Finance

Accountant Explains What Is Money Transfer? Complete Guide

Table of Contents

- Why How You Send Money Matters as Much as How Much You Send

- What Is Money Transfer?

- Types of Money Transfer

- Best UK Money Transfer Providers: 2026 Full Comparison

- The Real Cost of Sending £5,000 Abroad: Bank vs Specialist

- Wise: The Benchmark for Transparent International Transfers

- Revolut: The All-in-One Financial App That Became a UK Bank

- Large Transfers: Property, Emigration, and Business Payments

- Atlantic Money: The Cheapest for Large Standard Currency Transfers

- Currencies Direct and TorFX: Specialists for High-Value Transfers

- Personal Remittances: Sending Money to Family Abroad

- How to Stay Safe: Regulation, Safeguarding, and Fraud Prevention

- How to Make an International Money Transfer: Step by Step

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why How You Send Money Matters as Much as How Much You Send

Sending £5,000 to a family member in Europe, a property seller in Spain, a university in the United States, or an employee in India are all fundamentally the same financial act — moving money from one bank account to another across a currency border. The difference is in what it costs. Send that £5,000 through a UK high street bank and you could pay £25 to £50 in transfer fees on top of an exchange rate that is 2% to 5% worse than the mid-market rate — a total cost of £125 to £300 on a single transaction. Send the same amount through Atlantic Money, and you pay a flat fee of £3. Through Wise, from 0.41% of the transfer amount. The recipients receive materially more in both cases.This gap between bank pricing and specialist pricing for international money transfers is one of the most consistently and most easily avoidable financial costs available to UK consumers and businesses. Specialist money transfer services — Wise, Revolut, Atlantic Money, Currencies Direct, TorFX, OFX, Xe, Remitly, WorldRemit, and others — have spent the past decade disrupting the international payments market by offering exchange rates far closer to the real mid-market rate and transfer fees a fraction of what banks charge. Wise alone processes transfers for over 16 million customers. Revolut, which completed its UK banking licence launch on 11 March 2026, serves over 75 million customers worldwide and now benefits from FSCS protection up to £120,000 in the UK.

This guide explains exactly what money transfer is, how it works, the types available, what the real costs are, how to choose the right provider for your specific type of transfer — small personal remittances, large property transactions, regular business payments — and the practical rules that protect your money during the transfer process.

What Is Money Transfer?

Money transfer, in the context of this guide, refers specifically to international money transfer — the process of moving funds from one person, business, or account in one country to another person, business, or account in a different country, typically involving a currency conversion. The domestic equivalent — moving money between UK bank accounts in pounds — is handled through BACS, Faster Payments, or CHAPS and is effectively instant and free for UK consumers. It is the cross-border, cross-currency version that involves complexity, cost, and the need for a specialist approach.At its most basic, an international money transfer involves three elements: the amount in the sending currency (e.g. GBP), the conversion into the receiving currency (e.g. EUR, USD, INR), and the delivery to the recipient's bank account or other payment method. Each of these elements carries potential costs: the transfer fee (what you pay to use the service), the exchange rate (how favourable the conversion rate is compared with the mid-market rate), and the receiving fee (sometimes charged by the recipient's bank for accepting international wire transfers).

Types of Money Transfer

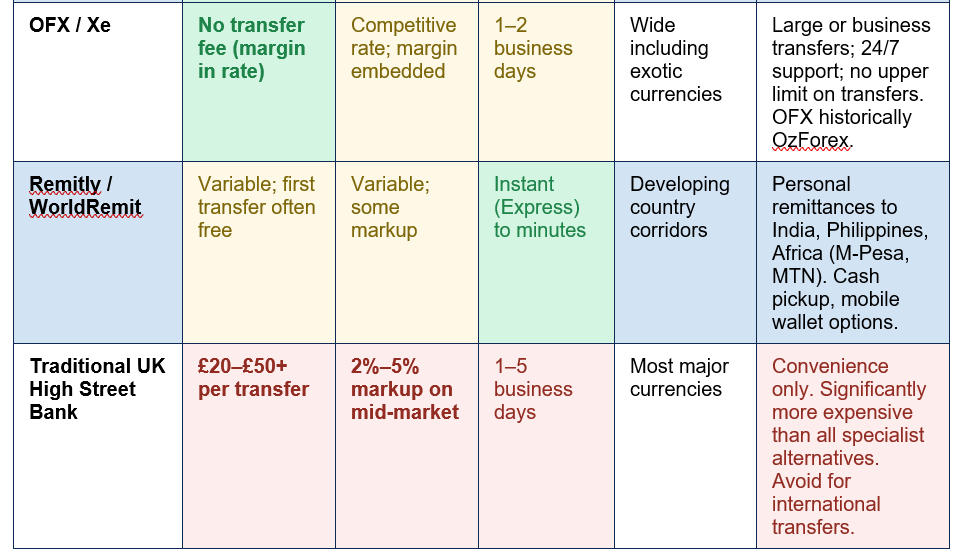

- Bank wire transfer (SWIFT): The traditional method used by high street banks. Money travels through the SWIFT interbank network, passing through one or more correspondent banks before reaching the recipient's account. Typically takes 1 to 5 business days, costs £15 to £50 per transfer in fees, and uses the bank's own (unfavourable) exchange rate. Every intermediate correspondent bank may deduct a fee. Once the dominant method, now the most expensive and slowest for most transfers.

- Specialist transfer service (Wise, Atlantic Money, Revolut, OFX, etc.): Digital transfer platforms that aggregate currency buying power and use internal matching or local payment networks to move money. Significantly cheaper than bank wires for most routes. Typically use exchange rates far closer to the mid-market rate. Speed varies from instant (for matched routes) to 1-2 business days for most transfers.

- Cash pickup / mobile money transfer (Western Union, Remitly, WorldRemit): The sender pays in GBP online or in a physical agent location; the recipient collects cash at an agent location abroad or receives funds directly into a mobile money wallet (M-Pesa, MTN Mobile Money). Essential in corridors where the recipient does not have a bank account. Typically higher fees than bank-to-bank transfers but provides delivery methods that specialist platforms do not.

- Peer-to-peer (P2P) matching (historical concept): Wise originally pioneered the concept of matching UK users sending money to Europe with European users sending money to the UK, effectively executing two domestic transfers rather than one international one. Modern platforms have evolved beyond pure P2P matching but continue to use local payment networks to minimise the number of cross-border movements and therefore costs.

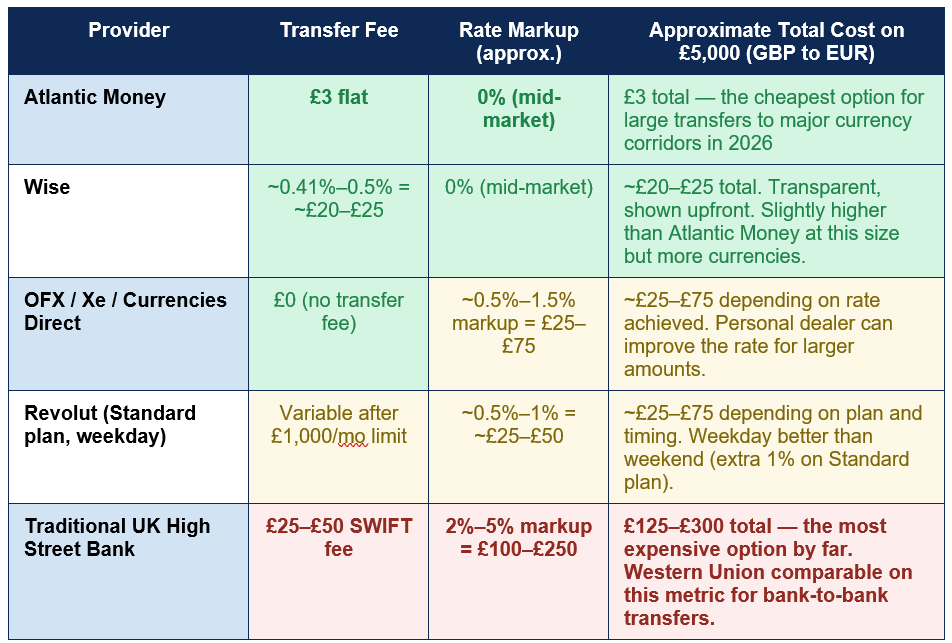

The cost gap between banks and specialists: Sending £5,000 through a UK bank can cost £125–£300 vs £3–£25 through a specialist — a UK high street bank typically charges £25–£50 in SWIFT transfer fees plus a 2%–5% exchange rate markup, totalling £125–£300 on a £5,000 transfer. Atlantic Money charges a £3 flat fee with the mid-market rate; Wise charges from 0.41% (~£20 on £5,000). The saving of using a specialist is not marginal — it is transformative for anyone making regular international transfers (CurrencyBrokers UK / Statrys, 2026).

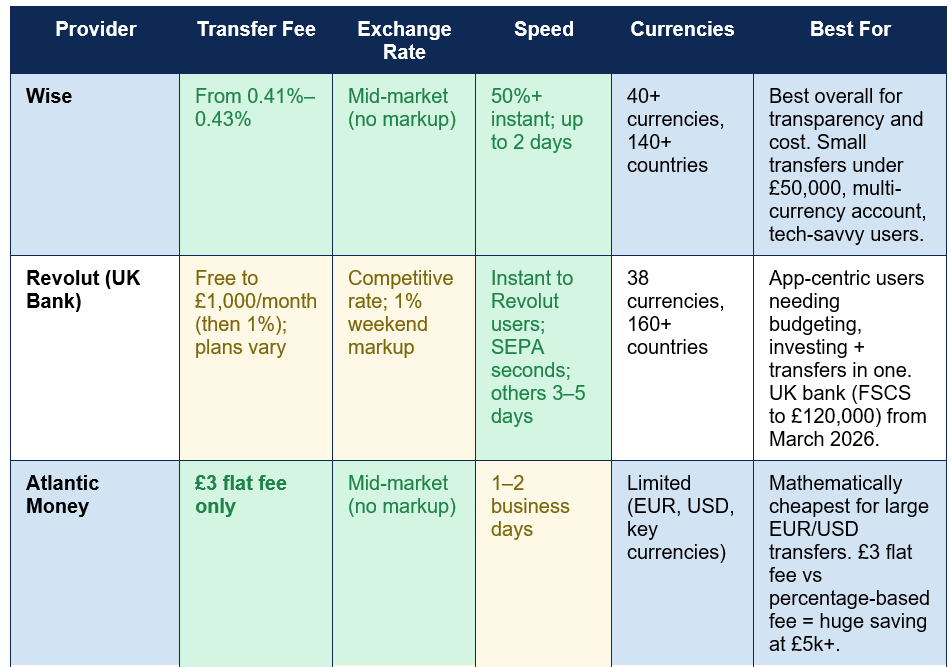

Best UK Money Transfer Providers: 2026 Full Comparison

The table below compares the leading UK money transfer providers in 2026 across the key dimensions that determine total cost and usability. Data sourced from CurrencyBrokers UK (May 2026), Statrys (May 2026), Wise (2026), and Revolut (June 2026). Exchange rates and fees change daily — always check directly before sending:

The Real Cost of Sending £5,000 Abroad: Bank vs Specialist

The most important factor most people overlook when comparing money transfer services is that the transfer fee and the exchange rate are two separate costs, and the exchange rate is typically the larger one. A service advertising 'no transfer fees' may still cost significantly more than a service charging an explicit fee, if the former uses a worse exchange rate. The table below shows the approximate total cost of sending £5,000 GBP to EUR in 2026 across all major provider types:

How the exchange rate markup works — and why it is the hidden cost: If the mid-market GBP/EUR rate is 1.18, and a bank applies a 3% markup, your effective rate is approximately 1.14. On £5,000, you receive approximately €5,700 at the mid-market rate versus approximately €5,530 at the bank's rate — a difference of €170 lost in the exchange rate alone, before any transfer fee. This is why providers who advertise 'zero transfer fees' but embed a large exchange rate margin are not necessarily cheaper than providers who charge an explicit percentage fee but use the mid-market rate. Always calculate the total amount your recipient will receive — not just the upfront fee — when comparing providers.

Wise: The Benchmark for Transparent International Transfers

Wise — formerly TransferWise, rebranded in 2021 — is the most commonly cited benchmark for transparent, cost-effective international money transfers in the UK in 2026. Its defining commitment is the mid-market exchange rate: the same rate shown on Google or XE.com, with no markup applied to the rate itself. All of Wise's cost is contained in an explicit percentage fee, shown upfront before you confirm the transfer. This fee starts from 0.41% of the transfer amount and varies by currency pair and payment method. There are no hidden costs.Wise operates in 40+ currencies, sends to 140+ countries, and over 50% of its payments arrive instantly. It offers a multi-currency account — the Wise Account — that allows users to hold, receive, and spend in multiple currencies simultaneously, with local bank account details (including sort code and account number for GBP, IBAN for EUR, routing number for USD, and more) that make it useful for international freelancers, expats, and businesses. The Wise card allows spending directly from the multi-currency account at the mid-market rate wherever Mastercard is accepted.

The limitation of Wise for very large transfers — property purchases, large business payments — is that its percentage-based fee, while low, scales with the amount. At 0.41%, a £200,000 property transfer costs approximately £820 in fees. Atlantic Money's £3 flat fee or Currencies Direct's no-fee-with-competitive-rate model becomes materially cheaper at these amounts. CurrencyBrokers UK's 2026 analysis explicitly segments: Wise is best for transfers under £50,000; specialist FX brokers are better above that threshold.

Revolut: The All-in-One Financial App That Became a UK Bank

Revolut's most significant development in 2026 is its UK banking licence, launched on 11 March 2026. As a fully regulated UK bank, eligible Revolut deposits are now protected by the Financial Services Compensation Scheme (FSCS) up to £120,000 per customer — a meaningful increase in consumer protection from the previous e-money safeguarding model. The company serves over 75 million customers worldwide and has expanded well beyond its original international transfer use case into a full financial platform including investing, cryptocurrency, savings vaults, and budgeting tools.For international transfers, Revolut's structure differs from Wise. Standard plan customers receive fee-free currency exchange up to £1,000 per month, then a 1% fair usage fee on additional exchanges. International transfers outside SEPA incur a small variable fee shown in-app. The exchange rate used by Revolut on weekdays is competitive; on weekends, Standard and Plus plan customers pay an additional 1% for currency conversion. Transfers between Revolut accounts anywhere in the world are typically instant and free of transfer fees.

The Wise vs Revolut choice in 2026 largely comes down to use case. For dedicated, frequent international transfers — especially larger amounts in standard currency pairs — Wise's consistent mid-market rate with no weekend surcharge is cheaper and more predictable. For those who want one app for their complete financial life, including budgeting, cryptocurrency, stock trading, and occasional international transfers, Revolut's broader platform justifies its position.

Large Transfers: Property, Emigration, and Business Payments

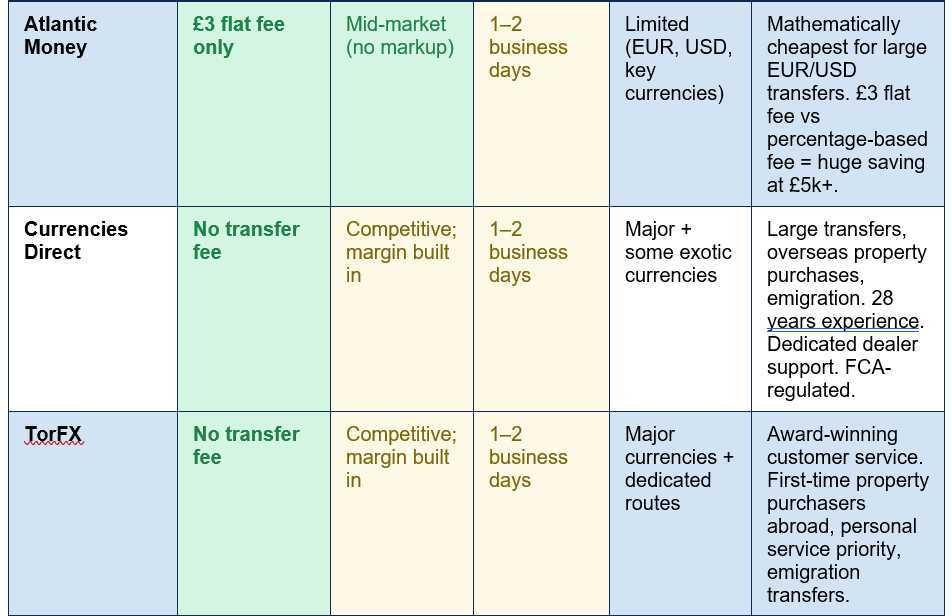

The provider landscape shifts materially for transfers above £50,000 — property purchases, emigration transfers, large business payments to overseas suppliers or employees. At these sizes, the percentage-based fees of Wise and Revolut become significant absolute amounts, and the dedicated FX broker model of Currencies Direct, TorFX, and OFX becomes more cost-competitive.Atlantic Money: The Cheapest for Large Standard Currency Transfers

Atlantic Money offers what is mathematically the cheapest model available for large transfers in major currency pairs: a flat £3 fee per transfer with the mid-market exchange rate and no markup. For a £200,000 property purchase transfer, the difference between Atlantic Money (£3) and Wise (approximately £820 at 0.41%) is approximately £817. The limitation is currency coverage — Atlantic Money currently covers the major corridors (EUR, USD, GBP, CAD, AUD, and a limited set of others) but does not handle exotic currencies or the full breadth of routes covered by Wise or Currencies Direct.Currencies Direct and TorFX: Specialists for High-Value Transfers

Currencies Direct (28 years of experience, no transfer fees) and TorFX (award-winning customer service, no transfer fees) both operate on a model where the cost is embedded in the exchange rate margin rather than a separate fee. For high-value transfers, dedicated dealers at both companies will work with clients to improve the rate relative to the published rate, particularly for amounts above £50,000. Both are fully FCA-regulated and carry professional indemnity insurance appropriate for large value transfers. Both offer forward contracts — locking in an exchange rate for a future transfer — which can be valuable when planning a property purchase with a completion date weeks away.The forward contract is one of the most important features available to property buyers purchasing abroad. Currency markets can move 5% to 10% in either direction over the months between exchanging contracts and completing a purchase. A forward contract with Currencies Direct or TorFX locks in the rate at exchange, eliminating this risk for a known future amount. Forward contracts are not available from consumer apps like Wise or Revolut.

THE FIVE-MINUTE CHECK BEFORE ANY LARGE TRANSFER: Before sending any amount over £1,000 internationally, spend five minutes comparing the total recipient amount — not just the fee — across at least three providers. Use Wise's fee calculator, Atlantic Money's calculator, and the rate from your bank. The difference on £5,000 between the cheapest specialist and your bank can easily be £200+. The difference on £200,000 can be several thousand pounds. This five-minute comparison is the highest-return financial action available to anyone making an international transfer.

Personal Remittances: Sending Money to Family Abroad

Personal remittances — money sent from the UK to family members in other countries — represent a significant and growing flow of international transfers. For remittances to developing country corridors — India, the Philippines, Nigeria, Ghana, Kenya, Pakistan, Bangladesh — the provider landscape is different from the standard EUR/USD transfer market. Speed, delivery method, and corridor-specific coverage matter as much as the exchange rate.Remitly is consistently rated as one of the strongest options for Southeast Asian and South Asian corridors, offering an Express transfer option for speed-sensitive senders and an Economy option for lower fees. WorldRemit provides particularly strong coverage in African corridors, with direct integrations to M-Pesa and MTN Mobile Money that allow recipients to receive funds directly into mobile money wallets without a bank account. Statrys' 2026 comparison confirms: WorldRemit is the stronger choice for Africa, particularly for M-Pesa and MTN Mobile Money corridors.

For remittances to India specifically, Wise offers competitive rates and speed to major Indian bank accounts. For cash pickup requirements — where the recipient does not have a bank account or where cash pickup is culturally preferred — Western Union's global agent network of over 500,000 locations remains unmatched, though its fees and exchange rates are significantly worse than digital alternatives for bank-to-bank transfers. The right choice depends on the recipient's specific location, bank access, and preferences.

How to Stay Safe: Regulation, Safeguarding, and Fraud Prevention

The safety of an international money transfer depends on the regulatory status of the provider you use. In the UK, all legitimate money transfer services must be either authorised or registered with the Financial Conduct Authority (FCA) as a payment institution, electronic money institution, or in Revolut's case (from March 2026) a full bank. Authorised firms have the strongest consumer protections; registered firms have lighter-touch oversight. The FCA register at fca.org.uk allows anyone to verify a firm's status in seconds.Safeguarding is the mechanism through which FCA-regulated e-money institutions protect customer funds when they are in transit between accounts. Unlike bank deposits (which are covered by FSCS), safeguarded funds must be held separately from the firm's operational funds in accounts at approved financial institutions. If the firm fails, customers have a priority claim on safeguarded funds. Wise operates under safeguarding. Revolut — now a full UK bank — operates under FSCS deposit protection for eligible deposits up to £120,000.

Fraud prevention is the other critical safety dimension. Money transfer fraud — where scammers impersonate legitimate transfer services, family members, or businesses to redirect funds — is a growing problem. The key rules: never transfer money to a recipient you have not verified through a trusted, independent channel; be suspicious of any instruction to change payment details at short notice; use the confirm-the-bank-details-by-phone rule before any transfer over £500 to a new recipient. Most reputable transfer services have 2,500+ person fraud prevention teams — Revolut's figure specifically — but the first line of defence is the sender.

AUTHORISED PUSH PAYMENT (APP) FRAUD: In 2025-2026, the Payment Systems Regulator (PSR) introduced mandatory reimbursement rules for Authorised Push Payment fraud — where victims are tricked into sending money themselves. Under these rules, UK payment service providers are required to reimburse victims of APP fraud in most cases, up to £85,000 per claim. This applies to transfers made via Faster Payments (domestic UK bank transfers). For international transfers, different rules apply and reimbursement is less certain. Always independently verify recipient details before any transfer. If you believe you have been a victim of transfer fraud, contact your provider immediately and report to Action Fraud (0300 123 2040).

How to Make an International Money Transfer: Step by Step

The practical process for making an international money transfer through a specialist provider is straightforward and typically takes less than 10 minutes to set up:- Choose your provider: Use the comparison in this guide to identify the right provider for your specific transfer type. For a standard EUR or USD transfer under £50,000, Wise or Atlantic Money. For a large property transaction, Currencies Direct or TorFX. For remittances to Asia or Africa, Remitly or WorldRemit.

- Create and verify an account: All FCA-regulated providers require identity verification (KYC) before allowing transfers. You will need to provide photo ID (passport or driving licence) and proof of address. Most providers complete verification online in minutes; some require manual review for higher-value accounts.

- Enter your transfer details: Input the amount you wish to send, the receiving currency, and compare the fee and exchange rate shown upfront. The platform will show you exactly how much the recipient will receive before you confirm — always check this total.

- Add your recipient: Enter the recipient's bank account details — name, account number, sort code (for UK), IBAN and BIC/SWIFT (for international), or routing number (for US). Double-check every digit. A single incorrect digit can delay or misdirect a transfer.

- Fund the transfer: Pay by bank transfer, debit card, or credit card (though credit card payments often attract additional fees). Bank transfer is typically the cheapest funding method.

- Track the transfer: Most providers offer real-time transfer tracking in their app or online dashboard. Keep your transfer reference number in case you need to follow up with either your provider or the recipient's bank.

Conclusion

International money transfer has been transformed by specialist digital providers over the past decade, and in 2026, the tools available to UK consumers and businesses are more powerful, cheaper, and more transparent than at any previous point. Using a traditional UK bank for international transfers now represents one of the most avoidable financial costs in personal finance — where £5,000 sent via a high street bank can cost £125 to £300 in combined fees and exchange rate markup, the same transfer through Atlantic Money costs £3, and through Wise from £20.The right provider depends on your specific use case. Wise offers the most consistent mid-market rate with full transparency for standard transfers under £50,000 across 40+ currencies. Atlantic Money is mathematically cheapest for large transfers in major currency corridors with its £3 flat fee. Revolut — now a fully licensed UK bank with FSCS protection to £120,000 — is the all-in-one financial platform for those who want budgeting, investing, and transfers in one app. Currencies Direct and TorFX provide dedicated dealer support and forward contracts for large property and emigration transfers. Remitly and WorldRemit cover developing country corridors and mobile money delivery that specialist platforms do not address. Western Union remains the global cash pickup network when bank-to-bank transfer is not an option.

The two universal rules that apply regardless of which provider you use: always compare the total amount your recipient will receive — not just the headline fee — before confirming any transfer; and always verify recipient details independently through a trusted channel before sending to a new account. The savings from using the right provider are real and significant. The cost of sending to the wrong account, or to a fraudster who has intercepted the recipient's bank details, can be devastating. Both outcomes are avoidable with five minutes of comparison and one phone call to verify.

Frequently Asked Questions (FAQ)

What is an international money transfer?

An international money transfer is the process of moving funds from a bank account or payment service in one country to a recipient in another country, typically involving a currency conversion. The three key elements are the transfer fee (what the provider charges for the service), the exchange rate (how the sending currency is converted to the receiving currency — the most significant cost on large transfers), and the delivery method (bank account, mobile money wallet, cash pickup). In the UK, specialist providers including Wise, Atlantic Money, Revolut, Currencies Direct, TorFX, and OFX all offer materially cheaper international transfers than traditional high street banks, which typically charge £25-£50 in fees plus a 2%-5% exchange rate markup.What is the cheapest way to send money abroad from the UK in 2026?

For large transfers in major currency corridors (GBP to EUR, USD, CAD, AUD), Atlantic Money offers the lowest possible cost: a £3 flat fee with the mid-market exchange rate and no markup. For smaller transfers or a wider range of currencies, Wise is typically the most cost-effective — its fees start from 0.41%, it uses the mid-market rate, and all costs are shown upfront before you confirm. Both are significantly cheaper than any UK high street bank for international transfers. For remittances to developing country corridors (India, Philippines, Africa), Remitly and WorldRemit typically offer the best combination of rate and delivery method for those specific routes.Is Wise or Revolut better for sending money abroad?

For dedicated, cost-effective international transfers, Wise generally wins on both price transparency and consistency. Wise uses the mid-market exchange rate at all times with no markup, charges an explicit percentage fee starting from 0.41%, and covers 40+ currencies and 140+ countries. Revolut is cheaper for transfers between Revolut users (instant, no fee) and free within SEPA up to plan limits, but applies a 1% weekend surcharge on currency exchange for Standard plan customers and has a £1,000/month limit before the fair usage fee applies. Revolut's broader financial platform (investing, crypto, savings) makes it the better choice for those who want one app for everything. For pure international transfer value, Wise is more predictable and usually cheaper for standard GBP-to-foreign-currency transfers above the Revolut monthly limit.Is it safe to use Wise or Revolut to transfer money?

Yes — both are FCA-regulated in the UK and use rigorous security measures. Wise holds customer funds separately from its operational accounts (safeguarding), meaning if Wise were to fail, customer funds would be protected as a priority claim. Revolut became a fully licensed UK bank on 11 March 2026, meaning eligible deposits are now covered by the Financial Services Compensation Scheme (FSCS) up to £120,000 per customer. Both have large fraud prevention teams. You can verify any money transfer provider's FCA regulatory status at fca.org.uk before sending. As with any financial service, always independently verify recipient bank details before making a transfer to a new account, particularly for large amounts.What is the difference between the transfer fee and the exchange rate markup?

These are two separate costs that both affect how much your recipient receives. The transfer fee is an explicit charge — either a flat amount (Atlantic Money's £3) or a percentage of the transfer (Wise's 0.41%+) — shown upfront. The exchange rate markup is a hidden or semi-hidden cost embedded in the exchange rate: if the mid-market rate is 1.18 EUR per GBP and the provider offers 1.14, the 0.04 difference is a 3.4% markup on your money. A provider advertising 'no transfer fees' may still be more expensive than Wise if it applies a large rate markup. Always compare the total amount your recipient will receive in their currency — not just the upfront fee — before choosing a provider. Wise's fee calculator and Atlantic Money's calculator both show this figure clearly.

External References

1. CurrencyBrokers UK — 10 Best International Money Transfer Companies in the UK 2026 (May 2026)https://www.currencybrokers.uk/blog/best-money-transfer-companies

2. Statrys — 8 Best International Money Transfer Apps 2026 (May 2026)

https://statrys.com/blog/best-international-money-transfer-apps

3. Wise — Revolut vs Wise (UK): Everything You Need to Know

https://wise.com/gb/blog/revolut-vs-wise-uk

4. Revolut — Revolut vs Wise: A Comprehensive Comparison (June 2026)

https://www.revolut.com/blog/post/revolut-vs-wise/

5. KaelTripton — Best Money Transfer Services UK 2026: Wise, Revolut and TorFX Compared (3 weeks ago)

https://www.kaeltripton.com/compare/best-money-transfer-services-uk/

6. FCA Register — Verify any UK financial firm's authorisation status

https://register.fca.org.uk/

7. Action Fraud — Report Money Transfer Fraud (0300 123 2040)

https://www.actionfraud.police.uk/

8. Payment Systems Regulator — APP Fraud Reimbursement Rules (2025-26)

https://www.psr.org.uk/our-work/app-scams/

0 Comments Comments