Investing

How to Make Money as a Hedge Fund Investor

Table of Contents

Hedge funds occupy a unique and often mythologised position in the public imagination — exclusive, secretive, and associated with extraordinary wealth. Names like Ray Dalio, Ken Griffin, and Renaissance Technologies have become symbols of financial sophistication and outsized returns. But the reality of making money as a hedge fund investor is considerably more nuanced, more accessible in some ways and more restricted in others, than popular perception suggests.

The global hedge fund industry now manages over $4.3 trillion in assets across approximately 8,300 active funds. Yet most retail investors have never directly invested in one — and many who could legally do so would find that the typical hedge fund's performance, after fees, does not necessarily justify the access barriers, illiquidity, and complexity involved. Understanding this reality, rather than the popular mythology, is the foundation of making genuinely informed decisions about whether and how to pursue hedge fund exposure.

This guide explains exactly how money is made — and lost — in the hedge fund world, from both the investor's and the manager's perspective. It covers the various legitimate access routes available depending on your investor status and capital, the fee structures that shape net returns, the actual comparative performance data against simpler alternatives like index funds, the path to becoming a hedge fund professional rather than just an investor, and the risks that any serious analysis must address honestly. By the end, you will have a clear, realistic framework for evaluating whether hedge fund exposure belongs in your financial strategy.

Hedge funds differ from mutual funds and ETFs in several legally and structurally significant ways. They are typically structured as limited partnerships, with the fund manager acting as the general partner and investors as limited partners. They are exempt from many of the regulatory requirements that govern mutual funds — including daily liquidity requirements and leverage restrictions — in exchange for restricting access to accredited or qualified investors who are presumed to have the financial sophistication to understand and bear the additional risk.

This regulatory exemption, granted under the Investment Company Act of 1940 and reinforced by SEC accredited investor rules, is precisely why most retail investors cannot directly invest in traditional hedge funds — and why understanding the alternative access routes discussed later in this guide is essential for anyone without qualifying wealth or income.

Hedge fund attrition rate: 50–60% close within 5 years — the majority of hedge funds launched do not survive a full market cycle, reflecting the extreme competitiveness and performance pressure within the industry (HFR data)

The performance reality check: Over the past decade, the average hedge fund has underperformed the S&P 500 by 4-5 percentage points annually after fees. This does not mean hedge funds are without value — many provide genuine diversification, downside protection, and access to strategies unavailable elsewhere — but it does mean 'hedge fund returns' should not be assumed to automatically outperform a simple low-cost index fund strategy.

Critically, hedge fund managers themselves make money primarily through fees — not exclusively through investment performance. This fee-driven income stream is one of the most significant and frequently overlooked aspects of how 'hedge fund money' actually gets made, and it shapes the entire incentive structure of the industry.

The mathematical impact of this fee structure on investor returns is substantial. Consider a hedge fund that generates a 12% gross return in a given year. After a 2% management fee (reducing the base to 10%) and a 20% performance fee on that 10% gain (a further 2% reduction), the investor's net return falls to approximately 8% — a full third of the gross return consumed by fees. Compounded over a 20 or 30-year investment horizon, this fee drag can reduce total accumulated wealth by 30% or more compared to a fee-free benchmark generating the same gross returns.

Fee drag over 30 years: 30%+ reduction in final wealth — a hedge fund charging 2-and-20 against a fee-free index fund generating identical gross returns can produce 30% or more less accumulated wealth over a 30-year horizon — a critical consideration often overlooked by prospective investors

This is precisely why due diligence on net-of-fee performance — not headline gross returns — is the single most important analytical step for any prospective hedge fund investor. A fund advertising a 'consistent 15% return' that charges 2-and-20 may deliver a genuinely competitive 11-12% net return — or it may be using selective reporting periods or survivorship-biased benchmarks to present a misleadingly favourable picture.

Due diligence imperative: Before any direct hedge fund investment, conduct (or have a qualified advisor conduct) thorough due diligence: verify the fund's audited performance history through an independent administrator, confirm proper custody of assets with a reputable prime broker, review the fund's regulatory filings (Form ADV for SEC-registered advisors), and understand the complete fee structure including any hidden costs. The additional complexity and reduced transparency of hedge funds relative to mutual funds make this due diligence step non-negotiable.

For the much larger population of retail investors who do not meet accredited investor thresholds, publicly traded alternative asset manager stocks, liquid alternative mutual funds, and hedge-fund-style ETFs provide meaningful, accessible exposure to similar strategies and economics without the lock-up periods, high minimums, and reduced transparency of traditional hedge funds. And for those with the relevant skills and ambition, building a career within the hedge fund industry itself remains one of the most financially rewarding professional paths in finance.

Whatever route you pursue, the data is clear on one point: hedge fund exposure should be evaluated on its net-of-fee performance against realistic benchmarks, not on industry mythology or headline gross returns. A well-constructed portfolio of low-cost index funds has outperformed the average hedge fund over the past decade — meaning hedge fund exposure should be pursued for genuine diversification and risk-management benefits, not as an assumed shortcut to outsized wealth. Approached with this realistic framework, hedge fund investing can be a valuable component of a sophisticated financial strategy rather than an expensive disappointment.

The following authoritative sources were used in researching this article and are recommended for further reading:

1. HFR (Hedge Fund Research) — Global Hedge Fund Industry Report 2024

https://www.hfr.com/

2. Preqin — Global Hedge Fund Report 2024

https://www.preqin.com/insights/global-reports/2024-preqin-global-hedge-fund-report

3. US Securities and Exchange Commission — Accredited Investor Definition

https://www.sec.gov/resources-small-businesses/capital-raising-building-blocks/accredited-investor

4. Investopedia — How Hedge Funds Make Money: Fee Structures Explained

https://www.investopedia.com/articles/financial-careers/09/how-hedge-funds-make-money.asp

5. S&P Dow Jones Indices — S&P 500 Historical Returns Data

https://www.spglobal.com/spdji/en/indices/equity/sp-500/

6. SEC — Investment Adviser Public Disclosure (IAPD) Database

https://adviserinfo.sec.gov/

7. Institutional Investor — Hedge Fund Compensation Report 2023

https://www.institutionalinvestor.com/

8. CFA Institute — Understanding Alternative Investments and Hedge Fund Strategies

https://www.cfainstitute.org/research/alternative-investments

- What a Hedge Fund Actually Is — and How It Differs From a Mutual Fund

- The Hedge Fund Industry by the Numbers

- How Hedge Funds Actually Generate Returns

- The 2-and-20 Fee Structure: Why Fees Matter More Than You Think

- Access Routes: How Different Investors Can Gain Hedge Fund Exposure

- Direct Hedge Fund Investment (Accredited/Qualified Investors)

- Funds of Hedge Funds

- Publicly Traded Asset Manager Stock

- Liquid Alternative Mutual Funds and Hedge-Fund-Style ETFs

- Becoming a Hedge Fund Professional

- The Risks: What Every Prospective Hedge Fund Investor Must Understand

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Hedge funds occupy a unique and often mythologised position in the public imagination — exclusive, secretive, and associated with extraordinary wealth. Names like Ray Dalio, Ken Griffin, and Renaissance Technologies have become symbols of financial sophistication and outsized returns. But the reality of making money as a hedge fund investor is considerably more nuanced, more accessible in some ways and more restricted in others, than popular perception suggests.

The global hedge fund industry now manages over $4.3 trillion in assets across approximately 8,300 active funds. Yet most retail investors have never directly invested in one — and many who could legally do so would find that the typical hedge fund's performance, after fees, does not necessarily justify the access barriers, illiquidity, and complexity involved. Understanding this reality, rather than the popular mythology, is the foundation of making genuinely informed decisions about whether and how to pursue hedge fund exposure.

This guide explains exactly how money is made — and lost — in the hedge fund world, from both the investor's and the manager's perspective. It covers the various legitimate access routes available depending on your investor status and capital, the fee structures that shape net returns, the actual comparative performance data against simpler alternatives like index funds, the path to becoming a hedge fund professional rather than just an investor, and the risks that any serious analysis must address honestly. By the end, you will have a clear, realistic framework for evaluating whether hedge fund exposure belongs in your financial strategy.

What a Hedge Fund Actually Is — and How It Differs From a Mutual Fund

A hedge fund is a pooled investment vehicle that uses a wide range of strategies — long and short positions, leverage, derivatives, arbitrage, and concentrated bets — to generate returns that are ideally uncorrelated with broader market movements. The term 'hedge' originally referred to the practice of hedging market risk by holding both long and short positions simultaneously, though modern hedge funds pursue an enormous diversity of strategies that often bear little resemblance to this original conservative concept.Hedge funds differ from mutual funds and ETFs in several legally and structurally significant ways. They are typically structured as limited partnerships, with the fund manager acting as the general partner and investors as limited partners. They are exempt from many of the regulatory requirements that govern mutual funds — including daily liquidity requirements and leverage restrictions — in exchange for restricting access to accredited or qualified investors who are presumed to have the financial sophistication to understand and bear the additional risk.

This regulatory exemption, granted under the Investment Company Act of 1940 and reinforced by SEC accredited investor rules, is precisely why most retail investors cannot directly invest in traditional hedge funds — and why understanding the alternative access routes discussed later in this guide is essential for anyone without qualifying wealth or income.

The Hedge Fund Industry by the Numbers

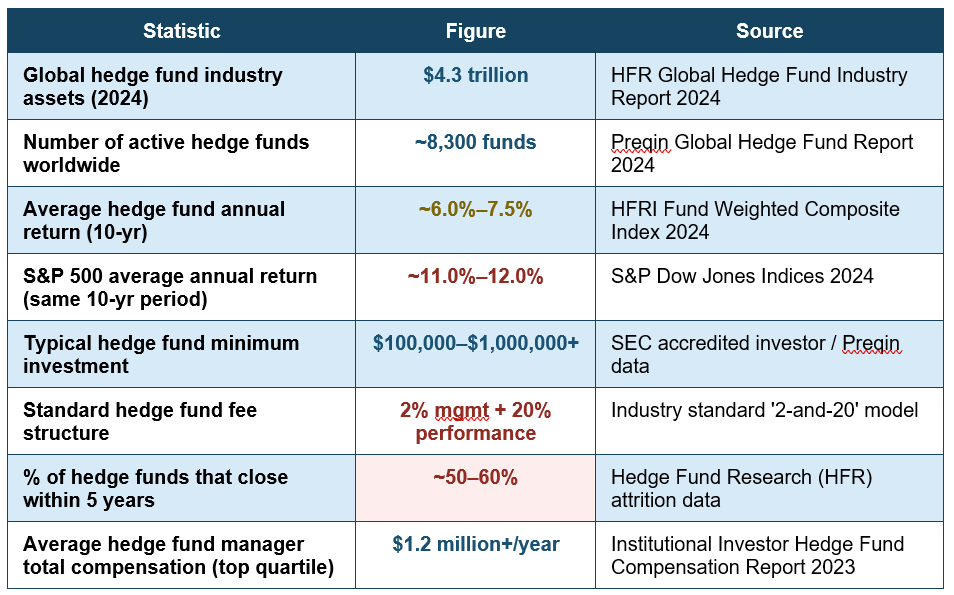

Understanding the scale, performance, and structural realities of the hedge fund industry provides essential context before exploring specific strategies for making money as an investor:Hedge fund attrition rate: 50–60% close within 5 years — the majority of hedge funds launched do not survive a full market cycle, reflecting the extreme competitiveness and performance pressure within the industry (HFR data)

The performance reality check: Over the past decade, the average hedge fund has underperformed the S&P 500 by 4-5 percentage points annually after fees. This does not mean hedge funds are without value — many provide genuine diversification, downside protection, and access to strategies unavailable elsewhere — but it does mean 'hedge fund returns' should not be assumed to automatically outperform a simple low-cost index fund strategy.

How Hedge Funds Actually Generate Returns

Understanding the actual mechanisms hedge funds use to generate profit is essential before evaluating whether — and how — to gain exposure to them. The strategies vary enormously, but the major categories include:- Long/short equity: Taking long positions in stocks expected to rise while simultaneously shorting stocks expected to fall, aiming to profit from the spread regardless of overall market direction.

- Global macro: Making large directional bets on macroeconomic trends — currency movements, interest rate changes, commodity price shifts — based on analysis of global economic and political conditions. Funds like Bridgewater Associates are famous practitioners of this approach.

- Event-driven strategies: Profiting from corporate events such as mergers, acquisitions, bankruptcies, and spin-offs, where pricing inefficiencies often emerge during the uncertainty surrounding the event.

- Quantitative and algorithmic strategies: Using mathematical models, statistical analysis, and increasingly machine learning to identify and exploit pricing patterns at a scale and speed beyond human analysis. Renaissance Technologies' Medallion Fund is the most famous example, reportedly generating average annual returns exceeding 60% before fees over several decades.

- Arbitrage strategies: Exploiting price discrepancies between related securities — convertible bond arbitrage, fixed income arbitrage, merger arbitrage — capturing small but relatively reliable spreads.

- Distressed debt and credit strategies: Purchasing the debt of financially troubled companies at a discount, profiting from restructuring, recovery, or successful bankruptcy resolution.

Critically, hedge fund managers themselves make money primarily through fees — not exclusively through investment performance. This fee-driven income stream is one of the most significant and frequently overlooked aspects of how 'hedge fund money' actually gets made, and it shapes the entire incentive structure of the industry.

The 2-and-20 Fee Structure: Why Fees Matter More Than You Think

The traditional hedge fund fee structure — known as '2-and-20' — charges investors a 2% annual management fee on total assets under management, regardless of performance, plus a 20% performance fee on any profits generated above a specified benchmark or hurdle rate. This structure has been a defining feature of the industry since its modern emergence in the 1980s and 1990s, though competitive pressure has pushed average fees down to closer to 1.4% management and 16-18% performance in recent years.The mathematical impact of this fee structure on investor returns is substantial. Consider a hedge fund that generates a 12% gross return in a given year. After a 2% management fee (reducing the base to 10%) and a 20% performance fee on that 10% gain (a further 2% reduction), the investor's net return falls to approximately 8% — a full third of the gross return consumed by fees. Compounded over a 20 or 30-year investment horizon, this fee drag can reduce total accumulated wealth by 30% or more compared to a fee-free benchmark generating the same gross returns.

Fee drag over 30 years: 30%+ reduction in final wealth — a hedge fund charging 2-and-20 against a fee-free index fund generating identical gross returns can produce 30% or more less accumulated wealth over a 30-year horizon — a critical consideration often overlooked by prospective investors

This is precisely why due diligence on net-of-fee performance — not headline gross returns — is the single most important analytical step for any prospective hedge fund investor. A fund advertising a 'consistent 15% return' that charges 2-and-20 may deliver a genuinely competitive 11-12% net return — or it may be using selective reporting periods or survivorship-biased benchmarks to present a misleadingly favourable picture.

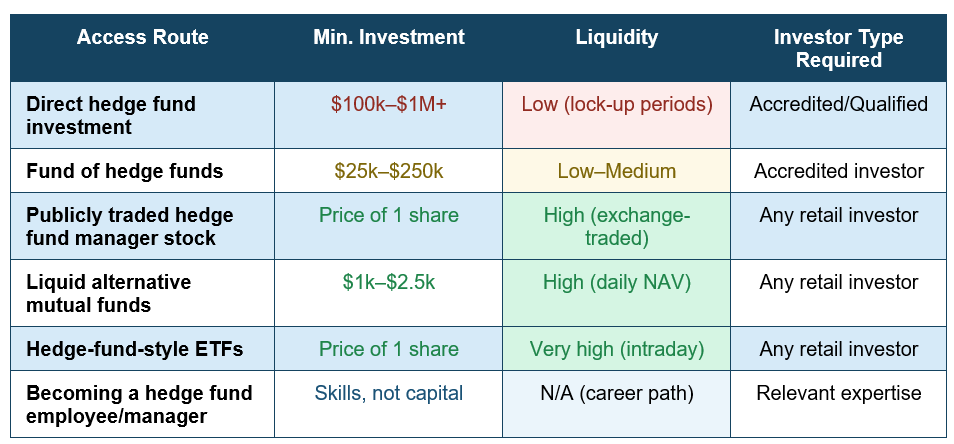

Access Routes: How Different Investors Can Gain Hedge Fund Exposure

The path to making money as a hedge fund investor depends fundamentally on your accredited investor status, available capital, and desired liquidity. The comparison below summarises the main access routes:

Direct Hedge Fund Investment (Accredited/Qualified Investors)

To invest directly in a traditional hedge fund in the United States, you must qualify as an accredited investor under SEC rules: an individual income exceeding $200,000 ($300,000 for joint filers) in each of the prior two years with a reasonable expectation of the same in the current year, or a net worth exceeding $1 million excluding primary residence. Many institutional-quality funds further require 'qualified purchaser' status — $5 million or more in investments. Minimum investments typically range from $100,000 to $1 million or more, with lock-up periods of one to three years restricting withdrawal.Funds of Hedge Funds

A fund of hedge funds pools investor capital and allocates it across multiple underlying hedge funds, providing diversification across strategies and managers with a lower minimum investment — typically $25,000 to $250,000 — than direct investment in any single fund. The trade-off is an additional layer of fees, as the fund of funds charges its own management fee on top of the underlying funds' fees, further compounding the fee drag problem discussed above.Publicly Traded Asset Manager Stock

One of the most accessible ways for retail investors to gain economic exposure to the hedge fund business model — without meeting accredited investor thresholds — is to purchase shares of publicly traded alternative asset managers. Firms including Blackstone (BX), Apollo Global Management (APO), KKR & Co. (KKR), and Ares Management (ARES) are publicly listed, allowing any investor to buy shares through a standard brokerage account. While these firms manage diverse strategies beyond pure hedge funds (private equity, credit, real estate), their stock performance reflects the broader alternative asset management business model, including fee income from hedge-fund-style strategies.Liquid Alternative Mutual Funds and Hedge-Fund-Style ETFs

Liquid alternatives are mutual funds and ETFs that attempt to replicate hedge fund-like strategies — long/short equity, managed futures, market-neutral approaches — while complying with the daily liquidity and transparency requirements of registered investment companies. These products are available to any retail investor with no minimum investment beyond the price of a single share, and offer daily liquidity, in stark contrast to the multi-year lock-up periods of traditional hedge funds. Performance and fees vary enormously across this category, and careful due diligence remains essential.Becoming a Hedge Fund Professional

The most financially lucrative way to 'make money as a hedge fund investor' — for those with the relevant skills, education, and risk tolerance — is to become a hedge fund employee or manager rather than simply an external investor. Top-quartile hedge fund portfolio managers and analysts earn total compensation exceeding $1.2 million annually, with the most successful fund founders earning hundreds of millions or billions of dollars through performance fee carry on their funds' returns. This path requires deep quantitative, financial, or domain-specific expertise, typically built through investment banking, quantitative research, or specialized trading experience before transitioning into hedge fund roles.The Risks: What Every Prospective Hedge Fund Investor Must Understand

A balanced and honest analysis of hedge fund investing requires a clear-eyed assessment of the risks involved — risks that are frequently understated in promotional materials and popular media coverage.- Illiquidity risk: Lock-up periods of one to three years (or longer for certain strategies) mean your capital is inaccessible regardless of personal financial needs or market conditions during that period.

- Survivorship and reporting bias: Hedge fund performance databases systematically overstate average returns because failed funds stop reporting and are often excluded from historical averages, creating an artificially rosy picture of typical performance.

- Leverage risk: Many hedge fund strategies use significant leverage to amplify returns, which equally amplifies losses. The collapse of Long-Term Capital Management in 1998 and the 2021 Archegos Capital implosion both illustrate how leveraged hedge fund strategies can produce catastrophic, rapid losses.

- Manager and operational risk: Hedge funds operate with far less regulatory oversight and transparency than mutual funds. Fraud cases — most infamously Bernie Madoff's multi-decade Ponzi scheme, which was structured and marketed as a hedge fund — demonstrate the heightened due diligence burden on investors in this less-regulated space.

-

Concentration risk: Many hedge fund strategies involve concentrated, high-conviction positions rather than diversified portfolios, increasing the potential for significant losses if a specific thesis proves incorrect.

Due diligence imperative: Before any direct hedge fund investment, conduct (or have a qualified advisor conduct) thorough due diligence: verify the fund's audited performance history through an independent administrator, confirm proper custody of assets with a reputable prime broker, review the fund's regulatory filings (Form ADV for SEC-registered advisors), and understand the complete fee structure including any hidden costs. The additional complexity and reduced transparency of hedge funds relative to mutual funds make this due diligence step non-negotiable.

Conclusion

Making money as a hedge fund investor is genuinely possible — but the path, the realistic expectations, and the appropriate strategy depend heavily on who you are, how much capital you have, and what level of complexity and risk you are prepared to manage. For accredited and qualified investors with substantial capital, direct hedge fund investment can provide genuine diversification benefits and access to sophisticated strategies unavailable elsewhere, provided rigorous due diligence is applied and fee structures are fully understood.For the much larger population of retail investors who do not meet accredited investor thresholds, publicly traded alternative asset manager stocks, liquid alternative mutual funds, and hedge-fund-style ETFs provide meaningful, accessible exposure to similar strategies and economics without the lock-up periods, high minimums, and reduced transparency of traditional hedge funds. And for those with the relevant skills and ambition, building a career within the hedge fund industry itself remains one of the most financially rewarding professional paths in finance.

Whatever route you pursue, the data is clear on one point: hedge fund exposure should be evaluated on its net-of-fee performance against realistic benchmarks, not on industry mythology or headline gross returns. A well-constructed portfolio of low-cost index funds has outperformed the average hedge fund over the past decade — meaning hedge fund exposure should be pursued for genuine diversification and risk-management benefits, not as an assumed shortcut to outsized wealth. Approached with this realistic framework, hedge fund investing can be a valuable component of a sophisticated financial strategy rather than an expensive disappointment.

Frequently Asked Questions (FAQ)

What qualifies someone as an accredited investor for hedge fund access?

Under current SEC rules, an individual qualifies as an accredited investor by having earned income exceeding $200,000 ($300,000 for joint filers) in each of the prior two years with a reasonable expectation of continuing at that level, or by having a net worth exceeding $1 million excluding the value of a primary residence. The SEC has also expanded accredited investor status to include individuals holding certain professional certifications, including Series 7, Series 65, and Series 82 licenses, regardless of income or net worth.Can a retail investor with no special qualifications invest in hedge funds at all?

Not directly in traditional, privately offered hedge funds — these are legally restricted to accredited and qualified investors. However, retail investors without these qualifications can still gain meaningful exposure to hedge-fund-style strategies and the hedge fund business model through publicly traded alternative asset manager stocks (Blackstone, KKR, Apollo, Ares), liquid alternative mutual funds, and hedge-fund-replicating ETFs — all of which are available through any standard brokerage account with no special qualification required.Do hedge funds really outperform the stock market?

On average, no — not over the past decade. The HFRI Fund Weighted Composite Index has returned approximately 6-7.5% annually over the trailing 10 years, compared to approximately 11-12% for the S&P 500 over the same period. However, this average masks enormous dispersion: top-quartile hedge funds and specific strategies (particularly during market downturns or periods of high volatility) have significantly outperformed, while many funds have underperformed substantially. Hedge funds are generally valued more for diversification and downside protection during market stress than for consistently beating equity market returns during bull markets.What is the difference between a hedge fund and a private equity fund?

Hedge funds typically invest in publicly traded securities (stocks, bonds, derivatives, currencies) using strategies that can be implemented relatively quickly, with most funds offering some form of periodic liquidity (often quarterly or annually, after an initial lock-up). Private equity funds typically acquire entire companies or significant ownership stakes in private businesses, hold these investments for much longer periods (typically 5-10 years), and offer essentially no liquidity until the fund's planned exit events (sale, IPO) occur. Both are generally restricted to accredited or qualified investors, but the underlying assets, time horizons, and liquidity profiles differ substantially.How do I evaluate whether a specific hedge fund is a good investment?

Key due diligence steps include: reviewing audited net-of-fee performance history (ideally five years or more) verified by an independent fund administrator; understanding the complete fee structure, including management fees, performance fees, and any hidden expenses; assessing the fund's strategy and whether it provides genuine diversification relative to your existing portfolio; verifying the fund's regulatory status and any disciplinary history through the SEC's Investment Adviser Public Disclosure (IAPD) database; confirming the use of a reputable, independent prime broker and fund administrator (separate from the fund manager) to reduce fraud risk; and assessing the lock-up period and redemption terms against your own liquidity needs. Engaging a qualified financial advisor experienced in alternative investments is strongly recommended for this evaluation process.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. HFR (Hedge Fund Research) — Global Hedge Fund Industry Report 2024

https://www.hfr.com/

2. Preqin — Global Hedge Fund Report 2024

https://www.preqin.com/insights/global-reports/2024-preqin-global-hedge-fund-report

3. US Securities and Exchange Commission — Accredited Investor Definition

https://www.sec.gov/resources-small-businesses/capital-raising-building-blocks/accredited-investor

4. Investopedia — How Hedge Funds Make Money: Fee Structures Explained

https://www.investopedia.com/articles/financial-careers/09/how-hedge-funds-make-money.asp

5. S&P Dow Jones Indices — S&P 500 Historical Returns Data

https://www.spglobal.com/spdji/en/indices/equity/sp-500/

6. SEC — Investment Adviser Public Disclosure (IAPD) Database

https://adviserinfo.sec.gov/

7. Institutional Investor — Hedge Fund Compensation Report 2023

https://www.institutionalinvestor.com/

8. CFA Institute — Understanding Alternative Investments and Hedge Fund Strategies

https://www.cfainstitute.org/research/alternative-investments

0 Comments Comments