Credits

What is The Credit Card Rule the Banks Won't Tell You in The UK?

Table of Contents

- The Most Powerful Consumer Right in Your Wallet

- The 10 Things Almost Nobody Knows About Credit Card Protection

- Section 75: The Statutory Right That Makes Your Bank Equally Liable

- The £1 Deposit Secret — The Most Underused Feature of the Law

- When Section 75 Applies — and the Critical Exceptions

- What Section 75 Lets You Claim: Including Consequential Losses

- Chargeback: The Debit Card User's Protection — and the Backup for Everyone

- Section 75 vs Chargeback: Which to Use When

- How to Make a Section 75 or Chargeback Claim: Step by Step

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Most Powerful Consumer Right in Your Wallet

Somewhere in the consumer protection landscape of the United Kingdom sits a legal right so powerful, so broadly applicable, and so consistently underused that MoneySavingExpert has called it one of the most important financial tools available to UK consumers. Most card companies do not mention it when you sign up. Most bank staff on customer service lines do not spontaneously explain it. And most people who would benefit from it have either never heard of it or believe it does not apply to their situation when it does.The rule is Section 75 of the Consumer Credit Act 1974. It makes your credit card company equally, legally liable alongside any retailer for purchases worth more than £100 and up to £30,000 — not as a courtesy, not as a scheme they can opt out of, but as a statutory right under UK law. The company can have gone bust. The goods can have been delivered defective. The service can have been misrepresented. You can have paid only a £1 deposit on the credit card. It does not matter. The bank is on the hook — equally with the seller — and has been since 1974.

Running alongside Section 75, but applying to debit cards, smaller purchases, and a wider range of situations, is chargeback — a card scheme mechanism most banks understand internally but frequently fail to explain to customers. Experian's guidance specifically notes that cardholders 'should be prepared to explain the chargeback rule to bank staff, as many don't know about it.' The combination of these two protections gives UK card users a safety net under virtually every non-cash purchase they make — provided they know it exists. This guide explains both, with all the hidden rules that banks leave out.

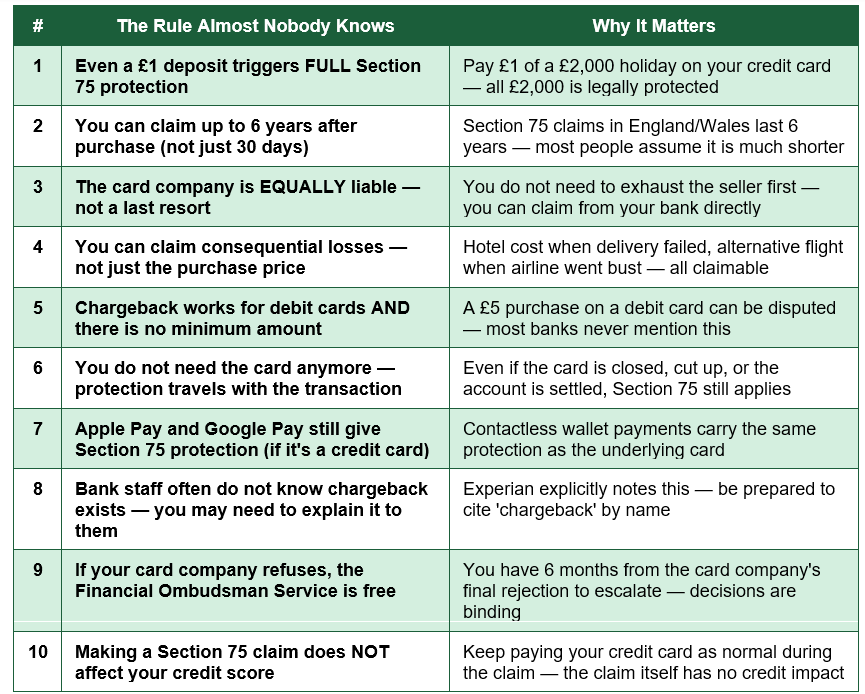

The 10 Things Almost Nobody Knows About Credit Card Protection

Before examining the rules in depth, the table below provides a quick reference to the ten most surprising, least-publicised facts about Section 75 and chargeback — the rules the banks simply do not volunteer:

The rule in one sentence: Pay £1 of any purchase over £100 on a credit card — your bank is legally equally liable for the full amount if anything goes wrong — Section 75 of the Consumer Credit Act 1974 creates 'joint and several liability' meaning the card provider and the retailer are equally responsible — this is not a scheme that can be opted out of; it is UK law (Consumer Credit Act 1974, s.75)

Section 75: The Statutory Right That Makes Your Bank Equally Liable

Section 75 of the Consumer Credit Act 1974 establishes what lawyers call 'joint and several liability.' This phrase means that your credit card company and the retailer are equally responsible for any breach of contract or misrepresentation in a qualifying transaction. You can pursue either one, or both, for the full amount. The card company cannot direct you back to the retailer first. The retailer's insolvency does not relieve the card company of its obligation. If the retailer has disappeared, the bank is still liable.The elegance of the law is in its breadth. It covers face-to-face purchases, online purchases, telephone orders, and mail order. It covers domestic retailers and international ones. It covers goods and services. It covers flights, holidays, cars, electronics, kitchen appliances, building work, and furniture. The relevant question is not what type of purchase it is but whether it meets three conditions: it was paid for (in whole or in part) using a personal credit card; the total cost of the individual item or linked set of items exceeds £100; and the total cost is £30,000 or less.

The £1 Deposit Secret — The Most Underused Feature of the Law

The single most surprising and most underused provision of Section 75 is the deposit rule. If you pay any portion of a qualifying purchase using your credit card — including a deposit that might be as small as £1, with the remainder paid by debit card, cash, or bank transfer — the credit card company becomes jointly and severally liable for the entire transaction value, not just the deposit amount you put on the card.The practical implication is significant. Booking a £3,000 family holiday and putting a £200 deposit on your credit card? The full £3,000 is protected. Paying a £500 deposit on a £15,000 kitchen and putting it on your credit card? The full £15,000 installation contract is covered. The card company's liability is not proportional to the amount charged to the card — it is proportional to the total value of the transaction, as long as the credit card was used for any part of the payment and the total value falls between £100 and £30,000.

Why banks don't explain this: Card companies are legally obligated to honour Section 75 claims when valid — but they are not legally obligated to explain the law's provisions to you proactively. The incentive structure runs in the opposite direction: the more cardholders understand this right, the more Section 75 claims card companies must process and pay. MoneySavingExpert, MoneyHelper, and consumer rights experts consistently identify this as one of the most significant information gaps in UK personal finance.

When Section 75 Applies — and the Critical Exceptions

Understanding the exceptions to Section 75 is as important as understanding its scope, because several common modern payment scenarios fall outside its protection in ways that are not obvious:- • PayPal payments break the 'debtor-creditor-supplier' link: Section 75 requires a direct legal relationship between you, your credit card company, and the retailer. When you pay through PayPal (or a similar intermediary payment processor), the legal contract for the purchase is between you and PayPal, not between you and the retailer directly. This breaks the statutory chain that Section 75 requires, and most PayPal transactions paid using a credit card do not benefit from Section 75 protection.

- Amazon Marketplace third-party sellers are not covered: Buying from Amazon directly is covered if you pay by credit card. Buying from a third-party seller through the Amazon Marketplace is not, because the contract is between you and the third-party seller via the Amazon platform, not directly with the retailer who supplied the goods. Amazon's own A-to-Z guarantee and chargeback are the alternative routes.

- Business credit cards do not qualify: Section 75 protects personal consumers, not businesses. Purchases made on a business credit card — even if the business is a limited company — are not covered. Sole traders are treated as individuals and may qualify, but limited company purchases using business cards do not.

- Individual items under £100 are not covered, even if the total exceeds £100: The £100 threshold applies per item, not per transaction. Buying three dresses at £80 each (total £240) does not trigger Section 75 for any individual dress. Buying a single dress at £150 does. The exception is linked items — if you buy a matching set sold as one unit, the total price of the set is used.

- Gift cards bought with a credit card are not themselves protected — but the inability to use a valid gift card is: If you buy a gift card using your credit card and the gift card is never used, Section 75 does not cover the gift card purchase. However, if you buy a gift card and then cannot use it because the issuing company has gone out of business, you can potentially claim back the value of the unused gift card.

What Section 75 Lets You Claim: Including Consequential Losses

The scope of a successful Section 75 claim extends well beyond simply getting the purchase price back. UK Finance's guidance on the scheme confirms that 'as well as the amount you actually spent on the card (such as a deposit), you can also recover your full losses, sometimes including consequential expenses.' This is the element of Section 75 that most people — and many bank staff — do not know about.Consequential losses are the additional costs you incur as a result of the seller's failure. If you booked a flight that was cancelled because the airline went into administration, Section 75 does not just cover the flight cost — it can cover the cost of the alternative flight you had to book, the hotel you had to pay for unexpectedly, and the taxis and transfers you incurred because the timing changed. If a sofa was delivered fundamentally defective and you had to stay in a hotel while your home was being repaired, that hotel cost may be recoverable.

Consequential loss claims require clear evidence — receipts, invoices, timelines, and a documented link between the seller's failure and the costs incurred. They are worth raising specifically in your claim letter rather than just asking for the purchase price back, particularly where the disruption caused genuine, quantifiable additional expense.

Chargeback: The Debit Card User's Protection — and the Backup for Everyone

Chargeback is not the same as Section 75. It is not a legal right. It is a voluntary rule operated by the card networks — Visa, Mastercard, and American Express — that allows your card issuer to attempt to reverse a transaction by recovering the funds from the merchant's bank. It applies to credit cards, debit cards, and prepaid cards, and there is no minimum purchase amount. A £5 purchase on a debit card can be disputed under chargeback if the goods never arrived.The time limit for chargeback is the critical constraint that makes it less powerful than Section 75 for people who discover a problem later: it is typically 120 days from the transaction date, or from the date when you expected to receive the goods or service (whichever is later). For a concert ticket purchased in January for a July event, the 120-day clock starts in July when the concert was due to happen — not in January when you bought the ticket. For a purchase whose delivery date is unspecified, the clock typically starts from the transaction date.

The debit card user's toolkit: If you primarily use a debit card and discover you have been charged twice, that a subscription continued after cancellation, that goods you ordered never arrived, or that you received counterfeit or significantly different items, chargeback is your protection — and the bank is not required to volunteer it. Contact your bank, explain you are disputing the transaction, specifically use the word 'chargeback,' and ask for the transaction to be reversed. If the bank says it cannot help, ask to speak to someone in their disputes team and reference the Visa/Mastercard chargeback scheme rules.

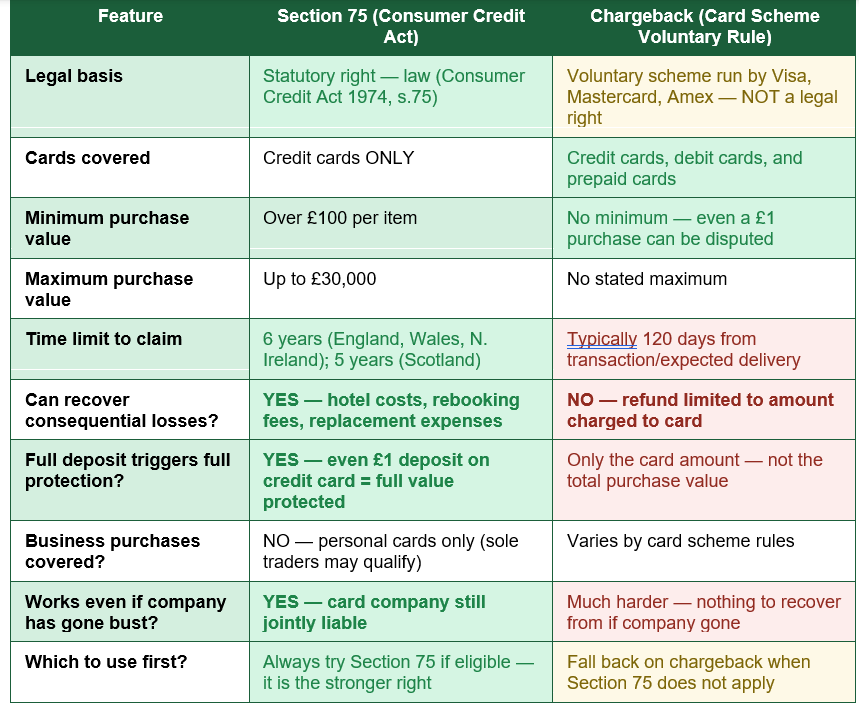

Section 75 vs Chargeback: Which to Use When

The comparison table below sets out every relevant dimension of Section 75 and chargeback side by side, enabling you to identify immediately which protection applies to your specific situation:

The decisive advantage of Section 75: 6 years vs 120 days — Section 75 gives you 6 years to claim in England, Wales, and Northern Ireland; chargeback requires a claim within approximately 120 days of the transaction or expected delivery — making Section 75 the more powerful protection for purchases where problems emerge gradually or late.

How to Make a Section 75 or Chargeback Claim: Step by Step

Both Section 75 and chargeback claims follow a similar practical process. The key difference is the legal basis — and the escalation route if the bank refuses. Here is the step-by-step approach:- Try the seller first (usually): Before claiming from your card company, attempt to resolve the issue directly with the retailer or service provider. Most card companies expect this as the first step — it demonstrates good faith and in many cases resolves the issue faster. Keep records of all contact: dates, what was said, any written responses. If the company has gone into administration or is refusing to engage, skip directly to step two.

- Contact your credit card company and explicitly invoke Section 75: Do not just call to 'complain about a purchase.' Use the phrase 'I want to make a Section 75 claim' or 'I would like to make a chargeback dispute.' This language routes your call to the correct team and avoids your complaint being handled as a general customer service issue. Many people who should succeed with Section 75 fail because they do not explicitly name the statutory right they are invoking.

- Gather and submit your evidence: You will need proof of purchase (confirmation email, receipt, or bank statement showing the transaction), evidence of the problem (photographs of defective goods, correspondence with the retailer, proof of non-delivery), and for Section 75, evidence of the breach of contract or misrepresentation. For consequential losses, include all relevant receipts and a clear explanation of the causal link between the seller's failure and the additional cost.

- Follow up in writing: After any phone call, send an email or letter summarising what was discussed and what you have submitted. Create a clear paper trail. If the bank subsequently tries to reject your claim, your written record of the conversation is important evidence.

- If rejected, escalate to the Financial Ombudsman Service: If your card company refuses your Section 75 or chargeback claim and you remain unsatisfied, you can take your case to the Financial Ombudsman Service (FOS) free of charge. You must first make a formal complaint to the card company and wait up to 8 weeks for a final response — or receive a 'deadlock letter' confirming they will not change their position. The FOS is independent, its decisions are binding on the card company, and there is no fee for the consumer. You have 6 months from the card company's final response to submit to the FOS.

Conclusion

Section 75 of the Consumer Credit Act 1974 is the most powerful, most underused consumer protection right in the United Kingdom. It makes your credit card company legally equally liable alongside any retailer for purchases between £100 and £30,000 — and it does so on the basis of any credit card payment, including a £1 deposit, regardless of whether the seller still exists, regardless of whether you have the card any longer, and regardless of whether the bank staff member on the phone knows it applies to your situation. You have six years to claim in England, Wales, and Northern Ireland. The protection travels with the transaction, not the card.Chargeback is its complement, not its replacement: broader in card coverage (including debit and prepaid cards) and purchase value range (no minimum), but narrower in time (120 days) and in what you can recover (the card charge only, not consequential losses). Together, they cover the vast majority of card-based consumer transactions in the UK. The combination of a credit card for purchases above £100 and the knowledge of how to use both protections is, in the view of consumer rights experts and personal finance organisations alike, one of the most financially valuable pieces of knowledge a UK consumer can have.

The banks are not going to explain these rules to you at sign-up or at the till. The law does not require them to. But the law does require them to honour Section 75 when you invoke it correctly — and the Financial Ombudsman Service is there, free of charge, if they refuse. Read this guide again before your next significant purchase. Put even £1 of it on a credit card you pay off in full. And keep this guide saved somewhere you can find it the next time something goes wrong.

Frequently Asked Questions (FAQ)

Can I really claim Section 75 if I only paid a deposit on my credit card?

Yes — this is one of the most powerful and least-known features of the law. Section 75 of the Consumer Credit Act 1974 does not require you to have paid the full purchase price on your credit card. If you pay any portion of a qualifying purchase — even just the deposit — the credit card company becomes jointly and severally liable for the full transaction value. This means a £500 credit card deposit on a £15,000 kitchen gives you Section 75 protection for all £15,000 if something goes wrong with the contract.My credit card is now closed. Can I still claim Section 75?

Yes. Section 75 protection is tied to the original transaction, not to the current status of the card or account. If you paid for something on a credit card that you have since closed, cancelled, or cut up, and a qualifying problem arises within the six-year claim window, you can still make a Section 75 claim against the card issuer. Contact the card company (whose details you should be able to find through a search or your old correspondence) and follow the same claim process as you would with an active card.Does chargeback work for a debit card purchase?

Yes — chargeback applies to credit cards, debit cards, and prepaid cards. It is the primary card protection available to debit card users, since Section 75 is credit card only. There is no minimum purchase amount for chargeback, making it applicable even for small purchases where Section 75's £100 threshold is not met. The key constraint is the time limit — typically 120 days from the transaction date or the date you expected to receive the goods or service. Contact your bank, use the word 'chargeback' specifically, and be prepared to explain what it is if the person you speak to is not familiar with it.Will making a Section 75 claim affect my credit score?

No. Making a Section 75 claim does not affect your credit score. The claim is a consumer rights dispute, not a financial default. However, it is important to continue making your normal credit card payments throughout the claims process. If you stop paying your credit card bill while waiting for a Section 75 claim to resolve, any missed or late payments will be recorded on your credit file and will affect your credit score — but the claim itself will not.What do I do if my credit card company refuses my Section 75 claim?

If your card company refuses your Section 75 or chargeback claim and you believe the refusal is wrong, escalate your complaint formally. First, make a written formal complaint to the card company and ask for their 'final response' or 'deadlock letter.' Wait up to eight weeks. Once you receive their final response — or after eight weeks if you have had no resolution — you can take the case to the Financial Ombudsman Service (FOS). The FOS is completely free to use, independent of the card company, and its decisions are legally binding on the card company. You can submit your case online at financial-ombudsman.org.uk. You have six months from the card company's final response to do so.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. MoneyHelper — Section 75 and Chargeback Protection (Official Government-backed Guidance)

https://www.moneyhelper.org.uk/en/everyday-money/credit/how-youre-protected-when-you-pay-by-card

2. UK Finance — Chargeback and Section 75 (Industry Body Official Guidance)

https://www.ukfinance.org.uk/our-expertise/cards/chargeback-and-section-75

3. MoneySavingExpert — Section 75 Refunds: Credit Card Purchase Protection

https://www.moneysavingexpert.com/reclaim/section75-consumer-credit-act/

4. Experian — Consumer Credit Act Section 75: Credit Card Protection

https://www.experian.co.uk/consumer/credit-cards/guides/section-75-protection.html

5. Consumer Rights Expert — Section 75 Credit Card Protection Guide (April 2026)

https://www.consumerrightsexpert.co.uk/section-75-credit-card-protection.html

6. UKLegalGuides.com — How Section 75 Protects Consumers (England & Wales, July 2026)

https://www.uklegalguides.com/how-section-75-protects-consumers/

7. Financial Ombudsman Service — How to Complain About a Credit Card Company

https://www.financial-ombudsman.org.uk/consumers/how-to-complain

8. Legislation.gov.uk — Consumer Credit Act 1974, Section 75 (Original Statute)

https://www.legislation.gov.uk/ukpga/1974/39/section/75

0 Comments Comments