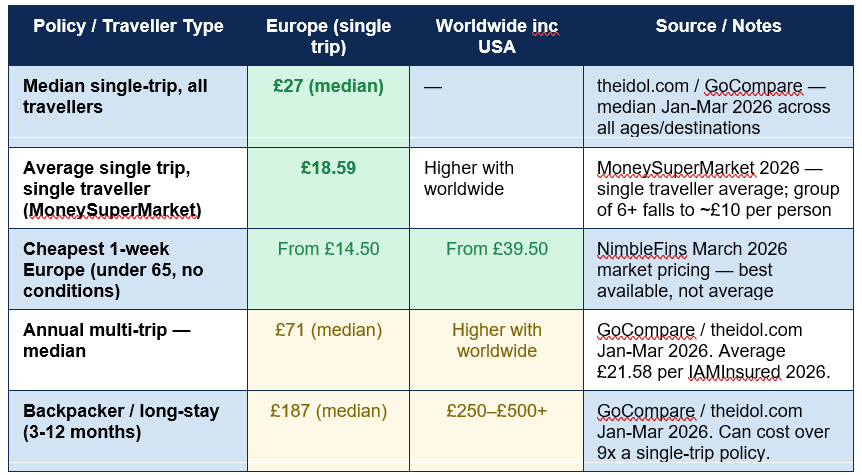

The core function of travel insurance is financial protection against losses you cannot prevent and cannot easily afford. The cost of an adequate travel insurance policy is typically a small fraction of the cost of the trip it is protecting — and a vanishingly small fraction of the cost of a serious medical emergency abroad. Go.Compare's June 2026 data, sourcing from theidol.com, shows the median single-trip travel insurance policy cost £27 for policies bought between January and March 2026. A standard week in hospital in the US without insurance can cost tens of thousands of dollars. This arithmetic is the entire argument for travel insurance.

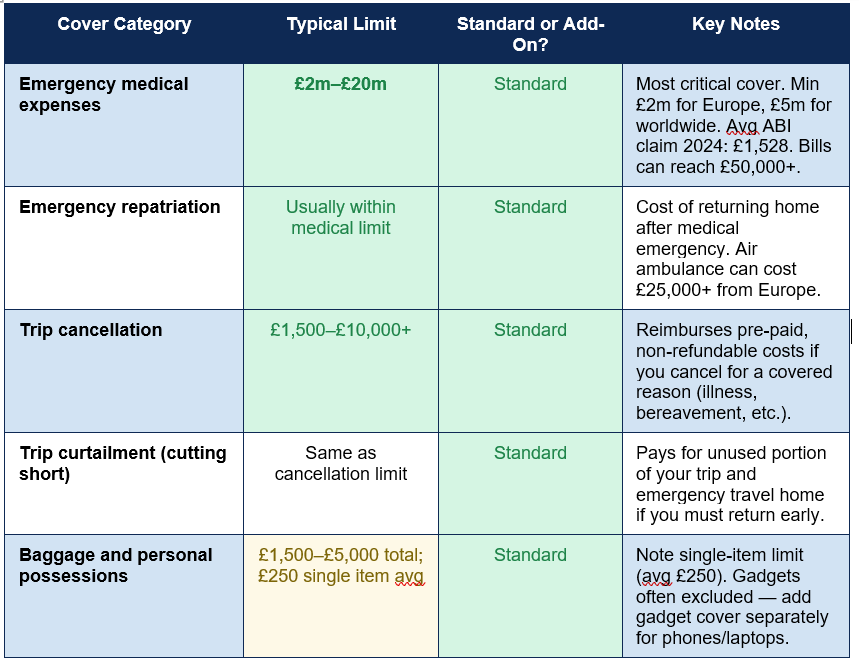

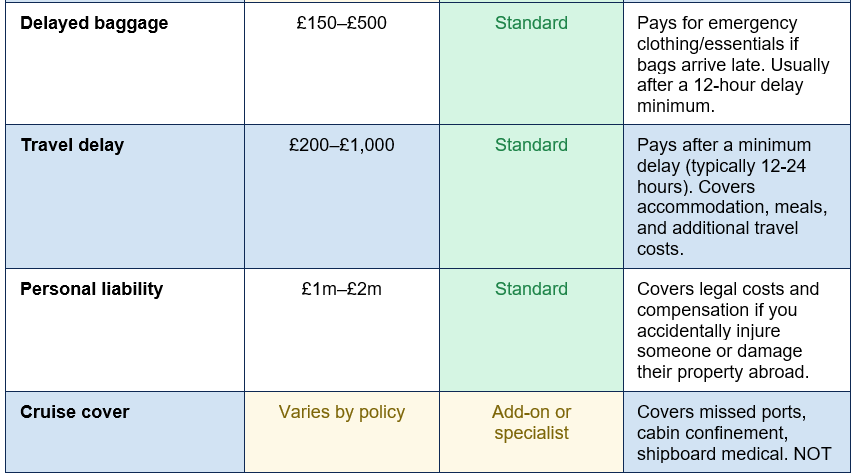

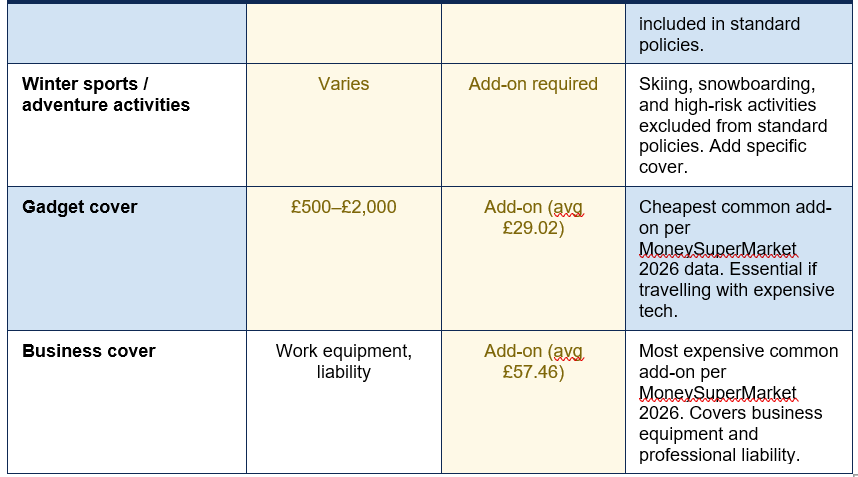

What Does Travel Insurance Cover?

A standard comprehensive travel insurance policy in 2026 typically covers the following categories, though limits and specific terms vary significantly between providers. The table below maps each major cover category to its typical limit, whether it is standard or requires an add-on, and key notes for UK travellers:

The industry claim payout in 2024: £472 million paid out across 500,000+ claims by UK insurers — the Association of British Insurers' 2024 data on travel insurance claims represents a 12% increase from the prior year, driven by rising trip costs, medical inflation abroad, and higher volume of international travel post-pandemic. The average emergency medical claim was £1,528 — but complex cases involving surgery, intensive care, and repatriation can run to £50,000 or more (ABI / GoCompare June 2026).

What Travel Insurance Does NOT Cover: Key Exclusions

Understanding what travel insurance does not cover is just as important as knowing what it does. The most common exclusions that catch UK travellers out are:- Pre-existing medical conditions not declared: Any condition for which you have received treatment, taken medication, or sought medical advice must be declared during the medical screening process. Failing to disclose a relevant condition — even one you do not think is significant — can invalidate your entire policy. The insurer may not only reject a claim related to that condition but decline all claims arising from the trip.

- Travel against FCDO advice: The Foreign, Commonwealth and Development Office (FCDO) issues travel advice for every country. If you travel to a destination where the FCDO advises against all but essential travel or against all travel, your policy will typically be invalidated. Always check fcdo.gov.uk before booking and before travelling. Confused.com noted in July 2026 that recent conflicts have disrupted some flight routes and raised specific policy questions around Middle East travel.

- Activities not covered by your policy: Many standard policies exclude high-risk activities — bungee jumping, skydiving, certain watersports, quad biking, and in some cases even skiing. If you plan to do anything adventurous, check your policy's activity list and add the relevant cover before travelling.

- Alcohol and substance-related incidents: If you are injured or incur losses while intoxicated, most policies will not cover the claim. This applies to both medical claims and personal liability.

- Valuables above single-item limits: The average single-item limit on baggage cover is £250 according to Confused.com's 2026 review of 46 insurers. Expensive jewellery, designer items, laptops, cameras, and phones often exceed this limit and may require specialist gadget or valuables add-ons.

- Losses from unattended baggage: If you leave a bag unattended and it is stolen, most policies will not pay. Personal possessions must be within your direct sight or secured to be covered under most standard policies.

- Coronavirus and pandemic exclusions: Many standard policies include limited or no cover for COVID-19-related cancellations. Check the specific terms of any policy if pandemic-related disruption is a concern for your trip.

The FCDO travel advice rule — one you cannot afford to miss: Every travel insurance policy in the UK contains a condition that cover is void if you travel against FCDO advice. This is not a technicality buried in small print — it is enforced consistently by insurers and upheld by the Financial Ombudsman Service. Check fcdo.gov.uk before you book, and check again before you travel. If advice changes for your destination after you have booked and paid for your trip, check with your insurer immediately about whether you are covered and what options you have.

The GHIC and Travel Insurance: Why You Need Both

The Global Health Insurance Card (GHIC) replaced the EHIC for UK citizens after Brexit and entitles holders to the same standard of state-funded healthcare as residents in EU countries and some other participating nations. It is free to obtain from the NHS at nhscard.co.uk, is valid for up to five years, and is a useful document to carry alongside your travel insurance. It is not, however, a replacement for travel insurance.The GHIC has significant limitations that make relying on it alone a serious financial risk. It does not cover emergency repatriation — the cost of flying you home after a medical emergency. It does not cover private hospital treatment — which in many EU countries is where you would receive English-speaking doctors and faster care. It provides no cover at all outside the EU and participating countries — meaning it is completely useless in the USA, Canada, Australia, most of Asia, and the Caribbean. And it covers none of the other travel insurance benefits: trip cancellation, baggage loss, personal liability, or travel delay.

The correct approach is to carry both. A valid GHIC reduces the amount your travel insurance needs to pay for basic state-funded medical care in EU countries, which can reduce your premium. But the GHIC is a supplement to travel insurance, not a substitute for it. Squaremouth's 2026 data on travel to the UK specifically notes that US health insurance is typically not accepted by UK providers, and NHS services are not free for international visitors — the same principle applies in reverse when UK citizens travel abroad.

Types of Travel Insurance: Which Policy Is Right for You?

Single-Trip Insurance

A single-trip policy covers one specific holiday or journey, from the date you leave home to the date you return. It is the most appropriate choice for someone who travels once or twice a year or who is taking a particularly long or high-value trip where the policy parameters need to match that specific journey precisely. Single-trip policies are often the cheapest option for any individual trip, with the median cost of £27 across all traveller ages (January-March 2026 data) and prices starting from £14.50 for a 30-year-old in good health travelling to Europe for a week.Annual Multi-Trip Insurance

An annual multi-trip policy covers an unlimited number of trips within a 12-month period, subject to a maximum duration per individual trip (commonly 30 or 31 days per trip). NimbleFins's March 2026 research found that annual multi-trip policies can often be cheaper than buying cover for a single trip if you travel more than once in the year. The annual median premium was £71 in early 2026, compared to £27 for a single trip — meaning two trips in a year already tips the economics in favour of annual cover. Annual policies also provide continuous protection: you are covered for cancellation from the moment the policy starts, for every trip you book throughout the year.Backpacker and Long-Stay Insurance

Long-stay or backpacker policies cover travellers who are away for months rather than weeks — gap year students, digital nomads, or those undertaking extended overseas work. Premiums are higher because the duration of exposure is much greater, but the per-day cost is typically lower than buying multiple single-trip policies for the same period. The median cost for backpacker policies was £187 in early 2026, per GoCompare data — though policies covering a full year worldwide can reach several hundred pounds more. These policies often include return flights if you are hospitalised for an extended period and need to return home for continuing treatment.Specialist Policies: Cruise, Winter Sports, and Business

Several categories of travel require specialist cover that is not provided as standard on most policies. Cruise travel insurance covers risks specific to sea voyages: onboard medical treatment, missed port departures, cabin confinement (payment if illness confines you to your cabin for multiple days), and itinerary changes. Standard policies typically exclude or minimise these elements, making dedicated cruise cover essential for anyone taking a sea voyage. Winter sports insurance extends standard cover to include skiing, snowboarding, and related activities, plus piste closure and avalanche delay cover. Business travel insurance extends to cover work equipment, professional liability, and business interruption.BUY AS SOON AS YOU BOOK (ASAB): Martin Lewis of MoneySavingExpert consistently recommends buying travel insurance on the same day you book your holiday, not just before you travel. Trip cancellation cover starts from the day you purchase the policy — meaning if you become ill or have a family emergency between booking and travel, only policyholders who bought insurance at the time of booking are covered for the cancellation costs. Waiting until you arrive at the airport gives you no protection for the months between booking and travel.

How Much Does Travel Insurance Cost in 2026?

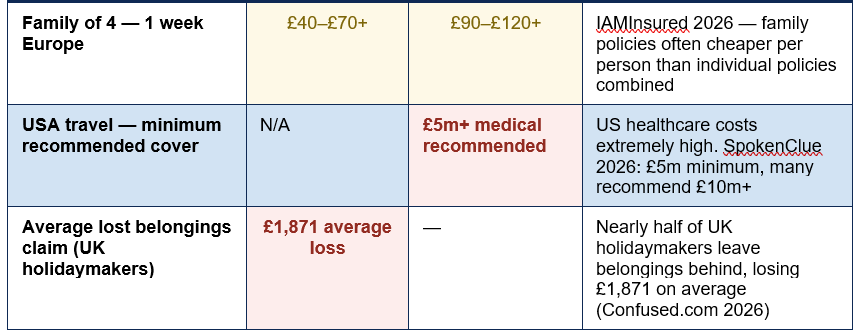

Travel insurance premiums in 2026 vary widely based on your age, destination, trip duration, the policy type, whether you have pre-existing medical conditions, and the cover level you choose. The table below provides a comprehensive cost reference for the most common UK traveller scenarios, sourced from NimbleFins (March 2026), MoneySuperMarket (May 2026), GoCompare/theidol.com (Jan-Mar 2026), IAMInsured (April 2026), and SpokenClue (2026):

Several important patterns in the cost data are worth understanding before you compare quotes. First, MoneySuperMarket's 2026 statistics show that as group size increases, the per-person cost falls — a single traveller pays an average of £18.59, while a group of six or more can pay as little as £10 per person on a group policy. Second, long-stay and backpacker policies can cost over nine times more than a basic single-trip policy, reflecting the extended exposure period. Third, US travel significantly increases premiums due to the high cost of American healthcare — always specify your destination when comparing.

How to Find and Buy the Best Travel Insurance

The practical process for finding the best travel insurance policy in 2026 follows a clear sequence that applies equally to first-time buyers and experienced travellers:- Decide on single-trip or annual cover: If you are taking one holiday this year, single-trip is usually cheapest. If you are taking two or more, compare annual prices — annual can be cheaper than two single trips combined even before the convenience factor is considered.

- Use a comparison site first: MoneySuperMarket, Compare the Market, GoCompare, and Confused.com all compare dozens of providers simultaneously. Run quotes on at least two comparison sites, as not every insurer appears on every platform.

- Complete the medical screening honestly: If you or any traveller on the policy has a pre-existing medical condition, declare it fully and accurately during the screening process. Non-disclosure can invalidate the entire policy, not just the related claim.

- Check the policy limits, not just the price: The cheapest policy is not always the best value. Check the medical cover limit (minimum £2 million for Europe, £5 million for worldwide), the cancellation limit relative to your trip cost, and the single-item baggage limit.

- Add the cover you need: If you are cruising, add cruise cover. If you are skiing, add winter sports. If you are travelling with expensive gadgets, add gadget cover. Adding these costs far less than finding you are not covered when you need to claim.

- Check the FCDO advice: Before purchasing and before travelling, check fcdo.gov.uk for your destination. If advice changes between booking and travel, contact your insurer immediately.

- Store your policy documents accessibly: Save digital and paper copies of your policy, including the emergency assistance number. Keep them easily accessible during your trip — not buried in email. You may need to call your insurer's emergency line at short notice.

Conclusion

Travel insurance is a simple product that does a straightforward job: it protects you against financial losses from events you cannot predict and cannot easily afford. The ABI paid out £472 million in travel insurance claims in 2024, across more than 500,000 claims — a figure that represents hundreds of thousands of UK travellers whose holidays went wrong in ways that would have been financially catastrophic without cover. The average emergency medical claim was £1,528, but serious incidents — surgery, intensive care, repatriation — routinely generate bills of £10,000 to £50,000 or more, costs that dwarf any travel insurance premium many times over.In 2026, a week's single-trip European travel insurance starts from £14.50 for a healthy traveller in their thirties. An annual multi-trip policy that covers every trip you take for a year costs a median of £71. These are not significant sums relative to the cost of a typical holiday — or relative to what they protect against. Yet many travellers skip them, delay buying them, or buy the cheapest possible option without reading what it actually covers. The advice in this guide, condensed to its most essential points: buy as soon as you book, declare all conditions honestly, compare on cover limits not just price, and always check FCDO advice.

Travel is one of life's great pleasures. Travel insurance is what allows that pleasure to remain unclouded by the financial anxiety of what might go wrong. At the prices available in 2026, it is among the most cost-efficient forms of protection any UK traveller can buy.

Frequently Asked Questions (FAQ)

What does travel insurance cover?

A standard comprehensive travel insurance policy in the UK covers emergency medical expenses abroad (including repatriation), trip cancellation before departure, trip curtailment (cutting a trip short), lost, stolen, or delayed baggage, travel delays, and personal liability if you accidentally injure someone or damage property. Most standard policies do not cover cruise-specific risks, winter sports, high-risk adventure activities, or business equipment — these require specific add-ons. Gadget cover (for phones, laptops, and cameras) is typically available as an add-on for an average of £29.02 per policy according to MoneySuperMarket's 2026 data, as standard baggage cover usually has a single-item limit averaging only £250.How much does travel insurance cost in the UK in 2026?

The median single-trip travel insurance policy cost £27 according to theidol.com data compiled by GoCompare for policies bought between January and March 2026. Prices start from around £14.50 for a week in Europe for a healthy traveller under 65, according to NimbleFins's March 2026 market research. Annual multi-trip policies cost a median of £71. The average single traveller paid £18.59, while group policies of six or more can fall as low as £10 per person. Cost is heavily influenced by age, destination (USA/worldwide costs significantly more), pre-existing medical conditions, and the cover level selected. Always compare quotes from multiple providers.Is the GHIC a replacement for travel insurance?

No. The Global Health Insurance Card (GHIC) entitles UK citizens to the same standard of state-funded healthcare as local residents in EU countries and some other participating nations — but it does not cover emergency repatriation, private hospital treatment, medical care outside the EU, or any non-medical travel insurance benefits (trip cancellation, baggage, personal liability, travel delay). The GHIC should be carried alongside travel insurance, not instead of it. It is free to obtain from the NHS at nhscard.co.uk, remains valid for up to five years, and can reduce the portion of a medical claim charged to your insurer in EU countries — but it is a complement to travel insurance, not a substitute.When should I buy travel insurance?

As soon as you book your holiday — this is the consistent advice from Martin Lewis and other UK consumer finance experts, expressed as the 'ASAB' (As Soon As You Book) principle. Trip cancellation cover begins the moment you purchase the policy, not the moment you travel. If you book a June trip in January and develop a serious health condition in March, only a traveller who bought insurance in January is covered for the cost of cancelling. Waiting until you pack your bags or arrive at the airport gives you protection for the journey itself but none of the months between booking and travel during which cancellation risks are very real. The price is not higher when you buy early.Do I need to declare pre-existing medical conditions?

Yes — always, and completely. Every pre-existing medical condition must be declared during the insurance application's medical screening process. A pre-existing condition is any illness, injury, or health issue for which you have received treatment, taken prescribed medication, or sought medical advice, typically within the past 12 to 24 months, though some policies look further back. Failing to declare a relevant condition — including one you consider minor or well-controlled — can invalidate your entire travel insurance policy, not just any claim related to that condition. If your conditions result in declined applications or very high premiums from mainstream insurers, the MoneyHelper Travel Insurance Directory and the British Insurance Brokers' Association can refer you to specialist providers.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. GoCompare — Travel Insurance Statistics and Facts (Updated June 2026)

https://www.gocompare.com/travel-insurance/

2. MoneySuperMarket — Travel Insurance Facts, Trends and Statistics 2026

https://www.moneysupermarket.com/travel-insurance/travel-insurance-statistics/

3. NimbleFins — How Much Does Travel Insurance Cost UK 2026? (March 2026)

https://www.nimblefins.co.uk/average-cost-travel-insurance

4. IAMInsured — Average Cost of Travel Insurance UK 2026 (April 2026)

https://iaminsured.co.uk/travel-insurance/guides/average-cost-of-travel-insurance-uk/

5. Confused.com — Travel Insurance Comparison (May 2026 data)

https://www.confused.com/travel-insurance

6. MoneyHelper — Travel Insurance for Medical Conditions Directory

https://www.moneyhelper.org.uk/en/everyday-money/insurance/travel-insurance-for-over-65s-and-medical-conditions

7. NHS — Get a UK Global Health Insurance Card (GHIC)

https://www.nhs.uk/using-the-nhs/healthcare-abroad/apply-for-a-free-uk-global-health-insurance-card-ghic/

8. FCDO — Foreign Travel Advice (Check Before You Travel)

https://www.gov.uk/foreign-travel-advice

0 Comments Comments