Real Estate

Parents Buying Homes for Kids With Strings Attached

Table of Contents

- The Scale of the Trend: How Common Is Family-Funded Homeownership?

- Why Parents Are Stepping In Now

- The 'Strings Attached': Five Ways Parents Are Structuring Help

- 1. The Outright Gift

- 2. The Intra-Family Loan

- 3. Co-Ownership

- 4. Parent Buys Outright, Child Lives Rent-Free or at Reduced Rent

- 5. Trust-Held Property

- The Emotional Side: Gratitude, Embarrassment, and Family Dynamics

- Should You Do It? A Practical Decision Framework

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

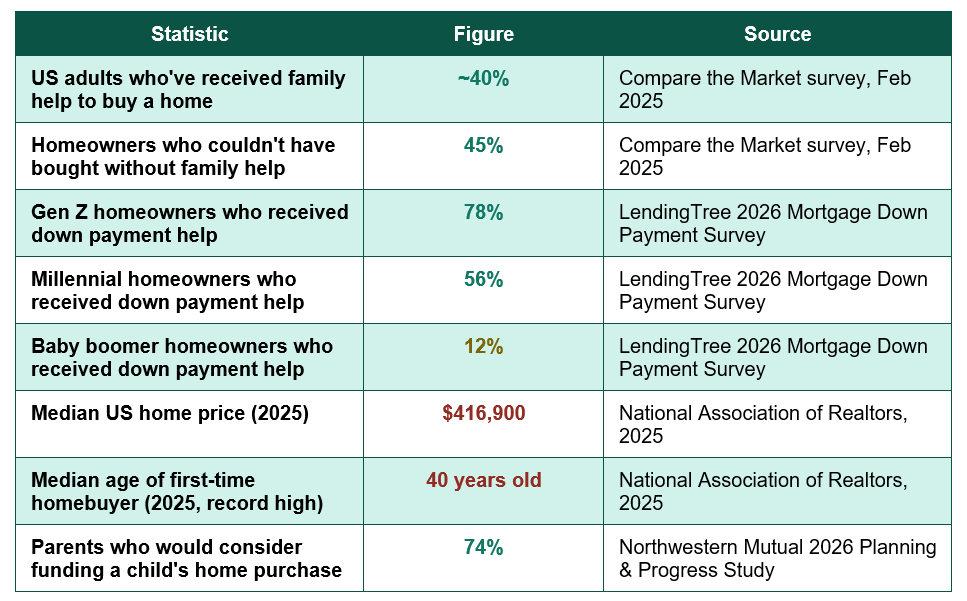

"I save and I can afford a couch, but I can't afford a house." That single line, from a young American renter describing her budgeting reality, captures why an entire industry of family-funded homeownership has quietly become mainstream. Across the United States, the so-called 'Bank of Mom and Dad' has become one of the most significant — and least discussed — forces shaping who can buy a home and when, with nearly 40% of US adults now reporting they received some form of family financial help to purchase property.

This is not a marginal trend confined to the wealthy. According to a February 2025 survey commissioned by Compare the Market, 45% of Americans who received family assistance say they could not have bought a home without it. Among Gen Z homeowners specifically, LendingTree's 2026 survey found that 78% received some form of financial help with their down payment, most commonly from parents — and a third of all recipients say the purchase simply would not have happened otherwise. As median home prices have climbed to $416,900 against a median household income of roughly $83,150, family assistance has shifted from a generous bonus to, for a large share of buyers, a genuine prerequisite.

But the financial assistance increasingly comes with structure — gift agreements, co-ownership arrangements, repayment expectations, or conditions tied to specific behaviours or milestones. This guide examines exactly how widespread parent-funded homeownership has become, the different structures parents are using (each with very different legal, tax, and relational implications), the genuine risks on both sides of the arrangement, and a practical framework for deciding whether, and how, this approach makes sense for your own family.

The Scale of the Trend: How Common Is Family-Funded Homeownership?

The data confirms that family assistance has become deeply embedded in how Americans, particularly younger Americans, actually buy homes today:

Generational gap in family assistance: 78% (Gen Z) vs 12% (Boomers) — younger buyers are roughly six and a half times more likely than baby boomers to have received family help with their down payment, reflecting how dramatically the affordability equation has shifted across generations (LendingTree 2026)

- Why now, specifically: the typical first-time homebuyer in the US is now 40 years old — a record high, up from 33 just five years ago — while the share of all home purchases made by first-time buyers fell to just 21% in 2025, the lowest since records began in 1981. Real estate agents increasingly describe a 'two-speed market,' in the words of one Douglas Elliman broker, where buyers with family wealth behind them move faster and more decisively, while those without it face longer timelines and more compromise on price, location, or size.

Why Parents Are Stepping In Now

The structural case for family assistance is straightforward arithmetic. The salary required to comfortably afford a median-priced home has roughly doubled between 2017 and 2025, while wage growth over the same period has fallen well short of keeping pace. Younger buyers face a particular disadvantage that previous generations did not: without an existing home to sell, they cannot draw on built-up equity, leaving personal savings and investments as the only source of a down payment — a much harder bar to clear when starting from zero.Parents, for their part, increasingly see this as both an emotional priority and a deliberate wealth-transfer strategy. Northwestern Mutual's 2026 Planning & Progress Study found that 74% of parents would consider, or are already planning, financially supporting a child's home purchase — and notably, 29% of those parents say helping a child buy a home is now more important to them than helping pay for college, a meaningful reordering of traditional family financial priorities.

The scale of typical contributions has grown accordingly. A Veterans United Home Loans survey found that most contributing parents expect to give between $25,000 and $49,999, while 23% plan to give between $50,000 and $99,999, and 12% expect to contribute between $100,000 and $199,999 — sums that, particularly at the higher end, represent genuine, carefully considered financial planning decisions rather than casual generosity.

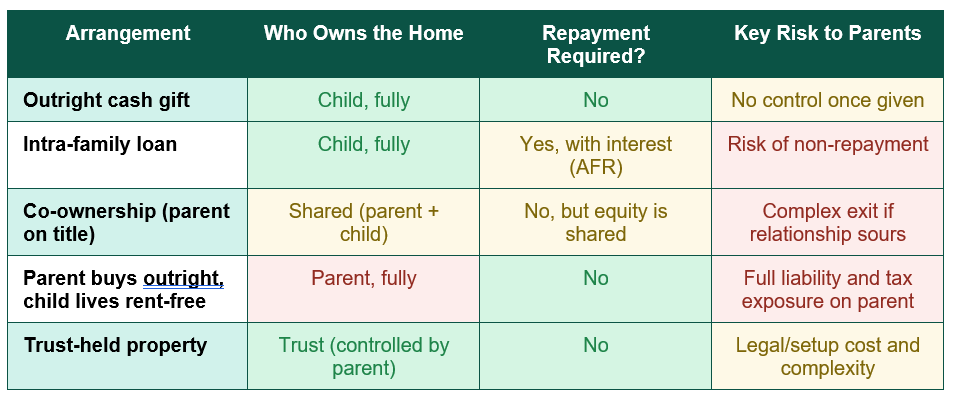

The 'Strings Attached': Five Ways Parents Are Structuring Help

The phrase 'with strings attached' reflects a genuine and important reality: the way family assistance is structured varies enormously, and each structure carries different legal status, tax treatment, and risk profile for both generations. The table below summarises the five most common approaches:

1. The Outright Gift

The simplest and most common structure is a straightforward cash gift toward the down payment, with no expectation of repayment. For 2026, an individual can gift up to $19,000 per recipient without using any of their lifetime estate and gift tax exemption; a married couple can together gift $38,000 to a single recipient, or effectively $76,000 if gifting separately to a married child and their spouse. Amounts above this annual exclusion simply draw down part of the giver's lifetime exemption, which sits at a generous $15 million per individual in 2026 following the One Big Beautiful Bill Act — meaning most families have substantial room before any actual gift tax becomes due.From a mortgage underwriting standpoint, gifts are typically the cleanest option: lenders are well accustomed to standard 'gift letter' documentation confirming the funds are a genuine gift with no repayment expectation, which is required precisely because undisclosed loans masquerading as gifts can distort a lender's assessment of the buyer's true debt obligations.

The 'string' on a pure gift: once money is gifted, it is legally no longer the parent's asset, meaning they retain no formal control over how it is ultimately used, and no legal right to its return if the marriage or relationship the home was intended to support later breaks down. Financial advisers increasingly recommend that families discuss expectations explicitly even where no formal legal mechanism enforces them.

2. The Intra-Family Loan

Rather than gifting funds outright, some parents structure their assistance as a formal loan, requiring repayment over time, typically at an interest rate at or above the IRS's Applicable Federal Rate (AFR) to avoid the loan being reclassified as a gift for tax purposes. This structure preserves the parents' claim to eventual repayment and can be documented with a promissory note, giving it genuine legal standing distinct from an informal family understanding.The genuine risk here sits with the parents: family loans frequently go partially or entirely unrepaid, particularly if the recipient encounters financial hardship, and pursuing formal collection against one's own child carries an obvious emotional cost that most parents are unwilling to bear in practice, even when the original agreement was clear.

3. Co-Ownership

Under this structure, the parent is added to the property title as a co-owner, providing capital in exchange for a genuine, documented ownership stake rather than a gift or loan. This arrangement gives parents a clear, legally enforceable claim on a share of the property's value, and can be structured to automatically convert to full child ownership after a defined period or upon specific conditions being met.The complexity here is real: co-ownership typically requires a formal agreement covering maintenance costs, what happens if the child wants to sell, how disputes are resolved, and the tax implications of eventually transferring the parent's share — making this the structure most likely to require dedicated legal drafting rather than a simple letter.

4. Parent Buys Outright, Child Lives Rent-Free or at Reduced Rent

In this arrangement, the parent purchases and retains full ownership of the property, while the adult child lives there rent-free or at a below-market rate. This preserves maximum control for the parent — they can sell, refinance, or change the arrangement unilaterally — but it also means the parent carries full liability for the mortgage, property taxes, insurance, and maintenance, along with the income tax implications of any rent actually charged below market rate, which the IRS can treat partially as a taxable gift.5. Trust-Held Property

For families with more complex estate planning goals, holding the property within a trust — with the parent as trustee or grantor — provides significant control and flexibility, including the ability to specify conditions under which the child gains greater ownership rights over time, protection from the child's potential creditors or divorce proceedings, and a clear mechanism for eventual transfer as part of broader estate planning. This is typically the most expensive and legally involved structure of the five, usually justified only for higher-value properties or families already engaged in broader estate planning.The Emotional Side: Gratitude, Embarrassment, and Family Dynamics

The financial mechanics of family-funded homeownership are only part of the picture. LendingTree's 2026 survey found that while 46% of recipients felt grateful for the assistance, 21% of Gen Z recipients specifically reported feeling embarrassed about needing the help — more than twice the 9% rate reported among millennials, suggesting the youngest generation of buyers carries more social stigma around family assistance even as it becomes increasingly statistically normal.This tension is worth taking seriously in any family discussion about assistance. Financial advisers who specialise in this area consistently emphasise that the most successful arrangements are those built around clear, explicit expectations discussed openly in advance — whether that means a formal gifting letter, a defined co-ownership agreement, or simply a candid family conversation about what is and is not expected in return. Ambiguity, more than the assistance itself, is what most reliably damages family relationships when these arrangements eventually face a test, such as a relationship breakdown, a job loss, or a disagreement about the property's future.

Fairness consideration for families with multiple children: A frequently overlooked issue — financial planners increasingly advise parents helping one child buy a home to document the gift clearly and consider how to treat other children equitably, either through comparable gifts, adjusted inheritance planning, or open family conversation about the reasoning — since unaddressed disparities are a common source of long-term family friction

Should You Do It? A Practical Decision Framework

For parents weighing whether and how to help an adult child buy a home, the following framework reflects the consistent guidance of financial planners working in this specific area:- Protect your own retirement security first: The single most consistent piece of advice from financial advisers is that assistance should never come at the cost of the parents' own retirement adequacy. Run your own retirement projections with and without the planned gift or loan before committing, and be honest about whether the assistance is genuinely affordable or simply aspirational.

- Choose the structure that matches your actual goals: A pure gift suits parents who want simplicity and are comfortable relinquishing control entirely. A loan suits parents who want their capital eventually returned. Co-ownership or a trust suits parents who want an ongoing stake in the property's value or specific conditions attached to the assistance. Be honest with yourself about which outcome you actually want before choosing a structure.

- Document everything in writing, regardless of how informal the relationship feels: Even a simple, friendly letter specifying whether funds are a gift or loan, and on what terms, provides crucial clarity for mortgage underwriting, tax reporting, and family record-keeping — and meaningfully reduces the risk of future misunderstanding or conflict.

- Consider fairness across all your children, not just the one buying now: If you have multiple children, think through, and ideally discuss openly, how this assistance fits into your broader plans for treating them equitably over time, whether through comparable future gifts, inheritance planning, or a clear, shared rationale for any difference in treatment.

- Get professional advice for any structure beyond a simple gift: Co-ownership agreements, intra-family loans at the AFR, and trust structures all carry genuine legal and tax complexity that a qualified estate planning attorney, tax advisor, and financial planner should review before implementation — the cost of professional advice is minor compared to the cost of an poorly structured arrangement.

Conclusion

Parents buying homes for their adult children, in one structure or another, has moved decisively from the exception to a genuinely mainstream feature of American homeownership. With nearly 40% of adults reporting family assistance, 78% of Gen Z homeowners having received help, and median home prices requiring a salary that has roughly doubled since 2017 while wages have lagged, the economic case for family involvement is, for many households, simply a reflection of present-day arithmetic rather than a lifestyle choice.The 'strings attached' framing in the popular conversation around this trend is not a criticism — it reflects a genuinely healthy evolution in how families are approaching these arrangements, moving away from undocumented, ambiguous generosity and toward structured gifts, loans, co-ownership agreements, and trusts that protect both generations and reduce the risk of the assistance becoming a source of future conflict. The right structure depends entirely on what each family is actually trying to achieve: simplicity and full relinquishment of control favours a gift; preserving an eventual return of capital favours a loan; an ongoing stake in the property favours co-ownership or a trust.

For families considering this path, the most important step is not choosing a structure quickly, but having an honest, explicit conversation about expectations, protecting the parents' own financial security as the non-negotiable first priority, and seeking qualified professional advice for any arrangement more complex than a simple, properly documented gift. Done this way, family-funded homeownership can be exactly what Northwestern Mutual's chief field officer described it as: a genuine bridge to the American dream and to generational wealth — rather than a source of confusion or resentment further down the line.

Frequently Asked Questions (FAQ)

How much can I gift my child for a down payment without paying gift tax?

In 2026, you can gift up to $19,000 per recipient without using any of your lifetime gift and estate tax exemption. A married couple can together gift $38,000 to a single recipient by 'splitting' the gift, and if your child is married, you can gift separately to your child and their spouse, allowing a married couple to give up to $76,000 in a single year without touching their lifetime exemption. Amounts above this simply draw down part of your lifetime exemption, which is a generous $15 million per individual in 2026, meaning most families will not owe any actual gift tax even on larger gifts, though amounts over the annual exclusion must still be reported to the IRS.What's the difference between a gift letter and an intra-family loan for mortgage purposes?

A gift letter confirms to the mortgage lender that the funds provided have no expectation of repayment, which is important because lenders need to assess the buyer's true ongoing debt obligations accurately. An intra-family loan, by contrast, does create a repayment obligation and, if not properly disclosed, can distort a lender's underwriting decision. If you intend the assistance to be a loan, it should generally be disclosed as such, properly documented with a promissory note, and structured with an interest rate at or above the IRS's Applicable Federal Rate to avoid being reclassified as a gift for tax purposes.Will helping my child buy a home affect my own mortgage or retirement plans?

It can, which is why financial planners consistently advise running your own retirement and cash flow projections, both with and without the planned assistance, before committing. Gifting a large sum can reduce your investable assets and the income or growth they would otherwise generate, while taking out a loan or home equity line of credit yourself to fund the gift adds a new, ongoing obligation to your own budget. The assistance should never be structured in a way that jeopardises your own long-term financial security, however well-intentioned the gesture.Is co-ownership a good idea if I want to help my child buy a home?

Co-ownership can be a good fit if you want an ongoing, legally documented stake in the property's value rather than simply giving the money away, or if you want specific conditions attached to your contribution. However, it introduces real complexity: you will need a clear written agreement covering responsibilities for maintenance and costs, what happens if your child wants to sell or if the relationship underlying the purchase (such as a marriage) ends, and the tax implications of eventually transferring your share. This structure is generally best pursued with the guidance of an estate planning attorney rather than as an informal family arrangement.How do I handle fairness if I can only afford to help one of my children buy a home right now?

This is a genuinely common and sensitive issue. Many financial planners recommend documenting the assistance clearly as either a gift or an advance against inheritance, and having an open conversation with all your children about your reasoning and your plans for treating them comparably over time, whether through similar future gifts, adjusted estate planning, or another approach that reflects your family's values. Leaving this unaddressed is one of the more common sources of long-term family conflict that advisers in this space see, often emerging only years later when a will or estate is being settled.

External References

The following sources informed this article and are recommended for further reading:1. National Association of Realtors — 2025 Profile of Home Buyers and Sellers

https://www.nar.realtor/research-and-statistics/research-reports/highlights-from-the-profile-of-home-buyers-and-sellers

2. LendingTree — 2026 Mortgage Down Payment Survey

https://www.lendingtree.com/home/mortgage/down-payment-help-survey/

3. Northwestern Mutual — 2026 Planning & Progress Study

https://news.northwesternmutual.com/planning-and-progress-study

4. Compare the Market — US Family Home-Buying Assistance Survey, Feb 2025

https://www.livenowfox.com/news/family-money-help-buy-house-survey

5. American Century Investments — Rules for Gifting Money to Family for a Down Payment in 2026

https://www.americancentury.com/insights/gifting-home-down-payment-child/

6. IRS — Frequently Asked Questions on Gift Taxes

https://www.irs.gov/businesses/small-businesses-self-employed/frequently-asked-questions-on-gift-taxes

7. Redfin — Homebuyers With Kids Twice as Likely to Get Family Help for Down Payments

https://www.redfin.com/news/homebuyers-kids-family-help-survey/

8. Moneywise — Why More Parents Are Buying Homes for Their Adult Kids

https://moneywise.com/mortgages/parents-kids-homeownership-family-mortgage-housing-affordability

0 Comments Comments