Credits

Pay Off $10,000 Credit Card Debt in 10 Months

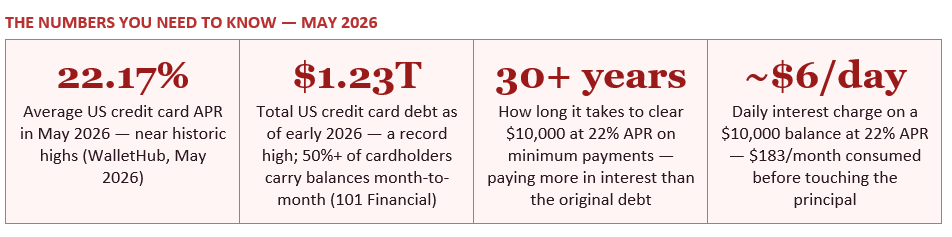

The average credit card APR in the US is 22.17% in May 2026 — near a record high. At that rate, $10,000 in credit card debt compounds by approximately $6 every single day. Making only minimum payments, you will spend over 30 years paying it off and pay more in interest than you originally borrowed. This guide shows a practical, month-by-month strategy to eliminate $10,000 in credit card debt in 10 months using strategic lump sum payments, saving over $19,000 compared to minimum payments alone.

101 Financial's May 2026 analysis documents the scale of the problem: Americans collectively carry $1.23 trillion in credit card debt as of early 2026, a record high. More than half of all credit cardholders carry balances month to month — meaning most people with credit cards are actively paying interest rather than paying in full. The Federal Reserve's H.15 data, cited by The Arca Labs' April 2026 analysis, confirms the average credit card interest rate reached 22.76% in early 2026, compared with 7.5% for a 60-month auto loan and roughly 6.5% to 7.0% for a 30-year mortgage.

The reason credit card rates are so high relative to other debt is structural: credit cards are unsecured. A mortgage is secured by the property — if you stop paying, the lender can take the house. A car loan is secured by the vehicle. Credit card debt has no underlying asset as collateral, so the lender prices the unsecured risk into a dramatically higher interest rate. For borrowers, this means that every day a credit card balance sits unpaid, the compounding mathematics work harder against them than on any other form of consumer debt.

If you pay only the minimum on a $6,580 balance at 22% interest, you'll spend over 30 years paying it off — and you'll pay more in interest than the original amount you borrowed. That's not a financial plan. That's a trap.

— 101 FINANCIAL — THE CREDIT CARD INTEREST RATE CAP IN 2026: WHAT IT MEANS FOR YOUR FAMILY'S DEBT (MAY 2026)

CDCalculators' March 2026 credit card interest calculator documents the minimum payment trap precisely. On a $5,000 balance at 18.99% APR with a $200 minimum payment, the total interest paid is $1,180 and the payoff takes 31 months — uncomfortable but manageable. Paying only the minimum payment of 2% ($100 initial)? Total interest: $7,240. Payoff time: 22 years. The same $5,000 debt, the same interest rate, but a near-doubling of interest paid, and a payoff timeline that stretches through almost a quarter century.

Scaled to $10,000 at 22% APR — the current average credit card rate — the numbers are even starker. A $200 minimum payment on $10,000 at 22% APR means roughly $183 of that $200 goes to interest in month one. Only $17 reduces the actual balance. Month after month, the vast majority of every payment is consumed by interest rather than reducing what you owe. Yahoo Finance's minimum payment analysis confirms: 'Minimum payments create a debt trap that's difficult to escape,' and that 'a typical $5,000 balance accumulates over $3 in new interest daily' at current rates — approximately $6 per day on a $10,000 balance.

The mathematics work as follows. Your annual APR of 22% is divided by 365 to produce a Daily Periodic Rate of approximately 0.0603%. This rate is applied to your average daily balance every day of the billing cycle. On a $10,000 balance, this means approximately $6.03 in new interest is added every single day — regardless of whether you make any payment. By the end of a 30-day billing cycle, $181 in interest has been added before you have made a single payment. Your $10,000 balance is now $10,181 before you have done anything at all.

The compounding element compounds this problem. In month two, the $181 in interest that was added in month one is now part of the principal balance — meaning it earns interest itself. Your interest accrues on interest, on interest, on interest. This is the mechanism that turns a manageable-sounding 22% APR into a balance that can grow faster than most people realise they are going deeper into debt. The only escape is to make payments that exceed the monthly interest charge — and ideally, to make periodic lump sum payments that dramatically reduce the principal balance and therefore the interest charged in all subsequent months.

The practical actions are specific: physically remove the high-interest card from your wallet and from any auto-saved payment methods (Amazon, streaming services, Apple Pay, Google Pay). Replace routine card spending with a debit card or cash for the duration of the payoff period. This is not forever — it is for 10 months. The temporary friction of not having the card immediately accessible is a feature, not a limitation: it creates a decision point before every potential new charge that would otherwise happen automatically.

Yakima Herald's April 2026 debt payoff guide is direct about this: 'The fastest way to pay off credit card debt is to stop adding new charges and aggressively pay more than the minimum.' Stopping new charges is not optional — it is the precondition that makes the 10-month plan achievable. Every dollar of new spending on the card while simultaneously trying to pay it down is fighting yourself.

The pattern that destroys most credit card payoff plans is predictable: a person pays down $2,000 of their balance over three months, then their car needs a $700 repair, they have no savings, they put it on the credit card, and they are back to nearly where they started — with two months of motivated paydown erased in a single emergency. The $500 to $1,000 emergency fund is the circuit breaker that prevents this cycle.

Once the micro emergency fund is in place — in a separate account from your everyday checking, so it is not spent casually — you have the financial foundation to attack the credit card balance aggressively. This fund should be treated as untouchable except for genuine emergencies (not discretionary purchases), and should be rebuilt immediately after any use.

With these three numbers, you can use a credit card payoff calculator (links in the References section) to see exactly what minimum payments produce versus what $1,000 per month produces versus what $1,000 per month plus periodic lump sums produces. Seeing the specific numbers for your exact situation — not hypothetical averages — is the most motivating input to the payoff plan, because the gap between the minimum payment outcome and the 10-month aggressive payoff is almost always dramatically larger than people expect.

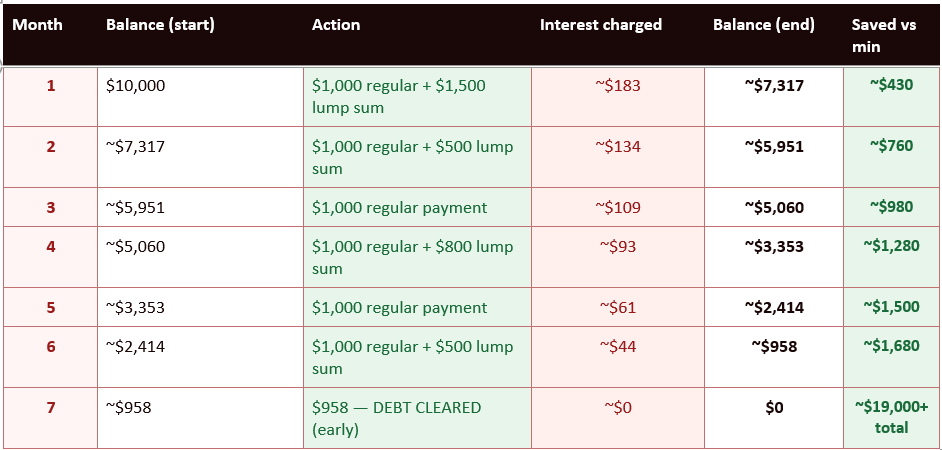

Illustrative figures. $1,000/month base + periodic lump sums at 22% APR. The table shows clearance in approximately 7 months in this scenario — the 10-month window allows for months with lower lump sum availability or unexpected expenses. Actual results depend on your specific balance, APR, payment timing, and lump sum amounts. Interest figures use approximate monthly interest = (Balance × APR/12).

The table illustrates the most important dynamic in the lump sum strategy: the effect on daily interest charges is visible and immediate. In month one, the $2,500 total payment (including the $1,500 lump sum) drives the balance from $10,000 to $7,317 — and the interest charge in month two falls from $183 to $134. By month three, the balance is below $6,000 and monthly interest has fallen to $109. By month six, the monthly interest charge is a fraction of what it was at the start. The lump sums break the compounding cycle at its most destructive phase — the period when the balance is highest and the interest charges are heaviest.

At 22% APR, every $1,000 of principal eliminated from the balance saves approximately $220 in annual interest — and because credit card interest compounds daily, the saving begins immediately rather than at the next monthly statement. A $1,500 lump sum applied in month one eliminates $1,500 of balance on which $330 per year in interest would have continued to accrue. Applied in month one rather than month six, this saves not just $330 in year-one interest but also all the compounded interest on the $330 in subsequent months.

The compounding savings work in reverse once you start reducing the principal. Just as compound interest on a growing balance accelerates debt growth, compound savings on a shrinking balance accelerate debt elimination. Each lump sum permanently reduces the daily interest calculation, which means each subsequent regular payment achieves a larger principal reduction than the previous one. This self-reinforcing acceleration is why a strategy that starts with larger early lump sums pays off faster than the same total amount spread evenly across the payoff period.

CNBC Select's February 2026 debt strategy guide explains the mechanism: 'A balance transfer card with a 0% intro APR period pauses the clock for up to 21 months, allowing you to make payments without accruing any additional interest.' CBS News' January 2026 analysis confirms: '0% introductory APR offers can allow you to temporarily escape interest charges altogether. These promotional rates typically last up to 21 months on purchases or balance transfers, giving you a window to pay down debt interest-free.'

The cost is a one-time balance transfer fee of 3% to 5% of the transferred amount. On $10,000, this is $300 to $500 — a significant upfront cost, but still far less than the $2,000+ in interest that a 10-month payoff plan at 22% APR would cost without the transfer. If you pay $1,000 per month on a $10,000 balance transferred to a 0% card with a $300 transfer fee, the total interest paid is $300 (the transfer fee) rather than $900 to $1,000 in APR-based interest charges. The saving is real and substantial.

The critical discipline is to complete the payoff before the promotional period ends. At the end of the 0% period, the remaining balance reverts to the card's standard APR — typically 24% to 28% — and the interest trap resumes. Set a clear payoff timeline before transferring, and calculate whether you can clear the balance within the promotional window at your monthly payment capacity. If you cannot, a balance transfer still makes sense but requires a plan for the remaining balance before the rate resets.

The avalanche method works as follows: list all your credit card balances with their APRs. Make minimum payments on every card. Direct all additional cash — regular overpayments and all lump sums — to the card with the highest APR first. When that card is paid off, redirect its entire payment (minimum plus any overpayment) to the card with the next highest APR. This eliminates the most expensive debt first, minimising total interest paid across all cards.

The Arca Labs' April 2026 comparison of avalanche versus snowball methods on multi-card debt shows that 'the avalanche saves approximately $400 in interest compared to the snowball approach and shaves roughly two months off the total payoff timeline.' For someone clearing $10,000 spread across three or four cards, $400 in additional interest savings plus two months faster payoff is a meaningful benefit from choosing the right sequencing strategy. The snowball method (paying smallest balances first for motivational wins) is psychologically effective but mathematically suboptimal — reserve it only for cases where motivational momentum is genuinely the limiting factor.

The sequence recommended by most financial planners follows a clear priority order. First, rebuild the emergency fund from the micro $1,000 level to a full three to six months of living expenses, held in a high-yield savings account. In the US in 2026, the best high-yield savings accounts are paying up to 5.00% APY (Varo Money) — dramatically better than a standard checking account and significantly better than the credit card debt rate you just eliminated. Second, if your employer offers a 401(k) match and you were not capturing it, increase your contribution to at least the employer match level — this is an immediate 50% to 100% return on that money. Third, any remaining surplus can be directed to investment accounts or additional savings.

The transformation from paying $1,000 per month in debt payments to saving and investing $1,000 per month is the practical definition of financial freedom — and Affordably.ai's debt payoff calculator captures this aspiration well: 'Debt-free! Now invest that money in your future: retirement, home, investments.' The 10-month credit card payoff is not the end of a financial journey. It is the elimination of the single biggest drag on wealth building that most American households carry.

A strategy of $1,000 monthly payments combined with strategic lump sums from tax refunds, bonuses, budget audits, and other sources can clear $10,000 in credit card debt in 7 to 10 months and save over $19,000 in interest compared with minimum payments. Each lump sum permanently reduces the daily interest calculation, making every subsequent payment more effective. The compound savings work as powerfully in your favour as compound interest previously worked against you. Stop adding new charges. Build the $1,000 safety net. Know your exact numbers. Apply every available lump sum to the balance as early as possible. And redirect the payment amount to savings and investment the month the debt is gone.

Motley Fool — Average Credit Card Interest Rate in February 2026 (April 2026) https://www.fool.com/money/research/average-credit-card-interest-rate/

101 Financial — The Credit Card Interest Rate Cap in 2026: What It Means for Your Family (May 2026) https://101financial.com/credit-card-interest-rate-cap-2026/

The Arca Labs — Debt Payoff: Snowball vs Avalanche Method Guide 2026 (April 2026) https://thearcalabs.com/en/insights/debt-payoff-strategies/

CDCalculators — How Much Credit Card Interest Will I Pay? 2026 Calculator USA (March 2026) https://cdcalculators.com/credit-card-interest-calculator/

CBS News — What's a Good Credit Card Interest Rate for 2026? (January 2026) https://www.cbsnews.com/news/whats-a-good-credit-card-interest-rate-for-2026/

CNBC Select — How to Break the Cycle of Debt in 2026 (April 2026) https://www.cnbc.com/select/how-to-break-the-cycle-of-debt/

Yakima Herald / NerdWallet — How to Pay off Credit Card Debt in 2026 (April 2026) https://www.yakimaherald.com/news/nation_and_world/business/how-to-pay-off-credit-card-debt-in-2026/article_817d3532-8f88-5f6f-a1fc-fad1bde29151.html

Affordably.ai — Free Debt Payoff Calculator: Avalanche vs Snowball (March 2026) https://affordably.ai/calculators/debt-payoff

TABLE OF CONTENTS

- Why Credit Card Debt Is Uniquely Dangerous

- The Minimum Payment Trap: What the Math Actually Shows

- How Daily Compounding Works Against You

- Step 1 — Stop the Bleeding: Freeze New Spending

- Step 2 — Build a Micro Emergency Fund First

- Step 3 — Know Your Exact Numbers

- The 10-Month Lump Sum Payoff Plan: Month by Month

- How Lump Sums Break the Compound Interest Cycle

- Sourcing Your Lump Sums: Practical Money Levers

- Should You Use a Balance Transfer Card First?

- The Avalanche Method: Optimising Multi-Card Debt

- What to Do with Your Money Once the Debt Is Gone

- Conclusion

- Frequently Asked Questions

- References

Why Credit Card Debt Is Uniquely Dangerous

Not all debt is created equal. A mortgage charges 6% to 7% per year. A federal student loan charges 5% to 7%. A car loan charges 5% to 8%. Credit card debt in May 2026 charges 22.17% on average — according to WalletHub's May 2026 Credit Card Landscape Report — with rates for borrowers with fair or poor credit frequently reaching 26% to 36%. This is not a minor difference in degree. It is a difference in kind that makes credit card debt categorically the most expensive form of consumer borrowing available to most Americans.101 Financial's May 2026 analysis documents the scale of the problem: Americans collectively carry $1.23 trillion in credit card debt as of early 2026, a record high. More than half of all credit cardholders carry balances month to month — meaning most people with credit cards are actively paying interest rather than paying in full. The Federal Reserve's H.15 data, cited by The Arca Labs' April 2026 analysis, confirms the average credit card interest rate reached 22.76% in early 2026, compared with 7.5% for a 60-month auto loan and roughly 6.5% to 7.0% for a 30-year mortgage.

The reason credit card rates are so high relative to other debt is structural: credit cards are unsecured. A mortgage is secured by the property — if you stop paying, the lender can take the house. A car loan is secured by the vehicle. Credit card debt has no underlying asset as collateral, so the lender prices the unsecured risk into a dramatically higher interest rate. For borrowers, this means that every day a credit card balance sits unpaid, the compounding mathematics work harder against them than on any other form of consumer debt.

If you pay only the minimum on a $6,580 balance at 22% interest, you'll spend over 30 years paying it off — and you'll pay more in interest than the original amount you borrowed. That's not a financial plan. That's a trap.

— 101 FINANCIAL — THE CREDIT CARD INTEREST RATE CAP IN 2026: WHAT IT MEANS FOR YOUR FAMILY'S DEBT (MAY 2026)

The Minimum Payment Trap: What the Math Actually Shows

Credit card issuers design minimum payments to feel manageable. The typical minimum is 1% to 3% of the outstanding balance — on a $10,000 balance, that is $100 to $300 per month. At that level, the payments feel reasonable. But the mathematics of what minimum payments actually accomplish are alarming.CDCalculators' March 2026 credit card interest calculator documents the minimum payment trap precisely. On a $5,000 balance at 18.99% APR with a $200 minimum payment, the total interest paid is $1,180 and the payoff takes 31 months — uncomfortable but manageable. Paying only the minimum payment of 2% ($100 initial)? Total interest: $7,240. Payoff time: 22 years. The same $5,000 debt, the same interest rate, but a near-doubling of interest paid, and a payoff timeline that stretches through almost a quarter century.

Scaled to $10,000 at 22% APR — the current average credit card rate — the numbers are even starker. A $200 minimum payment on $10,000 at 22% APR means roughly $183 of that $200 goes to interest in month one. Only $17 reduces the actual balance. Month after month, the vast majority of every payment is consumed by interest rather than reducing what you owe. Yahoo Finance's minimum payment analysis confirms: 'Minimum payments create a debt trap that's difficult to escape,' and that 'a typical $5,000 balance accumulates over $3 in new interest daily' at current rates — approximately $6 per day on a $10,000 balance.

How Daily Compounding Works Against You

The mechanism that makes credit card debt grow so fast — faster than any calculation based on simple annual percentages suggests — is daily compounding. Unlike most loans, which charge interest monthly, credit card issuers calculate and apply interest every single day using the Average Daily Balance method required by the CARD Act.The mathematics work as follows. Your annual APR of 22% is divided by 365 to produce a Daily Periodic Rate of approximately 0.0603%. This rate is applied to your average daily balance every day of the billing cycle. On a $10,000 balance, this means approximately $6.03 in new interest is added every single day — regardless of whether you make any payment. By the end of a 30-day billing cycle, $181 in interest has been added before you have made a single payment. Your $10,000 balance is now $10,181 before you have done anything at all.

The compounding element compounds this problem. In month two, the $181 in interest that was added in month one is now part of the principal balance — meaning it earns interest itself. Your interest accrues on interest, on interest, on interest. This is the mechanism that turns a manageable-sounding 22% APR into a balance that can grow faster than most people realise they are going deeper into debt. The only escape is to make payments that exceed the monthly interest charge — and ideally, to make periodic lump sum payments that dramatically reduce the principal balance and therefore the interest charged in all subsequent months.

Step 1 — Stop the Bleeding: Freeze New Spending

Before any payoff strategy can work, you must stop adding to the balance. This sounds obvious, but it is the most commonly skipped step. Every new purchase on a card with a balance negates some portion of the progress made by your payments, re-feeds the compounding cycle, and psychologically undermines the sense of progress that keeps people motivated through a 10-month payoff plan.The practical actions are specific: physically remove the high-interest card from your wallet and from any auto-saved payment methods (Amazon, streaming services, Apple Pay, Google Pay). Replace routine card spending with a debit card or cash for the duration of the payoff period. This is not forever — it is for 10 months. The temporary friction of not having the card immediately accessible is a feature, not a limitation: it creates a decision point before every potential new charge that would otherwise happen automatically.

Yakima Herald's April 2026 debt payoff guide is direct about this: 'The fastest way to pay off credit card debt is to stop adding new charges and aggressively pay more than the minimum.' Stopping new charges is not optional — it is the precondition that makes the 10-month plan achievable. Every dollar of new spending on the card while simultaneously trying to pay it down is fighting yourself.

Step 2 — Build a Micro Emergency Fund First

The second step before attacking the debt aggressively is counterintuitive but critical: build a small emergency fund of $500 to $1,000 before throwing all available cash at the credit card balance. This micro emergency fund exists for one purpose — to prevent you from returning to the credit card when an unexpected expense arises.The pattern that destroys most credit card payoff plans is predictable: a person pays down $2,000 of their balance over three months, then their car needs a $700 repair, they have no savings, they put it on the credit card, and they are back to nearly where they started — with two months of motivated paydown erased in a single emergency. The $500 to $1,000 emergency fund is the circuit breaker that prevents this cycle.

Once the micro emergency fund is in place — in a separate account from your everyday checking, so it is not spent casually — you have the financial foundation to attack the credit card balance aggressively. This fund should be treated as untouchable except for genuine emergencies (not discretionary purchases), and should be rebuilt immediately after any use.

Step 3 — Know Your Exact Numbers

Before building the payoff plan, gather three specific pieces of information about your credit card balance. First, the exact current balance. Second, the exact APR (not just the range mentioned in your agreement — the specific rate being applied to your account today, visible on your most recent statement). Third, the minimum payment formula your issuer uses (most use 1% to 2% of the balance plus interest, or a flat minimum of $25 to $35, whichever is greater).With these three numbers, you can use a credit card payoff calculator (links in the References section) to see exactly what minimum payments produce versus what $1,000 per month produces versus what $1,000 per month plus periodic lump sums produces. Seeing the specific numbers for your exact situation — not hypothetical averages — is the most motivating input to the payoff plan, because the gap between the minimum payment outcome and the 10-month aggressive payoff is almost always dramatically larger than people expect.

The 10-Month Lump Sum Payoff Plan: Month by Month

The following plan assumes a $10,000 balance at 22% APR, a base payment of $1,000 per month, and periodic lump sum injections from the sources described in the next section. All figures are illustrative and based on standard credit card amortisation calculations.Illustrative figures. $1,000/month base + periodic lump sums at 22% APR. The table shows clearance in approximately 7 months in this scenario — the 10-month window allows for months with lower lump sum availability or unexpected expenses. Actual results depend on your specific balance, APR, payment timing, and lump sum amounts. Interest figures use approximate monthly interest = (Balance × APR/12).

The table illustrates the most important dynamic in the lump sum strategy: the effect on daily interest charges is visible and immediate. In month one, the $2,500 total payment (including the $1,500 lump sum) drives the balance from $10,000 to $7,317 — and the interest charge in month two falls from $183 to $134. By month three, the balance is below $6,000 and monthly interest has fallen to $109. By month six, the monthly interest charge is a fraction of what it was at the start. The lump sums break the compounding cycle at its most destructive phase — the period when the balance is highest and the interest charges are heaviest.

How Lump Sums Break the Compound Interest Cycle

The reason lump sum payments are so disproportionately powerful in credit card debt payoff is the same reason they work on mortgages — but the effect is even more dramatic because the interest rate is three to four times higher.At 22% APR, every $1,000 of principal eliminated from the balance saves approximately $220 in annual interest — and because credit card interest compounds daily, the saving begins immediately rather than at the next monthly statement. A $1,500 lump sum applied in month one eliminates $1,500 of balance on which $330 per year in interest would have continued to accrue. Applied in month one rather than month six, this saves not just $330 in year-one interest but also all the compounded interest on the $330 in subsequent months.

The compounding savings work in reverse once you start reducing the principal. Just as compound interest on a growing balance accelerates debt growth, compound savings on a shrinking balance accelerate debt elimination. Each lump sum permanently reduces the daily interest calculation, which means each subsequent regular payment achieves a larger principal reduction than the previous one. This self-reinforcing acceleration is why a strategy that starts with larger early lump sums pays off faster than the same total amount spread evenly across the payoff period.

Sourcing Your Lump Sums: Practical Money Levers

Eight sources of lump sum credit card payments — practical for most households

- Tax refund (immediate highest-impact lump sum): The average US federal tax refund is approximately $3,000. Applied to a $10,000 credit card balance in the first month, a $3,000 tax refund eliminates roughly 30% of the balance instantly — saving approximately $660 in annual interest from the moment it is applied. Never deposit a tax refund into a checking account where it will be spent gradually. Apply it directly to the credit card balance on the day it clears.

- Work bonus or commission payment: If you receive an annual, quarterly, or performance bonus, commit 50% to 100% of the after-tax amount to the credit card before spending any of it. The psychological temptation to treat bonus money as discretionary income is the single biggest obstacle to this strategy. Treat bonuses as debt payments until the balance is zero.

- Budget audit — find $200 to $500/month: The debt payoff calculator at Affordably.ai notes that 'most people find $200 to $500 extra' when they audit their spending. Streaming subscriptions, gym memberships not used, food delivery habits, and discretionary subscriptions collectively often total $200 to $400 per month for average households. Temporarily redirecting these amounts to the credit card increases the monthly payment significantly without changing income.

- Sell unused items: Every household has items of value not being used — electronics, clothing, furniture, sports equipment, musical instruments. Selling these through eBay, Facebook Marketplace, or Craigslist generates one-time lump sums with zero impact on current income. A realistic $300 to $1,000 from selling unused items in a household is achievable within a month.

- Overtime or additional income: Taking additional shifts, freelancing, or consulting for one project during the payoff period generates income that can be specifically designated for debt payoff. Ten extra hours of overtime at $25 per hour generates $250 per fortnight — $500 per month — that can be treated as a dedicated lump sum payment rather than income to be budgeted.

- Cancel and redirect subscription spending: Identify every recurring subscription charge and cancel all non-essential services for the 10-month payoff period. A typical household with Netflix, Spotify, a gym, multiple streaming services, and miscellaneous subscriptions may be spending $150 to $300 per month on services that can be suspended temporarily. Redirect these amounts to the credit card balance as an automatic monthly lump sum top-up.

- Annual insurance or subscription renewals: Switching to annual billing for insurance (car, renters/homeowners) rather than monthly billing typically saves 10% to 15% — generating a one-time saving that can be applied to the balance. Simultaneously, shopping insurance policies at renewal often produces savings of $100 to $400 per year.

- Emergency fund surplus: Once the micro emergency fund is established at $1,000, any accumulation in that fund above $1,000 (from months when no emergency occurs) should be swept to the credit card balance. This prevents the emergency fund from growing while high-interest debt remains outstanding.

Should You Use a Balance Transfer Card First?

If your credit score is 670 or above, a balance transfer card with a 0% introductory APR offers one of the most powerful interest elimination tools available — pausing compounding entirely for up to 21 months and allowing every dollar of payment to reduce the principal rather than being partially consumed by interest.CNBC Select's February 2026 debt strategy guide explains the mechanism: 'A balance transfer card with a 0% intro APR period pauses the clock for up to 21 months, allowing you to make payments without accruing any additional interest.' CBS News' January 2026 analysis confirms: '0% introductory APR offers can allow you to temporarily escape interest charges altogether. These promotional rates typically last up to 21 months on purchases or balance transfers, giving you a window to pay down debt interest-free.'

The cost is a one-time balance transfer fee of 3% to 5% of the transferred amount. On $10,000, this is $300 to $500 — a significant upfront cost, but still far less than the $2,000+ in interest that a 10-month payoff plan at 22% APR would cost without the transfer. If you pay $1,000 per month on a $10,000 balance transferred to a 0% card with a $300 transfer fee, the total interest paid is $300 (the transfer fee) rather than $900 to $1,000 in APR-based interest charges. The saving is real and substantial.

The critical discipline is to complete the payoff before the promotional period ends. At the end of the 0% period, the remaining balance reverts to the card's standard APR — typically 24% to 28% — and the interest trap resumes. Set a clear payoff timeline before transferring, and calculate whether you can clear the balance within the promotional window at your monthly payment capacity. If you cannot, a balance transfer still makes sense but requires a plan for the remaining balance before the rate resets.

The Avalanche Method: Optimising Multi-Card Debt

If your $10,000 in credit card debt is spread across multiple cards rather than concentrated on one, the debt avalanche method is the most financially efficient payoff strategy. The Arca Labs' April 2026 analysis confirms: 'The avalanche method guarantees the lowest total interest cost among all deterministic payoff orderings.'The avalanche method works as follows: list all your credit card balances with their APRs. Make minimum payments on every card. Direct all additional cash — regular overpayments and all lump sums — to the card with the highest APR first. When that card is paid off, redirect its entire payment (minimum plus any overpayment) to the card with the next highest APR. This eliminates the most expensive debt first, minimising total interest paid across all cards.

The Arca Labs' April 2026 comparison of avalanche versus snowball methods on multi-card debt shows that 'the avalanche saves approximately $400 in interest compared to the snowball approach and shaves roughly two months off the total payoff timeline.' For someone clearing $10,000 spread across three or four cards, $400 in additional interest savings plus two months faster payoff is a meaningful benefit from choosing the right sequencing strategy. The snowball method (paying smallest balances first for motivational wins) is psychologically effective but mathematically suboptimal — reserve it only for cases where motivational momentum is genuinely the limiting factor.

What to Do with Your Money Once the Debt Is Gone

The month after the last credit card payment clears is a financial turning point. The $1,000 or more per month that was going to debt payments is now available — and the single most important financial decision is what to do with it before it is absorbed by lifestyle spending.The sequence recommended by most financial planners follows a clear priority order. First, rebuild the emergency fund from the micro $1,000 level to a full three to six months of living expenses, held in a high-yield savings account. In the US in 2026, the best high-yield savings accounts are paying up to 5.00% APY (Varo Money) — dramatically better than a standard checking account and significantly better than the credit card debt rate you just eliminated. Second, if your employer offers a 401(k) match and you were not capturing it, increase your contribution to at least the employer match level — this is an immediate 50% to 100% return on that money. Third, any remaining surplus can be directed to investment accounts or additional savings.

The transformation from paying $1,000 per month in debt payments to saving and investing $1,000 per month is the practical definition of financial freedom — and Affordably.ai's debt payoff calculator captures this aspiration well: 'Debt-free! Now invest that money in your future: retirement, home, investments.' The 10-month credit card payoff is not the end of a financial journey. It is the elimination of the single biggest drag on wealth building that most American households carry.

CONCLUSION

A $10,000 credit card balance at 22% APR compounds by approximately $6 every single day. On minimum payments alone, it will take 30 years and cost more in interest than the original debt. That is not an exaggeration or a worst-case scenario — it is the mathematical reality of how credit card debt at current average APRs works. But the same mathematics that makes credit card debt so expensive to carry in passivity makes it so responsive to aggressive, front-loaded attack.A strategy of $1,000 monthly payments combined with strategic lump sums from tax refunds, bonuses, budget audits, and other sources can clear $10,000 in credit card debt in 7 to 10 months and save over $19,000 in interest compared with minimum payments. Each lump sum permanently reduces the daily interest calculation, making every subsequent payment more effective. The compound savings work as powerfully in your favour as compound interest previously worked against you. Stop adding new charges. Build the $1,000 safety net. Know your exact numbers. Apply every available lump sum to the balance as early as possible. And redirect the payment amount to savings and investment the month the debt is gone.

Frequently Asked Questions

How much does $10,000 in credit card debt cost at 22% APR if I only make minimum payments?

On minimum payments alone (assuming 2% of the balance per month as the minimum), a $10,000 balance at 22% APR will take approximately 30 years or more to clear and will cost well over $10,000 in interest — meaning you pay back more than double what you originally owed. CDCalculators' March 2026 credit card interest calculator documents that at 18.99% APR (below the current 22% average), a $5,000 balance on minimum payments alone costs $7,240 in total interest over 22 years. At 22% APR on $10,000, the total interest paid on minimum payments only exceeds the original balance within roughly 15 years and the payoff extends past 30 years. The average daily interest charge on $10,000 at 22% is approximately $6.03 — roughly $183 per month consumed by interest before any principal reduction occurs.Why do lump sum payments reduce interest so quickly?

Credit card interest is calculated daily on your average daily balance. Every dollar of principal you remove from the balance is a dollar on which the 22% APR daily interest rate ($0.0603 per day per dollar) no longer applies — permanently, from the moment the payment clears. A $1,500 lump sum applied in month one eliminates $1,500 from the daily interest calculation for all remaining months. At 22% APR, that $1,500 of eliminated principal saves approximately $330 per year in interest — and because the savings begin immediately rather than gradually, the total interest saving is greater than it would be if the same amount were spread across monthly payments. The earlier in the payoff period you apply a lump sum, the longer the compounding savings chain you create.Should I get a 0% balance transfer card to pay off $10,000 in credit card debt?

If your credit score is 670 or above, a 0% introductory APR balance transfer card is one of the most powerful tools available for eliminating $10,000 in credit card debt efficiently. CNBC Select's February 2026 guide identifies offers of up to 21 months at 0% APR on balance transfers. The cost is a one-time transfer fee of 3% to 5% (approximately $300 to $500 on $10,000). This fee is substantially less than the $900 to $1,000+ in interest you would pay during a 10-month aggressive payoff at 22% APR. The critical requirement is to have a clear plan to pay off the transferred balance before the promotional period ends — if the balance rolls to the card's standard APR (typically 24% to 28%), the interest advantage evaporates. CBS News' January 2026 analysis confirms these offers provide 'meaningful savings if you can pay off the balance before the introductory period ends.'What is the difference between the avalanche and snowball method for credit card debt?

Both methods direct all available extra cash to one card at a time while making minimum payments on the rest. The difference is which card you target first. The debt avalanche method targets the card with the highest APR first — this is mathematically optimal and saves the most in total interest. The Arca Labs' April 2026 analysis shows the avalanche saves approximately $400 more in interest than the snowball method on comparable multi-card debts and pays off debt approximately two months faster. The debt snowball method targets the smallest balance first, regardless of APR — this generates faster early wins that maintain motivation but costs slightly more in total interest. For a single $10,000 balance on one card, the distinction is irrelevant. For debt spread across multiple cards with different APRs, the avalanche method is the more financially efficient choice.What should I do with the money I was spending on credit card payments once the debt is paid off?

The month your credit card balance reaches zero, redirect the entire monthly payment amount — $1,000 or more — into the following priority sequence rather than allowing it to be absorbed by lifestyle spending. First, rebuild your emergency fund from the $1,000 micro level to a full three to six months of essential living expenses, held in a high-yield savings account (currently paying up to 5.00% APY in the US). Second, ensure you are capturing any employer 401(k) match — this is a guaranteed 50% to 100% immediate return on that contribution. Third, increase contributions to retirement accounts (Roth IRA, 401(k) beyond the match) or other investment accounts. The shift from paying $1,000+ per month in credit card interest to saving and investing $1,000+ per month is one of the most powerful wealth-building transitions available to a household — and it begins the month the debt is cleared.References

WalletHub — Average Credit Card Interest Rates for May 2026 (May 2026) https://wallethub.com/edu/cc/average-credit-card-interest-rate/50841Motley Fool — Average Credit Card Interest Rate in February 2026 (April 2026) https://www.fool.com/money/research/average-credit-card-interest-rate/

101 Financial — The Credit Card Interest Rate Cap in 2026: What It Means for Your Family (May 2026) https://101financial.com/credit-card-interest-rate-cap-2026/

The Arca Labs — Debt Payoff: Snowball vs Avalanche Method Guide 2026 (April 2026) https://thearcalabs.com/en/insights/debt-payoff-strategies/

CDCalculators — How Much Credit Card Interest Will I Pay? 2026 Calculator USA (March 2026) https://cdcalculators.com/credit-card-interest-calculator/

CBS News — What's a Good Credit Card Interest Rate for 2026? (January 2026) https://www.cbsnews.com/news/whats-a-good-credit-card-interest-rate-for-2026/

CNBC Select — How to Break the Cycle of Debt in 2026 (April 2026) https://www.cnbc.com/select/how-to-break-the-cycle-of-debt/

Yakima Herald / NerdWallet — How to Pay off Credit Card Debt in 2026 (April 2026) https://www.yakimaherald.com/news/nation_and_world/business/how-to-pay-off-credit-card-debt-in-2026/article_817d3532-8f88-5f6f-a1fc-fad1bde29151.html

Affordably.ai — Free Debt Payoff Calculator: Avalanche vs Snowball (March 2026) https://affordably.ai/calculators/debt-payoff

0 Comments Comments