Real Estate

Bank of England April 2026: 5 Takeaways on Mortgages & Bills

Table of Contents

- A Hold That Says More Than It Keeps Quiet

- The Decision: 8-1 to Hold at 3.75%

- Takeaway 1: Mortgages — The Hold Buys Time, But Rates Remain High

- Takeaway 2: Energy Bills — The Bank Warns They Will Rise Further

- Takeaway 3: Jobs — The Bank Is Watching the Labour Market Closely

- Takeaway 4: Inflation — It Could Peak at 6.2% in Early 2027

- Takeaway 5: Savings — Rates Stay Competitive for Now

- What the Dissenting Vote Means

- The Key Numbers After the Decision

- When Is the Next Decision?

- Conclusion: Navigating an Uncomfortable Middle

- Frequently Asked Questions

- External References

A Hold That Says More Than It Keeps Quiet

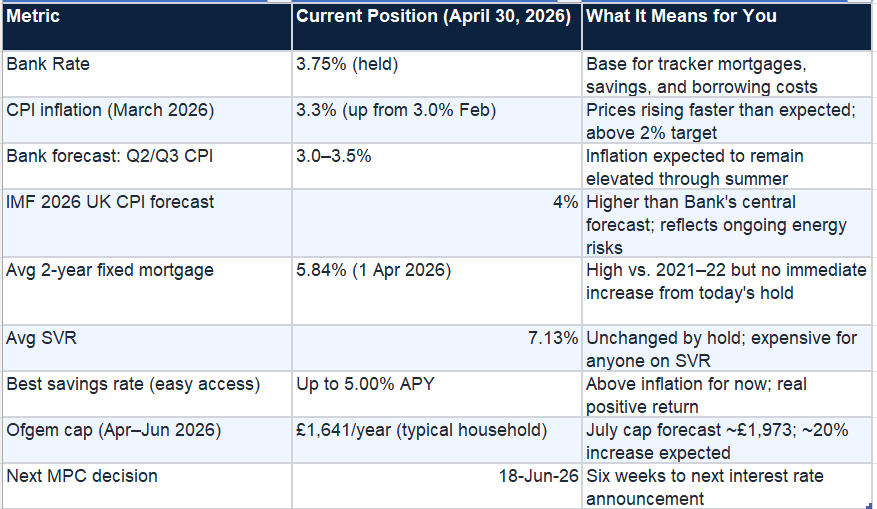

On Thursday 30 April 2026, the Bank of England's Monetary Policy Committee (MPC) met for the fourth time this year and voted, by eight votes to one, to hold the Bank Rate at 3.75 percent. The decision itself — a hold — was exactly what the majority of economists had expected. But the context, the vote split, the revised inflation forecasts, and the language the Bank used to explain its thinking tell a more complicated story about where the UK economy is heading.The hold comes against a backdrop of rising inflation (3.3 percent in March 2026, up from 3.0 percent in February), surging energy prices driven by the US-Iran conflict that began on 28 February, and an economic outlook that was already fragile before the external shock arrived. The Bank cut rates three times in the second half of 2025, lowering the base rate from 5.25 percent to 3.75 percent. Those cuts were predicated on an inflation path that was expected to fall toward 2 percent by spring 2026 and stay there. That path has been disrupted.

This article sets out five key takeaways from the April 30 decision — what it means for mortgages, for energy bills, for jobs, for the inflation outlook, and for savings — in plain language, drawing on the MPC's own statements, MoneySavingExpert's analysis, HomeOwners Alliance, and MoneyWeek's live coverage of the decision.

The Decision: 8-1 to Hold at 3.75%

The MPC voted eight to one to hold the Bank Rate at 3.75 percent at the April 30, 2026 meeting. The majority voted to hold, adopting what the HomeOwners Alliance described as a wait-and-see approach to the Middle East conflict and its inflationary effects.The sole dissenter was Huw Pill, the Bank's chief economist and executive director. Pill voted to raise the Bank Rate by 0.25 percentage points to 4 percent. His justification, reported by MoneyWeek, was that higher energy prices had the potential to create second-round effects that could raise UK inflation persistently. Second-round effects occur when workers seek higher wages to compensate for higher living costs, and when firms raise prices further to protect profit margins — a self-reinforcing cycle that can embed inflation well beyond the initial external shock.

This 8-1 vote split is significant. An 8-1 majority is a decisive hold, but the presence of the Bank’s own chief economist as a dissenter signals that the case for a rate rise is being taken seriously within the institution, not just among external commentators. Financial markets have been pricing in at least one rate rise before the end of 2026, though as of April 30, this probability has eased somewhat.

MPC Statement, 30 April 2026: CPI inflation has increased to 3.3%, and is likely to be higher later this year as the effects of higher energy prices feed through to household bills and business costs. The Committee is monitoring the situation very closely. Whatever happens, the Bank will make sure that inflation gets back to the 2% target in the medium term.

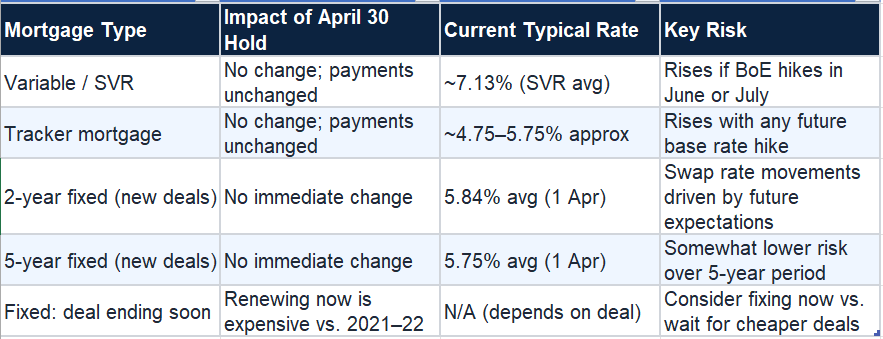

Takeaway 1: Mortgages — The Hold Buys Time, But Rates Remain High

The most immediate practical question for the millions of UK households with mortgages is: what does this mean for my payments? The short answer is that the hold provides relief from an immediate increase, but the picture for mortgage rates over the coming months remains uncertain.The Bank Rate directly affects variable and tracker mortgages, which move up or down when the base rate changes. The hold at 3.75 percent means these products are unchanged. The average standard variable rate (SVR) in April 2026 was approximately 7.13 percent. Tracker mortgages typically sit around 1 to 2 percent above the base rate, currently yielding rates of approximately 4.75 to 5.75 percent.

Fixed-rate mortgages are priced from swap rates — the wholesale market instruments that reflect where financial markets expect base rates to average over the fixed term. These had already risen sharply before the April 30 decision, driven by the swap rate movements following the Iran conflict in late February and March. The average 2-year fixed rate was 5.84 percent as of 1 April 2026, up from approximately 4.83 percent before the conflict. The April 30 hold does not automatically lower these rates — that would require swap rates to fall, which requires markets to expect future rate cuts.

David Hollingworth, associate director at broker L&C Mortgages, commented: the hold should be good news for borrowers on variable rates, who avoid any immediate increase in payments. However, he noted that the heightened expectation of rates rising or staying higher for longer means the broader mortgage market remains under pressure.

Takeaway 2: Energy Bills — The Bank Warns They Will Rise Further

The Bank's own statement on April 30 was explicit about energy bills: the war in the Middle East is disrupting the transportation and supply of energy, and the Bank expects utility bills to increase as a result. This is not speculation — it is a forecast embedded in the Bank’s revised economic projections.The mechanism is the Ofgem price cap, which is reviewed quarterly. The April to June 2026 price cap is £1,641 for a typical dual-fuel household. Based on wholesale gas prices following the Iran conflict, forecasts for the July 2026 cap had risen to approximately £1,973 — a 20 percent increase. If confirmed, this will add approximately £332 to the typical household's annual energy bill from July.

The Bank also warned that energy price rises will have knock-on effects across the economy: as businesses' bills go up, they are likely to increase their own prices to cover the cost. This cascade — from wholesale energy prices, to business operating costs, to consumer goods and services prices — is what makes energy price shocks so persistent in their inflationary effect.

For households, the practical message from the Bank’s April statement is to prepare for higher bills from July, rather than wait for the July announcement as confirmation. Households on standard variable tariffs should check whether any fixed energy tariffs are available below the expected July cap, as the window to lock in pre-cap prices may be narrow.

Takeaway 3: Jobs — The Bank Is Watching the Labour Market Closely

The Bank’s April statement did not announce specific new forecasts for employment, but its language makes clear that the labour market is central to its concern about second-round inflation effects. The specific risk is wage-price spiral dynamics: workers demand higher wages to compensate for higher energy and food bills, employers pass on higher wage costs through prices, which creates further inflation, which creates further wage demands.This was Huw Pill’s specific stated justification for voting to raise rates: the potential for second-round effects to raise inflation beyond the near term in a persistent manner. The Bank watches services inflation particularly closely as a gauge of domestic labour cost pass-through — services inflation was 4.5 percent in March 2026, up from 4.3 percent in February, suggesting some momentum.

Former chief economist of the Bank Andy Haldane, quoted by HomeOwners Alliance, offered a contrasting perspective: for now, growth in the economy calls for lower interest rates, not higher ones. This tension — between the inflation risk that Pill cited and the growth risk that Haldane identified — is the core dilemma the MPC is navigating. A rate rise controls inflation but slows the economy and increases unemployment risk. A rate cut or hold protects growth and jobs but risks letting inflation embed further.

For workers, the practical implication is that the Bank will be watching wage settlement data over the coming months, and that wage growth well above productivity is likely to keep the Bank's finger closer to the rate hike button than it has been since before the 2025 cutting cycle began.

Takeaway 4: Inflation — It Could Peak at 6.2% in Early 2027

The single most alarming number in the Bank’s April 30 projections is the inflation forecast for early 2027. The MPC’s report, published alongside the decision, indicates that under a specific scenario, inflation could hit a peak of 6.2 percent at the start of 2027. This is reported by MoneyWeek as part of the MPC’s scenario analysis rather than its central forecast, but it represents the upper bound of credible outcomes if the Iran conflict escalates and energy prices remain elevated.The IMF has separately forecast UK CPI to reach 4 percent in 2026 — more than twice the Bank of England’s 2 percent target. The Bank’s own central forecast in March projected 3 to 3.5 percent for Q2 and Q3 2026. MoneyWeek reports that under Scenario A, inflation rises to 3.6 percent at end-2026, and under Scenario B, to 3.7 percent by year end.

The Bank’s April 30 statement was explicit that inflation is likely to be higher later this year than its pre-conflict projections expected. It acknowledged that energy price rises will have knock-on effects into business prices and potentially wages. It committed to ensuring inflation gets back to the 2 percent target in the medium term — the phrase that always means rates may need to rise if needed to prevent expectations becoming unanchored.

Bank of England, April 30 2026: Monetary policy cannot affect global energy prices. Our job is to make sure that higher inflation does not persist and have long-lasting effects on the economy. We are monitoring the situation very closely and will do what is necessary.

Takeaway 5: Savings — Rates Stay Competitive for Now

The hold at 3.75 percent is good news for savers in the immediate term. The decision to hold means high-yield savings accounts (HYSAs), cash ISAs, and fixed-term savings bonds remain at their current rates for at least the next six weeks until the June 18 decision.MoneySavingExpert noted that the decision to hold means nothing major is likely to happen to savings account rates in the immediate term. The best easy-access savings accounts were offering up to 5.00 percent APY as of late April 2026 — still above headline CPI inflation of 3.3 percent, meaning cash savings are currently providing real positive returns after inflation. This is a notable and historically unusual situation.

However, the savings rate environment is not guaranteed to last. If the Bank raises rates in June or later, savings rates would typically follow upward, which is beneficial for savers. If the Bank eventually returns to cutting — as it was doing before the Iran conflict — savings rates would fall. The direction depends entirely on the inflation trajectory.

The practical action for savers: if you are holding significant cash on rates below the best available market rates, act now. The period of above-inflation savings rates is finite and the window to lock into competitive rates is open today. Fixed-rate bonds and cash ISAs allowing you to fix for six to twelve months at current rates are worth considering if you believe the next move in rates is down.

What the Dissenting Vote Means

The 8-1 vote with Huw Pill dissenting in favour of a hike is worth examining in some detail. An MPC dissent by the Bank’s chief economist is not a casual event. Pill is one of the most technically sophisticated members of the committee and his view on second-round inflationary effects reflects a genuine risk that the majority — while acknowledging — has chosen not to act on yet.The majority’s reasoning, implicit in the hold, is that the current inflation spike is primarily supply-driven and external. Raising rates now would slow the economy without solving the root cause (global energy prices). The Bank explicitly acknowledges: monetary policy cannot affect global energy prices. The hold buys time to see whether the Iran conflict de-escalates, whether energy prices normalise, and whether domestic inflation components (wages and services) remain contained.

Financial markets have noted the dissent. As MoneyWeek reported, traders initially priced in two potential rate hikes before year end, which has since eased to one. The 10-year gilt yield rose above 5 percent for the first time since 2008 in the days surrounding the decision — a market signal of concern about the UK's fiscal and inflationary position that has direct implications for the cost of government borrowing and, ultimately, taxes and public services.

The Key Numbers After the Decision

When Is the Next Decision?

The next Bank of England interest rate decision will be announced on Thursday 18 June 2026. The June meeting will be accompanied by the full Monetary Policy Report — a quarterly publication that contains the Bank’s detailed economic forecasts, scenarios, and analytical framework. This makes it a particularly significant decision, as it will include updated projections reflecting what has happened to energy prices, wage data, and economic activity in the six weeks since April 30.Between now and June 18, the key data releases to watch are:

- ONS April 2026 CPI data (due mid-May): will show whether inflation continued to rise in April, and how much of the fuel price spike has already fed through.

- Average weekly earnings data: the Bank watches wage growth closely for second-round effects; an acceleration in private sector wage settlements would strengthen the case for a rate rise.

- April UK GDP estimate: growth data will influence whether the MPC leans toward prioritising inflation control (hike) or growth support (hold or cut).

- Ofgem July price cap announcement: expected approximately six weeks before July, meaning an announcement around mid-May, which will give the MPC its most concrete data point on the energy bill trajectory.

Conclusion

The Bank of England’s April 30 hold at 3.75 percent places it in an uncomfortable middle position. It is neither cutting rates to support economic growth, as it was doing three months ago, nor raising rates to aggressively combat inflation. It is watching, waiting, and keeping its options open — while an external shock whose duration and severity it cannot control continues to drive UK prices higher.For households, the practical implications of the April 30 decision are specific and actionable. Mortgage holders on variable rates avoided an immediate payment increase. Those renewing fixed-rate deals face market rates that remain significantly higher than three years ago but should not wait indefinitely on the assumption that rates will fall quickly. Energy bill payers should prepare for the July cap increase rather than wait for it to arrive. Savers should ensure they are on competitive rates while the current environment persists.

The MPC will meet again on 18 June. By then, it will have April inflation data, April wage data, and the Ofgem July cap announcement. Those three data points will tell the Bank — and markets, mortgage lenders, and households — more than any forecast can. For now, 3.75 percent holds.

Frequently Asked Questions

What did the Bank of England decide on 30 April 2026?

The Bank of England's Monetary Policy Committee voted eight to one to hold the Bank Rate at 3.75% on 30 April 2026. The sole dissenter was Huw Pill, the Bank's chief economist, who voted to raise rates by 0.25 percentage points to 4%. The decision was widely expected. The Bank cited the Iran conflict's impact on energy prices and inflation as the primary factor affecting its outlook, warning that inflation is likely to be higher later in 2026 than previously predicted.What does the Bank Rate hold mean for my mortgage?

If you are on a variable or tracker mortgage, the hold means your payments are unchanged for now. The average SVR remains approximately 7.13% and tracker mortgages move directly with the base rate. If you are on a fixed-rate mortgage, today's decision does not change your rate — your rate is fixed for the duration of your deal. For those looking to take out or renew a fixed rate, rates remain elevated (2-year fix averaging 5.84% as of April 2026) because mortgage lenders price from swap rates, which reflect future Bank Rate expectations and have already risen significantly since the Iran conflict began.Why did Huw Pill vote to raise rates at the April 2026 MPC meeting?

Huw Pill, the Bank's chief economist, voted to raise rates by 0.25% to 4% because he was concerned about second-round inflationary effects from the energy price shock. Second-round effects occur when workers ask for higher wages to compensate for higher energy and food costs, and when businesses raise their prices further to protect profit margins. Pill's view was that these dynamics had the potential to raise UK inflation persistently beyond the near-term spike, warranting a rate increase rather than a hold.What is the Bank of England's inflation forecast for 2026?

The Bank's March MPC statement projected CPI of 3 to 3.5% in Q2 and Q3 2026. The April 30 statement confirmed inflation is likely to be higher later in 2026. MoneyWeek reports that the MPC's scenario analysis includes a path where inflation peaks at 6.2% in early 2027 under a more severe energy price scenario. The IMF separately forecasts UK CPI at 4% for 2026 — more than double the Bank's 2% target.What will happen to energy bills in 2026?

The Bank of England warned on 30 April that it expects utility bills to increase as a result of the Iran conflict's impact on energy markets. Based on wholesale gas prices in March and early April 2026, forecasts for the July 2026 Ofgem energy price cap stood at approximately £1,973 for a typical household — around 20% above the April 2026 cap of £1,641. This would add approximately £332 per year to the average household's energy bill from July. The cap will be confirmed by Ofgem approximately six weeks before July.When is the next Bank of England interest rate decision?

The MPC will announce its next interest rate decision on Thursday 18 June 2026. The June meeting is a Monetary Policy Report meeting, meaning it will be accompanied by updated economic forecasts and scenario analysis. Key data that will inform the June decision includes April CPI data (due mid-May), April wage data, April GDP, and the Ofgem July price cap announcement (expected around mid-May).Will UK interest rates go up or down in 2026?

As of 30 April 2026, market expectations are broadly split between rates staying at 3.75% and one rise of 0.25% by year end. Following the Iran conflict, two potential hikes had been priced in by some market participants but this has eased to approximately one. Former Bank chief economist Andy Haldane has argued that growth considerations call for rate cuts rather than hikes. Chief economist Huw Pill's dissenting vote suggests the Bank is genuinely divided. The outcome will depend on the inflation trajectory over the next few months and the trajectory of the Iran conflict.External References and Further Reading

Bank of England — What Is Happening with Interest Rates in the UK? (Updated 30 April 2026), Bank of England — Interest Rates and Bank Rate: Our Latest Decision (30 April 2026), MoneySavingExpert — Base Rate Held Again at 3.75%: What It Means for You (30 April 2026), MoneyWeek — UK Interest Rates: Bank of England Holds at 3.75% (Live Blog, April 2026), HomeOwners Alliance — Will the Bank of England Cut Interest Rates on 30 April 2026? (Updated), House of Commons Library — Inflation in the UK: Economic Indicators (Updated April 2026), Resolution Foundation — The Macroeconomic Policy Outlook Q2 2026 (April 2026), ONS — Consumer Price Inflation, UK: March 2026, Ofgem — Energy Price Cap: Current and Upcoming Levels, MoneySavingExpert — Best Savings Accounts and Highest Interest Rates (Updated Daily)

0 Comments Comments