Investing

How to Build $5,000 Per Month in Dividend Income

Table of Contents

- The Real Math: How Much Capital Do You Actually Need?

- The Best Dividend Asset Classes in 2026

- Dividend Growth ETFs: The Reliable Foundation

- REITs and REIT ETFs: The Income Engine

- Covered Call ETFs: Monthly Income at a Price

- High-Yield Bonds and Preferred Stocks: Fixed-Income Supplement

- The Tax Reality: What $5,000/Month Actually Costs You After Tax

- A Step-by-Step Approach to Building a $5,000/Month Dividend Portfolio

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

The idea of earning $5,000 a month in dividend income — a reliable, recurring payment arriving whether you work that month or not — is one of the most searched and most marketed concepts in personal finance. The promise is real. The path to it is achievable, but it is considerably more capital-intensive than most content on this topic suggests, and it involves genuine, unavoidable trade-offs between yield, risk, and the reliability of the income stream.

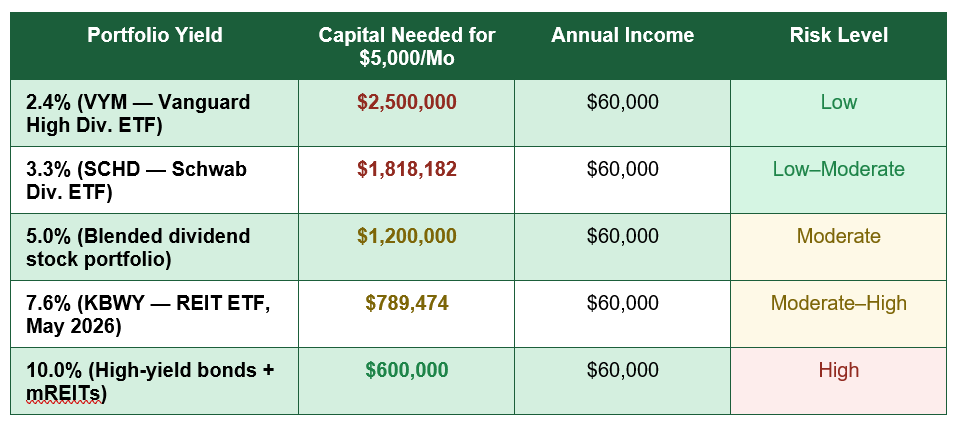

The honest starting point is arithmetic: $5,000 per month is $60,000 per year. To generate $60,000 annually from dividend income alone, the amount of capital you need depends entirely on the yield your portfolio generates. At a conservative, low-risk 3% yield, you need $2,000,000 invested. At a moderate, blended yield of 5%, you need $1,200,000. At the higher-yielding end of REITs and income ETFs — 8% or more — you need $750,000 or less, but you accept meaningfully more risk of dividend cuts and principal loss.

This guide provides the honest, complete picture: the capital required at various realistic yield levels, the specific asset classes generating the highest dividend income in 2026, the critical tax considerations most dividend income guides understate, the step-by-step approach to building a portfolio designed for this specific income goal, and — crucially — an honest assessment of what makes this goal faster or slower for different starting situations.

The Real Math: How Much Capital Do You Actually Need?

Before selecting a single investment, the most important calculation to complete is: how much capital, generating what yield, produces $5,000 per month? The formula is straightforward:Required Capital = Annual Income Target ÷ Portfolio Yield

$60,000 ÷ 0.05 (5% yield) = $1,200,000 required.

The table below shows how this plays out at a range of realistic 2026 yield levels, using actual fund yields from current data:

The yield-safety trade-off in one sentence: The faster you want to reach $5,000/month, the higher yield you need — and the higher the yield, the higher the risk of dividends being cut or principal being eroded — there is no asset class offering 10%+ yield with the reliability and safety of a 3% blue-chip dividend stock; the investor must choose how much risk they are willing to accept in exchange for requiring less capital.

Why 'fastest' is a nuanced question: Reaching $5,000/month in dividend income is 'fastest' if you start with the largest lump sum, invest at the highest sustainable yield, reinvest all dividends during the accumulation phase, and avoid tax drag through smart account selection. For someone starting from scratch with $1,000 per month to invest, even a 7% yield portfolio reaching $5,000/month in monthly income requires approximately 22 years of consistent investing and reinvestment. There is no shortcut that removes the requirement for either significant capital or significant time.

The Best Dividend Asset Classes in 2026

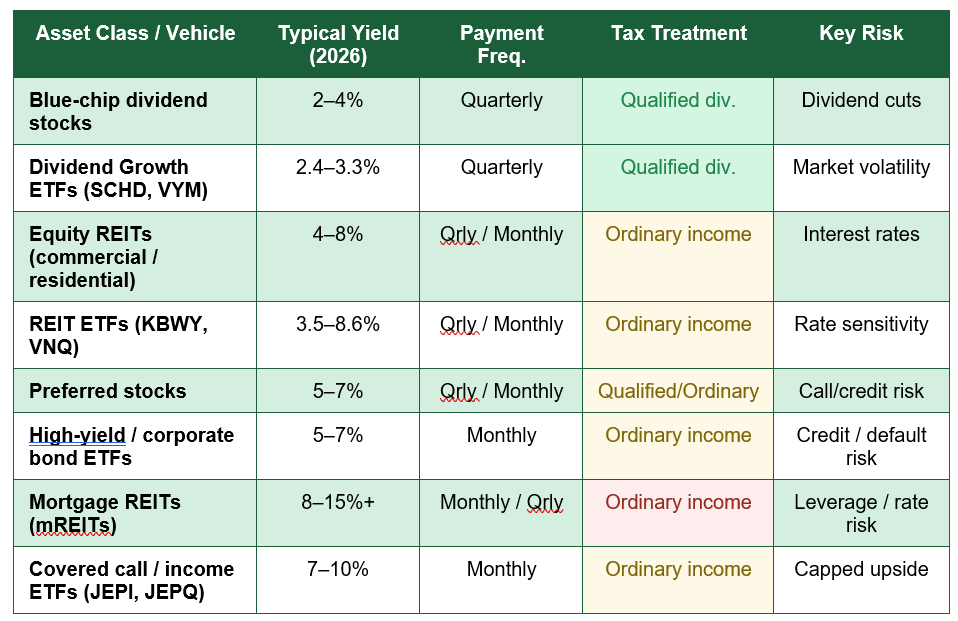

The dividend income landscape in 2026 has shifted meaningfully compared to the near-zero-rate environment of 2020-2021. With the Federal Reserve holding rates at 3.50-3.75% and real yields remaining positive across most fixed-income categories, investors now have genuine income-generating options across a wider range of asset classes than was available just a few years ago. The table below summarises the main categories available:

Dividend Growth ETFs: The Reliable Foundation

Funds like SCHD (Schwab US Dividend Equity ETF, 3.3% SEC yield) and VYM (Vanguard High Dividend Yield ETF, 2.4%) represent the safest, most liquid, and most tax-efficient core of a dividend portfolio. SCHD's underlying benchmark screens for at least ten consecutive years of dividend payments, then ranks companies by free cash flow to debt, return on equity, dividend yield, and five-year dividend growth rate — a disciplined selection process that has historically produced above-average dividend growth alongside a reasonable starting yield.The limitation at the $5,000/month target level is capital intensity: reaching $60,000 per year at SCHD's 3.3% yield requires just over $1.8 million invested. For most investors working toward the goal, these ETFs serve better as a tax-efficient foundation supplemented by higher-yielding instruments.

REITs and REIT ETFs: The Income Engine

Real Estate Investment Trusts are, by legal structure, required to distribute at least 90% of their taxable income to shareholders as dividends, which is why they consistently produce among the highest yields in the equity income space. As of May 2026, KBWY — the Invesco KBW Premium Yield Equity REIT ETF, focused on small- and mid-cap equity REITs — was yielding 7.6-8.6% SEC yield, representing one of the most income-intensive REIT ETF options available. The Vanguard Real Estate ETF (VNQ), the largest REIT ETF by assets, offers a more moderate yield in the 3.5-4% range but with considerably broader diversification and lower volatility.The critical REIT-specific tax consideration: REIT dividends are generally taxed as ordinary income rather than qualifying for the lower qualified dividend tax rate. This makes REITs significantly better suited to tax-advantaged accounts (IRA, 401(k), HSA) than to taxable brokerage accounts, where the ordinary income tax treatment can meaningfully reduce your effective after-tax yield.

Covered Call ETFs: Monthly Income at a Price

One of the fastest-growing categories in the dividend income space over the past three years has been covered call ETFs — funds like JEPI (JPMorgan Equity Premium Income ETF) and JEPQ (JPMorgan Nasdaq Equity Premium Income ETF), which generate enhanced monthly income by selling equity option premiums against their underlying stock portfolios. Yields in this category typically run 7-10%, paid monthly, making them attractive for immediate income.The trade-off is that selling calls caps the fund's upside participation in rising markets: when the S&P 500 or Nasdaq rises strongly, covered call funds participate only partially in those gains, since the options they have sold limit price appreciation beyond the strike price. This makes them excellent income generators in flat or modestly appreciating markets, but they can fall behind a simple index fund in strong bull markets. For income-focused investors who need the $5,000/month now rather than at some future point, this trade-off is often worth accepting.

High-Yield Bonds and Preferred Stocks: Fixed-Income Supplement

High-yield (non-investment-grade) corporate bond ETFs, such as SPHY (SPDR Portfolio High Yield Bond ETF), typically yield 5-7% with monthly distributions, providing a fixed-income supplement to equity-based dividend holdings. Preferred stocks, which sit between common equity and bonds in the capital structure, typically yield 5-7% and can offer either qualified or ordinary income depending on the issuer and structure.Both categories carry credit risk — the possibility that the issuing company defaults on its debt — that is absent from Treasury bonds and minimal in blue-chip equity dividends. High-yield bond exposure is best limited to 15-25% of a dividend portfolio rather than forming its core, both for credit risk diversification and because the income from these instruments does not grow over time the way equity dividends typically can.

The Tax Reality: What $5,000/Month Actually Costs You After Tax

Dividend income taxation is one of the most frequently glossed-over aspects of dividend income guides, and getting it wrong can cost thousands of dollars annually in unnecessary tax drag. The key distinction to understand is between qualified dividends and ordinary income dividends:- Qualified dividends: Dividends from most US common stocks held for more than 60 days, and many ETF distributions that pass through qualified dividends, are taxed at the lower long-term capital gains rate — 0%, 15%, or 20% depending on your taxable income. For most middle-income investors, this is 15%, making qualified dividends tax-efficient income.

- Ordinary income dividends: REIT dividends, covered call option premiums distributed by covered call ETFs, high-yield bond interest, and most mortgage REIT distributions are taxed as ordinary income at your full marginal tax rate. For someone in the 22% or 24% bracket, this is a meaningful difference from the 15% qualified rate.

- REIT QBI deduction: Individual REIT investors (not those holding through ETFs) can sometimes claim a 20% Qualified Business Income (QBI) deduction on REIT dividends under Section 199A, reducing the effective tax rate on that income. This deduction does not pass through REIT ETFs in most cases, making direct REIT ownership potentially more tax-efficient than ETF-based REIT exposure for investors in higher brackets.

The practical implication: a portfolio generating $60,000 annually in qualified dividends taxed at 15% leaves you with $51,000 net. The same portfolio generating $60,000 in REIT ordinary income taxed at 24% leaves you with $45,600 net — a $5,400 annual after-tax difference simply from the income source. Maximising tax-advantaged account allocations for the highest-ordinary-income instruments (REITs, high-yield bonds) while holding qualified dividend payers in taxable accounts is the most consistent advice given by tax-efficient income planning specialists.

A Step-by-Step Approach to Building a $5,000/Month Dividend Portfolio

Whether you are starting from a significant lump sum or building from a monthly savings contribution, the following sequence provides a practical, ordered framework:- Define your target portfolio yield and accept the corresponding risk level: Use the capital table above to identify what yield you need based on the capital you currently have or realistically expect to accumulate. Be honest with yourself about risk tolerance — a yield-chasing strategy that leads you to cut dividends mid-retirement is far worse than a lower-yielding, more stable starting point.

- Maximise contributions to tax-advantaged accounts first: Every dollar of REIT or high-yield bond income sheltered inside an IRA or 401(k) is a dollar taxed at your ordinary income rate that instead compounds tax-free or tax-deferred. Max your 401(k), IRA, and if applicable HSA contributions before deploying capital in a taxable brokerage account.

- Build a diversified core using low-cost ETFs: For most investors, a combination of SCHD (dividend growth, qualified dividends) and a REIT ETF (VNQ, KBWY depending on yield preference) provides the core income foundation with genuine diversification. Adding a covered call ETF component (JEPI/JEPQ) for monthly income and potentially a preferred stock ETF provides additional yield layers.

- Reinvest all dividends until the income target is reached: Dividend reinvestment (DRIP) during the accumulation phase accelerates compounding significantly. The portfolio growing from $500,000 toward $1,000,000 generates dramatically more from reinvested dividends than from new capital alone over a 10-year period at a 5%+ yield.

- Review yield sustainability, not just headline yield: A 12% yield from a mortgage REIT may be a trap if the fund's dividend has been cut three times in five years. Review the payout ratio, dividend history, and analyst coverage before weighting any single income source heavily. A stable 5% that grows is worth more over ten years than a volatile 10% that eventually gets cut.

- Phase from accumulation to distribution mode deliberately: The transition from reinvesting dividends to living on them requires explicit portfolio rebalancing — often shifting from higher-growth/lower-yield toward higher-yield/more-stable positions as the income target approaches. This is the stage at which a conversation with a qualified financial adviser and a tax professional is most valuable.

Conclusion

There is no magic fund or strategy that generates $5,000 per month in dividends without requiring either substantial capital or meaningful risk. At the most reliable yield levels available from high-quality dividend payers in 2026 — roughly 3-5% — reaching $60,000 annually requires $1.2 million to $2 million in invested assets. At higher-yield instruments like REITs and covered call ETFs (7-10%), the capital requirement falls to $600,000-$850,000, but the income stream is less stable, more tax-inefficient, and more vulnerable to rate changes and market stress.The 'fastest' path is not a single answer — it depends on your starting capital, your risk tolerance, your tax situation, and your timeline. Someone with $800,000 to invest today can reach $5,000/month faster by allocating toward higher-yield instruments and accepting the corresponding risk. Someone with $20,000 and $1,500 per month to save needs a long-horizon accumulation strategy with disciplined reinvestment, likely spanning 15-20 years at realistically achievable yield levels.

What the data consistently supports is that the foundational strategy — a diversified mix of dividend growth equities for qualified income, REITs in tax-advantaged accounts for the higher yield, and covered call or preferred stock ETFs to boost the yield curve — provides the most reliable path to a sustainable $5,000/month income stream. The honest version of this goal is a wealth-building project measured in years, not months. The reward at the end of that project — income that arrives monthly without requiring your daily labour — is genuinely worth the patience and discipline the journey demands.

Frequently Asked Questions (FAQ)

How much money do I need to invest to get $5,000 a month in dividends?

The amount depends on your portfolio's average dividend yield. At 3%, you need approximately $2,000,000. At 5%, approximately $1,200,000. At 8% (higher-yield instruments like certain REIT ETFs), approximately $750,000. At 10% (high-yield bonds, mortgage REITs), approximately $600,000. Higher yields require less capital but carry meaningfully more risk of dividend cuts, principal erosion, and tax inefficiency. The realistic 'sweet spot' for most income investors is a blended yield of 4-6%, requiring $1,000,000 to $1,500,000 in invested capital.Which dividend ETFs pay monthly?

Several well-regarded ETFs pay dividends monthly rather than quarterly, which is useful for income investors matching cash flow to monthly expenses. These include JEPI and JEPQ (JPMorgan covered call ETFs, 7-10% yield), DHS (WisdomTree US Dividend Index ETF, 3.6% yield), SPHY (SPDR High Yield Bond ETF), KBWY (Invesco REIT ETF, 7.6-8.6% yield as of May 2026), and various preferred stock ETFs. Many individual REITs also pay monthly dividends, including Realty Income (O), known as 'The Monthly Dividend Company'.Are REIT dividends taxed differently from stock dividends?

Yes, and this is one of the most important tax distinctions in dividend income planning. Most REIT dividends do not qualify for the lower qualified dividend tax rate and are instead taxed as ordinary income at your full marginal rate. This makes REITs significantly more tax-efficient when held inside a traditional or Roth IRA, where the ordinary income tax treatment is either deferred or eliminated entirely. In a taxable brokerage account, the after-tax return from a 7% REIT dividend taxed at 24% is equivalent to approximately 5.3% net — the tax drag matters significantly at high yields.What is a covered call ETF and why does it pay such a high monthly yield?

Covered call ETFs, like JEPI and JEPQ, generate high monthly income by holding a portfolio of stocks (or stock index exposure) and simultaneously selling equity call options against those holdings. When you sell a call option, you receive an immediate premium payment — this is the source of the high income distribution. In exchange, you agree to cap your participation in any price increases above the option's strike price. The result is a lower-volatility, high-income portfolio that does not fully participate in strong bull market rallies but provides more stable income than a pure equity portfolio. The income generated is typically taxed as ordinary income, since option premiums are not qualified dividends.Should I work with a financial adviser to build this kind of portfolio?

For portfolios above $250,000 or for investors approaching or in retirement, working with a fee-only financial adviser (one who charges a flat or hourly fee rather than commissions) is strongly advisable, particularly for the tax-planning aspects of a high-income dividend portfolio. The coordination between account types (taxable vs IRA vs Roth), the choice between individual securities and ETFs, the REIT QBI deduction calculation, and the transition from accumulation to distribution mode all involve significant tax complexity where professional guidance consistently produces better after-tax outcomes than self-directed trial and error.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. Morningstar — Top High-Dividend ETFs for Passive Income in 2026

https://www.morningstar.com/funds/top-high-dividend-etfs-passive-income-2026

2. US News & World Report — Best High-Dividend ETFs to Buy in 2026

https://money.usnews.com/investing/articles/best-high-dividend-etfs

3. US News & World Report — Best REIT ETFs to Buy in 2026

https://money.usnews.com/investing/articles/best-reit-etfs-to-buy-now

4. The Motley Fool — 20 Best High-Yield Dividend Stocks for 2026

https://www.fool.com/investing/stock-market/types-of-stocks/dividend-stocks/high-yield-dividend-stocks/

5. JPMorgan Asset Management — JEPI: JPMorgan Equity Premium Income ETF

https://am.jpmorgan.com/us/en/asset-management/adv/products/jpmorgan-equity-premium-income-etf-native-etf/

6. Vanguard — VYM: Vanguard High Dividend Yield ETF Overview

https://investor.vanguard.com/investment-products/etfs/profile/vym

7. Schwab — SCHD: Schwab US Dividend Equity ETF

https://www.schwab.com/etfs/schwab-us-dividend-equity-etf

8. IRS — Tax Treatment of Dividends and Capital Gains

https://www.irs.gov/taxtopics/tc404

0 Comments Comments