Investing

What Is the Uptick Rule in Trading?

Table of Contents

- A Rule Born from Collapse and Revived by Crisis

- What Is the Uptick Rule?

- The Complete History: From 1929 to Today

- The Alternative Uptick Rule (Rule 201): How It Works Today

- The Trigger: The 10% Circuit Breaker

- What the Restriction Requires

- Original vs Alternative Uptick Rule: Key Differences

- Worked Examples: How the Rule Operates in Practice

- Example 1 — Rule Triggered and Applied

- Example 2 — Odd-Lot Exemption (Short Seller Closing an Odd-Lot Position)

- Short Selling and Bear Raids: Why the Rule Exists

- What Is Short Selling?

- What Is a Bear Raid?

- Exemptions: When the Uptick Rule Does Not Apply

- Arguments For and Against the Uptick Rule

- Arguments in Favour of the Rule

- Arguments Against the Rule

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

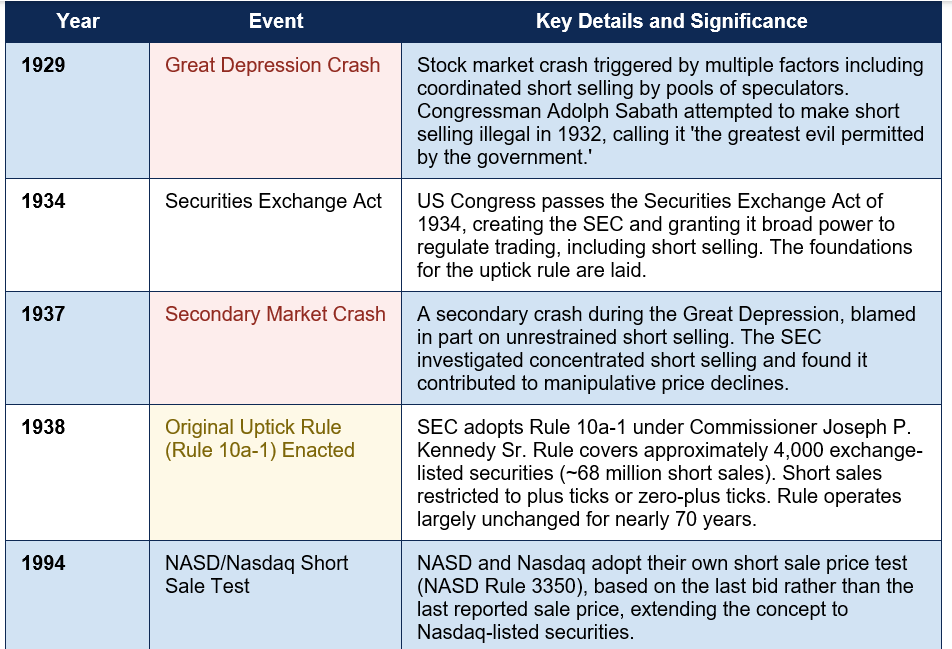

A Rule Born from Collapse and Revived by Crisis

Few trading regulations have as dramatic an origin story as the uptick rule. It was born in the wreckage of the Great Depression, spent nearly seven decades as an unremarkable but persistent fixture of US equity market regulation, was quietly eliminated by the SEC in 2007 in the name of modernisation and liquidity, and was implicated — fairly or not — in the ferocity of the financial crisis that followed just months later. By 2010 it was back, in a modified form, as part of the SEC's post-crisis regulatory response. Today, the Alternative Uptick Rule (Rule 201 of Regulation SHO) remains in force and is triggered hundreds of times each year on individual stocks experiencing severe intraday declines.The uptick rule is a short-selling restriction — a rule that limits when and how traders can execute short sales on a stock. Its purpose is to prevent a specific type of market manipulation called a 'bear raid': a coordinated or piling-on attack in which short sellers hammer a stock's price downward, each successive short sale triggering further selling by panicked long holders, causing a spiral of decline that may be disproportionate to any change in the company's actual value. The uptick rule's mechanism is simple: it requires that a short sale be executed at a price above the prevailing market price, preventing short sellers from hitting bids and accelerating downward price momentum.

This guide explains exactly what the uptick rule is, how both the original rule and today's Alternative Uptick Rule work mechanically, the complete history from 1938 to the present, worked examples of how the restriction operates in practice, the arguments for and against the rule, who is exempt, and what traders and investors need to know about short sale restrictions (SSR) in 2026. Whether you trade stocks actively, study market microstructure, or simply want to understand the full picture of how short selling is regulated in the United States, this guide provides the complete answer.

What Is the Uptick Rule?

The uptick rule is a trading regulation that restricts short selling to price levels above the last traded price (or more recently, above the national best bid). The term 'uptick' refers to an upward price movement — a trade that executes at a price higher than the previous trade. By requiring short sellers to sell only on an uptick, the rule prevents them from hitting every successive bid and thereby driving the price continuously lower through sequential short selling.The SEC's formal definition of the original Rule 10a-1 captures the mechanics precisely: 'Rule 10a-1(a)(1) provided that, subject to certain exceptions, a listed security may be sold short (A) at a price above the price at which the immediately preceding sale was effected (plus tick), or (B) at the last sale price if it is higher than the last different price (zero-plus tick). Short sales were not permitted on minus ticks or zero-minus ticks.'

In plain language: a short seller under the original rule could only execute their sell order at a price that was either above the most recent trade (a 'plus tick') or equal to the most recent trade if that most recent trade was itself above the trade before it (a 'zero-plus tick'). What they could not do is sell short on a down tick — at a price lower than or equal to the most recent price that was itself below the trade before it. This prevented short sellers from simply hitting the bid aggressively and driving prices lower with each successive sale.

The original rule's scale: ~4,000 exchange-listed securities covered, approximately 68 million short sales subject to restriction — the SEC's own description of Rule 10a-1's scope before its 2007 repeal: 'The SEC's former uptick test (former Rule 10a-1), based on the last sale price, covered approximately 4,000 exchange-listed securities (or 68 million short sales).' The rule operated for 69 years (1938–2007) without significant modification — one of the longest-running continuous trading regulations in US history (SEC.gov / Wikipedia).

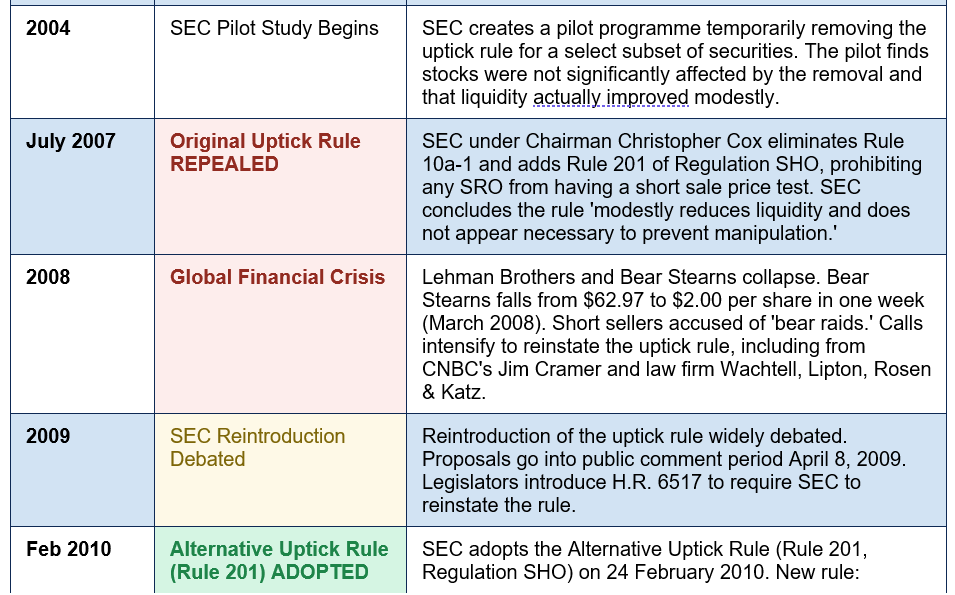

The Complete History: From 1929 to Today

The uptick rule has been shaped by every major US market crisis of the past century. The timeline below maps the key events that created, eliminated, and ultimately reformed the rule:

The Alternative Uptick Rule (Rule 201): How It Works Today

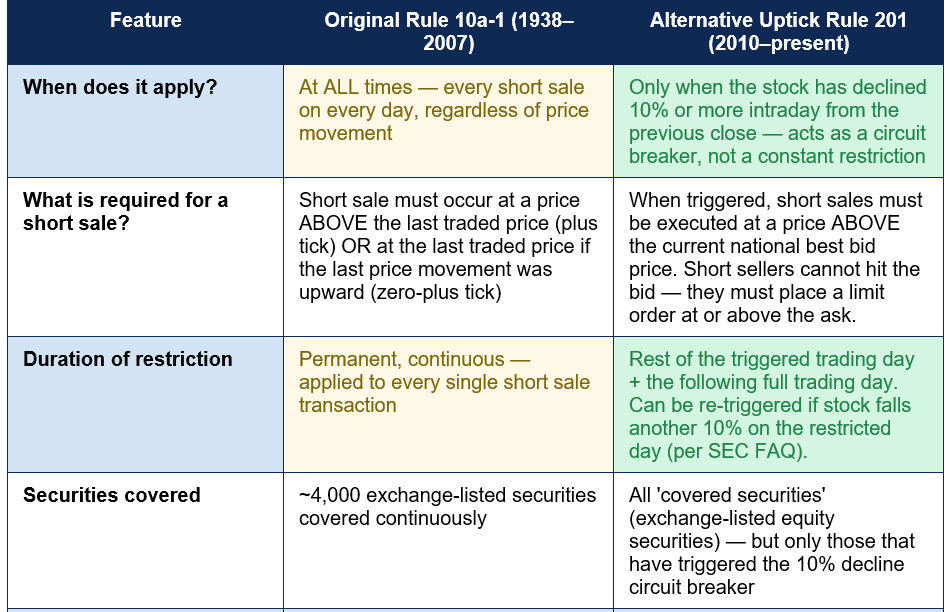

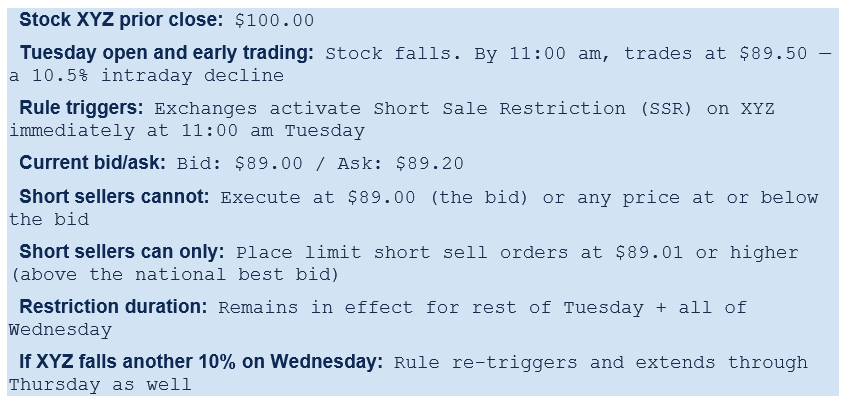

The version of the uptick rule in force in 2026 is the Alternative Uptick Rule — officially Rule 201 of Regulation SHO — adopted by the SEC on 24 February 2010. It is importantly different from the original rule in one fundamental way: it does not apply at all times. Instead, it is a circuit breaker that activates only when a specific condition is met.The Trigger: The 10% Circuit Breaker

The Alternative Uptick Rule is triggered when a 'covered security' — any exchange-listed equity security — declines by 10% or more intraday from the previous trading day's closing price. This trigger is monitored in real time by the exchanges, and the restriction activates automatically the moment the 10% threshold is crossed. Exchanges and trading venues notify market participants electronically when the restriction is in effect.For example: a stock closed at $50.00 on Monday. If on Tuesday it trades at or below $45.00 at any point during the session (a 10% decline), the Alternative Uptick Rule activates for that stock. The restriction applies for the rest of Tuesday and the entire trading session on Wednesday.

What the Restriction Requires

When the Alternative Uptick Rule is triggered, short sales on that security are restricted to prices above the current national best bid. In a standard market quote where a stock shows a bid of $44.90 and an ask of $45.00, a short seller cannot execute at $44.90 (the bid). They must place a short sale order at $44.91 or higher. In practice, this means short sellers can no longer 'hit the bid' — they must place limit orders rather than market orders, and they cannot execute immediately at the best available price.The practical effect on market dynamics is significant. When short sellers are forced to use limit orders above the current bid, they become passive — their orders sit in the order book waiting for buyers to come to them rather than actively driving the price down through successive market sell orders. This change from aggressive to passive order flow tends to reduce the downward pressure on price and can cause stocks to stabilise or even bounce after the rule activates.

The re-trigger mechanism — one of the most important operational details: Per the SEC's own FAQ on Rule 201 (SEC.gov): If a stock is already subject to the Alternative Uptick Rule restriction and then declines another 10% intraday from the previous close on that restricted day, the circuit breaker is re-triggered. The restriction then extends for that day's remaining session AND the following day, regardless of the fact that the stock was already restricted. For example: stock restricted on Monday and Tuesday due to a Monday 10% decline. If on Tuesday the stock drops another 10%, the restriction automatically extends through Wednesday. This means stocks in sustained decline can remain under the Alternative Uptick Rule for multiple consecutive days.

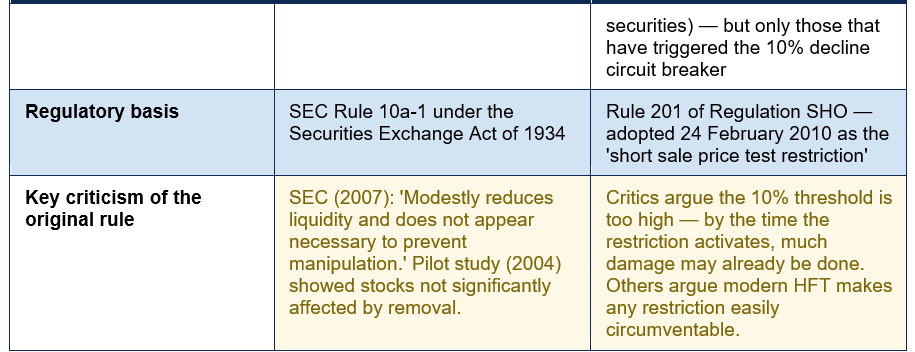

Original vs Alternative Uptick Rule: Key Differences

Understanding how the current rule differs from the 1938 original helps clarify both what has changed and what the current regulation's priorities are. The table below provides a direct side-by-side comparison:

Worked Examples: How the Rule Operates in Practice

Example 1 — Rule Triggered and Applied

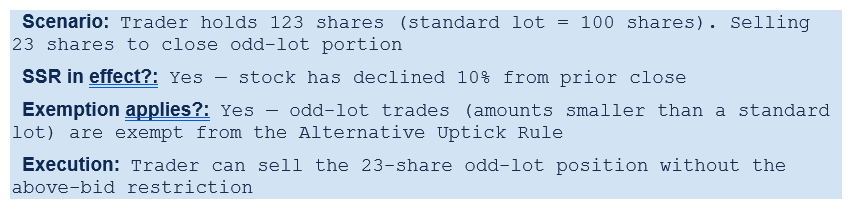

Example 2 — Odd-Lot Exemption (Short Seller Closing an Odd-Lot Position)

Short Selling and Bear Raids: Why the Rule Exists

To understand why the uptick rule was created and why it still matters, it is necessary to understand both short selling and the specific market dysfunction it is designed to prevent.What Is Short Selling?

Short selling is a trading technique in which an investor borrows shares from a broker, sells them at the current market price, and aims to repurchase them later at a lower price. The profit is the difference between the sale price and the repurchase price, minus borrowing costs and fees. If a trader borrows and sells 100 shares at $50 each (receiving $5,000) and later repurchases them at $40 each (paying $4,000), the profit is $1,000. If the price rises instead of falls, the trader must buy back at a higher price and incurs a loss — with theoretically unlimited upside for the loss since prices can rise without bound.Short selling serves a legitimate and important market function. It contributes to price efficiency by allowing traders who believe a stock is overvalued to act on that belief, incorporating negative information into prices faster. It provides liquidity — short sellers are buyers on the way down (when they cover their shorts). It enables hedging strategies for institutional investors. These are the reasons the SEC allows short selling at all — and they are the reasons the 2010 rule is a circuit breaker that permits short selling in most circumstances, rather than a ban.

What Is a Bear Raid?

A bear raid is the specific market manipulation that the uptick rule is designed to prevent. In a bear raid, short sellers — acting together or in rapid succession — execute multiple large short sale orders to artificially drive down the price of a stock. Each downward tick creates new selling by long holders who see their investment declining and panic, which in turn creates more downward pressure, which attracts more short sellers, in a self-reinforcing spiral. The short sellers profit from the artificial decline they have manufactured, then cover their positions at the bottom, leaving genuine long-term investors to absorb the losses.The SHU Law School academic analysis describes the context precisely: 'It was not unusual [prior to 1934] to discover groups of speculators pooling their capital and selling short for the sole purpose of driving down the stock price of a particular security.' The 2008 financial crisis provided a modern example of similar dynamics. Bear Stearns's stock fell from $62.97 to $2.00 in a single week in March 2008, with short sellers identified as significant contributors to the accelerated decline. Lehman Brothers experienced similar pressure before its collapse. These events were central to the political and regulatory momentum that produced the Alternative Uptick Rule in 2010.

UNDERSTANDING THE LIMITATIONS OF THE RULE: The Alternative Uptick Rule is not a ban on short selling and does not prevent a stock from declining. It prevents short sellers from actively accelerating a decline by hitting successive bids. A stock can still fall 10%, 20%, or more even with the rule in effect — it simply means the mechanism of the decline shifts from aggressive short selling (hitting bids) to more organic selling pressure from long holders and from short sellers who must patiently wait for their limit orders to be executed above the bid. The rule is a speed governor on the pace of short-selling-driven declines, not a floor on price.

Exemptions: When the Uptick Rule Does Not Apply

Rule 201 includes several specific exemptions that allow short sales without the above-bid restriction even when the circuit breaker has been triggered. Understanding these exemptions is important for professional traders and institutional participants:- Odd-lot trades: Short sales to close odd-lot positions (amounts smaller than a standard round lot of 100 shares) are exempt. This prevents small, non-market-moving sales from being unnecessarily delayed.

- VWAP (Volume-Weighted Average Price) orders: Short sales executed at a price equal to the consolidated last sale price, or at a price derived from the VWAP of trading activity over the course of the session, are exempt. VWAP trading is a standard institutional execution method, and the SEC permits it to continue without the above-bid restriction because it does not contribute to directional price manipulation.

- Institutional transactions resulting from negative business events: When a company itself must sell stock in response to a negative business event — such as a layoff or restructuring that triggers the release of treasury shares — this institutional selling is exempt. The exemption recognises that these sales are not manipulative in intent.

- Short sales in non-covered securities: The rule applies only to 'covered securities' — exchange-listed equity securities. Securities not meeting this definition are not subject to the restriction.

HOW TRADERS MONITOR SSR STATUS: When the Alternative Uptick Rule is triggered for a specific stock, brokers, trading platforms, and exchanges flag the security with an SSR (Short Sale Restriction) marker that appears on trading terminals, stock screeners, and broker platforms. Many active traders specifically monitor SSR-flagged stocks because the restriction can temporarily reduce downward pressure — stocks that have been in freefall sometimes stabilise or bounce once the restriction activates, creating potential long trading opportunities. Platforms including thinkorswim, Interactive Brokers, and TradeStation all display SSR status in real time.

Arguments For and Against the Uptick Rule

Arguments in Favour of the Rule

-

Prevents bear raids and manipulative short selling: The rule's original purpose — preventing coordinated or piling-on short selling that artificially drives prices below what fundamentals justify — remains valid. Bear raids are not merely a historical concept; accelerated decline dynamics from large institutional short sellers remain a real market phenomenon.

- Protects long-term investors from panic-spiral declines: By slowing the pace at which short sellers can drive a stock downward, the rule gives long-term investors time to make rational decisions rather than being forced to sell into a manipulated decline. The Balance Money's analysis confirms: 'By requiring that any sale take place at a higher price when a stock is down 10% for the day, the uptick rule cuts off additional short sales that could trigger panic-selling and force losses for investors with a long position.'

- Promotes market stability and investor confidence: Predictable circuit breakers that activate when markets stress provide systemic stability signals. Investors who know protection mechanisms exist may be less likely to panic-sell in response to sharp intraday declines.

Arguments Against the Rule

- The 10% threshold may be too high: Critics argue that by the time a 10% decline has occurred, significant damage has already been done to shareholders. A rule that activates after a 10% loss may be insufficient protection for many investors.

- May reduce price efficiency and liquidity: The SEC's own 2007 analysis, which justified the original repeal, found that the rule 'modestly reduces liquidity and does not appear necessary to prevent manipulation.' By preventing short sellers from acting freely, the rule may slow the incorporation of negative information into prices.

- Modern markets may circumvent it: High-frequency trading, algorithmic execution, and the fragmentation of trading across multiple venues have made traditional price-test restrictions easier to work around than in the era of floor trading when the original rule was conceived. Some argue that the rule provides more symbolic than substantive protection in today's electronic markets.

- May allow overvalued shares to go undetected: If short sellers are restricted from acting freely on negative information, overvalued stocks may remain elevated longer than they would otherwise, potentially creating larger eventual corrections.

Conclusion

The uptick rule is one of the most historically significant regulations in US equity market history — a rule that has spent nearly its entire existence in either political controversy or active deployment during periods of market stress. Born in 1938 from the market collapses of the Great Depression, operating unchanged for 69 years, repealed in 2007 in the name of market modernisation, implicated in the acceleration of the 2008 financial crisis, and reinstated in modified form in 2010, it represents the regulatory system's ongoing attempt to balance the legitimate role of short selling with the need to prevent the specific manipulation it can enable at scale.The Alternative Uptick Rule (Rule 201 of Regulation SHO), in force today, is meaningfully different from its 1938 predecessor. Rather than applying continuously to all short sales, it operates as a targeted circuit breaker: activating only when a stock has already declined 10% intraday from its previous close, and then requiring short sellers to sell above the national best bid rather than allowing them to hit bids aggressively. The restriction lasts for the rest of the triggered day and the following trading day, and can be re-triggered if the stock declines another 10% on the restricted day.

For active traders, understanding when the rule is in effect — and recognising what that means for the market dynamics of affected stocks — is practically important. Stocks under SSR (Short Sale Restriction) often stabilise or bounce because the aggressive short selling that was driving them down is forced into passive limit orders. For investors, the rule's existence is a reminder that markets have structural protections that activate during severe individual stock declines — though these protections are circuit breakers, not price floors, and do not prevent further decline from other sources of selling pressure. The uptick rule is one of the most discussed, debated, repealed, and reinstated regulations in US market history. In 2026, it remains in force — and its fundamental purpose, preventing manipulative bear raids from destroying market integrity, remains as relevant as it was when Joseph Kennedy Sr. enacted it nearly a century ago.

Frequently Asked Questions (FAQ)

What is the uptick rule in simple terms?

The uptick rule is a stock market regulation that restricts when short sellers can sell a stock they have borrowed. In simple terms, it prevents short sellers from selling at a price that is the same as or lower than the last traded price (or, under the current 2010 rule, at the current best bid price) when a stock has declined 10% or more from the previous day's close. The idea is to slow down what is called a 'bear raid' — a situation where short sellers repeatedly hit the bid to drive a stock's price lower in a self-reinforcing spiral. By requiring short sellers to sell at a higher price than the current bid, the rule forces them to be passive (placing limit orders) rather than aggressive, which reduces downward momentum. The current version (the Alternative Uptick Rule, Rule 201) only activates when a stock has fallen 10% in a day and stays in effect for the rest of that day and the following day.When does the Alternative Uptick Rule (Rule 201) trigger?

The Alternative Uptick Rule triggers automatically when a stock's price declines by 10% or more intraday from its previous trading day's closing price. The exchanges monitor this in real time and flag the security with an SSR (Short Sale Restriction) marker the moment the threshold is crossed. Once triggered, the restriction applies for the rest of that trading session and the full following trading day. If the stock declines another 10% on the already-restricted day, the circuit breaker re-triggers and the restriction extends for an additional day, per the SEC's official FAQ on Rule 201. For example, if a stock closes at $100 on Monday and falls to $89 on Tuesday, the rule activates on Tuesday and remains in effect through Wednesday's close.What is the difference between the original uptick rule and today's alternative uptick rule?

The original uptick rule (Rule 10a-1, 1938–2007) applied continuously to all short sales on all exchange-listed securities every day, regardless of what the stock's price was doing. Short sellers had to sell at a price above the last trade (a plus tick) or at the last price if the last price movement was upward (a zero-plus tick) at all times. The Alternative Uptick Rule (Rule 201, in force since 2010) is a circuit breaker rather than a continuous restriction. It applies only when a specific stock has already declined 10% intraday from the previous close — and even then, the restriction is defined differently: short sellers must sell above the current national best bid, not above the last trade price. The current rule is therefore less restrictive in normal market conditions (it does not apply at all) but provides targeted protection in the specific situation of severe intraday declines.Why was the uptick rule repealed in 2007?

The SEC repealed the original uptick rule on 3 July 2007 under Chairman Christopher Cox, citing the results of a 2004 pilot study that temporarily removed the rule for a subset of securities. The pilot found that the absence of the rule did not cause the predicted increase in volatility or manipulative short selling, and that liquidity actually improved modestly without the restriction. The SEC concluded that the rule 'modestly reduces liquidity and does not appear necessary to prevent manipulation' and that removing it would bring 'increased uniformity to short sale regulation' and 'level the playing field for market participants.' Within a year of the repeal, the 2008 financial crisis unfolded. While the causal relationship between the repeal and the crisis is disputed, the collapse of Bear Stearns and Lehman Brothers under significant short-selling pressure renewed calls for the rule's return, which was implemented in modified form in 2010.How does the uptick rule affect trading strategy?

For active traders, the uptick rule — specifically the SSR flag when Rule 201 is triggered — has several practical implications. Short sellers must switch from market orders (which can be executed immediately at the current bid) to limit orders placed above the current bid, making short execution slower and less aggressive. This change in order flow dynamics often reduces downward price momentum and can cause temporarily stabilisation or a bounce in SSR-flagged stocks. Many active traders monitor SSR status specifically for long trading opportunities: when a beaten-down stock enters SSR, the reduced short-selling pressure may create a more favourable risk-reward for a long trade based on the expected stabilisation. For algorithmic traders and market makers, the SSR status requires real-time monitoring and adjustment of execution logic for any short sale strategies. The SSR marker is displayed in real time on most major broker platforms and screeners.

External References

1. SEC.gov — Rule 201 Regulation SHO: Frequently Asked Questions (Official SEC FAQ on the Alternative Uptick Rule)https://www.sec.gov/rules-regulations/staff-guidance/trading-markets-frequently-asked-questions-7

2. Wikipedia — Uptick Rule (full history from 1938, including all major legislative milestones)

https://en.wikipedia.org/wiki/Uptick_rule

3. Warrior Trading — The Alternative Uptick Rule Explained for Beginners

https://www.warriortrading.com/alternative-uptick-rule/

4. The Balance Money — What Is the Uptick Rule?

https://www.thebalancemoney.com/uptick-rule-5216596

5. Wall Street Mojo — Uptick Rule: Meaning, Example, History, Exemptions (Updated February 2026)

https://www.wallstreetmojo.com/uptick-rule/

6. Liberated Stock Trader — Short Sale/Uptick Rule: Easy Guide For Traders (November 2025)

https://www.liberatedstocktrader.com/short-sale-rule-ssr/

7. Tokenist — Complete Guide to the Uptick Rule: A-Z Guide (February 2025)

https://tokenist.com/investing/uptick-rule/

8. Seton Hall University Law — The Alternative Uptick Rule: Restoring Short Selling as an Asset to the Market (peer-reviewed academic paper)

https://scholarship.shu.edu/cgi/viewcontent.cgi?article=1386&context=student_scholarship

0 Comments Comments