Retirement

Why Millions of Britons Are Not Saving for Retirement

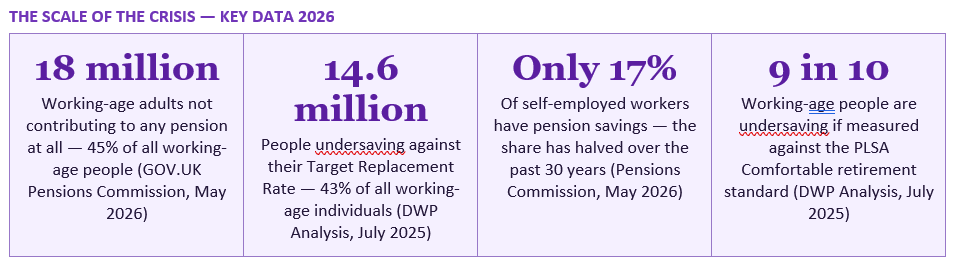

Forty-five per cent of working-age adults in Britain — approximately 18 million people — are not contributing to a pension at all, despite nearly half of them being in paid work. A new Pensions Commission, established by the Government in July 2025, has sounded the alarm in stark terms: without reform, millions of future retirees will be worse off than today's pensioners. This is not a fringe problem. It is a systemic crisis that the data shows is deepening in 2026.

In July 2025, the UK Government established a new Pensions Commission — only the second in British history — to examine why so many working-age Britons are not saving adequately for retirement and to make recommendations for reform. The first Commission, which reported between 2002 and 2006, produced the auto-enrolment system that has since enrolled 11.4 million additional workers who would otherwise have had no pension savings at all. The new Commission has been established because auto-enrolment, despite its success, has not solved the underlying problem.

The Commission's early findings, published in May 2026, are sobering. GOV.UK's official statement confirms: '45% of working-age adults — around 18 million people — are not saving into a pension at all, despite nearly half of them being in work. Where employers are contributing about the statutory minimum, this is largely benefiting higher earners. Low and middle earners are most at risk, with around half saving only at minimum auto-enrolment levels with little else to fall back on.'

GB News' May 2026 coverage of the Commission's findings reports the self-employed dimension in stark terms: 'When including all self-employed workers with mixed sources of income, the proportion with pension savings rises to only 17 per cent.' Sir Ian, cited in GB News' reporting, noted: 'The degree of the issue on self-employed is much starker than we would have thought.' The Commission, led by Jeannie Drake, warns that without reform, many future retirees could be worse off than today's pensioners — a deeply alarming reversal of the multigenerational progress that has defined British retirement security since the post-war settlement.

45% of working-age adults — around 18 million people — are not saving into a pension at all, despite nearly half of them being in work. Without reform, many future retirees risk being worse off than today's pensioners.

— GOV.UK — BRITAIN IS UNDERSAVING FOR RETIREMENT WARNS PENSIONS COMMISSION (MAY 2026)

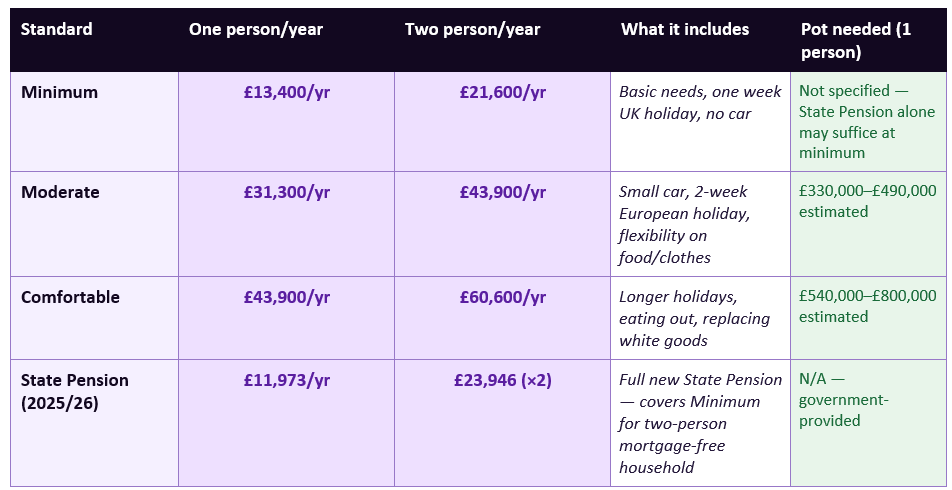

Sources: PLSA Retirement Living Standards 2025, Rest Less (May 2026). Pot estimates assume annuity purchase. Figures for mortgage-free households outside London. London adds £1,300–£3,200 per year. The DWP's 2025 analysis found that 9 in 10 working-age people are undersaving for the Comfortable standard, and 3 in 4 for the Moderate standard.

The Comfortable standard at £43,900 per year for a single person requires a private pension pot of £540,000 to £800,000 on top of the State Pension. Rest Less' May 2026 analysis confirms that on top of their State Pension, a single person seeking Comfortable retirement needs additional annual income of approximately £40,245, requiring a pension pot in that range. For most people on average UK earnings, this figure represents more than fifteen to twenty years of total gross salary — a gap that the current auto-enrolment minimum contribution of 8% of qualifying earnings will not, for most people, come close to filling.

But success in getting people into pensions is not the same as success in getting people to save enough. The minimum auto-enrolment contribution is 8% of qualifying earnings — 5% from the employee and 3% from the employer. The CSPA's May 2026 summary of the Pensions Commission's findings is explicit: 'Around half of those who are saving are doing so only at the minimum level required under automatic enrolment rules, leaving them with limited financial resilience in later life. The Commission suggests that this level is insufficient for many people to achieve a comfortable retirement.'

The design of auto-enrolment also limits its effectiveness for lower earners in a specific way. Contributions are calculated on 'qualifying earnings' — currently the band between £6,240 and £50,270 per year. Earnings below the £6,240 threshold are excluded from the calculation, meaning that a part-time worker earning £14,000 per year has their 8% contributions calculated only on £7,760 (£14,000 minus £6,240), producing an annual employer-employee contribution of approximately £621 rather than the £1,120 that would result from calculating on the full £14,000. This threshold design disproportionately disadvantages lower earners — the very group who have fewest alternative means of retirement provision.

The Pensions Commission's May 2026 findings, reported by GB News, show that only 17% of self-employed workers with mixed income sources have any pension savings — and the share of self-employed people contributing to a pension has halved over the past 30 years. Britain currently has nearly three million full-time self-employed workers, according to House of Commons Library research published in February 2026 — approximately one in eight full-time workers. The vast majority are on track for retirement income significantly below any of the PLSA's three living standards.

Sophia Singleton, head of defined contribution pension schemes at consultants XPS, summarised the structural gap clearly in the GB News May 2026 report: 'There is an obvious hole in policy relating to the self-employed given the absence of auto-enrolment as a mechanism to save.' Self-employed people can contribute to a SIPP (Self-Invested Personal Pension) or personal pension and receive basic rate tax relief on contributions — but without the auto-enrolment inertia mechanism or employer contribution, take-up remains dramatically lower than among employees.

The same Standard Life research found that 53% of UK adults worry they are not saving enough for retirement. Despite this worry, only 15% have pension saving as one of their top financial priorities for the year. The gap between worry and action is not complacency — it is the product of real financial constraint. When food, energy, housing, and childcare costs absorb the majority of a household's income, the rational response under financial pressure is to reduce or stop discretionary contributions beyond the auto-enrolment minimum. Pension contributions above the minimum are, for many employees, the largest single expenditure that feels genuinely reducible.

The Investors Centre's 2026 pension statistics analysis notes that pension tax relief costs the government £59.1 billion in 2025/26 — but that 55% of income tax relief goes to higher rate taxpayers. The system is structurally generous to those who can afford to save more and less effective for those who need more support to save at all.

The CSPA's May 2026 summary of the Pensions Commission's findings documents the scale of premature drawdown: 'Around 30% of private pension pots are drawn down at the earliest opportunity, with approximately half of those accessed being withdrawn in full. Nearly half of this money is spent on large purchases such as cars, holidays, or home improvements, rather than being preserved for long-term income.'

This behaviour is economically rational from the individual's short-term perspective but catastrophically damaging to their long-term retirement income. A pension pot accessed at 55 and spent over the following two to five years leaves the individual with no private pension income for the potentially 25 to 35 remaining years of their life — dependent entirely on the State Pension, which at £11,973 per year provides only the bare minimum standard of retirement living. The pension freedom reforms, while well-intentioned, created a structural vulnerability that the current Commission is examining closely.

The CSPA's May 2026 summary of the Pensions Commission's findings is unambiguous: 'Women approaching retirement have, on average, about half the private pension wealth of men. Median pension savings stand at around £81,000 for women compared to £156,000 for men.' The Investors Centre's 2026 pension statistics elaborate on the structural drivers: 'The UK gender pension gap is driven by the gender pay gap, career breaks for childcare or caring responsibilities, higher rates of part-time working among women, and occupational segregation into lower-earning sectors. Women face an average 10-year career gap costing approximately £39,000 in lost pension savings.'

The auto-enrolment system's lower earnings threshold of £6,240 per year particularly disadvantages women, who are significantly more likely than men to earn below this threshold through part-time or intermittent work. When pension contributions are calculated only on earnings above the threshold, the effective contribution rate for a woman working part-time across multiple lower-earning roles may be substantially below the nominal 8% — and she will also receive a lower employer contribution than a full-time worker on the same hourly rate.

Auto-enrolment harnesses inertia productively — by making the default position 'saving' rather than 'not saving,' it has enrolled millions who would never have taken active steps. But the same inertia that keeps people enrolled at the minimum rate also keeps them from increasing contributions when their income rises, combining pensions from multiple employers into a consolidated pot, or engaging with the value of their accumulated savings to assess whether they are on track for their target retirement income.

The Investors Centre's 2026 statistics cite the Wharton School: 'Research published by the Wharton School of the University of Pennsylvania found that 57% of older Americans regret not saving more for retirement.' The parallel finding in the UK context is Standard Life's 2025 data showing 53% of UK adults already worry they are not saving enough — which suggests widespread awareness of the problem but insufficient translation of that awareness into action. The challenge is not primarily education. It is the structural and financial barriers that prevent awareness from converting into behaviour change.

Standard Life's 2025 Retirement Voice report reveals a widening expectation gap: UK adults' preferred retirement age is 62, but their expected actual retirement age has risen to 67 — up from 66 in 2024. The gap between desired and expected retirement age grew by a full year in a single year, reflecting the creeping recognition that the pension savings needed to retire at 62 are beyond what most people are on track to accumulate. For some, this will translate into working longer. For others, it will mean a lower standard of living in retirement than they have planned for.

The DWP's Analysis of Future Pension Incomes 2025 provides the most granular picture of the expected adequacy gap. The analysis found that 43% of working-age individuals are undersaving against their Target Replacement Rate — the income level required to maintain a reasonable approximation of their pre-retirement standard of living. When measured against the PLSA standards rather than the TRR: 13% will fall below even the Minimum standard; 73% will fall below the Moderate standard; and 91% will fall below the Comfortable standard. On current savings trajectories, only one in ten working-age Britons is on track for a comfortable retirement.

But structural reform takes time, and the retirement of people currently in their thirties, forties, and fifties does not. The eight individual actions in Section 10 of this guide are available now, to anyone, regardless of where the policy debate lands. Find your pension pots. Increase contributions by 1%. Claim your tax relief. Check your State Pension forecast. Open a SIPP if you are self-employed. The gap between the retirement most Britons want and the retirement most are on track for is real and large — but it is not yet fixed. For those who act in the next decade, it is still closable.

CSPA — Millions of Britons Not Saving Enough for Retirement (May 2026) https://www.cspa.co.uk/news/millions-of-britons-not-saving-enough-for-retirement/

GB News — Pensions Crisis Deepens as Millions Not Saving Enough (May 2026) https://www.gbnews.com/money/pensions-crisis-deepens-as-millions-not-saving-enough

The Investors Centre — UK Pension Statistics 2026: Key Data and Trends (2026) https://www.theinvestorscentre.co.uk/investing/statistics/pension/

GOV.UK / DWP — Analysis of Future Pension Incomes 2025 (July 2025) https://www.gov.uk/government/statistics/analysis-of-future-pension-incomes-2025/analysis-of-future-pension-incomes-2025

Rest Less — How Much Do You Need to Retire Comfortably in 2026? (May 2026) https://restless.co.uk/pensions-retirement-planning/approaching-retirement/how-much-to-retire-comfortably/

PLSA — Retirement Living Standards 2025: Official Update https://www.retirementlivingstandards.org.uk/library/2025-rls-update

Pensions Age — Majority of UK Adults Worry About Retirement Savings Yet Few Prioritise Pensions (October 2025) https://www.pensionsage.com/pa/Majority-of-UK-adults-worry-about-retirement-savings-yet-few-prioritise-pensions.php

Saltus — Recalibrating Retirement: The PLSA's Retirement Standards 2025/26 (July 2025) https://www.saltus.co.uk/the-financial-planning-blog/recalibrating-retirement

TABLE OF CONTENTS

- The Alarm Has Been Sounded: The New Pensions Commission 2026

- How Much Do You Actually Need to Retire? The PLSA Standards

- Reason 1: The Auto-Enrolment Floor Is Too Low

- Reason 2: The Self-Employed Are Almost Entirely Left Out

- Reason 3: The Cost-of-Living Squeeze Has Crowded Out Pension Saving

- Reason 4: Pension Pots Are Being Raided Too Early

- Reason 5: The Gender Pension Gap Is Structural and Growing

- Reason 6: Low Awareness and Pension Inertia

- Reason 7: The Expectation Gap Is Widening

- What Should You Do? The Individual Action Plan

- Conclusion

- Frequently Asked Questions

- References

The Alarm Has Been Sounded: The New Pensions Commission 2026

In July 2025, the UK Government established a new Pensions Commission — only the second in British history — to examine why so many working-age Britons are not saving adequately for retirement and to make recommendations for reform. The first Commission, which reported between 2002 and 2006, produced the auto-enrolment system that has since enrolled 11.4 million additional workers who would otherwise have had no pension savings at all. The new Commission has been established because auto-enrolment, despite its success, has not solved the underlying problem.The Commission's early findings, published in May 2026, are sobering. GOV.UK's official statement confirms: '45% of working-age adults — around 18 million people — are not saving into a pension at all, despite nearly half of them being in work. Where employers are contributing about the statutory minimum, this is largely benefiting higher earners. Low and middle earners are most at risk, with around half saving only at minimum auto-enrolment levels with little else to fall back on.'

GB News' May 2026 coverage of the Commission's findings reports the self-employed dimension in stark terms: 'When including all self-employed workers with mixed sources of income, the proportion with pension savings rises to only 17 per cent.' Sir Ian, cited in GB News' reporting, noted: 'The degree of the issue on self-employed is much starker than we would have thought.' The Commission, led by Jeannie Drake, warns that without reform, many future retirees could be worse off than today's pensioners — a deeply alarming reversal of the multigenerational progress that has defined British retirement security since the post-war settlement.

45% of working-age adults — around 18 million people — are not saving into a pension at all, despite nearly half of them being in work. Without reform, many future retirees risk being worse off than today's pensioners.

— GOV.UK — BRITAIN IS UNDERSAVING FOR RETIREMENT WARNS PENSIONS COMMISSION (MAY 2026)

How Much Do You Actually Need to Retire? The PLSA Standards

Before examining why people are undersaving, it is worth establishing what adequate saving actually means. The Pensions and Lifetime Savings Association (PLSA), in partnership with Loughborough University's Centre for Research in Social Policy, publishes annual Retirement Living Standards — the most widely cited benchmark for UK retirement adequacy. The 2025 update sets out three tiers.Sources: PLSA Retirement Living Standards 2025, Rest Less (May 2026). Pot estimates assume annuity purchase. Figures for mortgage-free households outside London. London adds £1,300–£3,200 per year. The DWP's 2025 analysis found that 9 in 10 working-age people are undersaving for the Comfortable standard, and 3 in 4 for the Moderate standard.

The Comfortable standard at £43,900 per year for a single person requires a private pension pot of £540,000 to £800,000 on top of the State Pension. Rest Less' May 2026 analysis confirms that on top of their State Pension, a single person seeking Comfortable retirement needs additional annual income of approximately £40,245, requiring a pension pot in that range. For most people on average UK earnings, this figure represents more than fifteen to twenty years of total gross salary — a gap that the current auto-enrolment minimum contribution of 8% of qualifying earnings will not, for most people, come close to filling.

Reason 1: The Auto-Enrolment Floor Is Too Low

Auto-enrolment has been the single most successful pension policy reform in British history. The Investors Centre's May 2026 pension statistics confirm that 23.3 million UK employees were actively saving into a workplace pension in 2024, representing 82% of all employees — up from 55% in 2012 before auto-enrolment was rolled out. By February 2026, 11.4 million employees had been auto-enrolled who would not otherwise have been saving at all.But success in getting people into pensions is not the same as success in getting people to save enough. The minimum auto-enrolment contribution is 8% of qualifying earnings — 5% from the employee and 3% from the employer. The CSPA's May 2026 summary of the Pensions Commission's findings is explicit: 'Around half of those who are saving are doing so only at the minimum level required under automatic enrolment rules, leaving them with limited financial resilience in later life. The Commission suggests that this level is insufficient for many people to achieve a comfortable retirement.'

The design of auto-enrolment also limits its effectiveness for lower earners in a specific way. Contributions are calculated on 'qualifying earnings' — currently the band between £6,240 and £50,270 per year. Earnings below the £6,240 threshold are excluded from the calculation, meaning that a part-time worker earning £14,000 per year has their 8% contributions calculated only on £7,760 (£14,000 minus £6,240), producing an annual employer-employee contribution of approximately £621 rather than the £1,120 that would result from calculating on the full £14,000. This threshold design disproportionately disadvantages lower earners — the very group who have fewest alternative means of retirement provision.

Reason 2: The Self-Employed Are Almost Entirely Left Out

Auto-enrolment applies to employed workers. The UK's 4.9 million self-employed people are entirely outside the system — there is no employer to enrol them, no employer contribution to receive, and no automatic inertia mechanism to get them started. The consequences are stark.The Pensions Commission's May 2026 findings, reported by GB News, show that only 17% of self-employed workers with mixed income sources have any pension savings — and the share of self-employed people contributing to a pension has halved over the past 30 years. Britain currently has nearly three million full-time self-employed workers, according to House of Commons Library research published in February 2026 — approximately one in eight full-time workers. The vast majority are on track for retirement income significantly below any of the PLSA's three living standards.

Sophia Singleton, head of defined contribution pension schemes at consultants XPS, summarised the structural gap clearly in the GB News May 2026 report: 'There is an obvious hole in policy relating to the self-employed given the absence of auto-enrolment as a mechanism to save.' Self-employed people can contribute to a SIPP (Self-Invested Personal Pension) or personal pension and receive basic rate tax relief on contributions — but without the auto-enrolment inertia mechanism or employer contribution, take-up remains dramatically lower than among employees.

Reason 3: The Cost-of-Living Squeeze Has Crowded Out Pension Saving

Even among people who understand the importance of pension saving and are enrolled in a workplace pension, the sustained rise in the cost of living between 2022 and 2026 has made contributing above the auto-enrolment minimum feel financially impossible for many households. Standard Life's 2025 Retirement Voice report, cited by Pensions Age magazine, shows that only 30% of UK adults currently say they are living comfortably — meaning 70% are experiencing some degree of financial pressure that makes pension contributions compete with immediate needs.The same Standard Life research found that 53% of UK adults worry they are not saving enough for retirement. Despite this worry, only 15% have pension saving as one of their top financial priorities for the year. The gap between worry and action is not complacency — it is the product of real financial constraint. When food, energy, housing, and childcare costs absorb the majority of a household's income, the rational response under financial pressure is to reduce or stop discretionary contributions beyond the auto-enrolment minimum. Pension contributions above the minimum are, for many employees, the largest single expenditure that feels genuinely reducible.

The Investors Centre's 2026 pension statistics analysis notes that pension tax relief costs the government £59.1 billion in 2025/26 — but that 55% of income tax relief goes to higher rate taxpayers. The system is structurally generous to those who can afford to save more and less effective for those who need more support to save at all.

Reason 4: Pension Pots Are Being Raided Too Early

Since the pension freedom reforms of 2015, UK defined-contribution pension savers have been able to access their pension pots from age 55 (rising to 57 in April 2028), with 25% of the pot available tax-free. The intent was to provide flexibility for people approaching retirement. The consequence has been widespread early encashment that permanently depletes retirement savings.The CSPA's May 2026 summary of the Pensions Commission's findings documents the scale of premature drawdown: 'Around 30% of private pension pots are drawn down at the earliest opportunity, with approximately half of those accessed being withdrawn in full. Nearly half of this money is spent on large purchases such as cars, holidays, or home improvements, rather than being preserved for long-term income.'

This behaviour is economically rational from the individual's short-term perspective but catastrophically damaging to their long-term retirement income. A pension pot accessed at 55 and spent over the following two to five years leaves the individual with no private pension income for the potentially 25 to 35 remaining years of their life — dependent entirely on the State Pension, which at £11,973 per year provides only the bare minimum standard of retirement living. The pension freedom reforms, while well-intentioned, created a structural vulnerability that the current Commission is examining closely.

Reason 5: The Gender Pension Gap Is Structural and Growing

The pension undersaving crisis falls disproportionately on women — not because of individual choices or failures, but because of structural factors embedded in employment patterns, caring responsibilities, and the design of the auto-enrolment system itself.The CSPA's May 2026 summary of the Pensions Commission's findings is unambiguous: 'Women approaching retirement have, on average, about half the private pension wealth of men. Median pension savings stand at around £81,000 for women compared to £156,000 for men.' The Investors Centre's 2026 pension statistics elaborate on the structural drivers: 'The UK gender pension gap is driven by the gender pay gap, career breaks for childcare or caring responsibilities, higher rates of part-time working among women, and occupational segregation into lower-earning sectors. Women face an average 10-year career gap costing approximately £39,000 in lost pension savings.'

The auto-enrolment system's lower earnings threshold of £6,240 per year particularly disadvantages women, who are significantly more likely than men to earn below this threshold through part-time or intermittent work. When pension contributions are calculated only on earnings above the threshold, the effective contribution rate for a woman working part-time across multiple lower-earning roles may be substantially below the nominal 8% — and she will also receive a lower employer contribution than a full-time worker on the same hourly rate.

Reason 6: Low Awareness and Pension Inertia

Pension saving is the largest and most complex financial product in most people's lives, managed over a decades-long horizon, with rewards that are inherently delayed and progress that is difficult to visualise without active engagement. These characteristics make pensions uniquely vulnerable to inertia — the well-documented tendency to maintain the status quo rather than make active decisions, particularly when the benefit is distant and the cost is immediate.Auto-enrolment harnesses inertia productively — by making the default position 'saving' rather than 'not saving,' it has enrolled millions who would never have taken active steps. But the same inertia that keeps people enrolled at the minimum rate also keeps them from increasing contributions when their income rises, combining pensions from multiple employers into a consolidated pot, or engaging with the value of their accumulated savings to assess whether they are on track for their target retirement income.

The Investors Centre's 2026 statistics cite the Wharton School: 'Research published by the Wharton School of the University of Pennsylvania found that 57% of older Americans regret not saving more for retirement.' The parallel finding in the UK context is Standard Life's 2025 data showing 53% of UK adults already worry they are not saving enough — which suggests widespread awareness of the problem but insufficient translation of that awareness into action. The challenge is not primarily education. It is the structural and financial barriers that prevent awareness from converting into behaviour change.

Reason 7: The Expectation Gap Is Widening

Perhaps the most poignant dimension of the UK pension crisis is not what people are saving but what they expect retirement to look like — and how far that expectation has drifted from what is achievable on current savings trajectories.Standard Life's 2025 Retirement Voice report reveals a widening expectation gap: UK adults' preferred retirement age is 62, but their expected actual retirement age has risen to 67 — up from 66 in 2024. The gap between desired and expected retirement age grew by a full year in a single year, reflecting the creeping recognition that the pension savings needed to retire at 62 are beyond what most people are on track to accumulate. For some, this will translate into working longer. For others, it will mean a lower standard of living in retirement than they have planned for.

The DWP's Analysis of Future Pension Incomes 2025 provides the most granular picture of the expected adequacy gap. The analysis found that 43% of working-age individuals are undersaving against their Target Replacement Rate — the income level required to maintain a reasonable approximation of their pre-retirement standard of living. When measured against the PLSA standards rather than the TRR: 13% will fall below even the Minimum standard; 73% will fall below the Moderate standard; and 91% will fall below the Comfortable standard. On current savings trajectories, only one in ten working-age Britons is on track for a comfortable retirement.

What Should You Do? The Individual Action Plan

The systemic causes of the pension undersaving crisis are the responsibility of policy-makers and employers. But while structural reform works through the political process, individuals can take specific actions that significantly improve their own retirement outcomes.Eight actions to improve your UK retirement savings — starting now

- Find out your current pension pot value: Log in to every previous employer's pension scheme and your current workplace pension. If you have lost track of old pensions, use the Government's free Pension Tracing Service (gov.uk/find-pension-contact-details). The average UK worker changes employer eleven times, accumulating multiple small pension pots that are easily forgotten.

- Increase contributions by 1% this year: The most friction-free improvement is to increase your pension contribution by 1% of gross salary — often achievable by adjusting a single percentage on your employer's pension portal. On a £30,000 salary, 1% is £300 per year gross, or approximately £20 per month net for a basic rate taxpayer after pension tax relief. Over 30 years at 5% annual growth, that additional 1% adds approximately £20,000 to the final pot.

- Claim your pension tax relief: Basic rate taxpayers automatically receive 20% tax relief on pension contributions through the relief-at-source mechanism. Higher rate taxpayers must claim the additional 20% or 25% relief through their Self Assessment tax return. Many higher rate taxpayers fail to claim this additional relief — leaving free government money unclaimed.

- Consolidate old pension pots: If you have multiple small pension pots from previous employers, consolidating them into a single SIPP or your current employer's scheme reduces management complexity, may reduce charges, and makes it easier to track your total retirement savings against your target. Compare charges before consolidating — not all pension schemes are equally cost-efficient.

- Check your State Pension forecast: Visit your personal tax account at gov.uk to see your current State Pension forecast and how many qualifying National Insurance years you have accumulated. The full new State Pension for 2025/26 is £11,973 per year. If you have gaps in your NI record, buying additional qualifying years at £824 per year (Class 3 NI contributions in 2025/26) may be one of the best-value financial decisions available — a one-year purchase producing £329 of additional State Pension income per year for life.

- If self-employed: open a SIPP today: A SIPP (Self-Invested Personal Pension) is available to any UK resident under age 75. Basic rate tax relief of 20% means that a £800 contribution becomes £1,000 in the pension immediately — a guaranteed 25% uplift before any investment growth. Platforms like Vanguard, Hargreaves Lansdown, and Nutmeg offer low-cost SIPPs with index fund options.

- Use your Stocks and Shares ISA as a supplementary vehicle: If your pension contributions are constrained by the annual allowance (£60,000 in 2025/26) or by desire for pre-57 access, a Stocks and Shares ISA (£20,000 annual allowance in 2026/27) provides tax-free investment growth with full flexibility of access. For those retiring before age 57, the ISA is the primary vehicle for bridging the gap between retirement and the point at which the pension becomes accessible.

- Get regulated financial advice: The decisions around pension contribution levels, drawdown strategy, annuity vs income drawdown, and State Pension deferral are individually specific and genuinely complex. A one-off regulated financial advice session, particularly in the decade before retirement, typically produces better financial outcomes than any rule-of-thumb strategy. MoneyHelper (moneyhelper.org.uk) provides free, impartial guidance and can refer you to regulated advisers.

CONCLUSION

The UK pension undersaving crisis in 2026 is not a story of individual irresponsibility. It is a story of structural failure — an auto-enrolment system whose floor is too low, a self-employment sector entirely excluded from the mechanism that has enrolled 11.4 million workers, a cost-of-living crisis that has made additional contributions feel impossible, pension freedoms that have enabled premature encashment of long-term savings, and a gender pension gap driven by caring responsibilities and part-time work that the current system was never designed to fully address. The Government's new Pensions Commission exists precisely because the data — 18 million not saving, 14.6 million undersaving, 9 in 10 below the Comfortable standard — demands a systemic response.But structural reform takes time, and the retirement of people currently in their thirties, forties, and fifties does not. The eight individual actions in Section 10 of this guide are available now, to anyone, regardless of where the policy debate lands. Find your pension pots. Increase contributions by 1%. Claim your tax relief. Check your State Pension forecast. Open a SIPP if you are self-employed. The gap between the retirement most Britons want and the retirement most are on track for is real and large — but it is not yet fixed. For those who act in the next decade, it is still closable.

Frequently Asked Questions

How many Britons are not saving enough for retirement?

The UK Pensions Commission, established in July 2025 and publishing initial findings in May 2026, found that 45% of working-age adults — approximately 18 million people — are not contributing to a pension at all, despite nearly half of them being in paid employment. The DWP's Analysis of Future Pension Incomes 2025, published in July 2025, found that 43% of working-age individuals — 14.6 million people — are undersaving against their Target Replacement Rate (the income needed to maintain a reasonable approximation of pre-retirement living standards). When measured against the PLSA Comfortable retirement standard, 9 in 10 working-age people are currently on track to fall short. These are not fringe statistics — they reflect the mainstream experience of UK workers under current savings and contribution rates.How much do I need to retire comfortably in the UK?

The PLSA's 2025 Retirement Living Standards provide the most widely used UK benchmarks. For a one-person household outside London, the annual income needed after tax is: Minimum £13,400 (basics, one UK holiday, no car); Moderate £31,300 (small car, two-week European holiday); Comfortable £43,900 (longer holidays, eating out, replacing appliances). The full new State Pension for 2025/26 is £11,973 per year, which covers only the Minimum standard for a two-person mortgage-free household. For a single person seeking Comfortable retirement, Rest Less' May 2026 analysis confirms they need a pension pot of £540,000 to £800,000 on top of their State Pension — a figure that requires contribution rates considerably above the auto-enrolment minimum of 8% for most working-age savers.Why is the auto-enrolment contribution of 8% not enough?

The 8% minimum auto-enrolment contribution (5% employee, 3% employer) is calculated on qualifying earnings — the band between £6,240 and £50,270 per year. This threshold design means that contributions are not paid on the first £6,240 of earnings, reducing the effective contribution rate for lower earners. More fundamentally, 8% of qualifying earnings for a median earner over a working lifetime, invested at typical long-run returns, will produce a pension pot well below the £330,000 to £490,000 needed for Moderate retirement and far below the £540,000 to £800,000 needed for Comfortable retirement. The CSPA's May 2026 summary of the Pensions Commission's findings states directly: 'The Commission suggests that the minimum auto-enrolment level is insufficient for many people to achieve a comfortable retirement.'Why are self-employed people not saving into pensions?

Self-employed workers are excluded from auto-enrolment — the mechanism that has enrolled 11.4 million additional employees who would not otherwise have been saving. Without an employer to enrol them, without an employer contribution to receive, and without the inertia mechanism that makes doing nothing result in pension saving rather than non-saving, self-employed people face a purely opt-in decision. The CSPA's May 2026 Pensions Commission summary found that the share of self-employed people contributing to a pension has halved over the past 30 years, and that only 17% of self-employed workers have any pension savings. The solution for self-employed people is to open a SIPP (Self-Invested Personal Pension), which is available to any UK resident under 75 and provides 20% basic rate tax relief on contributions — making a £800 contribution worth £1,000 in the pension immediately.What is the gender pension gap in the UK?

Women approaching retirement have, on average, approximately half the private pension wealth of men — median pension savings of £81,000 for women compared to £156,000 for men, according to the CSPA's May 2026 summary of the Pensions Commission's findings. The Investors Centre's 2026 pension statistics identify four structural drivers: the gender pay gap (lower earnings mean lower pension contributions), career breaks for childcare and caring responsibilities, higher rates of part-time work among women, and occupational segregation into lower-earning sectors. Women face an average 10-year career gap costing approximately £39,000 in lost pension savings. The auto-enrolment lower earnings threshold of £6,240 also disproportionately affects women in part-time or low-paid roles, whose contributions may be calculated on a significantly reduced qualifying earnings base.References

GOV.UK — Britain is Undersaving for Retirement Warns Pensions Commission (May 2026) https://www.gov.uk/government/news/britain-is-undersaving-for-retirement-warns-pensions-commissionCSPA — Millions of Britons Not Saving Enough for Retirement (May 2026) https://www.cspa.co.uk/news/millions-of-britons-not-saving-enough-for-retirement/

GB News — Pensions Crisis Deepens as Millions Not Saving Enough (May 2026) https://www.gbnews.com/money/pensions-crisis-deepens-as-millions-not-saving-enough

The Investors Centre — UK Pension Statistics 2026: Key Data and Trends (2026) https://www.theinvestorscentre.co.uk/investing/statistics/pension/

GOV.UK / DWP — Analysis of Future Pension Incomes 2025 (July 2025) https://www.gov.uk/government/statistics/analysis-of-future-pension-incomes-2025/analysis-of-future-pension-incomes-2025

Rest Less — How Much Do You Need to Retire Comfortably in 2026? (May 2026) https://restless.co.uk/pensions-retirement-planning/approaching-retirement/how-much-to-retire-comfortably/

PLSA — Retirement Living Standards 2025: Official Update https://www.retirementlivingstandards.org.uk/library/2025-rls-update

Pensions Age — Majority of UK Adults Worry About Retirement Savings Yet Few Prioritise Pensions (October 2025) https://www.pensionsage.com/pa/Majority-of-UK-adults-worry-about-retirement-savings-yet-few-prioritise-pensions.php

Saltus — Recalibrating Retirement: The PLSA's Retirement Standards 2025/26 (July 2025) https://www.saltus.co.uk/the-financial-planning-blog/recalibrating-retirement

0 Comments Comments