Credits

Best Premium Credit Cards for the US 2026: Full Guide

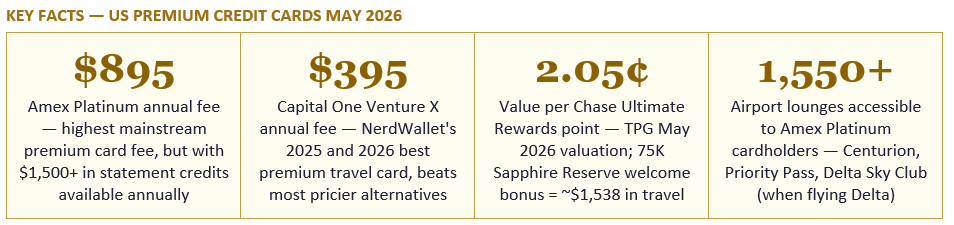

The best premium credit cards charge $95 to $895 per year — but for the right cardholder, each one returns significantly more value than it costs. The Capital One Venture X beats most $550+ cards at $395. The Chase Sapphire Reserve delivers over $3,000 in stated annual value. The Amex Platinum is the definitive luxury card but requires disciplined benefit use to justify $895. This is the honest, category-by-category guide to every top premium card for US consumers in May 2026.

Premium credit cards occupy the top tier of the US consumer credit market. They are distinguished not by their spending limits — plenty of no-fee cards have high limits — but by their benefit ecosystems: rich welcome bonuses worth hundreds or thousands of dollars in travel, annual statement credits that offset a significant portion of the fee, airport lounge access across thousands of locations worldwide, travel insurance protections that can cover tens of thousands of dollars in disruption losses, and concierge services that can arrange dining reservations or tickets to sold-out events.

The defining financial characteristic is the annual fee: premium cards charge anywhere from $95 (Chase Sapphire Preferred, the entry-level category) to $895 (American Express Platinum, the mainstream luxury ceiling) per year. Unlike a no-annual-fee card where any rewards are pure gain, a premium card requires its holder to earn back the annual fee through benefit usage before any profit begins. This break-even requirement is what makes premium cards genuinely worth it for some cardholders and genuinely not worth it for others — and the honest evaluation of which category you fall into is the core purpose of this guide.

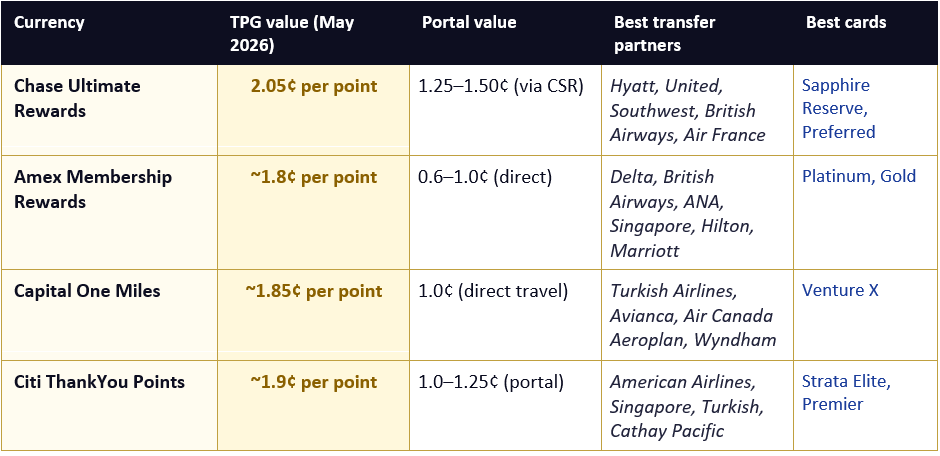

NerdWallet's 2026 premium card analysis, researching nearly 250 credit cards, identifies premium cards as 'typically aimed at higher-spending consumers with good to excellent credit,' and notes that 'it's important to make sure you will extract more value from the card than you pay.' The Points Guy's May 2026 valuation framework provides the most granular tool for making this calculation: by assigning a cents-per-point value to each major rewards currency (Chase Ultimate Rewards at 2.05 cents, Amex Membership Rewards at approximately 1.8 cents, Capital One miles at 1.85 cents), it enables direct comparison of reward earning potential across cards with different fees.

Despite its seemingly high $395 annual fee, it's easy to get a lot of value out of the Capital One Venture X. That's why it beat out an array of flashier, pricier cards to be the best premium travel credit card in both 2025 and 2026.

— NERDWALLET — BEST PREMIUM CREDIT CARDS MAY 2026

Two categories of benefits require special scrutiny in this calculation. Statement credits are the most straightforward: if a card offers a $300 annual travel credit and you spend at least $300 on travel each year, that credit effectively reduces the annual fee by $300. But many premium cards load their value into categories that require specific behaviour — $200 in airline incidental credits (only usable for baggage fees, not airfare), $200 in Uber Cash (only usable on Uber and Uber Eats), $120 in dining credits through a specific enrollment programme, $155 in Walmart+ credits. Each of these requires the cardholder to remember to enroll, to use the right payment method, and to actually spend in those specific categories. Cardholders who miss any of these credits are effectively paying a higher effective fee than the advertised one.

Lounge access is similarly variable in value. A frequent international traveller who uses airport lounges four times per month — a day pass to a comparable lounge typically costs $50 to $60 — generates $200 to $240 per month in lounge value, making lounge access worth $2,400 to $2,880 per year. An occasional domestic traveller who visits a lounge four times per year generates $200 to $240 annually. The same perk has very different values for different holders.

FinanceBuzz's 2026 guidance frames the qualifying question well: 'If you can comfortably earn the welcome bonus on a premium credit card without spending beyond your budget, that's a good sign you'll benefit from applying for one. But it's worth evaluating your past spending and calculating the value of different credit card point systems to choose the right one.'

Sources: NerdWallet (May 2026), CNN Underscored (May 2026), CNBC Select (May 2026), The Points Guy (May 2026 valuations). Annual fees, welcome offers, and benefits subject to change. Always verify current terms with card issuer before applying.

The core annual value proposition is straightforward. The $300 annual travel credit applies to any booking through Capital One Travel — including flights, hotels, and rental cars — making it broadly usable for most travellers. In addition, every card anniversary brings a 10,000-mile bonus worth $100 toward travel. Together, these two recurring benefits total $400 per year — meaning the Venture X generates positive net value before any consideration of rewards earned on spending, lounge access, or other benefits, simply by holding the card and using the $300 travel credit.

On top of this, the Venture X earns 10x miles on hotels and rental cars booked through Capital One Travel, 5x on flights through Capital One Travel, and 2x miles on every other purchase. With Capital One miles valued at approximately 1.85 cents per point by The Points Guy in May 2026, 2x miles on everyday spending equates to approximately 3.7% back in travel value — competitive with the best no-fee cards at a net effective cost of negative $5 (since the credits exceed the fee by $5).

The Venture X also includes Priority Pass airport lounge access for the primary cardholder and two guests, Global Entry or TSA PreCheck fee reimbursement, no foreign transaction fees, and a comprehensive travel insurance package. CNBC Select notes it as one of the best overall premium cards precisely because it delivers 'premium benefits without the premium price tag.'

The Reserve's $300 annual travel credit is the most broadly applicable of any premium card — it automatically applies to the first $300 of travel purchases charged to the card each year, with a broad definition of travel that includes airlines, hotels, rental cars, trains, Uber, Lyft, tolls, and parking. This effectively reduces the annual fee to $250 from the moment you spend $300 on any form of travel. Additionally, CNBC Select notes it offers 'more than $3,000 in annual value' when factoring in the $500 annual credit for stays at The EditSM by Chase Travel properties.

The Chase Ultimate Rewards currency — earning at 10x on Chase Travel purchases, 5x on flights, and 3x on dining and other travel — is valued by The Points Guy at 2.05 cents per point in May 2026, making it the most valuable major credit card currency in the US market. A 75,000-point welcome bonus is worth approximately $1,538 at that valuation — or $750 when redeemed at the straightforward 1.25 cents through the Chase travel portal.

The travel protections are best-in-class: trip cancellation and interruption insurance (up to $10,000 per person, $20,000 per trip), trip delay reimbursement ($500 per ticket for delays over six hours), primary rental car insurance (no need to decline the rental company's coverage), emergency medical and evacuation coverage ($100,000), and baggage delay insurance. For a frequent business traveller whose trips are sometimes disrupted, these protections can be worth substantially more than the annual fee in a single bad travel year.

The welcome offer is the most generous available in the premium card market: CNN Underscored notes cardholders 'may be eligible for as high as 175,000 Membership Rewards points after spending $12,000 in eligible purchases in the first 6 months.' This offer is not universal — it varies by applicant and channel — but at 1.8 cents per point, 175,000 points represent approximately $3,150 in travel value, making the first-year effective cost of the card negative even after the $895 fee.

The ongoing benefit suite includes access to over 1,550 airport lounges — the broadest of any consumer credit card — including Amex's own Centurion Lounges (widely considered the best airport lounges in North America), Priority Pass Select, Delta Sky Club (when flying Delta), and several other networks. For frequent international travellers, this lounge access has exceptional real-world value: a Centurion Lounge visit equivalent on the open market could easily cost $60 to $100 per person. CNBC Select notes the card delivers 'statement credit offers worth up to twice what the annual fee costs' for engaged cardholders, including $200 in airline incidental credits, $200 in hotel credits for Fine Hotels + Resorts or The Hotel Collection bookings of two or more nights, $155 in Walmart+ credits, $120 in Global Entry or TSA PreCheck credits, and Uber Cash and dining credits.

At 1.8 cents per Amex point, 4x on dining equates to approximately 7.2% effective return on restaurant spending — a rate that no other major card matches without a category cap. For a household spending $2,000 per month on dining and groceries combined, the Gold earns approximately $1,728 per year in Membership Rewards value at that valuation, well above the $325 annual fee.

FinanceBuzz identifies the Gold as 'the card I use for most of my spending' in its 2026 premium card analysis, noting its 'high rewards rates for restaurants, US supermarkets, and eligible travel' alongside 'unique payment options like Plan It and Send and Split.' The ongoing statement credits — $120 in dining credits (at specific restaurants including Grubhub, The Cheesecake Factory, Goldbelly, Wine.com, and Milk Bar) and $120 in Uber Cash — reduce the effective net fee to $85 per year for cardholders who use these credits fully.

At a $95 annual fee, the break-even is straightforward: the $50 annual hotel credit when booking through Chase Travel and the anniversary 10% points bonus on the prior year's spending combined typically offset most of the fee. The 75,000-point welcome bonus — available after $4,000 in spending within the first three months — is worth approximately $1,538 at TPG's 2.05 cents-per-point May 2026 valuation, making the first-year effective return extraordinarily positive.

The Preferred earns 5x on travel purchased through Chase Travel, 3x on dining, streaming, and online grocery purchases, 2x on all other travel, and 1x elsewhere. Its travel protections — while less comprehensive than the Reserve — include trip delay reimbursement, trip cancellation and interruption insurance, primary rental car insurance, and baggage delay insurance. For most cardholders who are not heavy lounge users, the Preferred provides 90% of the Reserve's point-earning value at 17% of the fee.

The Strata Elite earns 6x ThankYou points on dining (at select merchants, times, and platforms — a meaningful caveat), 3x on hotels, air, and rental cars, 3x on Citi Entertainment purchases, and 1x on everything else. ThankYou points are valued at approximately 1.9 cents per point by TPG in May 2026 — slightly below Chase Ultimate Rewards but above Capital One miles. The card includes a $300 Citi hotel statement credit annually and a TSA PreCheck or Global Entry fee reimbursement, making the effective net fee approximately $175 after those credits.

The Points Guy notes that 'Citi ThankYou Rewards points are worth slightly less than Ultimate Rewards points' but that the Strata Elite provides 'high earning rates when spending through its portal' and is 'best for earning Citi ThankYou Rewards points' in its premium card comparison. NerdWallet's caveat is worth noting: the 6x dining rate is 'available only on certain days at certain times' at 'Splurge' merchants — a category restriction that limits practical earning for many cardholders.

The key practical insight from this comparison is that Chase Ultimate Rewards — earned with the Sapphire Reserve, Sapphire Preferred, Freedom Flex, and Freedom Unlimited — is the most valuable currency in the premium card market when transferred to the right partners. A transfer to World of Hyatt for a luxury hotel stay, or to United Airlines for a premium cabin booking, can yield redemption values well above the 2.05 cents per point benchmark. The Hyatt transfer in particular — enabling night redemptions at properties where a cash rate would be $500 to $800 — can generate effective values of 5 to 8 cents per point for cardholders who stay at Hyatt properties.

A premium credit card that is paid in full is a financial tool that earns you real value on spending you were going to do anyway. The 75,000-point welcome bonus on a Chase Sapphire Preferred is worth $1,538 at full transfer value — earned for spending you were going to make on groceries, utilities, and daily expenses. The $300 annual travel credit on a Venture X is real money returned to you each year for holding the card and booking travel you were already planning. These benefits are genuinely free for full-balance payers.

A premium credit card that carries a balance is financially destructive. The average APR on premium credit cards is 19% to 28% variable. At 21% APR, a $5,000 balance costs $1,050 per year in interest — far exceeding the value of any welcome bonus, statement credit, or rewards programme. FinanceBuzz's guidance is direct: 'If any of the above apply [debt problems, no emergency fund], start by building credit, establishing a budget, and paying down debt first.' The premium card discussion belongs entirely in the financial stability chapter of your life, not the financial recovery chapter.

For those who are debt-free, have a fully funded emergency fund, and pay their credit cards in full every month, a single premium card — the Venture X for most, the Sapphire Preferred as an entry point — can deliver genuinely meaningful annual value: $400 to $800 in credits and rewards on top of welcome bonuses worth $750 to $1,500. This is real money, earned for zero incremental cost by a financially disciplined cardholder.

The golden rule applies at every fee level: these cards are for full-balance payers who treat them as tools rather than credit lines. Used correctly — charges paid in full every month, credits actively tracked and used, welcome bonuses earned without manufactured spending — the right premium card pays for itself many times over and adds meaningful real value to your financial year. Used incorrectly — as a revolving credit line, with interest charges piling up — no rewards programme in the world will compensate.

CNN Underscored — Best Credit Cards of May 2026: Picked by Our Editors https://www.cnn.com/cnn-underscored/money/best-credit-cards

CNBC Select — Best Luxury and Premium Credit Cards of May 2026 https://www.cnbc.com/select/best-luxury-credit-cards/

The Points Guy — Best Premium Travel Rewards Cards Side-by-Side (May 2026 valuations) https://thepointsguy.com/credit-cards/best-premium-travel-rewards-cards/

FinanceBuzz — Best Premium Credit Cards 2026: Perks That Are Worth the Annual Fee https://financebuzz.com/best-premium-credit-cards

NerdWallet — Best Credit Cards 2026 Awards (250+ cards reviewed) https://www.nerdwallet.com/l/awards-credit-cards-2026

The Points Guy — Monthly Points and Miles Valuations: May 2026 https://thepointsguy.com/points-valuation/

Capital One — Venture X Rewards Credit Card: Full Terms and Benefits https://www.capitalone.com/credit-cards/venture-x/

Chase — Sapphire Reserve and Sapphire Preferred: Full Terms and Benefits https://creditcards.chase.com/travel-credit-cards/sapphire/reserve

American Express — Platinum Card and Gold Card: Full Terms and Benefits https://www.americanexpress.com/en-us/credit-cards/credit-intel/best-premium-credit-cards/

TABLE OF CONTENTS

- What Makes a Credit Card 'Premium'?

- The Core Maths: How to Know If a Premium Card Is Worth It

- All Premium Cards Side-by-Side: The May 2026 Comparison Table

- Card Deep-Dive 1: Capital One Venture X — Best Value Premium

- Card Deep-Dive 2: Chase Sapphire Reserve — Best Travel Protections

- Card Deep-Dive 3: American Express Platinum — Best Luxury Perks

- Card Deep-Dive 4: American Express Gold Card — Best for Dining

- Card Deep-Dive 5: Chase Sapphire Preferred — Best Entry-Level Premium

- Card Deep-Dive 6: Citi Strata Elite — Best for ThankYou Points

- Understanding Points Currencies: Chase, Amex, and Capital One

- Airport Lounge Access Compared: Which Card Opens Which Doors

- How to Choose the Right Premium Card for Your Spending

- Are Premium Cards Compatible with Debt-Free Living?

- Conclusion

- Frequently Asked Questions

- References

What Makes a Credit Card 'Premium'?

Premium credit cards occupy the top tier of the US consumer credit market. They are distinguished not by their spending limits — plenty of no-fee cards have high limits — but by their benefit ecosystems: rich welcome bonuses worth hundreds or thousands of dollars in travel, annual statement credits that offset a significant portion of the fee, airport lounge access across thousands of locations worldwide, travel insurance protections that can cover tens of thousands of dollars in disruption losses, and concierge services that can arrange dining reservations or tickets to sold-out events.The defining financial characteristic is the annual fee: premium cards charge anywhere from $95 (Chase Sapphire Preferred, the entry-level category) to $895 (American Express Platinum, the mainstream luxury ceiling) per year. Unlike a no-annual-fee card where any rewards are pure gain, a premium card requires its holder to earn back the annual fee through benefit usage before any profit begins. This break-even requirement is what makes premium cards genuinely worth it for some cardholders and genuinely not worth it for others — and the honest evaluation of which category you fall into is the core purpose of this guide.

NerdWallet's 2026 premium card analysis, researching nearly 250 credit cards, identifies premium cards as 'typically aimed at higher-spending consumers with good to excellent credit,' and notes that 'it's important to make sure you will extract more value from the card than you pay.' The Points Guy's May 2026 valuation framework provides the most granular tool for making this calculation: by assigning a cents-per-point value to each major rewards currency (Chase Ultimate Rewards at 2.05 cents, Amex Membership Rewards at approximately 1.8 cents, Capital One miles at 1.85 cents), it enables direct comparison of reward earning potential across cards with different fees.

Despite its seemingly high $395 annual fee, it's easy to get a lot of value out of the Capital One Venture X. That's why it beat out an array of flashier, pricier cards to be the best premium travel credit card in both 2025 and 2026.

— NERDWALLET — BEST PREMIUM CREDIT CARDS MAY 2026

The Core Maths: How to Know If a Premium Card Is Worth It

The break-even calculation for any premium card is: (Total annual fee) — (Annual statement credits you will definitely use) — (Value of rewards earned on planned spending) — (Value of other benefits you will actually use) = Net cost or Net gain.Two categories of benefits require special scrutiny in this calculation. Statement credits are the most straightforward: if a card offers a $300 annual travel credit and you spend at least $300 on travel each year, that credit effectively reduces the annual fee by $300. But many premium cards load their value into categories that require specific behaviour — $200 in airline incidental credits (only usable for baggage fees, not airfare), $200 in Uber Cash (only usable on Uber and Uber Eats), $120 in dining credits through a specific enrollment programme, $155 in Walmart+ credits. Each of these requires the cardholder to remember to enroll, to use the right payment method, and to actually spend in those specific categories. Cardholders who miss any of these credits are effectively paying a higher effective fee than the advertised one.

Lounge access is similarly variable in value. A frequent international traveller who uses airport lounges four times per month — a day pass to a comparable lounge typically costs $50 to $60 — generates $200 to $240 per month in lounge value, making lounge access worth $2,400 to $2,880 per year. An occasional domestic traveller who visits a lounge four times per year generates $200 to $240 annually. The same perk has very different values for different holders.

FinanceBuzz's 2026 guidance frames the qualifying question well: 'If you can comfortably earn the welcome bonus on a premium credit card without spending beyond your budget, that's a good sign you'll benefit from applying for one. But it's worth evaluating your past spending and calculating the value of different credit card point systems to choose the right one.'

All Premium Cards Side-by-Side: The May 2026 Comparison Table

Sources: NerdWallet (May 2026), CNN Underscored (May 2026), CNBC Select (May 2026), The Points Guy (May 2026 valuations). Annual fees, welcome offers, and benefits subject to change. Always verify current terms with card issuer before applying.

Card Deep-Dive 1: Capital One Venture X — Best Value Premium

The Capital One Venture X has won NerdWallet's best premium travel credit card award in both 2025 and 2026, and the case for it is compelling. At a $395 annual fee — $155 to $500 less than its main competitors — it delivers benefits that can offset the entire fee without requiring exceptional benefit usage.The core annual value proposition is straightforward. The $300 annual travel credit applies to any booking through Capital One Travel — including flights, hotels, and rental cars — making it broadly usable for most travellers. In addition, every card anniversary brings a 10,000-mile bonus worth $100 toward travel. Together, these two recurring benefits total $400 per year — meaning the Venture X generates positive net value before any consideration of rewards earned on spending, lounge access, or other benefits, simply by holding the card and using the $300 travel credit.

On top of this, the Venture X earns 10x miles on hotels and rental cars booked through Capital One Travel, 5x on flights through Capital One Travel, and 2x miles on every other purchase. With Capital One miles valued at approximately 1.85 cents per point by The Points Guy in May 2026, 2x miles on everyday spending equates to approximately 3.7% back in travel value — competitive with the best no-fee cards at a net effective cost of negative $5 (since the credits exceed the fee by $5).

The Venture X also includes Priority Pass airport lounge access for the primary cardholder and two guests, Global Entry or TSA PreCheck fee reimbursement, no foreign transaction fees, and a comprehensive travel insurance package. CNBC Select notes it as one of the best overall premium cards precisely because it delivers 'premium benefits without the premium price tag.'

Who should get the Venture X

The Venture X is the right card for any US consumer who travels at least a few times per year, will use the $300 Capital One Travel credit, and wants premium lounge access without paying $550 to $895 for it. It is the strongest value-per-dollar premium card available in the US market in 2026.Card Deep-Dive 2: Chase Sapphire Reserve — Best Travel Protections

The Chase Sapphire Reserve is the most comprehensively protective travel card available to US consumers — and for frequent travellers whose plans are disrupted regularly, its travel insurance benefits alone can deliver thousands of dollars in value per year. CNBC Select rates it as 'best for travel protections,' and its $550 annual fee can be more than offset by the combination of statement credits, rewards, and insurance protection for the right holder.The Reserve's $300 annual travel credit is the most broadly applicable of any premium card — it automatically applies to the first $300 of travel purchases charged to the card each year, with a broad definition of travel that includes airlines, hotels, rental cars, trains, Uber, Lyft, tolls, and parking. This effectively reduces the annual fee to $250 from the moment you spend $300 on any form of travel. Additionally, CNBC Select notes it offers 'more than $3,000 in annual value' when factoring in the $500 annual credit for stays at The EditSM by Chase Travel properties.

The Chase Ultimate Rewards currency — earning at 10x on Chase Travel purchases, 5x on flights, and 3x on dining and other travel — is valued by The Points Guy at 2.05 cents per point in May 2026, making it the most valuable major credit card currency in the US market. A 75,000-point welcome bonus is worth approximately $1,538 at that valuation — or $750 when redeemed at the straightforward 1.25 cents through the Chase travel portal.

The travel protections are best-in-class: trip cancellation and interruption insurance (up to $10,000 per person, $20,000 per trip), trip delay reimbursement ($500 per ticket for delays over six hours), primary rental car insurance (no need to decline the rental company's coverage), emergency medical and evacuation coverage ($100,000), and baggage delay insurance. For a frequent business traveller whose trips are sometimes disrupted, these protections can be worth substantially more than the annual fee in a single bad travel year.

Who should get the Sapphire Reserve

The Sapphire Reserve is ideal for frequent travellers who value flexibility (the $300 credit works everywhere, not just through a portal), who eat out regularly (3x on dining on the best currency in the market), and who have experienced or are concerned about travel disruptions. Those already holding Chase Sapphire Preferred should note that holding both simultaneously is not permitted.Card Deep-Dive 3: American Express Platinum — Best Luxury Perks

The American Express Platinum Card is the definitive luxury premium card in the US market and the one with the highest annual fee at $895. At this price point, the card must be managed actively and strategically to generate net positive value — but for the right cardholder, the Platinum's benefit suite is genuinely unmatched.The welcome offer is the most generous available in the premium card market: CNN Underscored notes cardholders 'may be eligible for as high as 175,000 Membership Rewards points after spending $12,000 in eligible purchases in the first 6 months.' This offer is not universal — it varies by applicant and channel — but at 1.8 cents per point, 175,000 points represent approximately $3,150 in travel value, making the first-year effective cost of the card negative even after the $895 fee.

The ongoing benefit suite includes access to over 1,550 airport lounges — the broadest of any consumer credit card — including Amex's own Centurion Lounges (widely considered the best airport lounges in North America), Priority Pass Select, Delta Sky Club (when flying Delta), and several other networks. For frequent international travellers, this lounge access has exceptional real-world value: a Centurion Lounge visit equivalent on the open market could easily cost $60 to $100 per person. CNBC Select notes the card delivers 'statement credit offers worth up to twice what the annual fee costs' for engaged cardholders, including $200 in airline incidental credits, $200 in hotel credits for Fine Hotels + Resorts or The Hotel Collection bookings of two or more nights, $155 in Walmart+ credits, $120 in Global Entry or TSA PreCheck credits, and Uber Cash and dining credits.

Who should get the Amex Platinum

The Amex Platinum is for frequent international travellers who will use multiple lounges per trip, who value hotel status and fine hotel benefits, and who are disciplined enough to track and use its numerous statement credit categories. It is not for occasional travellers — the fee is too high to justify without active benefit usage. CNN Underscored summarises it precisely: 'best for luxury travelers who can use the benefits to offset the high fee.'Card Deep-Dive 4: American Express Gold Card — Best for Dining

The American Express Gold Card occupies the mid-tier premium category at $325 per year and delivers the best dining and grocery rewards of any card in the premium market. Earning 4x Membership Rewards points at restaurants worldwide and at US supermarkets (up to $25,000 in combined spending per year, then 1x), the Gold generates exceptional rewards value for cardholders whose spending is concentrated in food.At 1.8 cents per Amex point, 4x on dining equates to approximately 7.2% effective return on restaurant spending — a rate that no other major card matches without a category cap. For a household spending $2,000 per month on dining and groceries combined, the Gold earns approximately $1,728 per year in Membership Rewards value at that valuation, well above the $325 annual fee.

FinanceBuzz identifies the Gold as 'the card I use for most of my spending' in its 2026 premium card analysis, noting its 'high rewards rates for restaurants, US supermarkets, and eligible travel' alongside 'unique payment options like Plan It and Send and Split.' The ongoing statement credits — $120 in dining credits (at specific restaurants including Grubhub, The Cheesecake Factory, Goldbelly, Wine.com, and Milk Bar) and $120 in Uber Cash — reduce the effective net fee to $85 per year for cardholders who use these credits fully.

Who should get the Amex Gold

The Gold is the right premium card for households with significant regular spending at restaurants and US supermarkets who want to earn Amex Membership Rewards points. It is particularly powerful for those who can transfer points to Amex's airline and hotel partners for outsized travel redemptions. The dining credit requires specific merchant use — check the current eligible merchants before counting on it fully.Card Deep-Dive 5: Chase Sapphire Preferred — Best Entry-Level Premium

The Chase Sapphire Preferred is widely rated as the best entry-level premium card in the US market at $95 per year — a fraction of its higher-fee competitors. NerdWallet's 2026 awards programme rates it 'best for moderate spenders who want flexibility without a high annual fee,' and its combination of a 75,000-point welcome offer and the Chase Ultimate Rewards currency — the most valuable in the US premium card market — makes it exceptional value at its price point.At a $95 annual fee, the break-even is straightforward: the $50 annual hotel credit when booking through Chase Travel and the anniversary 10% points bonus on the prior year's spending combined typically offset most of the fee. The 75,000-point welcome bonus — available after $4,000 in spending within the first three months — is worth approximately $1,538 at TPG's 2.05 cents-per-point May 2026 valuation, making the first-year effective return extraordinarily positive.

The Preferred earns 5x on travel purchased through Chase Travel, 3x on dining, streaming, and online grocery purchases, 2x on all other travel, and 1x elsewhere. Its travel protections — while less comprehensive than the Reserve — include trip delay reimbursement, trip cancellation and interruption insurance, primary rental car insurance, and baggage delay insurance. For most cardholders who are not heavy lounge users, the Preferred provides 90% of the Reserve's point-earning value at 17% of the fee.

Who should get the Sapphire Preferred

The Sapphire Preferred is the right first premium card for most US consumers: it earns the best rewards currency at the lowest premium price point, builds toward the same transfer partner ecosystem as the Reserve, and carries the same welcome bonus. It is also the right upgrade from a no-fee card for anyone whose annual spending on dining and travel exceeds approximately $3,000 per year.Card Deep-Dive 6: Citi Strata Elite — Best for ThankYou Points

The Citi Strata Elite is NerdWallet's 2026 pick for best earning in the Citi ThankYou Rewards ecosystem. At a $595 annual fee, it is competitive with the Chase Sapphire Reserve and must be evaluated on the same terms: are the benefits and earning rates worth the fee for your specific spending pattern?The Strata Elite earns 6x ThankYou points on dining (at select merchants, times, and platforms — a meaningful caveat), 3x on hotels, air, and rental cars, 3x on Citi Entertainment purchases, and 1x on everything else. ThankYou points are valued at approximately 1.9 cents per point by TPG in May 2026 — slightly below Chase Ultimate Rewards but above Capital One miles. The card includes a $300 Citi hotel statement credit annually and a TSA PreCheck or Global Entry fee reimbursement, making the effective net fee approximately $175 after those credits.

The Points Guy notes that 'Citi ThankYou Rewards points are worth slightly less than Ultimate Rewards points' but that the Strata Elite provides 'high earning rates when spending through its portal' and is 'best for earning Citi ThankYou Rewards points' in its premium card comparison. NerdWallet's caveat is worth noting: the 6x dining rate is 'available only on certain days at certain times' at 'Splurge' merchants — a category restriction that limits practical earning for many cardholders.

Who should get the Citi Strata Elite

The Strata Elite is best for Citi ecosystem loyalists and cardholders whose regular spending includes hotels and flights booked through the Citi portal, and who eat regularly at high-spending restaurant environments where the elevated dining rate applies. American Airlines frequent flyers will particularly benefit from the airline's status with Citi's transfer partner network.Understanding Points Currencies: Chase, Amex, and Capital One

The value of a premium card is not determined solely by its annual fee or welcome bonus — it is determined by the underlying currency you are earning and how you intend to use it. The three dominant premium card currencies — Chase Ultimate Rewards, Amex Membership Rewards, and Capital One Miles — have meaningfully different values depending on redemption method.

TPG point valuations as of May 2026. Point values are estimates based on typical transfer and redemption scenarios. Actual value depends on specific redemption. Portal values reflect minimum guaranteed redemption without transfers.

The key practical insight from this comparison is that Chase Ultimate Rewards — earned with the Sapphire Reserve, Sapphire Preferred, Freedom Flex, and Freedom Unlimited — is the most valuable currency in the premium card market when transferred to the right partners. A transfer to World of Hyatt for a luxury hotel stay, or to United Airlines for a premium cabin booking, can yield redemption values well above the 2.05 cents per point benchmark. The Hyatt transfer in particular — enabling night redemptions at properties where a cash rate would be $500 to $800 — can generate effective values of 5 to 8 cents per point for cardholders who stay at Hyatt properties.

Airport Lounge Access Compared: Which Card Opens Which Doors

Airport lounge access is the single most visible premium card benefit and the one most commonly used to justify annual fees. Understanding which lounges each card accesses — and the quality differences between those lounges — is essential for evaluating lounge value for your specific travel patterns.Airport lounge access by card — what each card actually unlocks

- American Express Platinum — the broadest access. Over 1,550 lounges across Centurion Lounges (Amex's own premium brand, widely considered the best airport lounges in the US), Priority Pass Select (1,400+ lounges globally), Delta Sky Club (when flying Delta), Escape Lounges, and several other branded lounge networks. For frequent international travellers or those flying through hub airports with Centurion Lounges (New York JFK, Dallas, Miami, Los Angeles, etc.), this access is worth $80 to $120 per visit in real-world value.

- Capital One Venture X — Priority Pass access (1,400+ lounges) plus access to Capital One's own growing Lounge network (currently at Dallas DFW, Denver, and Washington Dulles, with further expansion planned). The Capital One Lounges are receiving strong reviews for quality comparable to Centurion Lounges. At $395 annual fee, this is outstanding lounge value relative to cost.

- Chase Sapphire Reserve — Priority Pass Select access (1,400+ lounges) plus every Chase Sapphire Lounge by The Club, with two guests included. CNBC Select confirms 'access over 1,300 airport lounges worldwide.' Chase Sapphire Lounges are a newer addition and currently exist at select airports; Priority Pass covers the broad global network.

- Citi Strata Elite — Priority Pass access, covering the same 1,400+ lounge network as the Reserve and Venture X. No proprietary branded lounges.

- American Express Gold Card and Chase Sapphire Preferred — No lounge access. Both are mid-tier premium cards without lounge benefits, which is a significant distinction from the $395+ tier.

- Key practical consideration: Priority Pass has been removing restaurant credits from many of its participating US airport restaurants in recent years, reducing the value of Priority Pass for US domestic travellers. The proprietary lounge networks — Centurion (Amex Platinum), Capital One Lounges (Venture X), and Chase Sapphire Lounges (Reserve) — tend to provide better quality and more consistent experiences than Priority Pass partner lounges at US airports specifically.

How to Choose the Right Premium Card for Your Spending

Are Premium Cards Compatible with Debt-Free Living?

The stability-over-status financial philosophy — the growing US movement toward financial security, debt freedom, and resilience over consumption and display — has a clear and honest answer to whether premium credit cards fit: yes, if and only if you pay the full balance every month, every time.A premium credit card that is paid in full is a financial tool that earns you real value on spending you were going to do anyway. The 75,000-point welcome bonus on a Chase Sapphire Preferred is worth $1,538 at full transfer value — earned for spending you were going to make on groceries, utilities, and daily expenses. The $300 annual travel credit on a Venture X is real money returned to you each year for holding the card and booking travel you were already planning. These benefits are genuinely free for full-balance payers.

A premium credit card that carries a balance is financially destructive. The average APR on premium credit cards is 19% to 28% variable. At 21% APR, a $5,000 balance costs $1,050 per year in interest — far exceeding the value of any welcome bonus, statement credit, or rewards programme. FinanceBuzz's guidance is direct: 'If any of the above apply [debt problems, no emergency fund], start by building credit, establishing a budget, and paying down debt first.' The premium card discussion belongs entirely in the financial stability chapter of your life, not the financial recovery chapter.

For those who are debt-free, have a fully funded emergency fund, and pay their credit cards in full every month, a single premium card — the Venture X for most, the Sapphire Preferred as an entry point — can deliver genuinely meaningful annual value: $400 to $800 in credits and rewards on top of welcome bonuses worth $750 to $1,500. This is real money, earned for zero incremental cost by a financially disciplined cardholder.

CONCLUSION

The best premium credit card for most US consumers in 2026 is the Capital One Venture X at $395 — a card whose $300 annual travel credit and 10,000-mile anniversary bonus more than offset the fee before any other benefit is considered. For heavier travellers who value travel protections and the flexibility of the best points currency in the market, the Chase Sapphire Reserve at $550 delivers exceptional value and over $3,000 in stated annual benefits. The Amex Platinum at $895 is genuinely the best luxury card for frequent international travellers who will use multiple lounges per trip and engage actively with its credit ecosystem — and genuinely not worth it for anyone who will not.The golden rule applies at every fee level: these cards are for full-balance payers who treat them as tools rather than credit lines. Used correctly — charges paid in full every month, credits actively tracked and used, welcome bonuses earned without manufactured spending — the right premium card pays for itself many times over and adds meaningful real value to your financial year. Used incorrectly — as a revolving credit line, with interest charges piling up — no rewards programme in the world will compensate.

Frequently Asked Questions

What is the best premium credit card for most US consumers in 2026?

NerdWallet named the Capital One Venture X the best premium travel credit card for both 2025 and 2026. At a $395 annual fee, it delivers a $300 annual travel credit and a 10,000-mile anniversary bonus (worth $100 in travel) — totalling $400 in recurring value that more than offsets the fee before any rewards earnings are counted. It also provides Priority Pass lounge access, access to Capital One's growing proprietary lounge network, Global Entry or TSA PreCheck reimbursement, no foreign transaction fees, and a 75,000-mile welcome bonus worth $750 in travel. For most US consumers, it beats every more expensive premium card on a net-value basis.Is the Amex Platinum worth $895 per year?

For frequent international travellers who actively use its benefit suite, yes. The Amex Platinum provides over 1,550 airport lounges including Centurion Lounges, $200 in airline incidental credits, $200 in hotel credits at Fine Hotels + Resorts or The Hotel Collection (two-night minimum), $155 in Walmart+ credits, $120 in Global Entry or TSA PreCheck, and Uber Cash and dining credits. CNBC Select notes that 'statement credit offers worth up to twice what the annual fee costs' are available to engaged cardholders. The welcome bonus of up to 175,000 Membership Rewards points — worth approximately $3,150 at 1.8 cents per point (TPG) — makes the first year strongly positive for most applicants. For occasional travellers who will not use the lounge access or most credits, it is not worth it.What is the difference between Chase Ultimate Rewards and Amex Membership Rewards?

Both are flexible points currencies that can be transferred to airline and hotel loyalty programmes or redeemed through travel portals. Chase Ultimate Rewards (earned on Sapphire Reserve, Sapphire Preferred) are valued at 2.05 cents per point by The Points Guy in May 2026 — the highest valuation of any major premium card currency. The most valuable transfers include World of Hyatt (luxury hotel stays), United Airlines, and Air France/KLM. Amex Membership Rewards (earned on the Platinum and Gold) are valued at approximately 1.8 cents per point, with best transfers to Delta SkyMiles, British Airways Avios, Air Canada Aeroplan, and Hilton and Marriott for hotels. Chase points are slightly more flexible and more consistently high-value; Amex points have access to some exclusive transfer partners and the broader Amex ecosystem.Is the Chase Sapphire Reserve worth the upgrade from the Preferred?

The upgrade from $95 Sapphire Preferred to $550 Sapphire Reserve costs $455 more per year. The incremental value of the Reserve over the Preferred includes: $300 annual travel credit (vs $50 hotel credit — an extra $250 in credits), Priority Pass lounge access, Chase Sapphire Lounge access, the $500 annual Edit hotel credit, higher earning rates (10x vs 5x on Chase Travel), and better travel insurance limits. If you can use the $300 travel credit and $500 Edit hotel credit, the incremental credits alone ($800 extra) more than justify the $455 fee increase. If you rarely use lounges and won't use the Edit credit, the Preferred is the better value.Should I get a premium card if I'm working on paying off debt?

No. Premium credit cards are beneficial only for full-balance payers. If you carry a balance, the interest charges at 19% to 28% APR will eliminate every dollar of rewards, statement credits, and welcome bonus value — typically many times over. FinanceBuzz's guidance is explicit: 'Start by building credit, establishing a budget, and paying down debt first.' Once you are debt-free, have three to six months of living expenses in an emergency fund (ideally in a high-yield savings account), and can commit to paying your card balance in full every month, a premium card can add meaningful value to your financial year. The order of financial priority is: debt repayment first, emergency fund second, then rewards optimisation.What credit score do you need for a premium credit card?

Premium credit cards generally require good to excellent credit — typically a FICO score of 700 or above, with the most competitive cards (Chase Sapphire Reserve, Amex Platinum) preferring 720 to 740 or higher. CNBC Select notes that 'most luxury cards require good or excellent credit to qualify.' Beyond the credit score, card issuers also review your income (premium cards are designed for higher spenders), existing credit card history (too many recent applications can hurt approval odds), and your relationship with the issuer (existing customers may have improved approval prospects). If your credit score is below 700, the most productive step is to build credit with a responsible no-annual-fee card before applying for a premium product.References

NerdWallet — Best Premium Credit Cards of May 2026 (updated daily) https://www.nerdwallet.com/credit-cards/best/premiumCNN Underscored — Best Credit Cards of May 2026: Picked by Our Editors https://www.cnn.com/cnn-underscored/money/best-credit-cards

CNBC Select — Best Luxury and Premium Credit Cards of May 2026 https://www.cnbc.com/select/best-luxury-credit-cards/

The Points Guy — Best Premium Travel Rewards Cards Side-by-Side (May 2026 valuations) https://thepointsguy.com/credit-cards/best-premium-travel-rewards-cards/

FinanceBuzz — Best Premium Credit Cards 2026: Perks That Are Worth the Annual Fee https://financebuzz.com/best-premium-credit-cards

NerdWallet — Best Credit Cards 2026 Awards (250+ cards reviewed) https://www.nerdwallet.com/l/awards-credit-cards-2026

The Points Guy — Monthly Points and Miles Valuations: May 2026 https://thepointsguy.com/points-valuation/

Capital One — Venture X Rewards Credit Card: Full Terms and Benefits https://www.capitalone.com/credit-cards/venture-x/

Chase — Sapphire Reserve and Sapphire Preferred: Full Terms and Benefits https://creditcards.chase.com/travel-credit-cards/sapphire/reserve

American Express — Platinum Card and Gold Card: Full Terms and Benefits https://www.americanexpress.com/en-us/credit-cards/credit-intel/best-premium-credit-cards/

0 Comments Comments