Investing

Women Are 'Risk-Appropriate' Investors — Here's Why

TABLE OF CONTENTS

- What Does 'Risk-Appropriate' Actually Mean?

- The Data: Women Outperform Men as Investors

- Why Women Trade Less — and Why That Matters

- Staying Calm in Volatile Markets

- The Long-Term View: Planning Over Prediction

- The Great Wealth Transfer: Women and the Future of Finance

- The Investment Gap: Why Many Women Still Hold Back

- What the Research Says Men Can Learn From Women

- Practical Tips From Women Investors Who Get It Right

- Conclusion

- Frequently Asked Questions

- References

What Does 'Risk-Appropriate' Actually Mean?

When Fidelity certified financial planner Alex Roca describes women as "risk-appropriate" investors, she is making a specific and important distinction. Being risk-appropriate does not mean being risk-averse in a way that leaves returns on the table. It means taking on the level of risk that genuinely matches your financial goals, your time horizon, and your personal circumstances — no more and no less.This distinction matters because the dominant narrative about women and investing has long been that women are simply more cautious, more fearful, or less willing to take the bold risks that generate big returns. That framing is both inaccurate and unhelpful. What the data actually shows is something quite different: women tend to approach investment risk with a clarity of purpose that many men lack. They are less likely to take on risk for the thrill of it, less likely to chase hot trends or the latest buzzworthy asset, and more likely to build a portfolio that reflects what they are actually trying to achieve over a realistic timeframe.

In volatile markets — like the one investors have navigated in 2025 and 2026, with geopolitical shocks from the Iran war, tariff uncertainties, and sharp swings in technology stocks — that kind of disciplined, purposeful approach to risk turns out to be a significant competitive advantage. While some investors sell in panic during market downturns and lock in losses they never needed to take, women who have built portfolios suited to their actual risk tolerance and goals tend to hold steady and let compounding do its work.

The Data: Women Outperform Men as Investors

The claim that women are better investors than men is not a slogan — it is a finding that has been replicated across multiple independent studies using large data sets over extended time periods. The evidence is consistent enough that it is now treated as an established finding in behavioural finance research.Fidelity's large-scale analysis

In 2021, Fidelity Investments published the results of an analysis of annual investment performance across 5.2 million accounts from January 2011 to December 2020. Women outperformed men by 40 basis points — 0.4 percentage points — per year. That might sound small, but compounded over a 30-year investing career, 0.4 percentage points of annual outperformance can translate into tens of thousands of dollars in additional wealth. Fidelity has confirmed that this trend continued in its subsequent analysis through 2025.Warwick Business School: 1.8% annual advantage

An earlier 2018 study by Warwick Business School found an even larger gap: women's investment portfolios outperformed men's by 1.8% annually, while women traded fewer times per year on average. The study's authors attributed the outperformance primarily to lower trading frequency and the avoidance of speculative positions.Wells Fargo Investment Institute 2025

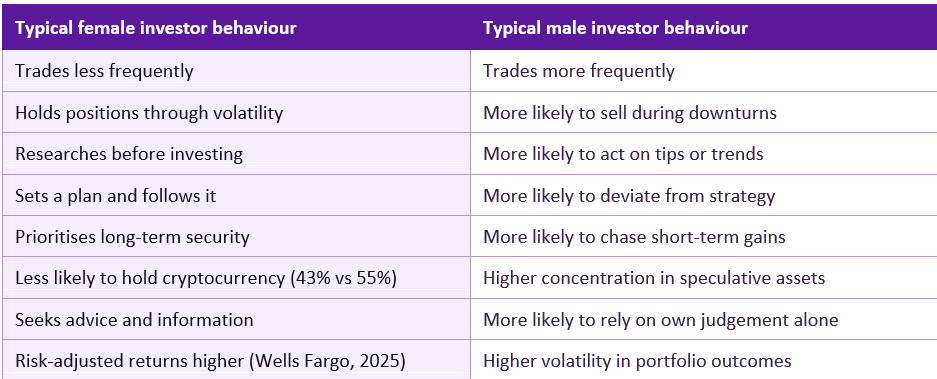

A 2025 report by the Wells Fargo Investment Institute found that women's risk-adjusted investment returns were higher than men's. The study also found that women-led joint accounts outperformed those led by men on an absolute basis. Women tended to be more disciplined investors and demonstrated a greater willingness to learn and seek advice before making decisions.One of the biggest misconceptions about women investors is that they are emotional, and that is just not the case. Women proceed in an analytical way — they are willing to do more research and hone a strategy. They are making a plan and sticking to that plan.

— ALEX ROCA, CFP, HOST OF FIDELITY'S WOMEN TALK MONEY (CNBC, APRIL 2026)

Why Women Trade Less — and Why That Matters

One of the most consistent findings across the research on women investors is that they trade less frequently than men. This sounds like a disadvantage — surely active management should produce better results than a passive, buy-and-hold approach? The data says otherwise, and the reason is rooted in the basic economics of investing.Every time an investor trades, they incur costs: transaction fees, bid-ask spreads, and the tax consequences of realising gains. More significantly, frequent trading almost always reflects a belief that the investor can predict short-term market movements — a belief that decades of research has consistently shown to be misplaced, even among professional fund managers. Studies consistently find that the more frequently retail investors trade, the worse their long-term returns tend to be. This effect is especially pronounced among men, who are statistically more likely to exhibit overconfidence in their ability to time the market.

Women, by contrast, are more likely to buy a diversified portfolio suited to their goals and hold it through market fluctuations. Fidelity's research has found that women maintain their portfolio allocations far more consistently than men — particularly during periods of market stress, when the temptation to sell and move to cash can be overwhelming. This discipline in not reacting to short-term market noise is, paradoxically, one of the most valuable investment skills a person can have. Warren Buffett famously described his favourite holding period as "forever" — and the research on gender and investing suggests that women are, on average, better natural practitioners of that principle.

Staying Calm in Volatile Markets

The year 2025 and the early months of 2026 have tested investors with a series of significant market shocks. The outbreak of the Iran-Israel-US conflict sent oil prices above $120 a barrel, disrupted global trade flows, and triggered sharp corrections in equity markets. Tariff announcements from the Trump administration created uncertainty for multinationals. Inflation remained sticky in several major economies. In this environment, the ability to stay calm and stick to a long-term investment plan has been worth considerably more than the ability to predict the next market move.A 2025 Fidelity Women and Money study found that 42% of women cut down non-essential spending in the past year in response to economic uncertainty — a proactive, practical response to external conditions. A similar share of women polled said they were committed to saving more and paying down debt in the year ahead. These are not the responses of people who are emotionally driven or impulsive. They are the responses of people who assess their financial situation clearly and make adjustments based on facts.

In contrast, research into investor behaviour during market sell-offs consistently finds that men are more likely to sell equities during periods of volatility and move to cash — locking in losses and then missing the recovery that invariably follows. Behavioural finance research has identified overconfidence as a key driver of this pattern: the same confidence that leads men to trade more frequently in calm markets also leads them to make bigger directional bets during turbulent ones. When those bets are wrong — and in volatile, unpredictable markets they frequently are — the financial cost can be substantial.

The Long-Term View: Planning Over Prediction

One of the most cited explanations for women's investment outperformance is their tendency to invest with a clear long-term goal in mind and to stick to a plan designed to achieve it. A 2025 study by McKinsey found that women tend to prefer stable investments and adopt a more cautious approach to their money, prioritising long-term financial security over short-term gains. This is not a limitation — it is a feature of sound investment thinking.The investment industry has long been structured around the idea that superior returns come from superior information — that if you can identify the next big winner before others do, you will outperform. In reality, most actively managed funds underperform their benchmark indices over long periods, precisely because the costs of trading and the difficulty of consistently predicting market movements erode any advantage. The investors who tend to build the most wealth over time are not those who pick the best stocks in any given year. They are those who invest consistently, diversify sensibly, keep costs low, and stay invested through market cycles.

Women investors tend to exhibit precisely the behaviours that align with this evidence-based approach. They are more likely to create a financial plan and stick to it. They are more likely to choose diversified, low-cost investment vehicles over concentrated, high-cost ones. They are less likely to be drawn in by the promise of exceptional returns from speculative investments. As Meghan Railey, co-founder and CEO of Optas Capital, has noted, while male clients tend to eagerly invest in the latest asset class everyone is talking about — like cryptocurrency — female clients generally do not jump on the latest trend. Only 43% of female investors hold cryptocurrency, compared with 55% of male investors, according to Behavioural Finance Consulting research from 2025.

The Great Wealth Transfer: Women and the Future of Finance

The conversation about women and investing has taken on a new urgency in 2025 and 2026 because of the scale of wealth that is now moving into women's hands. According to McKinsey's 2025 report, The New Face of Wealth, women currently control approximately one-third of all retail financial assets in the United States and European Union — roughly $60 trillion globally. Between 2018 and 2023, global financial wealth grew by 43%, while the wealth controlled by women grew by 51%, consistently outpacing the overall market.By 2030, women in the US are expected to control between 40% and 45% of all retail financial assets, up from about a third today. McKinsey's earlier projections were even more striking: some forecasts suggested that by 2030, roughly two-thirds of all private wealth in the US would be held by women, driven by the combination of women's longer lifespans — they outlive men by an average of nearly six years — and the transfer of Baby Boomer assets between generations.

This is not just a demographic curiosity. It represents a fundamental shift in who makes investment decisions, what those decisions prioritise, and how the financial services industry needs to respond. Research from McKinsey and other firms has consistently found that women's investment priorities differ from men's in important ways — they are more likely to value sustainability and ESG factors, more likely to seek financial security over wealth maximisation, and more likely to integrate their investments with broader life goals around family, community, and purpose.

Fidelity reports that 71% of women now invest in the stock market — the highest rate ever recorded — and that younger generations of women are leading the charge in both participation and financial literacy. This represents a transformation of the investing landscape that financial advisers, asset managers, and policymakers will need to respond to over the coming decade.

7. The Investment Gap: Why Many Women Still Hold Back

Despite the compelling evidence that women are highly effective investors, a significant investment gap between men and women persists. Research from SoFi found that in a 2024 survey, 53% of women said they did not invest because they did not have the funds to do so — a reflection of the persistent gender pay gap, which means women earn approximately 85 cents for every dollar men earn, according to a 2025 Pew Research Center analysis.

Beyond the pay gap, confidence plays a significant role. Despite the investment performance data in their favour, only 14% of women in one study expressed high confidence in their investing knowledge — even though 71% agree that investing is a way to build generational wealth. This confidence gap is in part a product of an investment industry that has historically been designed around and marketed to men. The language, imagery, and framing of financial services have often felt alien or unwelcoming to women investors.

Women are also somewhat more likely than men to report that they feel unprepared for their financial goals despite having a financial adviser. McKinsey has flagged this as a major opportunity: a significant portion of women's assets are currently underserved relative to potential demand, reflecting a misalignment between traditional advisory models and the priorities women actually bring to financial planning.

The combined effect of the pay gap, the confidence gap, and underserved advisory relationships means that despite their investing strengths, women on average still retire with significantly less wealth than men. The median retirement savings for women is $50,000, compared with $157,000 for men, according to a 2024 Prudential report. Closing these gaps — through equal pay, better financial education, and advisory services genuinely designed for women — remains one of the most important financial equity challenges of the decade.

What the Research Says Men Can Learn From Women

It is worth being clear that the research on gender and investing is not a competition. The point is not that men are bad investors and women are good ones. The point is that specific behaviours — lower trading frequency, consistent adherence to a plan, disciplined avoidance of speculative trends, and a focus on long-term goals over short-term performance — are consistently associated with better investment outcomes. And women, as a group, exhibit those behaviours more consistently than men.That means any investor — regardless of gender — can benefit from understanding and adopting these approaches. The investment case for patience, diversification, low costs, and long-term planning does not depend on your gender. What the data on women investors does is to make concrete and visible what good investment behaviour looks like in practice.

Financial advisers who work with both male and female clients often note that men can be more resistant to the idea of doing less. The instinct to monitor portfolios daily, to seek out new opportunities, and to act on market news can feel like due diligence — but the research suggests it often does more harm than good. Learning from the default behaviours of women investors means, in practice, setting up a diversified portfolio, automating contributions, reviewing it quarterly rather than daily, and resisting the urge to trade based on headlines.

Practical Tips From Women Investors Who Get It Right

Based on the research findings and expert guidance from advisers like Alex Roca and Meghan Railey, the following practices distinguish the most effective women investors — and are applicable to all investors regardless of gender.Investing habits that produce better long-term outcomes

- Start with a written financial plan. Define your goals, time horizon, and the level of risk you are genuinely comfortable with before you invest a single dollar. Review the plan annually rather than every time markets move.

- Automate contributions. Setting up regular automatic transfers into your investment account removes the temptation to time the market and ensures you invest consistently through both bull and bear markets.

- Diversify broadly. Spread investments across asset classes, geographies, and sectors. A diversified portfolio reduces volatility without necessarily reducing long-term returns.

- Keep trading to a minimum. Resist the urge to react to news, market moves, or tips from friends. Every trade carries a cost and is an opportunity for human behavioural bias to work against you.

- Keep costs low. Choose index funds or ETFs with low expense ratios wherever possible. The difference between a 0.1% and a 1.0% annual fee compounds to a significant amount over a long investing career.

- Seek independent financial advice. Women who work with an adviser aligned with their priorities and who speaks their language tend to achieve better outcomes. Do not settle for an adviser relationship that feels transactional or dismissive.

- Do not let the confidence gap stop you from starting. The research is clear: the average woman investor outperforms the average man. Waiting until you feel confident enough to invest is itself a form of financial risk.

CONCLUSION

The evidence is both robust and consistent: women are excellent investors, and the behaviours that make them excellent — disciplined planning, lower trading frequency, risk that is matched to actual goals, and the composure to hold steady in volatile markets — are exactly the behaviours that produce superior long-term returns. In a year defined by geopolitical shocks, tariff uncertainty, and sharp market swings, those strengths have been on full display.The narrative that women are timid or overly conservative investors is not supported by the data. The data says something far more interesting: women are appropriately calibrated. They take risks they can sustain, build portfolios designed to achieve their actual goals, and resist the short-term noise that derails so many investors who mistake activity for achievement. As women take control of an ever-larger share of global wealth — and as the investment gap slowly narrows — these strengths are becoming one of the most important stories in modern personal finance.

0 Comments Comments