Credits

What is Universal Credit Claim in the UK?

Table of Contents

- Who Is Eligible for Universal Credit in 2026?

- Universal Credit Rates 2026/27: What You Can Receive

- The Taper Rate and Work Allowance: How Work Affects Your UC

- The Savings Rules: What Counts and How It Affects Your Award

- The Five-Week Wait: The Most Significant Practical Barrier

- The April 2026 Changes: What Is New This Year

- Two-Child Limit Abolished (6 April 2026)

- Standard Allowance Increased by 6.2% (April 2026)

- LCWRA Element Reduced for New Claimants

- How to Claim Universal Credit: The Step-by-Step Process

- Myths vs Reality: What Prevents Eligible People from Claiming

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Universal Credit is the UK's primary means-tested benefit, supporting around six million households in 2026 — and yet it remains one of the most misunderstood entitlements in the British welfare system. The most persistent and damaging misunderstanding is that it is only for people who are out of work. In reality, approximately 40% of all Universal Credit claimants are in employment, using UC to top up low wages, cover housing costs, access childcare support, or manage the costs of caring for a disabled family member. Working does not disqualify you. Having savings does not necessarily disqualify you. Being self-employed does not disqualify you. Being a student, in most circumstances, does — but even there, exceptions exist.

April 2026 brought some of the most significant changes to Universal Credit since its introduction in 2013. The two-child limit — which had prevented families from claiming the child element for a third or subsequent child — was abolished from 6 April 2026, benefiting an estimated 700,000 families with three or more children. Standard allowances increased by 6.2% from the same date — the largest real-terms increase to UC since the pandemic uplift. At the same time, the health-related Limited Capability for Work and Work-Related Activity (LCWRA) element was restructured, with new claimants receiving a significantly lower rate than those already receiving it. The House of Commons Library's June 2026 briefing estimates that 750,000 claimants will receive the new lower LCWRA rate by 2029/30.

This guide covers everything you need to know about your right to claim Universal Credit in 2026: who qualifies, the 2026/27 rates for every element, how the taper rate and work allowance system works in practice, the savings rules, the five-week wait and what to do about it, the changes introduced in April 2026, the myths that prevent eligible people from claiming, and the step-by-step claim process. Whether you are applying for the first time, being migrated from a legacy benefit, or checking whether a change in your circumstances affects your entitlement, this is the complete 2026 reference.

Who Is Eligible for Universal Credit in 2026?

Universal Credit is available to people of working age who meet all of the following basic eligibility criteria:- Age: You must be 18 or over. Some 16 and 17-year-olds can claim in limited circumstances — for example, if they are responsible for a child, are estranged from their parents, are at serious financial risk, or have a disability.

- Under State Pension age: You must be below State Pension age (currently 66). When you reach 66, Universal Credit stops and you move to Pension Credit. The switch is not automatic — you must make a new claim for Pension Credit. For couples where one partner is under 66 and one is over 66, the couple must claim Universal Credit until both partners reach State Pension age.

- Resident in the UK: You must be habitually resident in England, Scotland, or Wales. Northern Ireland has a separate but broadly similar UC system administered by the Department for Communities. Non-UK nationals may face additional eligibility tests depending on their immigration status.

- Savings and capital below £16,000: If you have savings, investments, or other capital above £16,000, you cannot claim UC. Savings between £6,000 and £16,000 reduce your award — see the savings section below. Savings below £6,000 are completely disregarded.

- On a low income or out of work: There is no single income cut-off for Universal Credit. Your entitlement tapers down as your income rises, reaching zero when your earnings are high enough — but where that threshold sits depends on your household size, housing costs, and other elements in your award.

The most important thing most people don't know: 40% of UC claimants are in employment — Universal Credit is a working-age benefit that supports both unemployed people and those in low-paid or part-time work — being employed does not disqualify you, it simply means your award reduces gradually as your earnings rise above your work allowance (DWP Universal Credit Statistics, 2026).

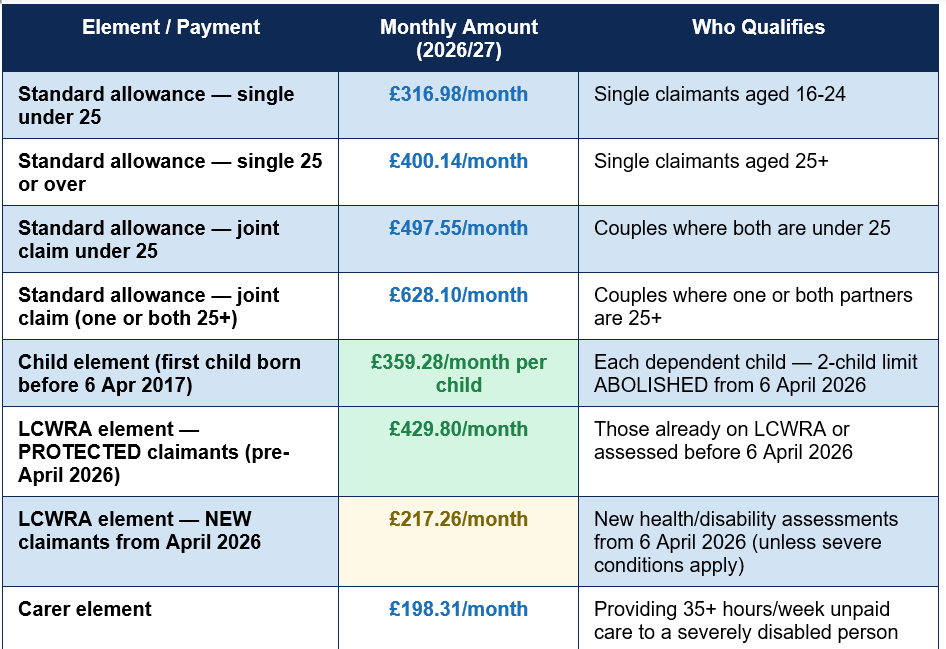

Universal Credit Rates 2026/27: What You Can Receive

Universal Credit is built from a standard allowance — the baseline payment for the adult or couple — plus additional 'elements' added on top for housing, children, disability, and caring responsibilities. The table below shows all current 2026/27 rates and who qualifies for each:

The April 2026 LCWRA change explained: Before April 2026, the health element for people assessed as having Limited Capability for Work and Work-Related Activity was £432.27/month for all recipients. From April 2026, this was split into two rates. Existing claimants who were already receiving the LCWRA element, and those who reported their condition before April 6 and were subsequently assessed as LCWRA, receive the protected higher rate of £429.80/month. New claimants who report a health condition from April 6, 2026 onward receive the lower rate of £217.26/month — unless they also meet the 'severe conditions' criteria defined by DWP, in which case they may qualify for the higher amount. Seek specialist welfare rights advice if you believe you meet the severe conditions criteria.

The Taper Rate and Work Allowance: How Work Affects Your UC

One of the most important and least understood features of Universal Credit is how it interacts with employment income. This is the point where the legacy benefit system's 'cliff edges' — where earning above a threshold could cause an entire benefit to stop abruptly — have been replaced with a gradual, smooth reduction. Understanding this is essential to understanding why UC is genuinely designed to make work pay.The taper rate is 55%. This means that for every £1 you earn above your work allowance, your Universal Credit reduces by 55p — and you keep 45p. There is no point at which earning more makes you financially worse off overall. UC simply reduces gradually until it reaches zero, at which point you are no longer eligible for that payment period.

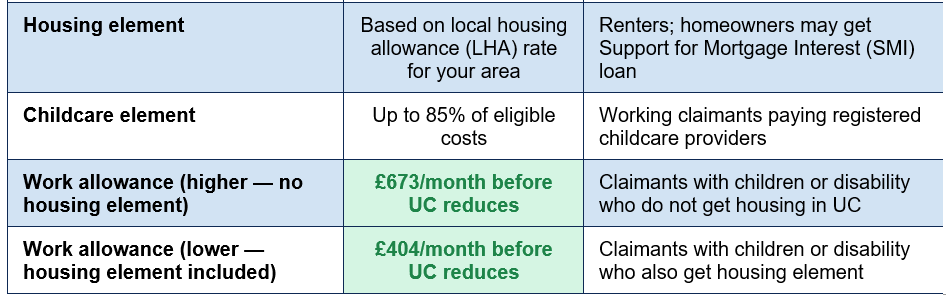

Not everyone has a work allowance. You only receive a work allowance if you have dependent children or if you have been assessed as having limited capability for work. If you have no children and no qualifying disability, your UC reduces from the first pound you earn. If you do have a work allowance, your earnings below that threshold are completely ignored — the 55% taper only applies to earnings above it.

A worked example for a single parent with housing element: Work allowance (lower) = £404/month. Monthly earnings = £1,000. Earnings above work allowance = £596. UC reduction = 55% × £596 = £327.80. If their UC maximum entitlement is £393.45/month, they receive £393.45 - £327.80 = £65.65/month. They keep every penny they earn, and continue to receive UC support on top.

The Savings Rules: What Counts and How It Affects Your Award

Many people wrongly assume they cannot claim Universal Credit because they have savings. The savings rules are more generous than most people expect — and they distinguish between savings that disqualify you and savings that simply reduce your award:- Under £6,000 in savings: Your savings are completely ignored in the UC calculation. They have no effect on your eligibility or your award amount.

- Between £6,000 and £16,000 in savings: The first £6,000 is disregarded. The remainder reduces your UC by a calculated 'tariff income.' For every £250 (or part thereof) above £6,000, DWP treats you as having a monthly income of £4.35, which is then deducted from your UC award. For example, with £8,000 in savings: £8,000 - £6,000 = £2,000 excess. Eight lots of £250 = 8 × £4.35 = £34.80 monthly reduction. This is not a large reduction for modest savings, and it should not deter eligible people from claiming.

- Over £16,000 in savings: You are not eligible to claim Universal Credit while you hold capital above this threshold. This includes savings, investments, shares, and some property (though your main home is excluded from the calculation).

What counts as savings for UC purposes includes current and savings account balances, ISA balances, stocks and shares, premium bonds, and most other financial assets. Your main home does not count. A car does not count. Personal possessions do not count.

The Five-Week Wait: The Most Significant Practical Barrier

The single most important practical fact about claiming Universal Credit that DWP does not prominently advertise is the five-week wait. Universal Credit is paid monthly in arrears, and after you make your claim, the first payment does not arrive for approximately five weeks — one full assessment period plus up to seven additional days for processing. This is structural and applies to almost all new claimants, regardless of how quickly or accurately they complete the claim process.For anyone who has just lost a job or experienced a significant drop in income, five weeks without UC income while awaiting the first payment is a genuine and serious hardship. There are two important things to know about this wait:

- You can request a UC Advance payment: An advance is essentially an interest-free loan of up to one month's UC, paid within a few days of your claim being approved. You repay it from your subsequent UC payments, typically over 24 months. It does not prevent you from receiving your full UC — it is a bridging payment. Ask for it at your initial Jobcentre appointment or through your online journal. This is not prominently explained in the claim process — you often need to ask specifically.

- If you are moving from a legacy benefit, you may get 2 weeks' run-on: If you are transitioning from income-related Employment and Support Allowance (ESA) or Housing Benefit following a UC claim, you may be entitled to two weeks of continued legacy benefit payment while you wait for UC to begin. This does not apply to all legacy benefits and is worth confirming with Citizens Advice.

CRITICAL: Universal Credit is NOT backdated. Your claim starts from the date you submit it — not from the date you first became eligible. Every day you delay applying for UC is a day's entitlement you permanently lose. If you think you may be eligible, claim immediately — even before you have gathered all the information you will need — as you can update your claim later. Do not wait until a convenient moment.

The April 2026 Changes: What Is New This Year

April 2026 brought several significant changes to Universal Credit that affect both existing claimants and new applicants. Understanding what changed — and which changes are beneficial versus which require careful consideration — is essential for anyone claiming or considering claiming:Two-Child Limit Abolished (6 April 2026)

The most widely welcomed change in April 2026 was the abolition of the two-child limit for the UC child element. Previously, families could only receive the child element for their first two children — a third or subsequent child attracted no additional child element. From 6 April 2026, this restriction was removed. Every dependent child in a qualifying household now generates a child element of £359.28 per month. Citizens Advice confirms this change applies automatically for most claimants, though errors in application have been reported and existing claimants should check their award letters to ensure all children are being included correctly.Standard Allowance Increased by 6.2% (April 2026)

From 13 April 2026, Universal Credit standard allowances increased by 6.2% — an above-inflation rise that the House of Commons Library describes as 'the largest real-terms increase to UC since the pandemic uplift.' This affects all UC claimants and is reflected in the 2026/27 rates shown in the table above. The Universal Credit Act 2025 legislates for above-inflation increases to the standard allowance to continue for the four financial years from 2026/27, meaning further above-inflation rises are planned.LCWRA Element Reduced for New Claimants

The health element — the LCWRA addition for those assessed as unable to work due to disability or health conditions — was reduced from approximately £432/month to £217.26/month for most new claimants from April 2026. This is one of the most contested changes in the 2026 reforms, with disability charities including the Joseph Rowntree Foundation and a coalition of campaigning organisations arguing it will increase hardship for disabled people. Existing LCWRA recipients are protected on the higher rate until at least 2029/30, but those newly assessed from April 2026 receive significantly less — the House of Commons Library estimates those affected will be around £2,700/year lower than the protected cohort by 2029/30.How to Claim Universal Credit: The Step-by-Step Process

Claiming Universal Credit is done entirely online at gov.uk/universal-credit. The process takes between 30 minutes and an hour depending on your circumstances. Before you start, gather the following:- Your National Insurance number.

- Your bank or building society account details (UC is paid into a bank account — no exceptions).

- Information about your housing costs (rent amount, landlord name and address).

- Details of any income, savings, investments, or property.

- Your GOV.UK One Login credentials — or create one at account.gov.uk before starting.

- Complete the online application at gov.uk/universal-credit: The form takes you through your circumstances step by step. Both partners must verify their identity individually if making a joint claim. If you cannot complete the claim online, call the UC helpline on 0800 328 5644.

- Await DWP contact and book your initial appointment: Within a few days of submitting, DWP will contact you to arrange either a phone appointment or a Jobcentre appointment. This is mandatory — failing to attend can result in your claim being closed.

- Agree your Claimant Commitment: At your first appointment you will be asked to agree a Claimant Commitment — a set of work-related conditions tailored to your circumstances. This is not a generic document. If anything in it is inaccurate, unreasonable given your health or caring responsibilities, or unclear, raise it at the appointment rather than simply signing. You can ask for changes.

- Request an Advance payment if needed: Ask specifically for a UC Advance payment if you cannot manage financially during the five-week wait. This is not automatic — you must request it. It is interest-free and repaid from future UC payments.

- Report changes promptly through your online journal: Any change in your circumstances — earnings, housing, health, relationships, dependent children — must be reported promptly through your UC online journal. Failing to report changes can result in overpayments that DWP will recover from future UC awards.

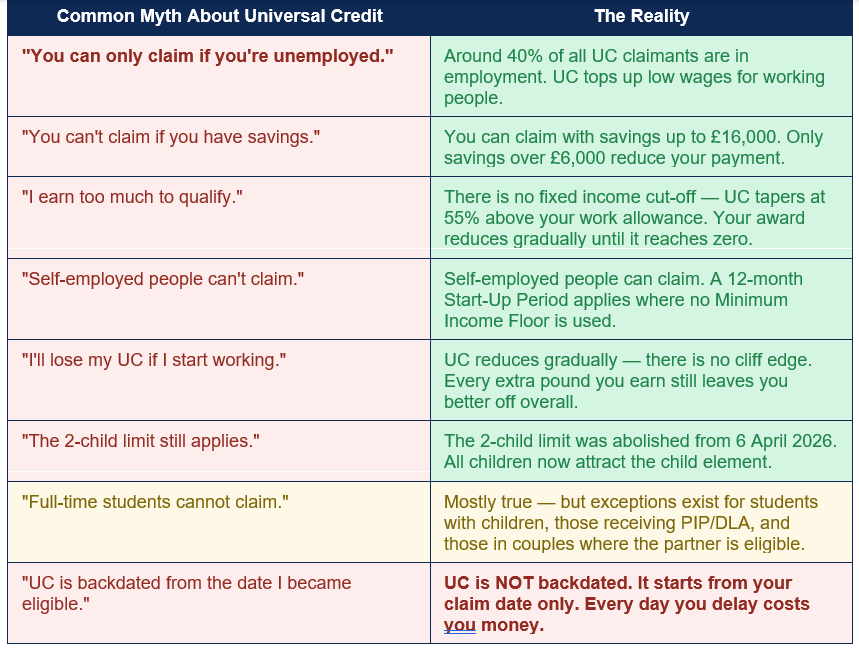

Myths vs Reality: What Prevents Eligible People from Claiming

Significant numbers of households eligible for Universal Credit are not claiming it. The following table addresses the most common misconceptions that contribute to under-claiming:

Conclusion

Universal Credit in 2026 is a fundamentally different benefit from the one many people picture when they hear the name. It is not only for unemployed people — 40% of its six million claimant households contain at least one working adult. It is not only for families without savings — you can have up to £16,000 in savings and still claim, with only amounts above £6,000 affecting your award. It is not only for people with very low incomes — the 55% taper rate means the threshold at which UC reaches zero depends on your household's specific elements and circumstances rather than a single fixed income cut-off.The April 2026 changes brought both welcome reforms and controversial cuts. The abolition of the two-child limit is a straightforwardly positive development for families with three or more children — affecting an estimated 700,000 families. The above-inflation standard allowance increase benefits all claimants and is legislated to continue. The reduction in the LCWRA element for new health claimants is more complex — existing recipients are protected, but those newly assessed from April 2026 receive significantly less and should seek specialist welfare rights advice if they believe they may meet the severe conditions criteria for the higher amount.

The single most important practical message in this guide remains the one in the quick-answer box at the top: Universal Credit is not backdated. If you are eligible — or think you might be — claim today. Use the Turn2Us benefits calculator, entitledto, or the Better Off calculator to estimate your entitlement before you apply. If your claim is refused or your award is lower than expected, request a Mandatory Reconsideration within one month and contact Citizens Advice or a welfare rights adviser for free support. The system is complex, but the entitlements are real — and every week you do not claim is money you cannot recover.

Frequently Asked Questions (FAQ)

Can I claim Universal Credit if I am working?

Yes. Around 40% of Universal Credit claimants are in employment. UC tops up low wages, contributes to housing costs, and supports childcare costs even when you are working. Your award reduces gradually via the 55% taper rate as your earnings rise above your work allowance — there is no cliff edge where your UC stops suddenly when you start work. For every extra pound you earn, you keep 45p and UC reduces by 55p. You are always better off earning more. Use the Turn2Us calculator or entitledto to estimate how much you might receive given your current earnings and circumstances.What is the two-child limit and has it really been abolished?

The two-child limit was a restriction that prevented UC claimants from receiving the child element for a third or subsequent child. It was abolished from 6 April 2026. From that date, every dependent child in an eligible household generates a child element of £359.28 per month, regardless of whether they are a first, second, third, or later child. Citizens Advice confirms this change and notes it benefits an estimated 700,000 families with three or more children. If you are an existing UC claimant with three or more children, check your award letters to confirm all children are now included — errors in application have been reported.What can I do about the five-week wait for my first payment?

Request a UC Advance payment as soon as your claim is submitted or at your first Jobcentre appointment. A UC Advance is an interest-free loan of up to one month's UC, typically paid within a few days of your claim being accepted. You repay it from your subsequent UC payments, usually over 24 months. It does not reduce the total UC you receive — it is a bridging payment. Ask specifically for it; it is not offered automatically. If you are migrating from income-related ESA or Housing Benefit, ask about the two-week run-on of legacy payments that may apply in your case.My UC claim was refused or my award seems too low. What can I do?

If you disagree with a UC decision, you have one month from the date of the decision to request a Mandatory Reconsideration (MR). Submit your MR through your UC online journal or in writing to DWP, explaining why you believe the decision is wrong and providing any supporting evidence. DWP must review the decision. If the MR upholds the original decision and you still disagree, you can appeal to an independent Social Security and Child Support Tribunal within one month of the MR decision. Citizens Advice provides free help with MR requests and appeals, including evidence preparation. Continue claiming while appealing — stopping your claim could cost you money.What free tools can I use to check whether I am eligible and how much I might get?

Three free, independent online benefits calculators are widely recommended for checking UC eligibility and estimating your award: Turn2Us (turn2us.org.uk), entitledto (entitledto.co.uk), and the Policy in Practice Better Off calculator. All three allow you to input your circumstances and see an estimated breakdown of what you might receive, including all elements. None of these tools share your data with DWP. For personalised free advice, contact Citizens Advice on 0808 223 1133 or visit citizensadvice.org.uk. The UC helpline is 0800 328 5644 (Monday to Friday, 8am to 6pm).External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. GOV.UK — Universal Credit: How to Claim

https://www.gov.uk/universal-credit/how-to-claim

2. GOV.UK — Universal Credit: What You'll Get (2026/27 rates)

https://www.gov.uk/universal-credit/what-youll-get

3. Citizens Advice — Check How Universal Credit Has Changed in 2026

https://www.citizensadvice.org.uk/benefits/universal-credit/claiming/check-how-universal-credit-is-changing-in-2026/

4. Citizens Advice — Check How Much Universal Credit You'll Get

https://www.citizensadvice.org.uk/benefits/universal-credit/on-universal-credit/check-how-much-universal-credit-youll-get/

5. House of Commons Library — Changes to Universal Credit Rates from April 2026 (June 2026)

https://commonslibrary.parliament.uk/research-briefings/cbp-10358/

6. GovExplained — Universal Credit: Eligibility, How to Apply, and Rates 2026/27

https://govexplained.co.uk/money-and-benefits/universal-credit/

7. Turn2Us — Free Benefits Calculator

https://benefits-calculator.turn2us.org.uk/

8. entitledto — Free Universal Credit and Benefits Calculator

https://www.entitledto.co.uk/

0 Comments Comments