Budgeting

What Are Emergency Fund Tiers? Accountant Explains

Table of Contents

- The Financial Foundation Most People Are Missing

- What Is an Emergency Fund and Why Does It Matter?

- What Are Emergency Fund Tiers?

- The Three Emergency Fund Tiers: UK 2026 Complete Reference

- Tier 1: The Starter Fund (£500–£1,500)

- Tier 2: The Core Emergency Fund (1–3 Months of Essential Expenses)

- Calculating Your Tier 2 Target

- Tier 3: The Extended Resilience Fund (3–12 Months of Expenses)

- How Much Emergency Fund Do You Need? A UK Risk Profile Guide

- Where to Keep Your Emergency Fund in the UK in 2026

- Tier 1 Accounts (Instant Access)

- Tier 2 Accounts (1–2 Business Days)

- Tier 3 Accounts (3–90 Days)

- How to Build Your Emergency Fund: A Step-by-Step UK Plan

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Financial Foundation Most People Are Missing

The headline figure from Bankrate's January 2026 Emergency Savings Report is stark: 59% of adults cannot cover a £1,000 emergency expense without going into debt. Not a £10,000 catastrophe. A single thousand pounds. A boiler breakdown. A car repair. A dental emergency. For 59% of households, events like these immediately trigger credit card borrowing or personal loans at 22% APR or more — a single unexpected bill becoming the start of a debt cycle that takes months to resolve. More alarming still: 24% of adults have zero emergency savings. They live entirely without financial cushion, one unexpected expense away from genuine crisis.An emergency fund is the foundational layer of personal financial resilience — the non-negotiable first step before investing in stocks, paying down low-interest debt, or building any other financial goal. Without it, every financial plan is vulnerable to derailment by the completely ordinary unexpected events that life reliably produces: redundancy, illness, essential appliance failure, accident, relationship breakdown. Emergency savings are not an investment. They are insurance — the financial equivalent of a seatbelt that you hope never to need urgently.

Emergency fund tiers make this foundational goal manageable. Rather than facing the daunting prospect of accumulating six months' worth of living expenses from zero — which for many UK households represents £10,000 to £25,000 or more — the three-tier approach breaks the journey into distinct, purposeful stages. Each tier provides meaningful protection on the way to the next. This guide explains the complete three-tier framework, how much each tier should contain for different household profiles, the best UK accounts for each tier in 2026, how to build each tier in sequence, and the practical rules for maintaining, using, and replenishing your emergency fund over time.

What Is an Emergency Fund and Why Does It Matter?

An emergency fund is money held separately from your everyday accounts, earmarked exclusively for genuine unexpected emergencies — unexpected, unavoidable, and immediate expenses that cannot be deferred. District Capital Management's 2026 guide defines the purpose precisely: 'An emergency fund is money set aside for unexpected, unavoidable expenses. The purpose of an emergency fund is not to grow wealth or earn high returns. Its purpose is protection. It allows you to handle financial shocks without relying on credit cards, loans, or early withdrawals from long-term investments.'What constitutes a genuine emergency deserves careful attention. Many people deplete emergency funds on non-emergency spending, leaving themselves exposed when a genuine crisis arrives. True emergencies are all three of: unexpected (not predictable in advance), unavoidable (not discretionary), and immediate (not safely deferrable). They include: sudden redundancy or income loss, essential car repairs needed for commuting to work, emergency home repairs (burst pipes, structural failures, boiler breakdown in winter), genuine medical emergencies, and emergency family travel. They do not include: planned holidays, annual recurring costs (MOT, insurance renewal, Christmas), discretionary shopping, or investment opportunities. These belong in separate sinking funds — monthly savings pots set aside specifically for predictable costs.

The financial case for an emergency fund is clear. Without one, unexpected expenses are paid for with credit cards at 22%–30% APR, personal loans, or by raiding long-term investments — all of which cost more in interest or lost returns than keeping cash accessible. A £2,000 boiler replacement funded by credit card at 22% APR over 12 months costs approximately £250 in interest. The same £2,000 kept in a high-yield savings account at 4.5% AER earns approximately £90 per year — a cost of approximately £90 in opportunity cost versus equity investment, rather than a cost of £250 in interest. The emergency fund is not an opportunity cost. It is the cheapest possible insurance against the financial disruption of unexpected events.

The emergency savings crisis in 2026: 59% of adults cannot cover a £1,000 emergency without borrowing. 24% have no emergency savings at all. — Bankrate's Emergency Savings Report (January 2026, surveyed December 2025) and Empower's Safety Net Survey (June 2025, 2,200 adults) both confirm the scale of the savings gap. By age group: Gen Z (18-29) median emergency savings = just $400 (Empower). Adults 60+ are strongest: 71% have three months saved (Federal Reserve SHED, October 2025). The emergency savings gap is most acute among under-40s and lower-income households

What Are Emergency Fund Tiers?

Emergency fund tiers are a structured, layered approach that divides the total emergency savings target into three distinct stages — each with a specific size, purpose, and appropriate savings product for the speed of access and return it requires. The tier framework addresses the psychological barrier of the full emergency fund goal: most people find the prospect of saving six months' expenses at once so daunting that they do not start. By breaking the goal into three tiers, each stage is achievable and each stage provides meaningful protection on the way to the next.The framework is consistent across UK and US personal finance education in 2026. Smart Finance Tool's Emergency Fund Calculator — calibrated against HMRC, IRS, and FDIC benchmarks — articulates the sequencing: 'Before you invest a single pound in the stock market or pay down low-interest debt, you MUST have at least £1,000 as a starter safety net, followed by a full 3-6 month runway.' The tier system provides the roadmap from zero to that full runway, stage by stage.

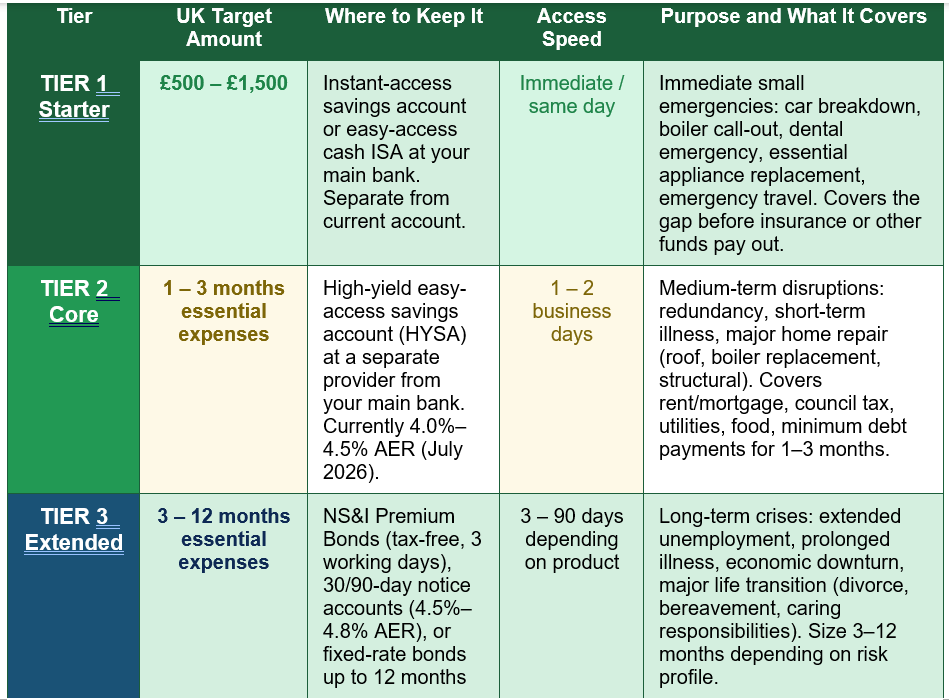

Three tiers are recognised across the personal finance literature: Tier 1 (the starter fund — immediate small emergencies, £500 to £1,500), Tier 2 (the core emergency fund — medium-term disruptions, 1 to 3 months of essential expenses), and Tier 3 (the extended resilience fund — long-term crises, 3 to 12 months of expenses). Each tier has a distinct target, a distinct purpose, and the most appropriate savings product for its specific speed-of-access and return requirements.

The Three Emergency Fund Tiers: UK 2026 Complete Reference

The table below maps all three tiers with UK-specific targets, appropriate account types at July 2026 rates, access speed, and the specific situations each covers:

Tier 1: The Starter Fund (£500–£1,500)

Tier 1 is the most urgently needed and the most achievable layer of the emergency fund structure — a small cash buffer held in an instantly accessible account, calibrated to handle the most common modest-but-damaging unexpected expenses. Meriwest's Emergency Funds 2.0 guide (October 2025) describes it as being for 'urgent, smaller expenses, like a car repair or a sudden medical bill. Aim for £1,000–£2,000, depending on your lifestyle. Choose an account with no fees and instant access.'The specific Tier 1 amount should reflect your most likely immediate emergency costs. A household with a car and a property to maintain should target £1,000 to £1,500 to cover the most common scenarios: an emergency boiler call-out (£200 to £500), a significant car repair (£400 to £1,200), or an urgent dental treatment (£200 to £600). Those who rent and use public transport can be comfortable with a £500 target. The key property of Tier 1 money is instant, frictionless access — same-day, at any hour, through your banking app. This rules out notice accounts, fixed bonds, and Premium Bonds (which take up to 3 working days).

Building Tier 1 takes priority over all other financial actions for anyone with zero or minimal savings. Smart Finance Tool's 2026 recommendation: 'Stop all extra debt payments and all stock market investing until your Tier 1 starter safety net is in place.' The logic is simple: a single £800 unexpected expense before Tier 1 is built results in credit card debt at 22% APR, instantly reversing any financial progress made elsewhere. Tier 1 is the firewall that protects all other financial goals from being disrupted by ordinary life.

Tier 2: The Core Emergency Fund (1–3 Months of Essential Expenses)

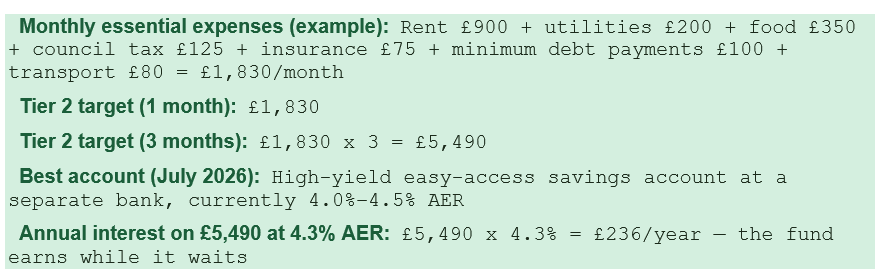

Tier 2 is the heart of the emergency fund framework — the amount that provides genuine medium-term financial protection against the most common serious disruptions. It covers one to three months of essential household expenses: rent or mortgage, council tax, utilities, food, insurance, and minimum debt payments. This is essential expenses only — not total spending. Discretionary spending (restaurants, subscriptions, clothing, entertainment) is naturally reduced during a crisis and should not inflate the Tier 2 calculation.Calculating Your Tier 2 Target

Tier 2 should be held at a different institution from your everyday banking. Meriwest's guide recommends keeping money at separate providers: 'Diversifying where you keep your money adds an extra layer of security. What if your bank has an outage, or you need funds while travelling?' If your main bank's systems are down during a genuine emergency, Tier 2 at a separate provider ensures you can still access funds within 1-2 business days. The 2026 UK market for high-yield easy-access savings is competitive: top rates from Chip, Atom Bank, and Chase UK were around 4.0%–4.5% AER in July 2026, against a national average savings rate of just 0.61% AER. On a £5,490 Tier 2 fund, the difference between 4.3% and 0.6% is approximately £200 per year for zero additional risk.

Tier 3: The Extended Resilience Fund (3–12 Months of Expenses)

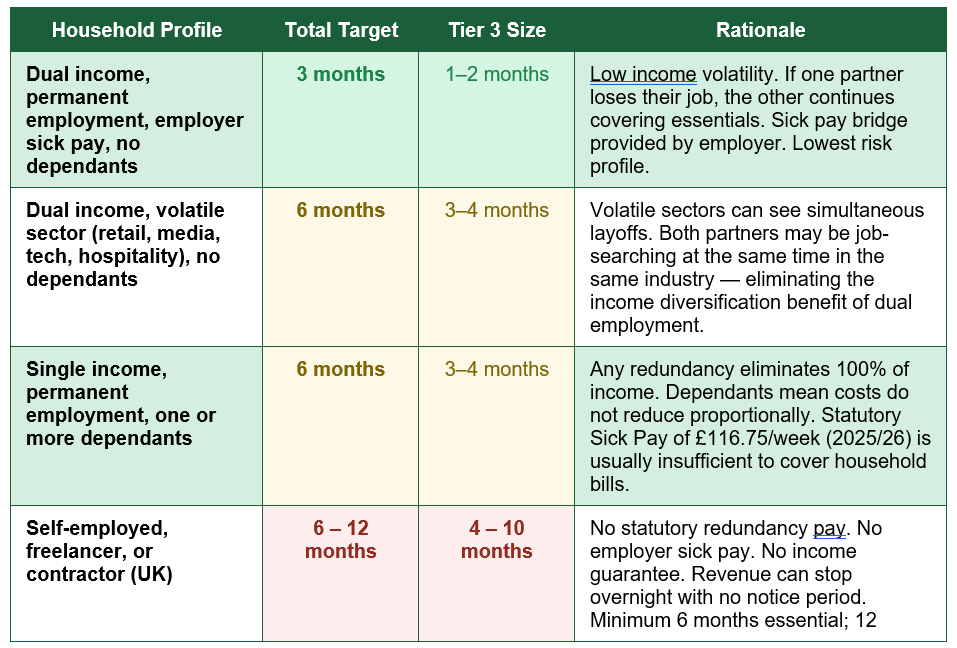

Tier 3 is the extended buffer for prolonged financial disruptions — situations where recovery takes months rather than weeks. Extended unemployment in a difficult job market, prolonged illness or injury, caring responsibilities, major economic downturns, and significant life transitions all belong in the Tier 3 planning horizon. The size of Tier 3 is the most variable component of the framework, determined primarily by your employment type, income sources, and household structure.Smart Finance Tool's risk-based sizing framework is the clearest available: government employees and tenured professionals target 3 months total; most employed households with some dependants target 6 months; commission-based salespeople, freelancers, and designers can 'lose income overnight' and should target 12 months minimum. FinanceWonk's 2026 guidelines map this to specific situations: 3 months for stable dual-income households with no dependants; 6 months for standard single-income or volatile sector employment; 12 months for the self-employed; up to 24 months for FIRE practitioners living on investment income.

Tier 3 money can earn slightly more than Tier 1 or 2 in exchange for slightly slower access, because Tier 3 scenarios typically allow days or weeks to liquidate. The best UK Tier 3 products in 2026: NS&I Premium Bonds (100% government-backed, prize fund equivalent ~4.4% tax-free, up to 3 working days access, up to £50,000 per person), 30-day notice savings accounts (approximately 4.5%–4.8% AER), and 1-year fixed-rate bonds (approximately 4.5%–5.0% AER) for the portion of Tier 3 you are very confident will not be needed within the year.

NS&I Premium Bonds as the UK Tier 3 product of choice: Premium Bonds are backed by HM Treasury — the only UK savings product with 100% government backing rather than FSCS protection up to a £85,000 limit. Their prize fund rate equivalent of approximately 4.4% (July 2026) is tax-free regardless of income, making them particularly attractive for higher-rate and additional-rate taxpayers who have used their Personal Savings Allowance. The maximum holding is £50,000 per person. Access takes up to 3 bank working days — entirely appropriate for Tier 3 scenarios where a few days' delay is acceptable. For Tier 3 money held specifically as financial insurance rather than investment, Premium Bonds offer a compelling combination of absolute government safety, tax-free return, and easy access.

How Much Emergency Fund Do You Need? A UK Risk Profile Guide

The right emergency fund target is not universal — it depends on income stability, household structure, employment type, and financial obligations. The table below maps common UK profiles to their recommended total fund size:

Where to Keep Your Emergency Fund in the UK in 2026

In 2026, the difference between the right and wrong savings account for an emergency fund is substantial. MyFinancialFreedomTracker's April 2026 analysis makes the cost explicit: a £10,000 emergency fund in an average current account at 0.39% APY earns £39 per year. The same fund in a top high-yield savings account at 4.5% AER earns £450 per year — £411 more for zero additional risk, zero effort, and no reduction in accessibility. Over five years without touching the fund, that difference compounds to over £2,000.Tier 1 Accounts (Instant Access)

- Easy-access savings accounts: Available from all UK banks and digital providers. Same-day withdrawal via bank transfer. Current top rates: 4.0%–4.5% AER (Chip, Atom Bank, Chase UK, July 2026). Prioritise accounts with no withdrawal limits and no notice requirement.

- Easy-access cash ISA: Same instant access. Interest entirely tax-free. Annual allowance £20,000. Particularly beneficial for higher earners who have used their Personal Savings Allowance (PSA: £1,000 for basic rate taxpayers, £500 for higher rate).

Tier 2 Accounts (1–2 Business Days)

- High-yield easy-access account at a separate provider: Current top rates 4.0%–4.5% AER. FSCS-protected up to £85,000 per person per institution. Being at a different bank from your main account provides resilience against bank outages.

- Cash ISA from a separate provider: Tax-free interest, same easy-access availability, contributes to the same £20,000 annual allowance. Good choice if approaching the PSA limit on taxable savings.

Tier 3 Accounts (3–90 Days)

- NS&I Premium Bonds: Government-backed (100%), tax-free prizes, prize fund rate equivalent ~4.4% (July 2026). Access within 3 working days. Maximum £50,000 per person. Best for tax-efficiency and absolute safety.

- 30-day or 90-day notice savings accounts: Currently 4.5%–4.8% AER for top accounts. Slightly higher rate than easy-access in exchange for giving notice before withdrawal. Only suitable for Tier 3 — too slow for Tier 1 or 2 emergencies.

- 1-year fixed-rate bonds: Currently 4.5%–5.0% AER. Only appropriate for the portion of Tier 3 you are very confident will not be needed within the fixed term. Early withdrawal penalties vary significantly by provider.

THE RATE-SWITCHING OPPORTUNITY: Check your emergency savings rate every six months. The UK savings market in 2026 is competitive but variable — the best easy-access rate changes regularly as providers adjust to the Bank Rate environment. Set a calendar reminder every April and October to compare your current rate against the market using MoneySuperMarket or MoneySavingExpert. Switching a £10,000 emergency fund from 0.6% to 4.5% AER takes 15 minutes and earns approximately £400 more per year.

How to Build Your Emergency Fund: A Step-by-Step UK Plan

The tier framework works because each stage provides meaningful protection on the way to the next. Building in sequence means you are never fully unprotected while working toward the larger goal:- Open a dedicated easy-access savings account immediately: If you have no emergency savings, open a separate easy-access savings account today — not your current account. Name it 'Emergency Fund' or 'Tier 1'. The psychological separation from your everyday spending account is important. Set up a standing order from payday.

- Build Tier 1 to £500: Make this your first and only financial goal. Pause any extra debt repayment above minimums. Pause additional investing beyond the employer pension match. Direct every spare pound to this £500 target. Most households can reach this within 4 to 8 weeks with deliberate effort.

- Build Tier 1 to your full starter target (£500–£1,500): Once £500 is secured, continue to your personalised Tier 1 target based on your most likely small emergency costs. Keep this money completely separate and touch it only for genuine emergencies.

- Begin Tier 2 while managing high-interest debt: Once Tier 1 is complete, open a separate high-yield easy-access account at a different bank for Tier 2. Split money between Tier 2 saving and aggressively clearing high-interest debt (credit cards above 10% APR). Low-interest debt can be managed more gradually once Tier 2 is funded.

- Complete Tier 2 and begin Tier 3: Once Tier 2 is fully funded, begin Tier 3 in NS&I Premium Bonds or a notice account. Use windfalls — tax refunds, bonuses, HMRC rebates, overtime — to accelerate Tier 3 rather than spending them. Once Tier 3 is fully funded, redirect savings into investments, pensions, and debt repayment.

- Review annually and after major life changes: Your essential expenses change — with a new mortgage, a baby, a change in employment, or a pay rise. Review your targets each April (start of the new tax year) and immediately after any major life change. Inflation means the nominal amount needed for a given number of months of expenses also increases over time.

WHAT COUNTS AS A GENUINE EMERGENCY: A common and costly mistake is using the emergency fund for non-emergency expenses. Genuine emergencies are unexpected, unavoidable, and immediate. A sale on flights is not an emergency. Christmas is not an emergency — it happens every December and should have its own sinking fund. Annual car insurance renewal is not an emergency. If the emergency fund is used, make replenishing it the top financial priority — before any additional investing, extra debt repayment, or discretionary spending. Smart Finance Tool's 2026 guidance: 'Once the crisis passes, your number one financial priority must be replenishing the shield.' An empty emergency fund is the most financially vulnerable position available.

Conclusion

Emergency fund tiers transform one of the most important and most frequently neglected areas of personal finance into a manageable, sequential plan. The 2026 statistics confirm the scale of the need: 59% of adults cannot cover a £1,000 emergency without borrowing, and 24% have no emergency savings at all. The tier system addresses this not by demanding an immediate six-month buffer — which feels insurmountable to most people — but by building financial resilience in purposeful stages that each provide genuine protection.Tier 1 (£500 to £1,500, instant access) creates the firewall against the small unexpected costs that send unprepared households into credit card debt. Tier 2 (one to three months of essential expenses in a high-yield easy-access account) provides genuine medium-term protection against redundancy, illness, and major repairs. Tier 3 (three to twelve months depending on risk profile, in notice accounts, Premium Bonds, or short fixed bonds) provides the extended resilience needed for prolonged crises and major life transitions. Together, the three tiers represent financial security that allows you to make deliberate, considered decisions rather than panicked, reactive ones when life's inevitable disruptions arrive.

The right tier sizes depend on your risk profile: three months total for stable dual-income households in permanent employment; six months for single-income or volatile-sector households; six to twelve months for the self-employed; up to twenty-four months for those living on investment income. The right accounts for each tier are readily available in the UK in 2026, with top easy-access rates at 4.0%–4.5% AER meaning your emergency fund earns meaningfully while it waits. The best time to build your emergency fund was before your last emergency. The second-best time is now.

Frequently Asked Questions (FAQ)

What are emergency fund tiers?

Emergency fund tiers are a structured three-stage approach to building financial resilience. Tier 1 is a starter fund of £500 to £1,500 in an instant-access account, covering immediate small emergencies such as car repairs, emergency home call-outs, or dental treatment. Tier 2 is the core emergency fund covering one to three months of essential household expenses in a high-yield easy-access account, for medium-term disruptions like redundancy or illness. Tier 3 is the extended resilience fund covering three to twelve months of expenses in slightly less liquid but higher-yielding accounts such as notice savings or NS&I Premium Bonds, for prolonged crises including extended unemployment, major life transitions, or economic downturns. The tier structure makes an overwhelming financial goal achievable by providing meaningful protection at each stage of the build.How much should I have in my emergency fund in the UK in 2026?

The standard guidance for most UK households is three to six months of essential expenses — the unavoidable monthly costs including rent or mortgage, council tax, utilities, food, insurance, and minimum debt repayments, but not discretionary spending. The right amount depends on your personal risk profile. Stable dual-income households with employer sick pay and no dependants can manage with three months. Single-income households with dependants should target six months. The self-employed, freelancers, and contractors — who have no statutory redundancy pay and whose income can stop without notice — should target six to twelve months as a baseline. Those approaching financial independence or retirement should consider twelve to twenty-four months to protect against sequence-of-returns risk. Calculate your actual monthly essential expenses first, then multiply by your target number of months.Where should I keep my emergency fund in the UK?

The answer depends on the tier. Tier 1 money needs instant same-day access and belongs in an easy-access savings account at your main or a linked bank — top UK easy-access rates in July 2026 are 4.0%–4.5% AER. Tier 2 should be in a high-yield easy-access savings account at a separate financial institution from your main bank, providing both competitive interest (4.0%–4.5% AER) and resilience if your main bank has a system outage. Tier 3 can earn slightly more in NS&I Premium Bonds (government-backed, tax-free prizes at ~4.4% equivalent, up to 3 working days access), 30-day or 90-day notice accounts (4.5%–4.8% AER), or 1-year fixed-rate bonds (4.5%–5.0% AER) for the portion unlikely to be needed within the year. Never keep emergency funds in stocks and shares ISAs, pensions, or investment accounts where the value can fall precisely when you need the money most.Should I build an emergency fund or pay off debt first?

Build Tier 1 first — before extra debt repayment, before any additional investing. Without a Tier 1 starter fund, any unexpected expense immediately generates new debt at 22%+ APR, undoing any progress made on repayment. Once Tier 1 (£500 to £1,500) is funded, the right balance depends on the interest rate of your debt. For high-interest debt (credit cards above roughly 10% APR), split contributions between Tier 2 building and aggressive debt repayment simultaneously — the interest rate on the debt likely exceeds what the savings earn. Once high-interest debt is cleared, focus fully on completing Tier 2, then Tier 3. Low-interest debt (student loans, 0% finance) can wait until the full emergency fund is built, as the cost of carrying it is likely below what the savings earn. The employer pension match should always be captured throughout — it represents an immediate 100% return.How do I rebuild my emergency fund after I have used it?

Rebuilding after using an emergency fund follows the same sequence as building it initially, but with greater urgency because you are temporarily vulnerable. Immediately resume automated savings transfers to your Tier 1 account as the top financial priority, ahead of any extra investing or extra debt repayment. Use any available windfalls — tax refunds, HMRC rebates, bonuses, overtime — to accelerate the rebuild rather than spending them. Review whether the event that depleted the fund was truly unexpected and unavoidable, or whether it was a predictable cost that should have had its own sinking fund (for example, a recurring car maintenance cost should have its own monthly saving pot). Once Tier 1 is restored, return to rebuilding Tier 2, then Tier 3, in normal sequence. Smart Finance Tool's guidance: 'When a crisis hits, use the fund without guilt. That is what it is for. Once the crisis passes, replenishing the shield is your number one financial priority.'External References & Further Reading

1. Bankrate — Emergency Fund: What It Is and How to Start One (January 28, 2026 — 59% statistic and 24% zero savings)https://www.bankrate.com/banking/savings/starting-an-emergency-fund/

2. KaelTripton — UK Emergency Fund: How Much to Save, Where to Keep It and When to Use It (June 8, 2026)

https://www.kaeltripton.com/uk-emergency-fund-guide/

3. Smart Finance Tool — Emergency Fund Calculator: Job-Loss and Crisis Planning 2026 (April 18, 2026 — tier definitions and risk profiles)

https://smartfinancetool.com/tools/emergency-fund-calculator

4. Meriwest — Emergency Funds 2.0: Building Resilience Beyond the Basics (October 2025 — three-tier framework)

https://www.meriwest.com/our-story/blog/emergency-funds-20-building-resilience-beyond-basics

5. HeyCostrade — Emergency Fund Strategy 2026: Where to Park 3 to 6 Months of Expenses (May 23, 2026 — HYSA rates and T-bill ETFs)

https://www.heygotrade.com/en/blog/emergency-fund-strategy-2026-where-to-park-3-6-months-expenses/

6. Forbes — Are You Saving Enough for Emergencies? How You Compare by Age (1 month ago — SHED and Empower survey data by generation)

https://www.forbes.com/sites/investor-hub/article/median-emergency-savings-by-age/

7. District Capital Management — Emergency Fund: How Much Should I Save in 2026? (January 22, 2026)

https://districtcapitalmanagement.com/emergency-fund-how-much-should-i-save/

8. FinanceWonk — Emergency Fund Guidelines: 3 to 12 Months by Situation (2026 — FDIC APY data and risk-based sizing)

https://www.financewonk.com/references/emergency-fund-guidelines

0 Comments Comments