Vehicles & Cars

UK Car Loan Firms Accept £9bn Mis-Selling Redress Deal

TABLE OF CONTENTS

- What Is the Car Finance Mis-Selling Scandal?

- How Did the Mis-Selling Work?

- The Road to the £9bn Redress Scheme

- Which Lenders Have Accepted the Scheme?

- Who Is Eligible to Claim?

- How Much Compensation Could You Receive?

- How to Make Your Claim — Step by Step

- Key Dates and Deadlines

- Risks, Legal Challenges and What Comes Next

- Conclusion

- Frequently Asked Questions

- References

What Is the Car Finance Mis-Selling Scandal?

The UK car finance mis-selling scandal is the largest consumer financial scandal since the Payment Protection Insurance (PPI) affair, which ultimately cost lenders more than £50 billion in compensation payouts over more than a decade. Like PPI, the car finance scandal centres on hidden charges and arrangements that were not properly disclosed to customers — in this case, commission arrangements between car dealerships and lenders that inflated the cost of borrowing without the buyer's knowledge.Between 6 April 2007 and 1 November 2024, millions of UK consumers took out Personal Contract Purchase (PCP) or Hire Purchase (HP) agreements when buying a car. In a significant proportion of those deals — the Financial Conduct Authority (FCA) estimates around 37% of all agreements in that period — the commission structure used was either undisclosed, excessively high, or operated under arrangements that created a conflict of interest that was never explained to the customer.

On 30 March 2026, the FCA published its final rules for a mandatory industry-wide redress scheme under policy statement PS26/3. Major lenders have since confirmed they will not challenge the scheme, paving the way for what the regulator expects will be millions of compensation payments in 2026 and the vast majority of claims resolved by the end of 2027.

How Did the Mis-Selling Work?

To understand why compensation is owed, it helps to understand precisely how the commission arrangements worked — and why they were harmful to consumers.Discretionary Commission Arrangements (DCAs)

The most prevalent form of mis-selling involved what the FCA calls Discretionary Commission Arrangements. Under a DCA, a car dealer acting as a credit broker had the power to set — or adjust upward — the interest rate charged to the customer. The higher the interest rate, the more commission the dealer received from the lender. This created a direct financial incentive for dealers to charge customers the highest interest rate they could justify, regardless of the customer's creditworthiness.Customers were not told about this arrangement. They reasonably assumed their interest rate had been set by the lender based on their credit profile. In reality, it had often been inflated by the dealer to earn more commission. The FCA estimates this practice affected around 10.6 million agreements and that consumers paid approximately £500 million more per year in excess interest costs than they would have done under flat commission rates. DCAs were banned by the FCA in January 2021.

High Commission Arrangements

A second category of mis-selling covers agreements where the commission paid to the broker was excessively high — specifically, where it amounted to at least 39% of the total cost of credit and at least 10% of the loan amount — and where this was not disclosed to the customer. Even without the discretionary element, the FCA found that undisclosed high commissions of this nature were unfair to consumers.Contractual Ties

A third category covers cases where a lender had given a dealership exclusive or preferential rights — for example, a right of first refusal on financing deals — that the customer was not told about. This deprived customers of the opportunity to shop around for a better finance rate, as they were being channelled toward a specific lender without their knowledge.Courts have found that firms broke the law by failing to disclose important information to customers. An industry-wide scheme is the quickest and most cost-effective way to deliver fair compensation.

— FINANCIAL CONDUCT AUTHORITY, MARCH 2026

The Road to the £9bn Redress Scheme

The FCA first announced a formal investigation into motor finance commission practices in January 2024. The investigation was triggered by a surge in consumer complaints — many prompted by awareness raised through MoneySavingExpert.com's free complaint tool — and by growing evidence that undisclosed commission arrangements had been widespread across the industry for many years.In October 2024, the Court of Appeal ruled in a landmark judgment that undisclosed commission arrangements in car finance deals were potentially unlawful, and that consumers had a right to seek redress. The Supreme Court affirmed the position in August 2025, confirming that non-disclosure of commission and excessive commission charges could render a car finance agreement unfair and give consumers a right to compensation.

On 7 October 2025, the FCA launched its formal consultation on a proposed mass redress scheme, estimating at that stage that around £8.2 billion would be paid on approximately 14 million agreements. Following an extensive consultation period in which the regulator received over 1,000 responses from lenders, consumer groups, legal representatives, manufacturers, and industry bodies, the FCA published its final rules in PS26/3 on 30 March 2026.

The final scheme differs from the consultation proposal in several important ways. The number of covered agreements was reduced from approximately 14 million to 12.1 million, reflecting tighter eligibility criteria designed to ensure only those genuinely treated unfairly would receive compensation. The average estimated payout was revised upward from £700 to £829. The total consumer redress figure was set at £7.5 billion, with the total scheme cost — including administration and complaints handling — reaching £9.1 billion.

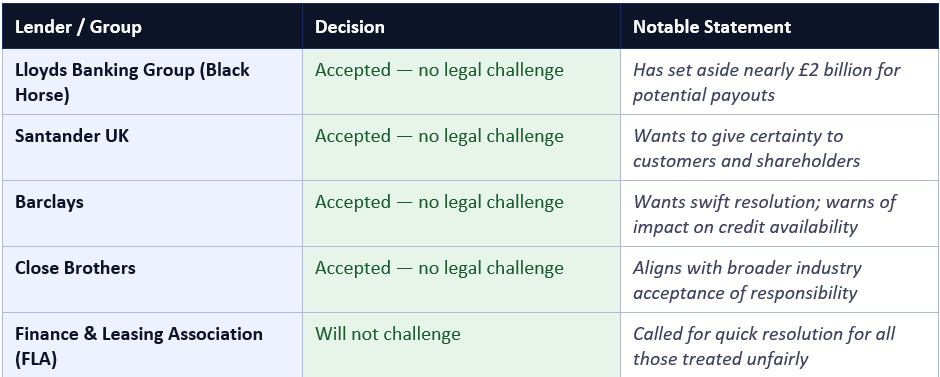

Which Lenders Have Accepted the Scheme?

The scheme's viability received a significant boost in late April 2026 when all major lenders and the Finance and Leasing Association (FLA) — the industry's representative body — confirmed they would not mount a legal challenge against it. This was not a foregone conclusion: industry sources had previously suggested some lenders were considering estimates of the total bill at £18 billion to £20 billion, far above the FCA's figure, and were prepared to challenge the methodology in court.

Note: On 27 April 2026, the FCA confirmed that the scheme has also been subject to a separate legal challenge — from consumer advocacy group Consumer Voice, which argues the scheme is too favourable to lenders and could leave some drivers hundreds of pounds short of what they are owed. The FCA has stated it is considering its approach and will set out its position shortly.

Who Is Eligible to Claim?

Eligibility is determined by the FCA's PS26/3 rules. You may be entitled to compensation if all of the following apply to your agreement:Eligibility Checklist

- You used car finance to buy a motor vehicle (car, van, motorbike or campervan) — caravans are excluded

- The finance agreement was taken out between 6 April 2007 and 1 November 2024

- The agreement was a Personal Contract Purchase (PCP) or Hire Purchase (HP) — leasing/PCH agreements are not covered

- The vehicle was for personal use (or as a sole trader/small partnership for loans under £25,000)

- You were not told about a DCA, a high commission arrangement, or an exclusive contractual tie between the lender and dealer

- You have not already received compensation or had your complaint upheld by the Financial Ombudsman Service

- Your loan was not in the top 0.5% by value for that year (very high-value loans are outside the mass scheme)

- Your agreement was not a zero-percent interest deal

The scheme also applies whether or not the vehicle has since been sold or the loan fully repaid. Making a complaint does not affect your credit score.

How Much Compensation Could You Receive?

The FCA estimates an average payout of £829 per eligible agreement. However, the actual amount will vary depending on the specific arrangements in your contract and the size of the commission involved.Two calculation methods will be applied under the scheme. For most cases involving an undisclosed DCA or high commission arrangement, consumers will receive the excess interest they paid — that is, the difference between what they paid and what a fair rate would have been. For cases where commission was both undisclosed and exceptionally high (at least 50% of the total cost of credit and 22.5% of the loan amount), consumers will receive a full refund of all commission paid, plus interest. This applies to an estimated 90,000 claimants and could result in significantly higher payouts than the average.

If you had more than one eligible agreement during the covered period, you will receive a separate payment for each. Research by MoneySavingExpert suggests that the average consumer has approximately two car finance agreements, giving an estimated total claim value of around £1,658 per person where both are eligible.

Around one-third of eligible claims are expected to be capped to prevent overpayment where the commission charged, while high, did not result in a loss of that amount to the customer.

How to Make Your Claim — Step by Step

The FCA has deliberately designed the scheme to be accessible without using a claims management company or solicitor, both of which will typically charge between 15% and 36% of any payout as a fee. You are entitled to claim directly through your lender at no cost.Step-by-Step: Claiming Directly

- Step 1: Identify your lender — This is the finance company (not the dealership). Check your credit file via Experian, Equifax, or ClearScore if you no longer have your documents. A soft credit check will show all regulated finance agreements.

- Step 2: Submit a complaint — Write to your lender referencing FCA PS26/3 and undisclosed commission arrangements. You can use MoneySavingExpert's free complaint letter tool or the FCA's consumer information pages.

- Step 3: Wait for the implementation period — Lenders are not required to issue responses during the implementation period (ending 30 June 2026 for post-April 2014 agreements; 31 August 2026 for earlier ones).

- Step 4: Receive your redress determination — Lenders have 3 months from the end of the implementation period to tell you whether you are owed compensation and how much.

- Step 5: Accept or challenge — You have 1 month to accept the offer. If you are unhappy with the outcome, you can refer the complaint to the Financial Ombudsman Service (free) within the timeframe specified in your lender's letter.

- Step 6: Receive payment — Once you accept, the lender must pay you within 1 month.

Key Dates and Deadlines

Risks, Legal Challenges and What Comes Next

While the decision by all major lenders to accept the scheme without legal challenge was a significant development, the path to payouts is not entirely clear. On 27 April 2026 — the day after the FLA confirmed it would not challenge the scheme — the FCA announced that a legal challenge had nonetheless been lodged by consumer advocacy group Consumer Voice. The group argues that the FCA's scheme is excessively favourable to lenders and could leave millions of drivers receiving less compensation than they are legally entitled to.Consumer Voice contends that the scheme can proceed in parallel with its challenge, meaning consumer payouts should not necessarily be delayed. However, the FCA stated it was considering its approach and expected to set out its position within days. Legal experts suggest that even if the challenge proceeds to a judicial review, the more recent Scheme 2 — covering agreements from April 2014 onward — is unlikely to be delayed, as the FCA specifically designed the two-scheme structure to insulate post-2014 claims from challenges relating to the older period.

Separately, some lenders — notably Barclays — have accepted the scheme while issuing stark warnings about its long-term consequences. Barclays argued that compelling firms to pay compensation where customers suffered no demonstrable financial harm sets a dangerous precedent, risking higher borrowing costs and reduced availability of consumer credit. These concerns were echoed by the Finance and Leasing Association, which argued that the scheme's methodology should accurately reflect actual losses to consumers rather than a broader definition of unfairness.

The comparisons to PPI are instructive. The PPI scandal began with individual complaints, escalated to a regulatory intervention, faced legal challenges, and ultimately resulted in over £50 billion being repaid to consumers over more than a decade. The car finance scheme is designed to move much faster — but the history of large-scale financial redress in the UK suggests that complexity, legal challenges, and implementation difficulties are rarely avoided entirely.

CONCLUSION

The acceptance of the FCA's £9.1 billion car finance mis-selling redress scheme by all major UK lenders marks a decisive turning point in one of the largest consumer finance scandals in British history. For the 12.1 million drivers potentially eligible for compensation, this is a significant and long-awaited moment of accountability.The most important action for eligible consumers is to submit a complaint to their lender before the scheme's deadlines — particularly 30 June 2026 for agreements from April 2014. This can be done for free, directly through the lender, without engaging a claims management company. With millions of claims expected to be settled in 2026 and the vast majority by end of 2027, and with payouts averaging £829 per agreement, the scheme represents a meaningful financial opportunity for many households. Act early, keep it free, and let the regulators and lenders do the rest.

Frequently Asked Questions

Do I need a solicitor or claims management company to claim?

No. You can submit your complaint directly to your lender for free. The FCA has designed the scheme specifically so consumers can access it without professional help. Claims management companies charge between 15% and 36% of your payout. MoneySavingExpert.com's free complaint tool is widely used and has generated over 3.6 million complaints to date.How do I find out which lender held my finance agreement?

If you no longer have your documents, a soft credit check through a free service such as Experian, Equifax, or ClearScore will show all regulated consumer credit agreements held in your name, including the lender's name. This check does not affect your credit score.I no longer own the car and have fully repaid the loan — can I still claim?

Yes. You can claim even if you no longer own the vehicle or have fully repaid the finance agreement, provided the loan was taken out between 6 April 2007 and 1 November 2024 and meets the other eligibility criteria.Are leasing (PCH) agreements covered by the scheme?

No. Personal Contract Hire (leasing) agreements are explicitly excluded from the FCA's redress scheme. Only Personal Contract Purchase (PCP) and Hire Purchase (HP) agreements are within scope.I already complained — do I need to do anything else?

No action is required if you have already submitted a complaint. Your complaint remains paused until 31 May 2026 and will be automatically reviewed under the new scheme rules. Lenders are required to contact you with their redress determination within three months of the relevant implementation period ending.What if I disagree with the compensation offer from my lender?

You have one month to accept or challenge the lender's redress determination. If you are unsatisfied, you can refer the complaint to the Financial Ombudsman Service free of charge within the timeframe stated in your lender's letter. The ombudsman will assess whether the scheme rules were correctly applied.Could the Consumer Voice legal challenge affect my payout?

Consumer Voice is challenging the scheme on the grounds it is too favourable to lenders. The group contends the scheme can proceed in parallel with the challenge. The FCA is expected to set out its position shortly. The FCA's two-scheme structure was specifically designed so that a legal challenge to the pre-2014 period does not delay payouts under the post-2014 scheme.References

FCA — Motor Finance Consumer Redress Scheme (PS26/3) https://www.fca.org.uk/publications/policy-statements/ps26-3-motor-finance-consumer-redress-schemeFCA — Car Finance Claims: Consumer Information https://www.fca.org.uk/consumers/car-finance-complaints

FCA — FCA Confirms Motor Finance Redress Scheme (Statement) https://www.fca.org.uk/news/statements/fca-confirms-motor-finance-redress-scheme

MoneySavingExpert — Car Finance Free Reclaim Tool & Guide https://www.moneysavingexpert.com/reclaim/reclaim-car-finance/

Auto Express — Car Finance Mis-Selling Scandal: Full Guide https://www.autoexpress.co.uk/car-finance-scandal

LBC — Path Clears for £9.1bn Car Finance Payout Scheme https://www.lbc.co.uk/article/b7e70e55c4f54e50922eca7fb6081fc7-5HjdYJq_2/

Kennedys Law — FCA Confirms Final Car Finance Redress Scheme https://www.kennedyslaw.com/en/thought-leadership/article/2026/fca-confirms-final-car-finance-redress-scheme-after-key-revisions/

Santander Consumer Finance — Commission Arrangement Complaints https://www.santanderconsumer.co.uk/making-a-complaint/commission-arrangement-complaints/

0 Comments Comments