Retirement

Things That Feel Responsible But Wreck Your Retirement

Table of Contents

- The Problem With Feeling Financially Responsible

- The State of American Retirement in 2026: The Key Statistics

- Feels Responsible vs Financial Reality: The Complete Comparison

- 1. Paying Off the Mortgage Early — At the Cost of Retirement Contributions

- 2. Claiming Social Security Early 'Just to Be Safe'

- 3. Keeping Too Much Money in Cash 'To Be Safe'

- 4. Financially Supporting Adult Children at the Expense of Retirement

- 5. Going Too Conservative With Investments as Retirement Approaches

- 6. Treating Social Security as a Retirement Plan Rather Than a Supplement

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Problem With Feeling Financially Responsible

There is a particular category of financial mistake that is uniquely dangerous: the kind that feels like the right thing to do. Not reckless spending or ignoring retirement entirely — those mistakes at least come with a nagging sense that something is wrong. The most costly retirement mistakes are the ones that feel disciplined, prudent, even admirable. Paying off the house before retiring. Claiming Social Security early to 'lock it in.' Keeping money in a savings account because the market is scary. Helping adult children financially because you love them and have worked hard. Going conservative with your portfolio because you are getting older.Northwestern Mutual's 2026 Planning and Progress Study found that Americans now believe they need $1.46 million to retire comfortably — yet 23% of those with retirement savings have one year or less of their current income saved, and among Gen Xers specifically, one in three has three times or less of their annual income put away. The gap between intention and outcome is not primarily explained by recklessness. It is explained by a series of individually reasonable-feeling financial decisions that, in combination and viewed through the lens of long-term compounding, quietly undermine the retirement that all of the underlying intention was designed to protect.

This guide works through the most common of these responsible-feeling mistakes — what each one feels like, what the financial data actually shows about its long-term impact, and what a better approach looks like. None of these corrections require you to become a financial expert. Most of them require only a shift in how you frame the decision — from 'what feels safe' to 'what does the math say over 20 or 30 years.'

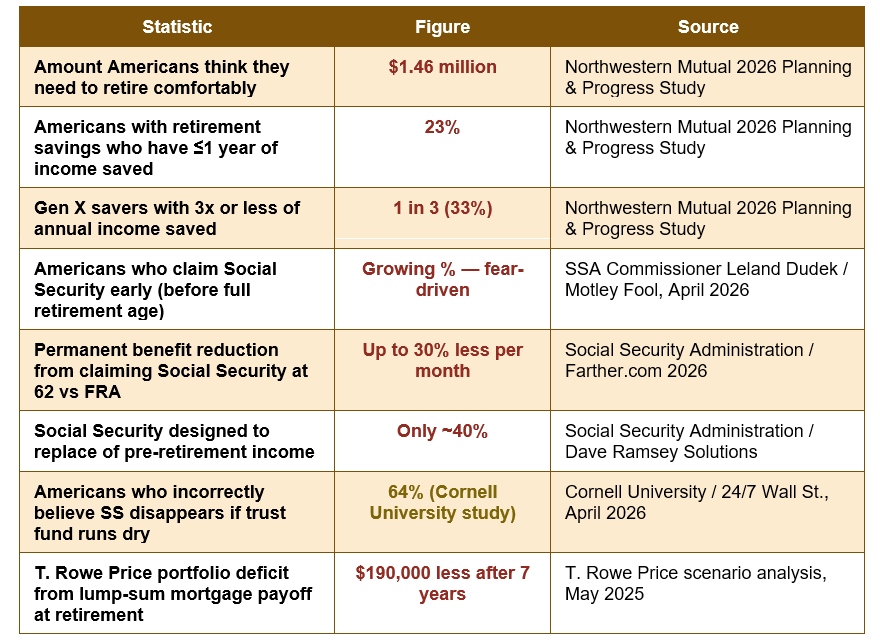

The State of American Retirement in 2026: The Key Statistics

The $1.46 million gap: Americans say they need $1.46M to retire — 23% have 1 year or less of income saved — the gap between what Americans believe is required and what they have actually accumulated reflects decades of individually reasonable-feeling financial decisions that collectively fell short — and understanding which decisions are responsible for the gap is the starting point for closing it (Northwestern Mutual 2026 Planning & Progress Study).

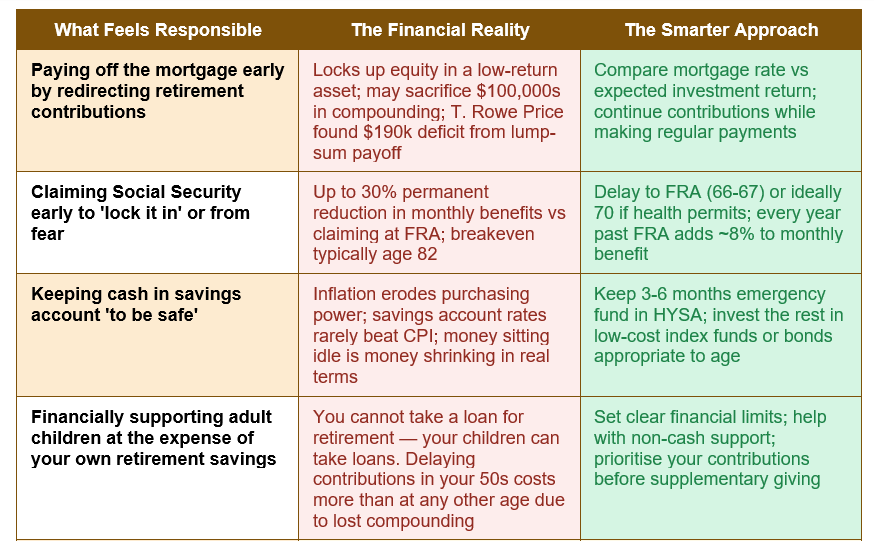

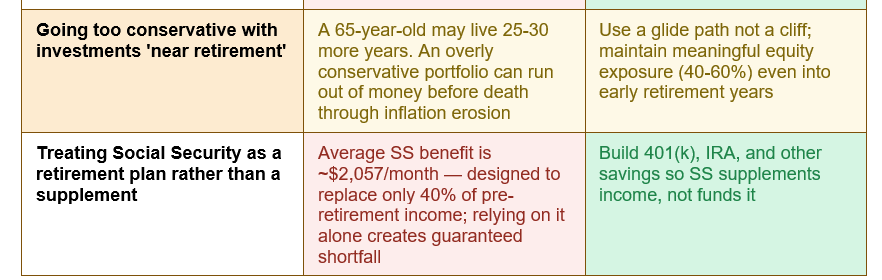

Feels Responsible vs Financial Reality: The Complete Comparison

The table below maps each common responsible-feeling behaviour against what the financial data shows about its impact:

1. Paying Off the Mortgage Early — At the Cost of Retirement Contributions

Owning your home outright before retirement feels like the ultimate expression of financial responsibility. No debt, no monthly obligation, a house that is fully yours. The emotional case is strong — even financial author Morgan Housel, who wrote The Psychology of Money, admitted to Bankrate that he carries no mortgage despite acknowledging it is 'on paper, the dumbest thing you could possibly do.' As a purely mathematical statement, this is accurate for many homeowners.The critical question is not whether paying off your mortgage feels good — it does — but what you are giving up to do it. If the money redirected to accelerated mortgage payments would otherwise go into a 401(k) or IRA that earns a long-term average of 7-8% annually, and your mortgage rate is 3-4%, the opportunity cost of those accelerated payments is the difference between those two rates, compounded for decades. T. Rowe Price's detailed scenario analysis from May 2025 found that a retiree who paid off their mortgage using a lump-sum distribution at the start of retirement — but continued their $5,000 per month spending — had a portfolio balance $190,000 lower after just seven years compared with the retiree who maintained their mortgage.

As Ameriprise Financial's guidance notes: 'You cannot take a loan for retirement. You can take a loan for a mortgage.' This framing clarifies the asymmetry. The mortgage can be serviced with income; retirement savings cannot be borrowed later. The general principle from multiple financial institutions in 2025-2026 is: if your mortgage rate is below the expected return on low-risk investments — and certainly below the expected long-term return on a diversified portfolio — you are usually better off maintaining the mortgage and investing the difference.

The rate comparison rule: Bankrate's January 2026 guide states that if your mortgage rate is around 3%, it may not make sense to pay it off early when CDs or money market accounts are earning closer to 4%. If your mortgage rate is 6% or 7%, directing extra money toward it becomes more defensible since low-risk investments earning above that rate are harder to find. The key calculation: compare your after-tax mortgage rate to the after-tax expected return on whatever alternative investment you would make instead.

2. Claiming Social Security Early 'Just to Be Safe'

The fear that drives early Social Security claiming is understandable and, in some cases, rational. SSA Commissioner Leland Dudek noted in 2025 that fear — specifically, fear about Social Security's long-term solvency — was causing a growing number of people to claim benefits before their Full Retirement Age (FRA). Cornell University research, cited by 24/7 Wall St. in April 2026, found that 64% of Americans who see a graph of the Social Security trust fund's projected depletion assume that benefits will disappear entirely — when in fact, even under the worst depletion scenario, ongoing payroll tax revenue would fund approximately 75-80% of scheduled benefits.The financial cost of early claiming is permanent and specific. Claiming at 62 — the earliest eligible age — rather than waiting until Full Retirement Age (66-67 depending on birth year) permanently reduces your monthly benefit by up to 30%. Every year you delay claiming past FRA adds approximately 8% to your monthly benefit, up to age 70. The Motley Fool's April 2026 analysis of this dynamic confirmed: 'Filing early means locking in a permanent reduction in benefits, up to 30% if your full retirement age is 67.' The breakeven point — where the higher delayed benefit has paid back more than the forgone early payments — is typically around age 82 under current conditions.

For anyone in reasonable health who can manage cash flow without the Social Security payment, delaying to at least FRA — and ideally to 70 — dramatically increases lifetime benefits. As GOBankingRates reported in 2026, the Social Security Administration estimated that approximately 71 million Americans receive Social Security benefits, with an average monthly benefit of $2,057 for retirees. At a 30% early-claiming reduction, the difference is a permanent $617 per month — over $7,400 per year for the rest of your life.

The 8% annual return for patience: Each year you delay Social Security past FRA adds ~8% to your monthly benefit — delaying from 67 (FRA for those born after 1960) to 70 produces a 24% larger monthly payment for the rest of your life — the equivalent of a guaranteed 8% annualised return that no other low-risk investment reliably matches (Social Security Administration / Farther.com, 2026).

3. Keeping Too Much Money in Cash 'To Be Safe'

The impulse to keep money in savings accounts or money market funds feels entirely prudent, especially as retirement approaches. The market has had dramatic downturns; losing money you cannot afford to lose would be catastrophic. The instinct to protect principal is not irrational — it is just frequently taken too far and confused with the genuinely appropriate step of maintaining an emergency fund.The problem with excessive cash holdings is inflation. Over the past decade, the average US inflation rate has consistently eroded the purchasing power of money held at savings account rates. A dollar earning 0.5% in a standard savings account against 3-4% inflation loses real purchasing power every year it sits there. High-yield savings accounts have helped somewhat, with rates reaching 4-5% at their peak in 2024-2025, but these rates are variable and typically lag inflation over long periods. Money that is not invested is not safely stored — it is slowly losing value in real terms.

The appropriate amount of cash to hold before and in early retirement is generally three to six months of living expenses in a truly liquid account. Beyond that, the money should be working — in bonds, dividend-paying equities, a diversified retirement fund, or another instrument that at least preserves purchasing power. Kiplinger's retirement guidance from 2026 notes that retirees need meaningful exposure to growth assets because a 65-year-old can reasonably expect to live 25-30 more years. An overly conservative portfolio — one that is 80-90% cash and bonds — may protect nominal value while slowly losing the battle against inflation and healthcare cost growth over a three-decade retirement.

4. Financially Supporting Adult Children at the Expense of Retirement

Helping your children is not a mistake. Depleting your retirement savings to do so might be. The financial reality of supporting adult children — whether paying for college tuition from savings rather than loans, subsidising rent and living expenses for an adult child, or cosigning debt — is that it depletes assets and redirects cash flow at precisely the most expensive moment to do so. The compounding cost of money not invested in your 50s is dramatically higher than the same decision made in your 30s, because the time for that money to grow before retirement is measured in years rather than decades.The Ameriprise framing captures this clearly: you cannot take a loan for retirement. Your adult children can take student loans; they can find ways to supplement their income; they can build their own financial resilience. Your retirement savings, once depleted or foregone, cannot be recovered through any mechanism other than working longer. Working longer is always an option — but it should be a choice, not a compelled consequence of having redirected retirement contributions to support someone who had alternative options.

This is not an argument for financial hardheartedness toward children you love. It is an argument for ensuring that the financial support you provide does not come from the specific bucket — tax-advantaged retirement accounts, especially during the catch-up contribution years after age 50 — that cannot be borrowed, worked back, or replaced. Non-financial support (advice, time, connection, help with childcare, shared housing) has significant value and does not come from the retirement bucket.

The put your own oxygen mask on first principle: Retirement advisers consistently use this airline safety metaphor because it captures the financial reality precisely. A parent who runs out of money in retirement becomes a financial burden on their adult children — the very people they were trying to help. Maintaining your own financial security is the most sustainable form of support you can provide to the next generation.

5. Going Too Conservative With Investments as Retirement Approaches

The conventional wisdom that you should shift dramatically from equities to bonds as you approach retirement has evolved considerably over the past decade, and in its most extreme form — moving 80% or more into cash and fixed income at age 60 or 65 — it can create a serious long-term risk that is less visible than market volatility: the risk of outliving your money.Today's 65-year-old American has a significant probability of living into their late 80s or early 90s. A 25-30 year retirement requires a portfolio that continues to grow in real terms throughout that period, not one that merely protects nominal principal. The Northwestern Mutual 2026 Planning and Progress Study noted that one in five Americans in every age cohort believe they will 'never be financially independent' — a despair that often traces back to portfolios that grew insufficiently during the accumulation phase, compounded by investment approaches that were too conservative too early in the distribution phase.

The smarter approach is a glide path rather than a cliff: gradually reducing equity exposure across the decade or two before and after retirement, rather than a sudden shift at a specific birthday. Many target-date funds implement this automatically, and Kiplinger's retirement guidance from 2026 specifically recommends that savers review their target-date fund at least annually to ensure the target date still aligns with their intended retirement, and that the fund's allocation is appropriate for their actual risk tolerance rather than merely their birth year.

6. Treating Social Security as a Retirement Plan Rather Than a Supplement

Social Security was designed as a safety net — a supplemental income floor that, combined with personal savings, pensions, and other income sources, provides for retirement security. It was never designed to be the primary or sole source of retirement income. Yet Dave Ramsey Solutions' research found that nearly half of Americans are not saving enough for retirement, and the Social Security Administration itself notes that the program is designed to replace approximately 40% of pre-retirement income. A worker earning $60,000 per year might receive approximately $24,000 annually from Social Security at full retirement age — a figure that does not cover average US housing costs alone in most markets.The average monthly Social Security benefit of approximately $2,057 per month works as part of a broader income picture that also includes 401(k) distributions, IRA withdrawals, rental income, part-time work, or other sources. As a standalone income, it leaves most Americans well below their pre-retirement standard of living. The Motley Fool's April 2026 analysis confirmed that Social Security alone cannot fund a comfortable retirement — yet the gravitational pull of Social Security as a concrete, guaranteed number makes it easy to use it as an anchor that crowds out the harder work of projecting and filling the gap.

Conclusion

The most insidious threats to a secure retirement are not laziness, recklessness, or financial ignorance. They are decisions that feel responsible — that come from a genuine desire to be debt-free, cautious, generous, and secure — but that, when measured against the mathematics of compounding over decades, systematically undermine the outcome they are intended to protect. Paying off a low-rate mortgage by redirecting retirement contributions. Claiming Social Security early from fear of a solvency problem that would not actually eliminate benefits. Accumulating cash at inflation-lagging rates in the name of safety. Supporting adult children from retirement savings that cannot be recovered. Moving too aggressively to conservative investments before a retirement that may last 30 years.Northwestern Mutual's 2026 data crystallises the scale of the problem: Americans believe they need $1.46 million to retire comfortably, yet 23% of those with any savings have only one year of income put away. Among Gen X, one-third are at three times or less their annual income — a group that is close enough to retirement that the compounding clock is nearly exhausted. The gap between intention and outcome is not inevitable. It can be narrowed by examining which of these responsible-feeling decisions are actually costing the most, and making the specific, targeted adjustments that the data supports.

The corrections are not dramatic. Keep contributing to tax-advantaged accounts before accelerating the mortgage. Learn the actual numbers on Social Security delay before claiming early from fear. Maintain an emergency fund in cash and invest the rest. Draw a clear line between supporting your children from current income and raiding retirement accounts. And maintain enough equity exposure to give your portfolio the growth runway a 30-year retirement requires. None of these changes requires you to feel less responsible. They require you to redefine what responsible means in a financial context — from what feels safe in the short term to what the data shows produces financial security over a lifetime.

Frequently Asked Questions (FAQ)

Should I pay off my mortgage before I retire?

It depends on your specific mortgage rate and your investment alternatives. If your mortgage rate is below what you can earn on low-risk investments — a reasonable assumption for anyone with a pre-2022 mortgage rate of 3-4% — paying it off early often means forgoing investment returns that exceed the interest you are saving. T. Rowe Price's analysis found that using a lump sum to pay off a mortgage at retirement left one couple with a portfolio $190,000 lower after seven years compared with keeping the mortgage and investing normally. The better question is whether your mortgage rate exceeds your expected after-tax return on the next best use of that money. If it does, pay it off. If it does not, continue regular payments and invest the difference. Consult a fee-only financial advisor for your specific numbers.At what age should I claim Social Security?

The optimal age to claim Social Security depends on your health, your other income sources, your marital status, and whether you need the income immediately. The mechanics are clear: claiming at 62 (the earliest age) permanently reduces your monthly benefit by up to 30% compared with claiming at Full Retirement Age. Every year you delay past Full Retirement Age adds approximately 8% to your monthly benefit, up to age 70. The breakeven age — where delaying has paid back more than the forgone early payments — is typically around 82. For anyone in good health who can manage financially without claiming early, delaying to at least FRA and ideally to 70 produces significantly higher lifetime income. The Social Security Administration's 'my Social Security' portal at ssa.gov provides personalised projections at every claiming age.How much should I have in cash vs invested as I approach retirement?

The general guidance from financial planners is to maintain three to six months of living expenses in a liquid cash account (high-yield savings account or money market fund) as an emergency reserve. Beyond that amount, money held in cash earns below-inflation returns over most time periods and slowly loses purchasing power. Additional savings should be invested in a mix appropriate to your age and risk tolerance — most financial advisors recommend maintaining meaningful equity exposure (40-60% in equities) even into early retirement, because a retirement that lasts 25-30 years requires portfolio growth to outpace inflation and healthcare cost increases. Moving entirely to cash and bonds at 65 creates a different kind of risk than market volatility: the risk of running out of money.Is it really a mistake to help my adult children financially?

Helping your children is not inherently a mistake — the issue is the source of the help. Providing assistance from current income, non-retirement savings, or non-cash support (time, advice, shared housing, childcare) does not compromise your retirement security. Drawing down retirement accounts, stopping contributions during the high-catch-up years after age 50, or cosigning debt that affects your own creditworthiness can permanently compromise your retirement in ways that cannot later be corrected. The key principle is that your children have access to mechanisms you do not — student loans, time to build wealth, decades of future earning. You cannot borrow for your retirement, and you cannot work back lost compounding years in your 50s once they are gone.Will Social Security really disappear if the trust fund runs dry?

No — and this is one of the most consequential financial misconceptions in America. Cornell University research found that 64% of people who see projections of the trust fund's depletion assume benefits will disappear entirely. This is incorrect. Even if the Social Security trust fund is depleted — projected as early as 2032-2035 under current trajectories — ongoing payroll tax revenue would continue flowing into the system. Under most projections, this revenue would fund approximately 75-80% of scheduled benefits indefinitely. A cut would be serious; a complete elimination is not the projected outcome. Claiming early from fear of total elimination is a decision that trades a permanent, certain 30% reduction in benefits for protection against a scenario that, in its catastrophic form, is not actually projected to occur.External References & Further Reading

The following authoritative sources were used in researching this article and are recommended for further reading:1. Northwestern Mutual — 2026 Planning & Progress Study: Retirement Savings and Expectations

https://news.northwesternmutual.com/planning-and-progress-2026

2. T. Rowe Price — Should I Pay Off My Mortgage Before I Retire? (May 2025)

https://www.troweprice.com/personal-investing/resources/insights/should-i-pay-off-my-mortgage-before-i-retire.html

3. Bankrate — Should I Pay Off My Mortgage or Invest? (Updated January 2026)

https://www.bankrate.com/mortgages/pay-off-mortgage-or-invest/

4. Farther.com — Social Security Mistakes to Avoid in 2026

https://www.farther.com/foundations/social-security-mistakes-to-avoid-in-2026

5. The Motley Fool — The 5 Biggest Social Security Mistakes Retirees Make (April 2026)

https://www.fool.com/retirement/2026/04/26/the-5-biggest-social-security-mistakes-retirees-ma/

6. 24/7 Wall St. — 64% of Americans Are Making a Fundamental Social Security Mistake (April 2026)

https://247wallst.com/investing/2026/04/01/64-of-americans-are-making-a-fundamental-mistake-on-social-security/

7. Kiplinger — 16 Retirement Mistakes That Could Haunt Your Golden Years (2026)

https://www.kiplinger.com/slideshow/retirement/t047-s001-retirement-mistakes-you-will-regret-forever/index.html

8. Ameriprise Financial — Should You Pay Off Your Mortgage or Invest?

https://www.ameriprise.com/financial-goals-priorities/personal-finance/should-you-pay-off-your-mortgage

0 Comments Comments