Retirement

UK New ISA and Lifetime ISA Changes Explained 2026

Table of Contents

UK savers are facing the most significant set of changes to the Individual Savings Account (ISA) system in over a decade. Following confirmation in the Autumn Budget 2025, the Treasury published detailed technical specifications on 23 June 2026 covering two major reforms: a reduction in the tax-free Cash ISA allowance for under-65s, alongside a new charge on cash held within investment ISAs, and a consultation on a brand new First-Time Buyer ISA designed to eventually replace the Lifetime ISA (LISA) entirely.

For the roughly 1.3 million people who currently hold a Lifetime ISA, and the millions more who rely on Cash ISAs as their primary tax-free savings vehicle, these changes carry genuine financial consequences that require active decisions in the months ahead. None of the changes take effect immediately — the current £20,000 overall ISA allowance remains fully in place for the 2026/27 tax year — but the direction of travel is now confirmed, and the window to act on the current, more generous rules is finite.

This guide explains exactly what is changing, when each change takes effect, who is affected, and what you should consider doing now while the existing rules remain available. Given how quickly this story has developed — final technical detail was only published this week — this guide reflects the most current confirmed government position as of late June 2026.

Separately, the Treasury Select Committee's 2025 review of the Lifetime ISA concluded that its dual purpose — serving simultaneously as a first-time buyer savings vehicle and an informal retirement product — was fundamentally confusing for savers and frequently led to poor outcomes, particularly around the 25% early withdrawal penalty, which many savers misunderstood until they were actually charged it. Committee Chair Dame Meg Hillier argued that two separate, properly tailored products would serve savers far better than one product trying to do both jobs at once.

Martin Lewis's view: Consumer finance campaigner Martin Lewis has been a vocal commentator throughout this process, arguing the policy goal of encouraging investment is reasonable but that the Government should have used a 'carrot, not a stick' approach rather than cutting the Cash ISA allowance to force behaviour change. He successfully campaigned for older savers to be exempted from the reduced limit, and the Treasury's 23 June 2026 announcement confirmed that anyone aged 65 or over keeps the full £20,000 Cash ISA allowance.

Current overall ISA allowance, 2026/27 tax year: £20,000 — unchanged — savers of any age can still place the full £20,000 into any combination of ISA types this tax year, including up to the full amount in a Cash ISA if under 65 (HM Treasury, June 2026)

Crucially, this is a forward-looking change only. Cash ISA balances built up before April 2027 are entirely unaffected by the new cap; only new subscriptions from that date onward are subject to the reduced £12,000 limit. This means the 2026/27 tax year (running to 5 April 2027) represents the final opportunity for under-65 savers to place the full £20,000 allowance into cash if they wish to do so.

This rule exists specifically to close a loophole the lower Cash ISA limit would otherwise create: without it, a saver could simply hold cash inside a Stocks & Shares ISA wrapper instead of a dedicated Cash ISA, sidestepping the new £12,000 cap entirely while still earning tax-free interest. HMRC has been explicit that the new charge is designed to 'minimise the opportunity for the lower cash ISA limit to be circumvented, while preserving the flexibility needed for legitimate investment activity within non-cash ISAs.'

Consumer advocates, including Martin Lewis, have specifically flagged the practical difficulty this creates for savers who deliberately drip-feed money into investments gradually, a widely recommended strategy for managing market timing risk known as pound-cost averaging. Cash awaiting investment, sitting in a Stocks & Shares ISA even briefly, will now generate a tax liability on any interest earned during that holding period — a meaningful behavioural disincentive for an investing approach many financial advisers otherwise actively recommend.

The proposed new product strips out the retirement-saving function entirely, focusing solely on helping first-time buyers save for a home deposit — directly addressing the Treasury Select Committee's criticism that the LISA's dual purpose created confusing and sometimes poor outcomes for savers who treated it primarily as a retirement vehicle, only to discover the harsh 25% penalty applied to non-qualifying withdrawals.

Lifetime ISA holders currently: ~1.3 million people — all of whom can continue saving into their existing LISA under the current rules indefinitely, regardless of when or whether the new First-Time Buyer ISA is eventually introduced (HM Treasury, June 2026)

This is not a minor administrative difference. A saver contributing consistently over several years loses the compounding benefit of receiving and growing that bonus throughout the saving period, rather than only at the end. For a long-term saver, particularly one investing rather than holding cash, this could meaningfully reduce the total value built up compared to the current monthly-bonus LISA structure, even before accounting for the removal of the early withdrawal penalty.

For most savers, the most important immediate takeaway is that nothing changes for the remainder of the current tax year: the full £20,000 ISA allowance remains available to everyone, in whatever combination of cash and investments suits their needs, and existing Lifetime ISA holders face no cut-off or forced migration to a new product. The window to make full use of the current, more generous Cash ISA rules and the existing LISA structure closes in April 2027 and April 2028 respectively — providing a clear, finite period in which to plan and act rather than an immediate emergency requiring rushed decisions.

Given how recently the full technical detail was published — much of it within the past week — this is an area worth continuing to monitor closely. The consultation on the First-Time Buyer ISA remains genuinely open, the final design details for property price caps and contribution limits have not yet been settled, and further announcements are likely as the Government works toward the planned 2028 implementation. Reviewing your own ISA strategy now, with a clear understanding of exactly what is and is not changing, is the most useful action any UK saver can take in response to this reform package.

1. GOV.UK — Tax Update 2026: Simplification, Modernisation and Fairness Summary

https://www.gov.uk/government/publications/summary-of-tax-update-2026-simplification-modernisation-and-fairness/tax-update-2026-simplification-modernisation-and-fairness-summary

2. HM Treasury — First-Time Buyer ISA: Consultation (Published 22 June 2026)

https://www.gov.uk/government/consultations

3. HMRC — ISA Reform 2027: Anti-Circumvention Rules Factsheet (23 June 2026)

https://www.gov.uk/government/publications

4. MoneySavingExpert — Cash and Investment ISA Reforms Explained (June 2026)

https://www.moneysavingexpert.com/news/2026/06/cash-investment-isa-reforms/

5. UK Parliament Treasury Committee — Lifetime ISA Report and Reform Statement

https://committees.parliament.uk/committee/158/treasury-committee/news/210678/lifetime-isa-reform-welcomed-by-chair/

6. St. James's Place — ISA Changes: 22% Charge on Cash in Investment ISAs

https://www.sjp.co.uk/individuals/news/isa-changes-22-charge-on-cash-in-investment-isas-plus-simpler-first-time-buyer-isa

7. GOV.UK — Individual Savings Accounts (ISA) Official Guidance

https://www.gov.uk/individual-savings-accounts

8. GOV.UK — Lifetime ISA Official Guidance

https://www.gov.uk/lifetime-isa

- The Big Picture: Why ISAs Are Being Reformed

- The Full Timeline: Key Dates You Need to Know

- What's Changing: The Cash ISA Allowance Cut

- The Over-65 Exemption

- Transfer Restrictions From 2027

- What's Changing: The New 22% Charge on Cash Held in Investment ISAs

- What's Changing: The Lifetime ISA Will Be Replaced by a First-Time Buyer ISA

- What Happens to Your Existing Lifetime ISA?

- The Bonus Payment Timing Change

- Removal of the Upper Age Limit

- Removal of the Withdrawal Penalty

- What You Should Consider Doing Now

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

UK savers are facing the most significant set of changes to the Individual Savings Account (ISA) system in over a decade. Following confirmation in the Autumn Budget 2025, the Treasury published detailed technical specifications on 23 June 2026 covering two major reforms: a reduction in the tax-free Cash ISA allowance for under-65s, alongside a new charge on cash held within investment ISAs, and a consultation on a brand new First-Time Buyer ISA designed to eventually replace the Lifetime ISA (LISA) entirely.

For the roughly 1.3 million people who currently hold a Lifetime ISA, and the millions more who rely on Cash ISAs as their primary tax-free savings vehicle, these changes carry genuine financial consequences that require active decisions in the months ahead. None of the changes take effect immediately — the current £20,000 overall ISA allowance remains fully in place for the 2026/27 tax year — but the direction of travel is now confirmed, and the window to act on the current, more generous rules is finite.

This guide explains exactly what is changing, when each change takes effect, who is affected, and what you should consider doing now while the existing rules remain available. Given how quickly this story has developed — final technical detail was only published this week — this guide reflects the most current confirmed government position as of late June 2026.

The Big Picture: Why ISAs Are Being Reformed

The reforms stem from a long-running government concern that the UK has a culture of holding too much household wealth in cash rather than in productive, growth-generating investments. The Treasury's stated aim, set out alongside the Autumn Budget 2025 and reaffirmed in the June 2026 technical announcements, is to nudge savers — particularly younger savers — toward Stocks & Shares ISAs and other investment vehicles, in the hope of building a stronger UK retail investment culture and channelling more household savings into the economy.Separately, the Treasury Select Committee's 2025 review of the Lifetime ISA concluded that its dual purpose — serving simultaneously as a first-time buyer savings vehicle and an informal retirement product — was fundamentally confusing for savers and frequently led to poor outcomes, particularly around the 25% early withdrawal penalty, which many savers misunderstood until they were actually charged it. Committee Chair Dame Meg Hillier argued that two separate, properly tailored products would serve savers far better than one product trying to do both jobs at once.

Martin Lewis's view: Consumer finance campaigner Martin Lewis has been a vocal commentator throughout this process, arguing the policy goal of encouraging investment is reasonable but that the Government should have used a 'carrot, not a stick' approach rather than cutting the Cash ISA allowance to force behaviour change. He successfully campaigned for older savers to be exempted from the reduced limit, and the Treasury's 23 June 2026 announcement confirmed that anyone aged 65 or over keeps the full £20,000 Cash ISA allowance.

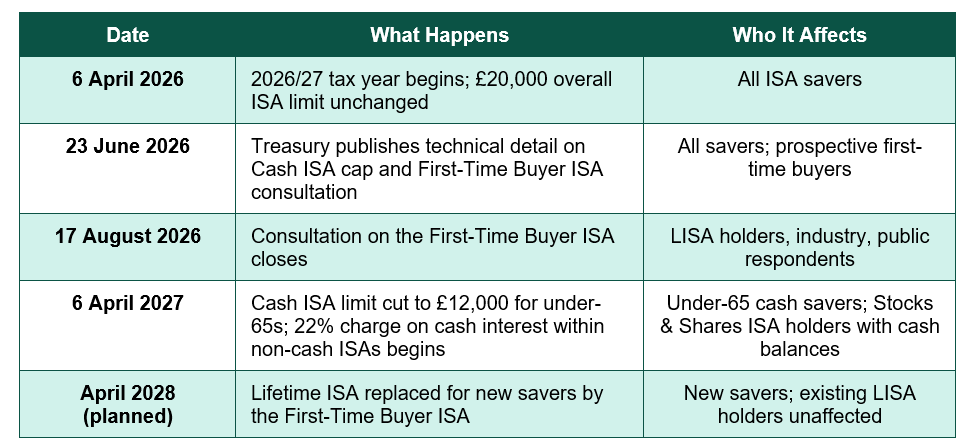

The Full Timeline: Key Dates You Need to Know

The reforms are being introduced in stages, not all at once. The table below sets out every confirmed date in the process so far:Current overall ISA allowance, 2026/27 tax year: £20,000 — unchanged — savers of any age can still place the full £20,000 into any combination of ISA types this tax year, including up to the full amount in a Cash ISA if under 65 (HM Treasury, June 2026)

What's Changing: The Cash ISA Allowance Cut

From 6 April 2027, savers under the age of 65 will only be able to subscribe up to £12,000 of their overall £20,000 ISA allowance into a Cash ISA each tax year, down from the current £20,000. The remaining £8,000 of allowance must be placed into a non-cash ISA — typically a Stocks & Shares ISA, though Innovative Finance ISAs also qualify — if the saver wishes to use their full annual allowance.Crucially, this is a forward-looking change only. Cash ISA balances built up before April 2027 are entirely unaffected by the new cap; only new subscriptions from that date onward are subject to the reduced £12,000 limit. This means the 2026/27 tax year (running to 5 April 2027) represents the final opportunity for under-65 savers to place the full £20,000 allowance into cash if they wish to do so.

The Over-65 Exemption

Following sustained pressure from consumer campaigners including Martin Lewis, the Treasury confirmed that savers aged 65 and over will retain the full £20,000 Cash ISA allowance, with no requirement to allocate any portion to non-cash investments. This exemption begins from the start of the tax year in which a saver turns 65, providing a clear and reasonably generous transition point for those approaching that age.Transfer Restrictions From 2027

To prevent savers from circumventing the new cash limit, the rules tighten transfers between ISA types from April 2027. Under-65s will no longer be permitted to transfer funds from a Stocks & Shares ISA or Innovative Finance ISA into a Cash ISA. However, transfers in the opposite direction — moving money from a Cash ISA into a Stocks & Shares ISA — will remain fully permitted, reflecting the Government's clear policy preference for nudging savings toward investment rather than away from it.What's Changing: The New 22% Charge on Cash Held in Investment ISAs

Perhaps the most technically significant — and most criticised — element of the June 2026 announcement is a new flat 22% charge that will apply to interest earned on cash balances held within non-cash ISAs, such as Stocks & Shares ISAs and Innovative Finance ISAs, from April 2027.This rule exists specifically to close a loophole the lower Cash ISA limit would otherwise create: without it, a saver could simply hold cash inside a Stocks & Shares ISA wrapper instead of a dedicated Cash ISA, sidestepping the new £12,000 cap entirely while still earning tax-free interest. HMRC has been explicit that the new charge is designed to 'minimise the opportunity for the lower cash ISA limit to be circumvented, while preserving the flexibility needed for legitimate investment activity within non-cash ISAs.'

- Who this catches, and why it matters: The 22% charge applies universally to all ISA holders regardless of age or income tax bracket — including non-taxpayers, and including savers aged 65 and over who are otherwise exempt from the lower Cash ISA cap. Money market funds held within a Stocks & Shares ISA will not be classified as cash for this purpose, and so will not attract the charge, provided they do not make up the entirety of the ISA's holdings — a detail that gives sophisticated savers a partial workaround, but one that requires active management rather than simply leaving uninvested cash sitting in the account between trades.

Consumer advocates, including Martin Lewis, have specifically flagged the practical difficulty this creates for savers who deliberately drip-feed money into investments gradually, a widely recommended strategy for managing market timing risk known as pound-cost averaging. Cash awaiting investment, sitting in a Stocks & Shares ISA even briefly, will now generate a tax liability on any interest earned during that holding period — a meaningful behavioural disincentive for an investing approach many financial advisers otherwise actively recommend.

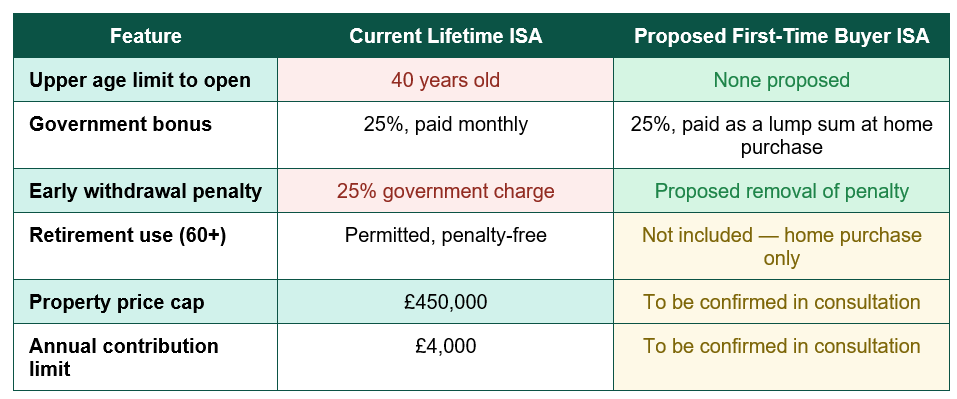

What's Changing: The Lifetime ISA Will Be Replaced by a First-Time Buyer ISA

The second major strand of reform addresses the Lifetime ISA directly. The Government has confirmed that a new, simpler First-Time Buyer ISA will eventually replace the LISA for new savers, expected from around April 2028, following the consultation that opened on 23 June 2026 and closes on 17 August 2026.The proposed new product strips out the retirement-saving function entirely, focusing solely on helping first-time buyers save for a home deposit — directly addressing the Treasury Select Committee's criticism that the LISA's dual purpose created confusing and sometimes poor outcomes for savers who treated it primarily as a retirement vehicle, only to discover the harsh 25% penalty applied to non-qualifying withdrawals.

What Happens to Your Existing Lifetime ISA?

This is the detail causing the most concern, and the Government's messaging on it has been consistent and reassuring: there is no cut-off date for the existing Lifetime ISA. Anyone who already holds a LISA, or who opens a new one before the replacement product becomes available, can continue contributing under the current rules indefinitely — both before and after the new First-Time Buyer ISA launches. The 25% government bonus, the £4,000 annual contribution limit, and the existing withdrawal rules will continue to apply to existing LISAs exactly as they do today, with no forced migration to the new product.Lifetime ISA holders currently: ~1.3 million people — all of whom can continue saving into their existing LISA under the current rules indefinitely, regardless of when or whether the new First-Time Buyer ISA is eventually introduced (HM Treasury, June 2026)

The Bonus Payment Timing Change

One of the most consequential design differences in the proposed new product is how the government bonus is paid. The current Lifetime ISA pays its 25% bonus monthly, meaning the bonus itself begins earning investment growth or interest immediately, compounding over the years a saver contributes. The proposed First-Time Buyer ISA would instead pay the entire 25% bonus as a single lump sum only at the point of completing a qualifying home purchase.This is not a minor administrative difference. A saver contributing consistently over several years loses the compounding benefit of receiving and growing that bonus throughout the saving period, rather than only at the end. For a long-term saver, particularly one investing rather than holding cash, this could meaningfully reduce the total value built up compared to the current monthly-bonus LISA structure, even before accounting for the removal of the early withdrawal penalty.

Removal of the Upper Age Limit

The current Lifetime ISA cannot be opened by anyone over the age of 40, a restriction that has drawn increasing criticism as the average age of first-time buyers has risen well into the early thirties and beyond. The proposed First-Time Buyer ISA would have no upper age limit at all, reflecting the reality that saving for a first home deposit increasingly extends into a buyer's late thirties or forties, particularly in higher-cost regions.Removal of the Withdrawal Penalty

The current 25% early withdrawal penalty on a Lifetime ISA — charged when funds are withdrawn for any purpose other than a qualifying first home purchase or after age 60 — has been one of the product's most criticised features, since it can leave savers with less than they originally contributed if they are forced to withdraw in an emergency. The proposed First-Time Buyer ISA aims to remove this penalty entirely, a change that, if implemented as proposed, would represent a genuine improvement in flexibility and saver protection compared to the current product.What You Should Consider Doing Now

With the direction of these reforms now confirmed, savers have a genuine window to make informed decisions while the current, more generous rules remain in place:- Use your full Cash ISA allowance this tax year if cash suits your needs: If you are under 65 and prioritise capital security — for an emergency fund, a near-term house deposit, or simply a lower risk tolerance — the 2026/27 tax year is your last opportunity to place the full £20,000 into a Cash ISA before the £12,000 cap applies from April 2027.

- Open a Lifetime ISA now if you are eligible and have not already done so: If you are under 40 and saving toward a first home or considering the retirement-savings flexibility the LISA currently offers, opening one now locks in access to the current rules — including the monthly bonus payment structure and the ability to use it for retirement from age 60 — for as long as you wish, with no forced transition to the new product.

- Reconsider holding cash inside a Stocks & Shares ISA from 2027: If you currently hold meaningful cash balances within an investment ISA, for example awaiting deployment into the market, review whether a money market fund structure (which avoids the new 22% charge, provided it does not make up the entire ISA) better suits your needs once the rules change, or whether moving genuinely uninvested cash to a dedicated Cash ISA before April 2027 makes more sense.

- Respond to the consultation if you have a view: The consultation on the new First-Time Buyer ISA remains open until 17 August 2026. Savers, particularly existing LISA holders, are explicitly invited to submit views on the technical design, including the bonus payment timing and the proposed property price cap, before the final product design is settled.

- Avoid panic-driven decisions based on headlines alone: None of these changes affect existing ISA balances retrospectively, and the Lifetime ISA is not disappearing for current holders. Take time to understand exactly which changes apply to your specific circumstances — your age, your existing ISA holdings, and your savings goals — before making any significant changes to your savings strategy.

Conclusion

The UK's ISA system is undergoing its most significant restructuring in years, driven by a clear government policy goal of shifting household savings away from cash and toward investment, and by a long-standing recognition that the Lifetime ISA's dual purpose was creating confusing and sometimes costly outcomes for savers. The headline changes — a reduced Cash ISA allowance for under-65s from 2027, a new 22% charge on cash held within investment ISAs, and the eventual replacement of the Lifetime ISA with a more focused First-Time Buyer ISA — are now confirmed in their broad shape, even though some technical details remain subject to the consultation closing in August 2026.For most savers, the most important immediate takeaway is that nothing changes for the remainder of the current tax year: the full £20,000 ISA allowance remains available to everyone, in whatever combination of cash and investments suits their needs, and existing Lifetime ISA holders face no cut-off or forced migration to a new product. The window to make full use of the current, more generous Cash ISA rules and the existing LISA structure closes in April 2027 and April 2028 respectively — providing a clear, finite period in which to plan and act rather than an immediate emergency requiring rushed decisions.

Given how recently the full technical detail was published — much of it within the past week — this is an area worth continuing to monitor closely. The consultation on the First-Time Buyer ISA remains genuinely open, the final design details for property price caps and contribution limits have not yet been settled, and further announcements are likely as the Government works toward the planned 2028 implementation. Reviewing your own ISA strategy now, with a clear understanding of exactly what is and is not changing, is the most useful action any UK saver can take in response to this reform package.

Frequently Asked Questions (FAQ)

Will I lose any money I've already saved in my Cash ISA or Lifetime ISA?

No. None of the confirmed changes affect existing ISA balances retrospectively. The reduced £12,000 Cash ISA limit only applies to new subscriptions made from April 2027 onward — money already saved in a Cash ISA before that date is completely unaffected. Similarly, existing Lifetime ISA holders can continue contributing under the current rules indefinitely, with no forced transition to the new First-Time Buyer ISA when it eventually launches.Can I still open a new Lifetime ISA, and should I?

Yes, you can still open a new Lifetime ISA if you are between 18 and 39 years old, and there is currently no announced cut-off date for doing so before the new First-Time Buyer ISA becomes available, expected around April 2028. Whether you should depends on your circumstances: if you are eligible and saving toward a first home or want the retirement-use flexibility the current LISA offers, opening one now secures access to the existing rules, including the monthly bonus payment structure, for as long as you continue to hold and contribute to the account.Does the 22% cash charge apply to me if I'm over 65?

Yes. The 22% charge on interest earned on cash held within non-cash ISAs (such as Stocks & Shares ISAs) applies to all ISA holders regardless of age, including those aged 65 and over who are otherwise exempt from the reduced Cash ISA contribution limit. The over-65 exemption only relates to the £12,000 versus £20,000 Cash ISA subscription cap, not to this separate charge on cash interest within investment ISAs.What happens if I want to drip-feed cash into my Stocks & Shares ISA over time?

From April 2027, any interest earned on cash sitting in your Stocks & Shares ISA while awaiting investment will be subject to the new 22% charge. One potential workaround is holding that cash in a money market fund within the ISA rather than as plain cash, since money market funds are not classified as cash for this purpose, provided they do not constitute the entire holding within the ISA. This is a more active management approach than simply leaving cash uninvested, and you should consider discussing the best approach for your specific situation with a regulated financial adviser.When exactly will the Lifetime ISA stop being available to new savers?

The Government's current plan is for the new First-Time Buyer ISA to become available from around April 2028, at which point it would be offered in place of the Lifetime ISA for new savers opening an account for the first time. This date is not yet finalised in legislation and remains subject to the consultation process, which closes on 17 August 2026, and the subsequent legislative timetable. Existing LISA holders are unaffected by this date and can continue contributing to their accounts under the current rules regardless of when the new product launches.External References & Further Reading

The following official and authoritative sources were used in researching this article and are recommended for further reading:1. GOV.UK — Tax Update 2026: Simplification, Modernisation and Fairness Summary

https://www.gov.uk/government/publications/summary-of-tax-update-2026-simplification-modernisation-and-fairness/tax-update-2026-simplification-modernisation-and-fairness-summary

2. HM Treasury — First-Time Buyer ISA: Consultation (Published 22 June 2026)

https://www.gov.uk/government/consultations

3. HMRC — ISA Reform 2027: Anti-Circumvention Rules Factsheet (23 June 2026)

https://www.gov.uk/government/publications

4. MoneySavingExpert — Cash and Investment ISA Reforms Explained (June 2026)

https://www.moneysavingexpert.com/news/2026/06/cash-investment-isa-reforms/

5. UK Parliament Treasury Committee — Lifetime ISA Report and Reform Statement

https://committees.parliament.uk/committee/158/treasury-committee/news/210678/lifetime-isa-reform-welcomed-by-chair/

6. St. James's Place — ISA Changes: 22% Charge on Cash in Investment ISAs

https://www.sjp.co.uk/individuals/news/isa-changes-22-charge-on-cash-in-investment-isas-plus-simpler-first-time-buyer-isa

7. GOV.UK — Individual Savings Accounts (ISA) Official Guidance

https://www.gov.uk/individual-savings-accounts

8. GOV.UK — Lifetime ISA Official Guidance

https://www.gov.uk/lifetime-isa

0 Comments Comments