Finance

Financial Reality of Divorce for a Father in the US

Table of Contents

Divorce is one of the most financially disruptive events that can occur in a person's life — and for a man with children in the United States, its financial consequences are particularly complex, wide-ranging, and long-lasting. Beyond the emotional weight of family separation, a divorcing father faces a simultaneous restructuring of nearly every dimension of his financial life: housing costs, legal fees, child support obligations, potential spousal support, asset division, retirement account impacts, tax filing status changes, and the need to rebuild a single-income household from whatever resources remain after the settlement.

Yet despite the profound financial significance of divorce for fathers, many men enter the process with limited understanding of what to expect. The conversation around divorce and finances is often framed in general terms, leaving men without the specific, data-grounded picture they need to plan effectively, negotiate fairly, and protect their long-term financial health — while continuing to meet their obligations to their children, which remain a genuine and non-negotiable priority.

This guide provides that picture. Drawing on current data from the US Census Bureau, the American Academy of Matrimonial Lawyers, the Brookings Institution, and family law research, it presents the financial reality of divorce for American fathers with children across every major cost dimension — from legal fees and child support to asset division, retirement impacts, and the path to financial rebuilding. The aim is not to discourage but to prepare: informed fathers navigate this process better, protect more, and rebuild faster.

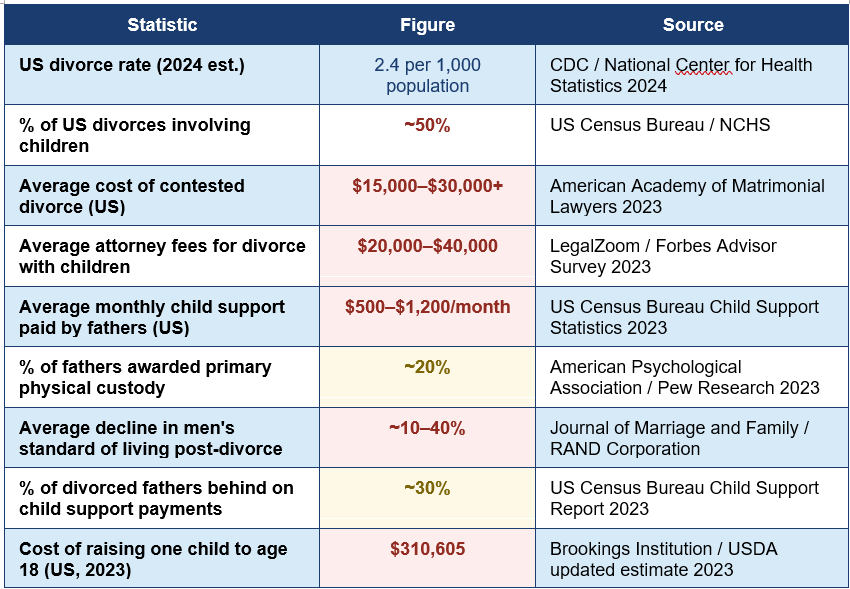

Cost of raising one child to 18: $310,605 — the USDA/Brookings updated 2023 estimate for a middle-income family — a figure that will be divided, shared, and contested during divorce proceedings

Average contested divorce cost: $15,000–$30,000+ — rising to $40,000–$80,000 when high-conflict custody battles and complex asset division are involved (AAML 2023)

Family law attorneys in the United States typically charge between $200 and $500 per hour, with rates reaching $700 to $1,000 or more in major metropolitan areas. A straightforward uncontested divorce may cost $2,000 to $5,000 in legal fees. A contested divorce involving custody disputes, support disagreements, and asset division routinely costs $15,000 to $30,000 per party — and high-conflict cases with forensic accountants, expert witnesses, and extended litigation can reach $100,000 or more per side.

The presence of children significantly increases divorce costs. Custody and parenting time disputes are among the most time-intensive and emotionally charged elements of divorce proceedings, and they are almost always the last to be resolved. Every contested hearing, guardian ad litem appointment, custody evaluation, and mediation session adds to the legal bill. A father committed to maximising his involvement in his children's lives — which is both his right and increasingly supported by research on child wellbeing — must be prepared for the legal investment that commitment may require.

Strategic legal approach: The single most cost-effective decision a divorcing father can make is investing in a skilled family law attorney from the outset rather than attempting to minimise legal costs in the early stages. Early errors in negotiation, documentation, or court filings frequently cost far more to correct than competent initial representation would have cost. Choose experience over price.

Under either model, additional expenses — health insurance, child care, extraordinary medical costs, and extracurricular activities — are typically added to the base support obligation and shared proportionally. Fathers who have children in private schools, who participate in multiple expensive activities, or who have significant health care needs may find their effective child support obligation substantially higher than the base formula calculation.

Child support duration: Until age 18–21 — depending on state law; some states extend support through college, and agreements can include provisions for post-secondary education costs — potentially extending financial obligations well beyond majority

Unlike child support, which follows state formula guidelines, spousal support is highly discretionary and varies enormously based on the judge, the jurisdiction, and the specific facts of the marriage. The Tax Cuts and Jobs Act of 2017 changed the tax treatment of alimony for divorces finalised after December 31, 2018: alimony payments are no longer deductible by the paying spouse and are no longer treated as taxable income by the receiving spouse. This change significantly increased the effective cost of alimony for higher-earning divorcing men, as the pre-2018 deduction had substantially offset the financial burden.

Combined obligations warning: A father paying both child support and alimony simultaneously may find that 40–60% of his net income is committed to these court-ordered obligations before he covers his own housing, food, or transportation. This financial reality requires urgent budgeting, legal strategy, and if applicable, career income maximisation from the moment divorce proceedings begin.

The distinction matters enormously in practice. In a community property state, a man who earned significantly more than his spouse during a long marriage will typically see his assets divided in half regardless of earning contribution. In an equitable distribution state, arguments can be made for a larger share based on greater financial contribution — but outcomes remain unpredictable and highly dependent on the specific judge and jurisdiction.

Retirement impact: Up to 50% of 401(k) balance — marital contributions to retirement accounts are divisible — a man with $300,000 in a 401(k) accumulated during the marriage may exit with $150,000 or less, significantly altering his retirement timeline

The cumulative monthly cost increase of $3,200 to $7,500 represents the most immediate financial shock of divorce for most fathers. For a man earning $80,000 per year — approximately $5,300 take-home per month after federal taxes — even the lower end of this range eliminates most financial discretionary space. This reality is why financial planning from the earliest possible stage of divorce proceedings is not optional but essential.

But the picture is not without agency. Fathers who engage competent legal representation early, who understand the financial mechanics of child support and asset division before negotiations, who engage financial professionals during rather than after the process, and who build a realistic post-divorce budget before the ink is dry on the settlement agreement consistently emerge in a stronger position than those who approach the process reactively.

The most important obligation a divorcing father carries is to his children — financially, emotionally, and in terms of time and presence. Meeting that obligation responsibly requires that he remain financially stable, informed, and proactive. This guide is intended to provide the knowledge base from which that stability can be built — because children's wellbeing is always best served when both parents are financially secure, clearly informed, and positioned to provide.

The following authoritative sources were used in researching this article and are recommended for further guidance:

1. US Census Bureau — Child Support Statistics and Custodial Parents Report 2023

https://www.census.gov/topics/families/child-support.html

2. American Academy of Matrimonial Lawyers (AAML) — Divorce Cost and Trends Survey

https://www.aaml.org/

3. Brookings Institution — Updated Cost of Raising a Child in the United States

https://www.brookings.edu/articles/cost-of-raising-a-child/

4. IRS — Alimony, Divorce, Separation, and Taxes (Post-TCJA)

https://www.irs.gov/taxtopics/tc452

5. US Department of Health and Human Services — Child Support Enforcement Data

https://www.acf.hhs.gov/css

6. Investopedia — Qualified Domestic Relations Order (QDRO) Explained

https://www.investopedia.com/terms/q/qdro.asp

7. American Bar Association — Family Law Section Resources

https://www.americanbar.org/groups/family_law/

8. Institute for Divorce Financial Analysts — CDFA Resources

https://www.institutedfa.com/

- Key Divorce Statistics for American Fathers

- The Legal and Procedural Cost: Where the Money Goes First

- Child Support: Obligations, Calculations, and Long-Term Impact

- How Child Support Is Calculated

- Modification and Enforcement

- Spousal Support and Alimony: What Fathers Need to Know

- Asset Division: Marital Property, the Family Home, and Retirement Accounts

- Equitable Distribution vs Community Property

- The Family Home

- Retirement Accounts

- The Monthly Budget Reality: A Post-Divorce Financial Picture

- Rebuilding Financially After Divorce: A Practical Roadmap

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Divorce is one of the most financially disruptive events that can occur in a person's life — and for a man with children in the United States, its financial consequences are particularly complex, wide-ranging, and long-lasting. Beyond the emotional weight of family separation, a divorcing father faces a simultaneous restructuring of nearly every dimension of his financial life: housing costs, legal fees, child support obligations, potential spousal support, asset division, retirement account impacts, tax filing status changes, and the need to rebuild a single-income household from whatever resources remain after the settlement.

Yet despite the profound financial significance of divorce for fathers, many men enter the process with limited understanding of what to expect. The conversation around divorce and finances is often framed in general terms, leaving men without the specific, data-grounded picture they need to plan effectively, negotiate fairly, and protect their long-term financial health — while continuing to meet their obligations to their children, which remain a genuine and non-negotiable priority.

This guide provides that picture. Drawing on current data from the US Census Bureau, the American Academy of Matrimonial Lawyers, the Brookings Institution, and family law research, it presents the financial reality of divorce for American fathers with children across every major cost dimension — from legal fees and child support to asset division, retirement impacts, and the path to financial rebuilding. The aim is not to discourage but to prepare: informed fathers navigate this process better, protect more, and rebuild faster.

Key Divorce Statistics for American Fathers

The data surrounding divorce and its financial impact on men with children provides essential context before examining each cost component in depth:Cost of raising one child to 18: $310,605 — the USDA/Brookings updated 2023 estimate for a middle-income family — a figure that will be divided, shared, and contested during divorce proceedings

Average contested divorce cost: $15,000–$30,000+ — rising to $40,000–$80,000 when high-conflict custody battles and complex asset division are involved (AAML 2023)

The Legal and Procedural Cost: Where the Money Goes First

The first major financial shock of divorce is the legal cost — and it typically arrives before any settlement is reached, any child support order is issued, or any asset is divided. Attorney fees represent the most immediate and uncontrollable expense in the divorce process for most men.Family law attorneys in the United States typically charge between $200 and $500 per hour, with rates reaching $700 to $1,000 or more in major metropolitan areas. A straightforward uncontested divorce may cost $2,000 to $5,000 in legal fees. A contested divorce involving custody disputes, support disagreements, and asset division routinely costs $15,000 to $30,000 per party — and high-conflict cases with forensic accountants, expert witnesses, and extended litigation can reach $100,000 or more per side.

The presence of children significantly increases divorce costs. Custody and parenting time disputes are among the most time-intensive and emotionally charged elements of divorce proceedings, and they are almost always the last to be resolved. Every contested hearing, guardian ad litem appointment, custody evaluation, and mediation session adds to the legal bill. A father committed to maximising his involvement in his children's lives — which is both his right and increasingly supported by research on child wellbeing — must be prepared for the legal investment that commitment may require.

Strategic legal approach: The single most cost-effective decision a divorcing father can make is investing in a skilled family law attorney from the outset rather than attempting to minimise legal costs in the early stages. Early errors in negotiation, documentation, or court filings frequently cost far more to correct than competent initial representation would have cost. Choose experience over price.

Child Support: Obligations, Calculations, and Long-Term Impact

Child support is the most significant ongoing financial obligation most divorcing fathers will face, and it is both legally mandatory and not subject to discharge in bankruptcy. Understanding how it is calculated, how long it lasts, and what it covers is essential for financial planning.How Child Support Is Calculated

Every US state uses a child support formula, but two main models predominate. The Income Shares Model — used in approximately 40 states — calculates child support based on both parents' combined income and the estimated cost of raising children at that income level. The Percentage of Income Model — used in states including Texas, Mississippi, and Wisconsin — bases support entirely on the non-custodial parent's income as a fixed percentage: typically 20% for one child, 25% for two, and so on.Under either model, additional expenses — health insurance, child care, extraordinary medical costs, and extracurricular activities — are typically added to the base support obligation and shared proportionally. Fathers who have children in private schools, who participate in multiple expensive activities, or who have significant health care needs may find their effective child support obligation substantially higher than the base formula calculation.

Child support duration: Until age 18–21 — depending on state law; some states extend support through college, and agreements can include provisions for post-secondary education costs — potentially extending financial obligations well beyond majority

Modification and Enforcement

Child support orders are modifiable when there is a substantial change in circumstances — a significant change in either parent's income, a change in custody arrangement, or a change in the child's needs. Fathers who experience job loss, disability, or a major income reduction should petition for modification promptly, as support arrears — unpaid back support — accrue from the date of the change event, not from the date a modification is requested. Allowing arrears to accumulate carries severe consequences: wage garnishment, license suspension (including driver's and professional licenses), passport denial, and in extreme cases, incarceration.Spousal Support and Alimony: What Fathers Need to Know

Alimony — or spousal support — is not automatic in every divorce, and its prevalence has declined as dual-income households have become more common. However, in marriages where a significant income disparity existed, where one spouse reduced their career to care for children, or where the marriage was of long duration, spousal support remains a real possibility and must be factored into post-divorce financial planning.Unlike child support, which follows state formula guidelines, spousal support is highly discretionary and varies enormously based on the judge, the jurisdiction, and the specific facts of the marriage. The Tax Cuts and Jobs Act of 2017 changed the tax treatment of alimony for divorces finalised after December 31, 2018: alimony payments are no longer deductible by the paying spouse and are no longer treated as taxable income by the receiving spouse. This change significantly increased the effective cost of alimony for higher-earning divorcing men, as the pre-2018 deduction had substantially offset the financial burden.

Combined obligations warning: A father paying both child support and alimony simultaneously may find that 40–60% of his net income is committed to these court-ordered obligations before he covers his own housing, food, or transportation. This financial reality requires urgent budgeting, legal strategy, and if applicable, career income maximisation from the moment divorce proceedings begin.

Asset Division: Marital Property, the Family Home, and Retirement Accounts

The division of marital assets is the one-time financial event of divorce that can most profoundly reshape a man's long-term wealth trajectory. Understanding the framework in advance is critical to negotiating effectively.Equitable Distribution vs Community Property

The vast majority of US states — 41 of them — operate under equitable distribution, meaning marital assets are divided fairly but not necessarily equally. The court weighs factors including each spouse's income, earning capacity, length of marriage, contributions to the household (including non-financial contributions such as homemaking), and the needs of any dependent children. Nine states — including California, Texas, Arizona, Nevada, and Washington — are community property states, where assets and debts acquired during marriage are generally divided 50/50.The distinction matters enormously in practice. In a community property state, a man who earned significantly more than his spouse during a long marriage will typically see his assets divided in half regardless of earning contribution. In an equitable distribution state, arguments can be made for a larger share based on greater financial contribution — but outcomes remain unpredictable and highly dependent on the specific judge and jurisdiction.

The Family Home

The family home is typically the largest single marital asset and the most emotionally charged. Three common outcomes occur: the home is sold and proceeds split; one spouse buys out the other's equity and retains the home; or the custodial parent remains in the home temporarily until the children reach a certain age, at which point it is sold. For a father who wishes to maintain stability for his children by keeping them in the family home, the buyout option may require refinancing the mortgage into a single name — which requires meeting income-only qualification standards that may be difficult immediately post-divorce.Retirement Accounts

Retirement accounts accumulated during the marriage are marital property in most states and subject to division. A Qualified Domestic Relations Order (QDRO) is the legal instrument required to divide 401(k) plans and pension accounts without triggering immediate tax liability or early withdrawal penalties. IRAs are divided through a different process — a transfer incident to divorce — that also avoids immediate taxation when executed correctly. Improperly executed retirement account division generates significant tax consequences and penalties that permanently reduce the asset's value. Any divorce involving substantial retirement assets requires a CPA or financial planner experienced in divorce financial planning.Retirement impact: Up to 50% of 401(k) balance — marital contributions to retirement accounts are divisible — a man with $300,000 in a 401(k) accumulated during the marriage may exit with $150,000 or less, significantly altering his retirement timeline

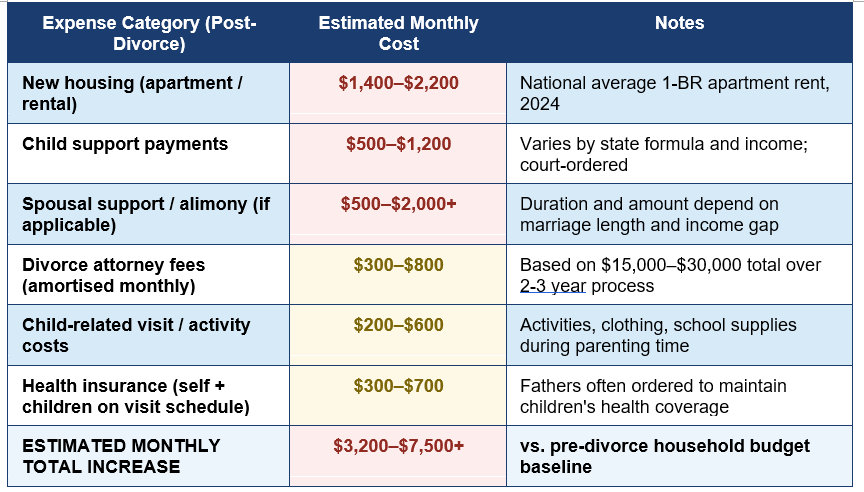

The Monthly Budget Reality: A Post-Divorce Financial Picture

The following table illustrates the estimated monthly cost increase a father typically faces in the immediate post-divorce period, based on national average data. These figures will vary by state, income level, number of children, and specific court orders:The cumulative monthly cost increase of $3,200 to $7,500 represents the most immediate financial shock of divorce for most fathers. For a man earning $80,000 per year — approximately $5,300 take-home per month after federal taxes — even the lower end of this range eliminates most financial discretionary space. This reality is why financial planning from the earliest possible stage of divorce proceedings is not optional but essential.

Rebuilding Financially After Divorce: A Practical Roadmap

The financial aftermath of divorce is genuinely difficult — but it is also navigable with a clear strategy and disciplined execution. The following framework reflects the priorities most commonly recommended by certified divorce financial analysts (CDFAs) and family financial planners:- Establish a new, honest budget immediately: The single most important post-divorce financial act is building a zero-based budget that reflects your new reality — new housing cost, child support obligation, legal fee amortisation, and all other changes. Do not try to maintain a pre-divorce lifestyle on a post-divorce income. Identify exactly what you have and what each dollar must do.

- Rebuild your emergency fund as the first savings priority: Before resuming retirement contributions at their previous level, rebuild an emergency fund of three to six months of your new essential expenses. As a divorced father with court-ordered financial obligations, you are particularly vulnerable to financial shock — any gap in income has immediate legal consequences if it affects your ability to meet child support.

- Engage a Certified Divorce Financial Analyst (CDFA): A CDFA is specifically trained to model the long-term financial implications of different divorce settlement scenarios — tax treatment, liquidity, retirement timing, cash flow. Engaging one during, rather than after, the divorce process often produces materially better settlement outcomes and long-term financial results.

- Petition immediately for child support modification if income changes: If your income decreases — through redundancy, illness, or business disruption — file a modification petition immediately. Courts cannot retroactively reduce child support arrears, so delay is always costly.

- Rebuild retirement savings as quickly as circumstances allow: The loss of marital retirement assets combined with the transition to a single-income household creates a significant retirement gap. Maximise 401(k) contributions — including catch-up contributions if you are over 50 — as soon as your cash flow stabilises, and model your revised retirement timeline with a financial planner.

- Protect your credit independently: Establish credit in your own name only, monitor your credit report for any joint debts that are the responsibility of your ex-spouse, and dispute any unauthorized use. Divorce decrees do not change your legal liability with creditors for joint accounts — only lenders do.

Conclusion

The financial reality of divorce for a man with children in the United States is challenging, layered, and long-lasting. Legal fees, child support, potential spousal support, asset division, retirement account splitting, and the transition to single-household living combine to create a financial restructuring of a magnitude few other life events can match. The statistics confirm that most divorcing fathers experience a significant reduction in their standard of living — and that without deliberate planning, this reduction can persist for years.But the picture is not without agency. Fathers who engage competent legal representation early, who understand the financial mechanics of child support and asset division before negotiations, who engage financial professionals during rather than after the process, and who build a realistic post-divorce budget before the ink is dry on the settlement agreement consistently emerge in a stronger position than those who approach the process reactively.

The most important obligation a divorcing father carries is to his children — financially, emotionally, and in terms of time and presence. Meeting that obligation responsibly requires that he remain financially stable, informed, and proactive. This guide is intended to provide the knowledge base from which that stability can be built — because children's wellbeing is always best served when both parents are financially secure, clearly informed, and positioned to provide.

Frequently Asked Questions (FAQ)

Can a father get primary custody of his children in the United States?

Yes. While historically courts showed a preference for maternal custody, modern US family law operates on the presumption that children benefit from substantial involvement of both parents. Joint physical custody has increased significantly in prevalence over the past two decades, and many states now begin proceedings from an equal parenting time presumption. A father who is actively involved, maintains stable housing, demonstrates a strong parenting relationship, and is represented by competent counsel has a genuine and legally supported path to shared or primary custody. Approximately 20% of fathers currently receive primary physical custody.How is child support calculated if both parents share custody equally?

In most states, even a 50/50 custody arrangement does not eliminate child support — it reduces it, because each parent now bears direct costs during their parenting time. The child support calculation in shared custody situations typically applies the state's formula to both parents' incomes and adjusts for the time each parent spends with the children. The higher-earning parent generally still pays support to the lower-earning parent to equalise the children's standard of living across both households. The specific calculation methodology varies by state.Can child support be modified after the divorce is finalised?

Yes — child support can be modified when there is a substantial change in circumstances. Common qualifying events include a significant increase or decrease in either parent's income (typically 15-20% or more, depending on the state), a change in the custody arrangement, a change in the child's needs, or a change in either parent's financial obligations. Modifications must be requested formally through the court — informal agreements between parents about changing the support amount are not legally enforceable and do not protect against arrears claims.What is a QDRO and why is it important?

A Qualified Domestic Relations Order (QDRO) is a court order that directs a retirement plan administrator to pay a portion of a participant's retirement account to an alternate payee — typically a former spouse — as part of a divorce settlement. Without a properly drafted and approved QDRO, any attempt to transfer or divide a 401(k) or pension triggers immediate income tax and — if the account holder is under 59.5 — a 10% early withdrawal penalty. QDROs must be drafted carefully to comply with the specific requirements of the retirement plan and the relevant federal and state laws. Always use an attorney or specialist experienced in QDRO drafting for any retirement account division.Does paying alimony affect child support?

The interaction between alimony and child support varies by state and by how they are calculated. In some states, alimony payments can reduce the paying spouse's income for the purposes of child support calculation — potentially reducing the child support obligation. In others, the two obligations are calculated independently. The combined obligation of both alimony and child support can represent 40-60% of a man's net income in high-disparity marriages, making legal strategy around the negotiation of both obligations — and their respective tax treatment — a critical component of divorce financial planning. This is one area where a Certified Divorce Financial Analyst adds exceptional value.

External References

The following authoritative sources were used in researching this article and are recommended for further guidance:1. US Census Bureau — Child Support Statistics and Custodial Parents Report 2023

https://www.census.gov/topics/families/child-support.html

2. American Academy of Matrimonial Lawyers (AAML) — Divorce Cost and Trends Survey

https://www.aaml.org/

3. Brookings Institution — Updated Cost of Raising a Child in the United States

https://www.brookings.edu/articles/cost-of-raising-a-child/

4. IRS — Alimony, Divorce, Separation, and Taxes (Post-TCJA)

https://www.irs.gov/taxtopics/tc452

5. US Department of Health and Human Services — Child Support Enforcement Data

https://www.acf.hhs.gov/css

6. Investopedia — Qualified Domestic Relations Order (QDRO) Explained

https://www.investopedia.com/terms/q/qdro.asp

7. American Bar Association — Family Law Section Resources

https://www.americanbar.org/groups/family_law/

8. Institute for Divorce Financial Analysts — CDFA Resources

https://www.institutedfa.com/

0 Comments Comments