Investing

What Are Bid, Ask and Spread in Trading? Complete Guide

Table of Contents

- The Hidden Cost Inside Every Trade

- What Are Bid, Ask and Spread? The Definitions

- The Bid Price

- The Ask Price

- The Spread

- Why the Spread Exists: The Role of Market Makers

- Bid-Ask Spreads Across Markets: 2026 Complete Reference

- What Determines the Size of the Spread?

- How to Calculate Spread Cost: Worked Examples

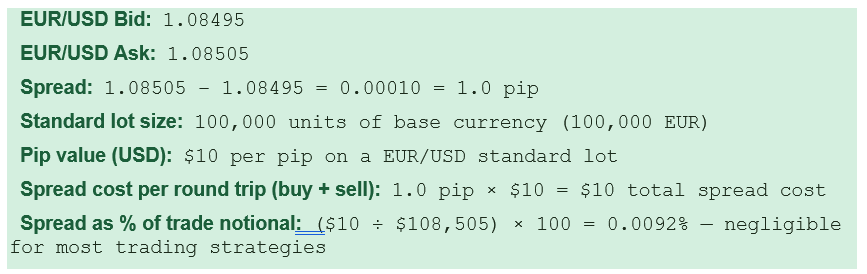

- Example 1 — Forex: EUR/USD Standard Lot

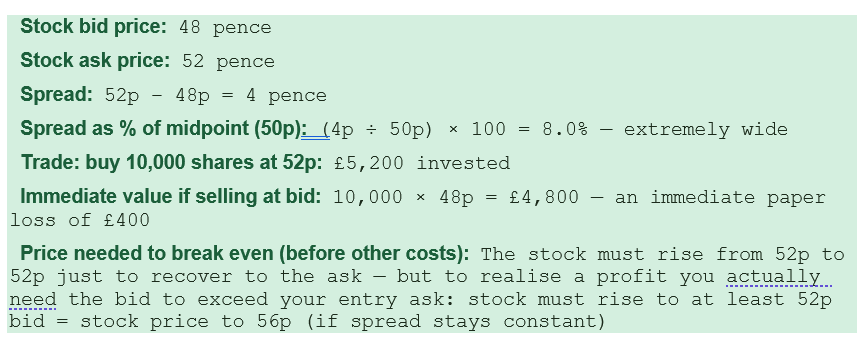

- Example 2 — UK Small-Cap Stock (AIM)

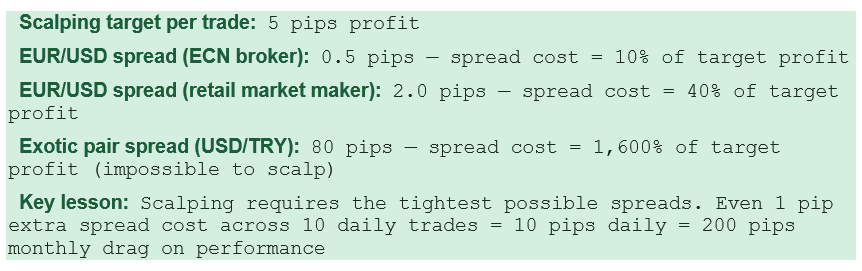

- Example 3 — Scalping Strategy Cost Analysis

- Bid, Ask and Spread in Practice: Key Trading Scenarios

- How to Reduce Your Spread Costs: Practical Strategies

- The Spread and Risk Management: Stop Losses, Take Profits, and Slippage

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Hidden Cost Inside Every Trade

Every single trade you ever place in any financial market — stocks, forex, crypto, bonds, options, commodities — starts with a built-in cost. You pay it whether your broker charges a commission or not. It does not appear as a line item on your transaction confirmation. It is invisible to most new traders until they look closely at why their trade opened at a slight loss even in the very first second after execution. This cost is the bid-ask spread.The bid-ask spread is the difference between two prices that exist simultaneously for every tradable instrument: the bid (the price at which you can sell) and the ask (the price at which you can buy). The ask is always higher than the bid. The gap between them — the spread — is the cost of entering a trade and the primary source of income for market makers who provide liquidity by standing ready to buy and sell at both prices. Quantt's April 2026 analysis identifies it with precision: 'For active traders and institutions moving large volumes, spread costs often dwarf commission costs. In 2026, with zero-commission trading now standard across most brokers, the spread has become the primary cost of trading for most retail traders.'

This guide explains everything about bid, ask, and spread: what each term means, how the spread forms and who sets it, why it varies so dramatically across different instruments and market conditions (from 0.1 pip on EUR/USD to 100+ pips on exotic currency pairs, from 1 cent on Apple stock to 8% on an AIM-listed micro-cap), how to calculate the spread cost in real money, and the practical strategies for reducing the spread's impact on your trading performance. Whether you trade forex, stocks, crypto, or any other instrument, understanding the bid-ask spread is one of the most practically important concepts in trading.

What Are Bid, Ask and Spread? The Definitions

The Bid Price

The bid price is the highest price that a buyer is currently willing to pay for an asset. In practice, when you want to sell any instrument — whether you are closing a long position or opening a short — your trade executes at the bid price. Think of the bid as the price the market is 'bidding' to buy from you. It represents the immediate selling price: if you need to sell right now, at the current market price, you will receive the bid.In forex, if EUR/USD shows a bid of 1.08495, it means buyers in the market are willing to pay 1.08495 USD per euro at this moment. If you hold euros and want to sell them into dollars immediately, you will receive 1.08495 for each euro. If you are opening a short position on EUR/USD (expecting the euro to fall), you sell at the bid price.

The Ask Price

The ask price — sometimes called the offer price — is the lowest price that a seller is currently willing to accept for an asset. When you want to buy any instrument, your trade executes at the ask price. The ask is always higher than the bid. It represents the immediate buying price: if you need to buy right now, at the current market price, you will pay the ask.In the same EUR/USD example, if the ask is 1.08505, it means sellers are willing to sell euros at 1.08505 USD per euro. If you want to buy euros against dollars, you pay 1.08505 for each euro. If you are opening a long position on EUR/USD (expecting the euro to rise), you buy at the ask price.

The Spread

The spread is the difference between the ask price and the bid price. It is calculated as: Spread = Ask − Bid. This gap is the transaction cost that is built into every trade. The moment you enter a position, your trade is immediately worth the bid price (the price you could exit at if you sold immediately) while you paid the ask price (a higher price) to enter. The spread is the distance between these two prices — the immediate loss you would crystallise if you reversed the trade at once.In forex, spreads are measured in pips. In stocks, spreads are measured in currency units (cents, pence). In percentage terms, the spread on major currency pairs is typically less than 0.01% of the price — so small as to be almost irrelevant for position traders holding for days or weeks. The spread on an illiquid small-cap stock at 8% of the price is a significant, strategy-defining cost that must be overcome through price movement before any profit is realised.

The spread cost at scale: £10 million in FTSE 100 at 0.01% spread = £1,000 round-trip. Same in illiquid AIM at 1% = £100,000 — 100x more expensive — Quantt's April 2026 analysis of spread costs illustrates why institutional traders are acutely focused on spread and why liquidity is the foundation of tradability. The spread that appears trivially small on a liquid instrument becomes a strategy-destroying cost on an illiquid one — the only difference is how many buyers and sellers are present and competing (Quantt.co.uk, April 2026)

Why the Spread Exists: The Role of Market Makers

The bid-ask spread exists because financial markets require intermediaries — called market makers or liquidity providers — who stand ready to buy and sell at any time, even when there is no natural buyer for every seller or no natural seller for every buyer. Market makers continuously quote both a bid price (where they will buy from you) and an ask price (where they will sell to you). The spread between these two prices is how they are compensated for this service.Consider the analogy of a currency exchange bureau at an airport. The bureau quotes a rate to buy your foreign currency (the bid — what they will pay you) and a rate at which they will sell you foreign currency (the ask — what they charge you). The difference between these two rates is their profit for providing the immediate currency conversion service. Financial market makers operate on the same principle, but with vastly tighter margins and at enormous volumes.

Market makers face two primary risks when providing liquidity. The first is inventory risk: if they buy an asset from you and the price falls before they can sell it to someone else, they suffer a loss. The wider the spread, the more cushion they have against this risk. The second is adverse selection: the risk that the person on the other side of the trade has better information than the market maker. If institutional traders are selling because they know bad news is coming, the market maker who buys from them at the bid will be left holding a losing position. The spread compensates the market maker for both of these risks.

The zero-commission era and the spread's growing importance: In 2026, zero-commission trading is standard across most retail broker platforms — Robinhood, Trading 212, eToro, and most major UK and US brokers have eliminated explicit per-trade commissions. This has dramatically reduced the stated transaction cost that traders see. However, it has not eliminated trading costs — it has shifted them. Where once you paid a visible £10 commission, you now pay through the bid-ask spread, which is invisible, embedded in the execution price, and often more expensive for active traders than the old commission structure was. Quantt's April 2026 analysis is explicit: 'Understanding the bid-ask spread matters because it's a hidden cost that doesn't appear on your transaction confirmation.' In the zero-commission era, understanding and minimising the spread is more important than ever.

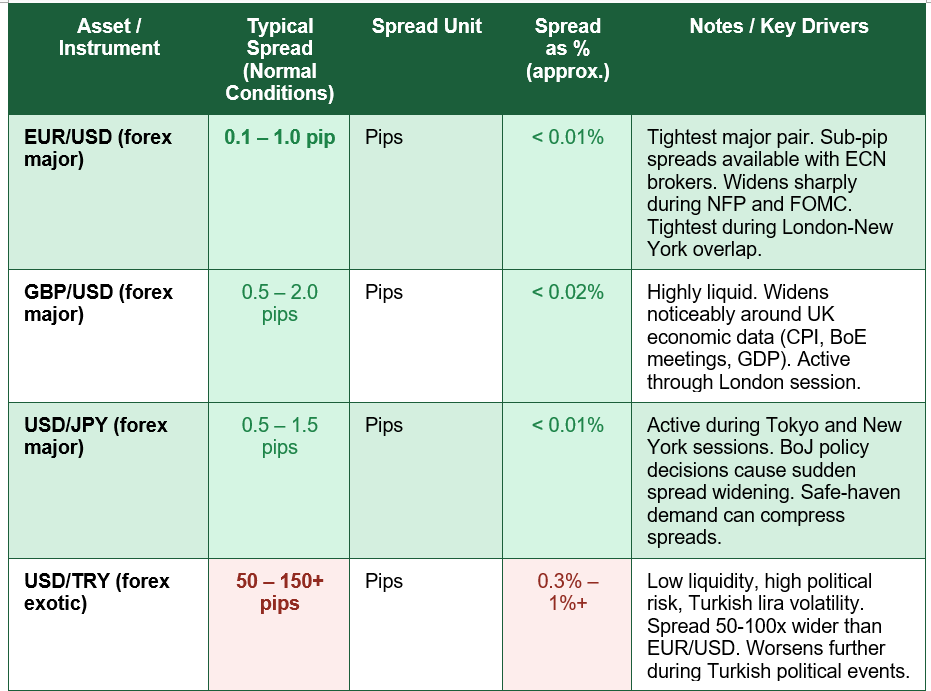

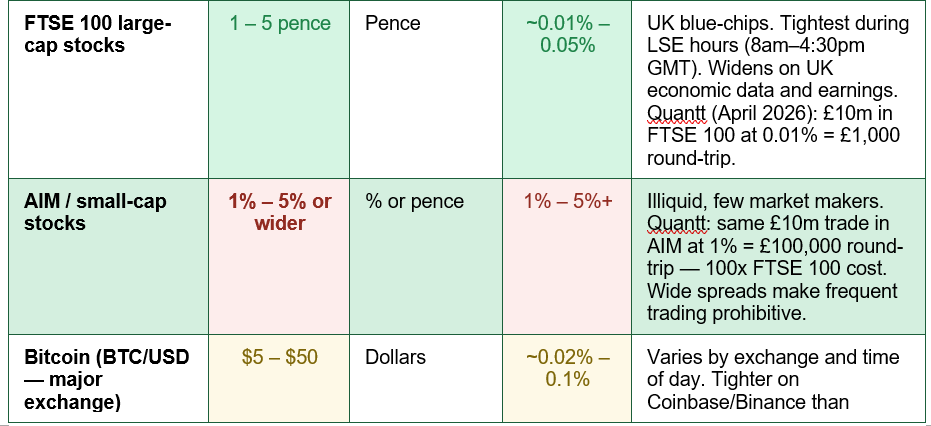

Bid-Ask Spreads Across Markets: 2026 Complete Reference

The spread varies dramatically across different asset classes, instruments, and trading conditions. The table below provides a comprehensive reference for typical bid-ask spreads across all major asset classes in 2026:

What Determines the Size of the Spread?

The spread on any instrument is not fixed. It expands and contracts continuously in response to several interconnected factors. Understanding what drives spread size is the foundation for managing spread costs effectively:- Liquidity: The most fundamental driver of spread size. Liquidity is the degree to which an asset can be bought or sold quickly at a stable price. High liquidity means many buyers and sellers are active simultaneously, creating competition that narrows the spread. EUR/USD — the world's most liquid currency pair, with $7.5 trillion in daily forex volume — has spreads under 1 pip because thousands of participants are competing to buy and sell at the same time. An AIM-listed micro-cap with only a handful of transactions per day has a wide spread because market makers cannot quickly find a natural buyer for any asset they purchase.

- Volatility: When asset prices are moving rapidly and unpredictably, market makers face greater inventory risk. To compensate for the heightened risk of holding assets during volatility, they widen their spreads. This is why spreads widen sharply around major economic data releases (NFP, CPI, FOMC), during market crises, and during earnings announcements for individual stocks. EBC Financial Group's analysis notes: 'During major news announcements, such as central bank decisions or earnings reports, spreads can suddenly widen just before or after such events because traders and market makers alike are uncertain about which direction the market will take.'

- Time of day and trading session: Spreads are tightest when the most participants are active. In forex, the London-New York overlap (1 PM to 5 PM GMT) produces the tightest spreads across major pairs because the world's two largest financial centres are both open simultaneously. During the Asian session, EUR/USD spreads may widen as European and American traders are absent. In stocks, spreads are tightest during regular exchange hours and widen significantly in pre-market and after-hours trading when fewer participants are present.

- Broker type (ECN vs market maker): Different broker models have fundamentally different spread structures. ECN (Electronic Communications Network) brokers connect traders directly to the interbank market, passing through raw market spreads that can be as low as 0.0 pips — but charging a separate commission per lot traded. Market maker brokers incorporate their profit margin directly into the spread — no separate commission, but a slightly wider spread. For active traders and scalpers, ECN models typically produce lower total costs. For infrequent traders, the all-in market maker spread may be simpler and more predictable.

- Instrument-specific characteristics: Some instruments are structurally less liquid due to the nature of the underlying asset. Options have wider spreads than the underlying stock because they are less actively traded and more complex to hedge. Deep out-of-the-money options and long-dated options are significantly wider than near-the-money options with nearer expiry. Exotic currency pairs, frontier market equities, and low-volume cryptocurrencies all carry wide spreads as a structural characteristic independent of market conditions.

How to Calculate Spread Cost: Worked Examples

Example 1 — Forex: EUR/USD Standard Lot

Example 2 — UK Small-Cap Stock (AIM)

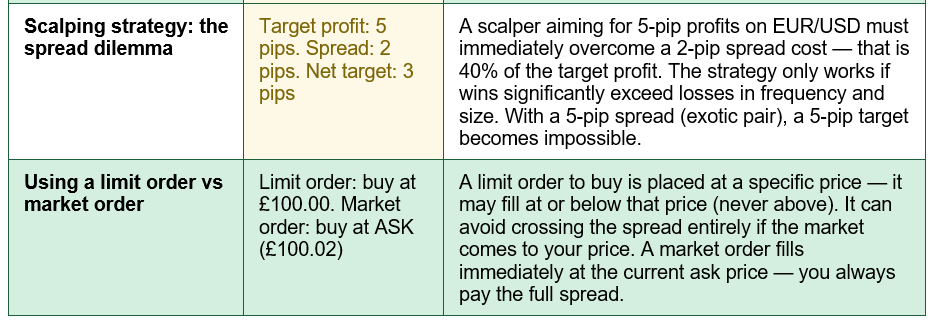

Example 3 — Scalping Strategy Cost Analysis

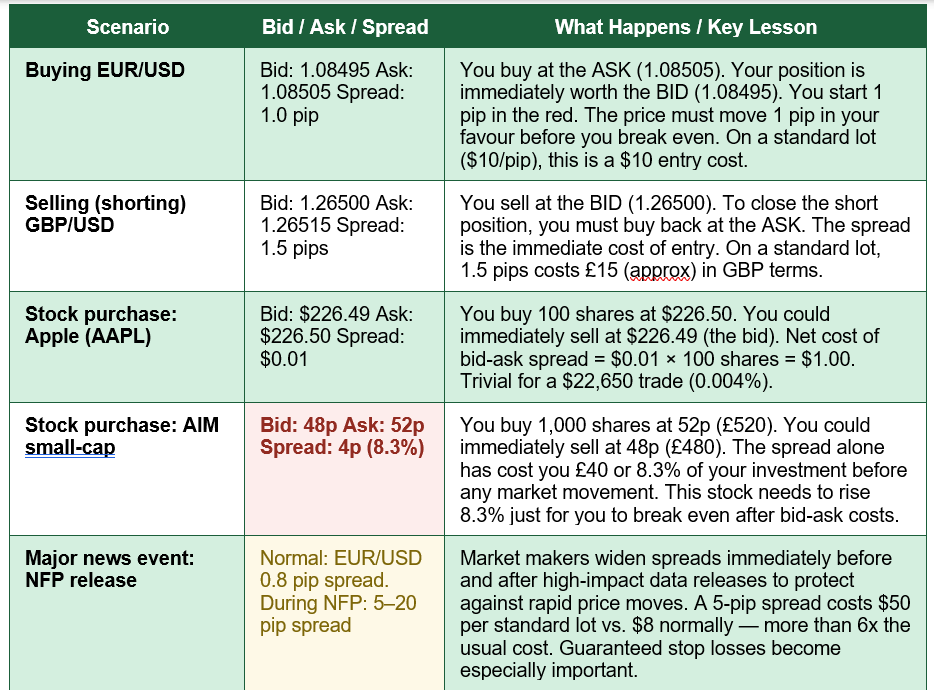

Bid, Ask and Spread in Practice: Key Trading Scenarios

The table below maps the most important trading scenarios to show exactly how bid, ask, and spread affect real trade execution — the starting point, the cost, and the key lesson from each:

How to Reduce Your Spread Costs: Practical Strategies

While the spread cannot be eliminated — it is the price of market access and the compensation of liquidity providers — it can be managed and minimised through deliberate choices about what to trade, when to trade, and how to trade. The following strategies reduce spread costs for both active and occasional traders:- Trade the most liquid instruments: Major currency pairs (EUR/USD, GBP/USD, USD/JPY), large-cap stocks (FTSE 100, S&P 500 blue-chips), and major indices all carry the tightest spreads. Daily Price Action's guide is direct: 'The #1 rule is to choose popular currency pairs to trade. If you stick to the major pairs such as EUR/USD and GBP/USD, the factors above will have a limited effect on the spreads you pay.' Every deviation toward less liquid instruments means higher spread costs.

- Trade during peak liquidity hours: For forex, the London-New York overlap (1 PM to 5 PM GMT) produces the tightest spreads. For UK stocks, spreads are tightest during LSE hours (8 AM to 4:30 PM GMT). Avoid trading illiquid hours — pre-market, after-market, overnight, or the Asian session for European pairs — where spreads can be significantly wider.

- Use limit orders instead of market orders: A market order fills immediately at the current ask (for a buy) or bid (for a sell) — you always pay the full spread. A limit order is an instruction to buy or sell only at a specified price or better. If placed between the bid and ask (for example, at the midpoint), a limit order may be filled without paying the full spread — though it is not guaranteed to fill at all. For patient traders who are not rushing to enter immediately, limit orders can meaningfully reduce spread costs.

- Choose an ECN broker for high-frequency trading: If you trade frequently or scalp, the difference between an ECN broker with raw 0.2-pip spreads plus a $7 commission per lot and a market maker with 1.5-pip spreads plus no commission can be significant over hundreds of trades. At 1.0 standard lot per trade, ECN total cost: $7 commission + $2 spread = $9. Market maker: $15 spread + $0 commission = $15. The ECN is 40% cheaper per trade. Over 100 trades, this saves $600.

- Avoid trading around major news releases: Spreads widen dramatically before and during high-impact economic releases (NFP, CPI, FOMC). If you do not have a specific news-trading strategy, closing or not opening positions in the 30-minute window around major releases avoids the elevated spread cost entirely.

THE PERCENTAGE TEST: When comparing spreads across different instruments, always convert to percentage terms to make meaningful comparisons. A 1-pip spread on EUR/USD at 1.0850 is (0.0001 ÷ 1.0850) × 100 = 0.0092%. A 4-pence spread on an AIM stock at 50p is (4 ÷ 50) × 100 = 8.0%. These are not comparable in absolute terms but are directly comparable in percentage terms. The percentage test reveals which instrument is truly more expensive to trade — and the difference between 0.009% and 8.0% in the above example is the difference between a trivial cost and a devastating one.

The Spread and Risk Management: Stop Losses, Take Profits, and Slippage

The bid-ask spread has practical implications for stop loss and take profit placement that many new traders overlook. In any trading platform, when you place a buy order, your entry is at the ask price. If you immediately place a stop loss 10 pips below your entry, the stop loss is triggered when the bid price falls to 10 pips below your entry ask — meaning the price only needs to move adversely by 10 pips from the ask before your stop fires. But your take profit is also calculated from the bid price — so to reach a 10-pip profit, the bid (which is always lower than the ask by the spread amount) must rise 10 pips above your entry ask, meaning the midprice must actually move 10 pips plus the spread before you profit.FXTM's trading academy makes this explicit: 'When buying, the bid price has to reach the Take Profit or the Stop Loss price for the position to close. When selling, the ask price has to reach the Take Profit or Stop Loss price for the position to close.' This asymmetry means that in a tight, sideways market, a trade opened with a 1-pip spread is already 1 pip closer to the stop loss than the take profit from the moment of execution.

Slippage is a related concept: the difference between the price at which you expected your order to fill and the price at which it actually filled. During high-volatility periods, particularly around major economic releases, market orders may experience significant slippage because prices are moving faster than orders can be matched. Slippage is most severe in illiquid markets and during crises. PrimeXBT's 2026 guide notes: 'During the March 2020 shock, spreads on major indices blew out far beyond their usual range.' During such periods, the effective trading cost is far higher than normal spreads suggest.

CRISIS SPREAD WIDENING — THE RISK YOU CANNOT AVOID: During market stress events — flash crashes, pandemic announcements, geopolitical shocks, and financial crises — bid-ask spreads widen dramatically and rapidly. What is normally a 0.5-pip EUR/USD spread can become 10, 20, or more pips. Stop losses may not be filled at the expected price due to gapping. Buy orders may fill at significantly worse prices than indicated. This is not a broker malfunction — it is the natural market response to a sudden imbalance between buyers and sellers. Historic Financial News (2025) notes that 'even the most liquid government bond markets can experience wider spreads during stress.' Factor potential spread widening into all risk management calculations, particularly for leveraged positions, and consider reducing position size during periods of elevated uncertainty.

Conclusion

The bid-ask spread is the most fundamental cost of trading — present in every market, every instrument, and every transaction. The bid is the price at which you can sell; the ask is the price at which you can buy; the spread is the gap between them, and it represents the cost of market access, the compensation of liquidity providers, and the most reliable indicator of how liquid and efficiently priced any instrument is. Every position you open starts slightly in the red by exactly the amount of the spread, and must overcome that cost before generating any profit.In 2026, with zero-commission trading now standard across most retail platforms, the spread has become the primary transaction cost for most traders — making it more important to understand and manage than at any point in the past decade. The range of spread costs across instruments is dramatic: EUR/USD at 0.1 pip (less than 0.01% of price) versus an AIM micro-cap at 8% of price; Apple stock at $0.01 versus a small altcoin at several percent. That 100x or even 1,000x difference in spread cost is the difference between a strategy that works and one that is structurally impossible regardless of how good the trading signals are.

Managing spread costs is as much a part of trading strategy as choosing which direction to trade. Trade the most liquid instruments in their most active hours, use limit orders where time permits, choose an ECN broker for high-frequency strategies, avoid major news releases if spread trading is not the strategy, and always convert spreads to percentage terms to enable meaningful comparison across instruments. The spread is not the enemy of trading — it is the price of market access. Understanding it, measuring it, and minimising it where possible is how professional traders ensure that every cost in their trading operation is earned back by the strategy's edge.

Frequently Asked Questions (FAQ)

What is the bid-ask spread in simple terms?

The bid-ask spread is the difference between the price you can sell an asset at (the bid) and the price you can buy it at (the ask). The ask is always higher than the bid. For example, if EUR/USD has a bid of 1.08495 and an ask of 1.08505, the spread is 1.0 pip. This 1-pip gap is the immediate cost of entering any trade — the moment you buy at the ask, your position is already worth the lower bid price, and the market must move in your favour by the amount of the spread before you break even. The spread compensates market makers and liquidity providers for the service of standing ready to buy and sell at any time.Why is the spread on some instruments so much wider than others?

Spread width is fundamentally driven by liquidity — how many buyers and sellers are actively trading an instrument at any given moment. When many participants compete to trade the same asset, the bid and ask prices are pushed very close together (tight spread). When few participants are present, market makers must widen the spread to protect against the risk of holding assets that are difficult to resell. EUR/USD — the world's most liquid currency pair — trades with spreads under 1 pip because it is traded continuously in enormous volume. A small-cap AIM stock with a handful of daily transactions may have an 8% spread because market makers need significant compensation for the difficulty and risk of providing liquidity in a rarely traded instrument.How does the spread affect stop losses and take profits?

The spread affects stop loss and take profit calculations because buy positions open at the ask price but are measured and closed at the bid price. When you buy, your stop loss triggers when the bid price falls to your stop level — and since the bid is always below the ask by the spread amount, your stop is already (spread size) below your break-even point at the moment of entry. Your take profit triggers when the bid price rises to your target level — so the price must move (spread size) further in your favour than you might initially expect. For a 1-pip spread and a 10-pip take profit, the market must actually move approximately 11 pips in your favour (10 pip target plus 1 pip spread) before your take profit is reached. This asymmetry becomes significant for tight-stop, small-target scalping strategies.What is the difference between a fixed spread and a variable spread?

A fixed spread stays constant regardless of market conditions — it does not widen during news events or low-liquidity periods. Market maker brokers often offer fixed spreads for popular instruments. Fixed spreads provide cost certainty and can be particularly useful for traders who hold positions through news events. The trade-off is that fixed spreads are typically slightly wider than variable spreads during normal market hours to compensate the broker for the risk of maintaining the fixed rate during volatile periods. A variable (floating) spread changes in real time with market conditions — it is tighter during liquid, quiet periods and widens during volatility. ECN brokers and most STP (Straight Through Processing) brokers offer variable spreads. Variable spreads are typically tighter on average but unpredictable around news events.How can I reduce the spread I pay as a trader?

The most effective strategies for reducing spread costs are: trade the most liquid instruments (major forex pairs, large-cap stocks) where competition among market makers naturally compresses spreads; trade during peak liquidity hours (London-New York overlap for forex, regular exchange hours for stocks); use limit orders rather than market orders when not urgently needing to enter — a limit order placed between the bid and ask may fill without paying the full spread; choose an ECN broker for high-frequency trading, where raw spreads plus commission often produce lower total cost than market maker all-in spreads; and avoid trading around major news releases where spreads widen significantly. For longer-term position traders, the spread is a one-time entry cost that represents a negligible percentage of the overall trade's potential gain — spread management matters most for scalpers and day traders who enter and exit positions many times per day.External References

1. Quantt — Bid-Ask Spread: What It Is and How It Works 2026 (April 2026 — institutional spread cost analysis)https://www.quantt.co.uk/resources/bid-ask-spread-explained

2. PrimeXBT — Bid-Ask Spread Explained: Forex vs Crypto vs Stocks (2 weeks ago)

https://primexbt.com/for-traders/bid-ask-spread/

3. FXTM Academy — Bid, Ask and Spread Explained (Official FXTM education)

https://www.fxtm.com/en/learn/bid-ask-spread/

4. IG International — Understanding Bid-Ask Spread in Trading (February 2025)

https://www.ig.com/en/trading-strategies/bid-ask-spread--what-is-it-and-how-does-it-work--250207

5. EBC Financial Group — What Is the Bid-Ask Spread and Why Does It Matter? (June 2025)

https://www.ebc.com/forex/what-is-the-bid-ask-spread-and-why-does-it-matter

6. Daily Price Action — Bid vs Ask in Forex: Simple Guide to Quotes and Spreads (September 2025)

https://dailypriceaction.com/blog/bid-vs-ask/

7. Historic Financial News — Bid-Ask Spread Guide: Understanding Market Pricing in 2026 (December 2025)

https://www.historicfinancialnews.com/finance-term/bid-ask-spread

8. FOREX.com — What Is the Bid/Ask Spread? (US — Glossary with practical examples)

https://www.forex.com/en-us/glossary/bid-ask-spread/

0 Comments Comments