Investing

Accountant Exolains What Is Diversification in Investment?

Table of Contents

- The Only Free Lunch in Investing

- What Is Diversification in Investment?

- Modern Portfolio Theory: The Mathematics Behind Diversification

- The Six Dimensions of Diversification: Complete 2026 Framework

- What Diversification Cannot Do: The Systematic Risk Reality

- UK Investors: Holdings vs Best Practice — The 2026 Gap Analysis

- The UK Home Bias Problem: The Biggest Diversification Mistake

- Diversification in 2026: The 'Anything But AI' Rotation

- The Six Most Common Diversification Mistakes

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

The Only Free Lunch in Investing

Nobel laureate Harry Markowitz, whose 1952 paper 'Portfolio Selection' transformed the theory and practice of investment management, famously described diversification as 'the only free lunch in investing.' The phrase has become one of the most repeated in personal finance — and one of the most frequently misunderstood. Diversification is not simply owning many things. It is owning things that respond differently to the same economic events, so that when some positions fall others hold their value or rise, smoothing the overall portfolio's return over time.The 2025 investment year delivered one of the most compelling real-world proof points for diversification in years. Morningstar's 2026 Diversification Landscape report (Amy C. Arnott CFA, April 14, 2026) found that a thoughtfully diversified portfolio returned approximately 18.3% in 2025, compared with 13.3% for a basic 60/40 portfolio of US stocks and bonds. The 5-percentage-point advantage was the biggest win for diversification since 2009. Gold surged nearly 70%. International equities outperformed US stocks. Bonds — after the 2022 debacle — returned to their traditional role as equity diversifiers, rising while stocks fell during the April 2025 tariff turmoil. In early 2026, the story has continued: international stocks, value stocks, small-cap equities, and dividend-paying companies are all outperforming US mega-cap technology as investors rotate away from the concentrated AI trade.

For UK investors, the 2026 diversification picture has a particular urgency. A Market Financial Solutions survey (July 2025) of UK investors found that 46% consider diversification their top investment priority — yet 29% hold equities, 26% hold cash, only 8% hold fixed income, 5% commodities, and 4% digital assets. The data suggests that while UK investors talk about diversification, many remain heavily concentrated in domestic cash and equities. This guide explains what diversification really is, why it works mathematically, the six dimensions across which it should be applied, what the 2025-2026 performance data teaches, how many holdings you actually need, the UK-specific home bias problem, and the most common mistakes that produce the appearance of diversification without the reality.

What Is Diversification in Investment?

Investment diversification is the practice of spreading a portfolio across different assets, asset classes, geographies, sectors, and investment styles in a deliberate way that reduces the impact of any single investment's poor performance on the overall portfolio. The Vanguard guide to portfolio diversification articulates the principle with the classic analogy: 'Don't put all your eggs in one basket. If the basket falls, you could lose everything. But if your eggs are in multiple baskets, you have a much better chance of getting home safely.'In financial terms, diversification works through the mathematical concept of correlation. Correlation is a statistical measure ranging from -1 to +1 that quantifies how closely two assets move together. When assets have a correlation of +1, they rise and fall in perfect unison — holding both provides no diversification benefit whatsoever. When assets have a correlation of 0, they move completely independently — combining them reduces the portfolio's overall volatility without reducing expected return. When assets have a correlation of -1, they move in opposite directions — a portfolio combining them eliminates variability entirely.

Real-world correlations between asset classes are rarely perfectly negative but are frequently meaningfully below +1 — particularly between different asset classes. Stocks and government bonds have historically shown low or negative correlations, particularly during economic stress. Gold has shown near-zero or negative correlation with equities in many periods. International equities have lower correlations to UK equities than UK equities have to each other. These imperfect correlations are the mechanism through which diversification reduces portfolio risk without proportionally reducing expected return — the mathematical 'free lunch' that Markowitz formalised.

2025 diversification in numbers: Diversified multi-asset portfolio +18.3% vs basic 60/40 +13.3% — a 5 percentage-point advantage, the biggest since 2009 — Morningstar's 2026 Diversification Landscape (Amy C. Arnott CFA, April 14, 2026). The outperformance was driven by: non-US international equities outperforming US; gold surging ~70%; bonds returning to negative stock correlation. Simultaneously, the US stock market was more concentrated in its top 10 names than at any point since 1932 by year-end 2025 — making the diversification benefit of holding beyond the mega-caps especially pronounced

Modern Portfolio Theory: The Mathematics Behind Diversification

Harry Markowitz's Modern Portfolio Theory (MPT), published in the Journal of Finance in 1952, proved mathematically that a portfolio combining imperfectly correlated assets can achieve a higher expected return for any given level of risk — or equivalently, lower risk for any given expected return — than any individual asset within it. This insight earned Markowitz the Nobel Memorial Prize in Economic Sciences in 1990 and remains the foundational intellectual framework for professional portfolio construction.The key practical insight from MPT is that the risk-reducing power of diversification comes entirely from the correlation between assets, not from the number of holdings. Two assets with a correlation of 0.2 combined in a portfolio produce significantly more risk reduction than two assets with a correlation of 0.9, regardless of how many you hold. This is why Morningstar UK's January 2026 analysis emphasises: 'Diversification, investors are told, is about combining assets that behave differently. You want some to zig while others zag.' The insight is correct, but the implementation requires careful attention to actual correlations, which change over time.

The academic research on how many stocks are needed to achieve sufficient diversification provides clear guidance. A peer-reviewed ScienceDirect study (2022) analysing 20 years of US stock price data across the global financial crisis and COVID-19 crash confirmed the '30-40 stock rule': approximately 30-40 stocks sampled from at least 9 different sectors is sufficient to eliminate most unsystematic (company-specific) risk. Critically, the study found: 'It is typically more beneficial to diversify across sectors rather than within.' Nine stocks in nine sectors outperforms 36 stocks in three sectors, even though the number of holdings is higher in the latter. 200Calculators' 2026 analysis adds the modern alternative: 'A single low-cost global index ETF holds 1,500-3,500 companies across 23-50 countries — providing more diversification than most private investors could construct themselves, at a fraction of the cost.'

Why UK equities are underestimated as global diversifiers: An important and often missed insight from Trustnet's August 2024 analysis: of all major regional equity markets, the UK was the LEAST correlated to the MSCI World Index during the year to August 2024. The UK market's sector composition — overweight in financials, energy, healthcare, and mining versus the technology-heavy US market — means that UK equities can actually provide diversification within a globally-oriented portfolio. Henry Cobbe of Elston Consulting: 'Whilst fund flows show deallocations from UK equities, presumably to chase higher returns elsewhere, those investors may be missing the point of what a UK allocation is useful for — genuine diversification.' For 2026, this insight has become more relevant: as the 'anything but AI' trade benefits value, income, and non-tech sectors, the UK market's structural tilt toward these areas is providing positive differentiation.

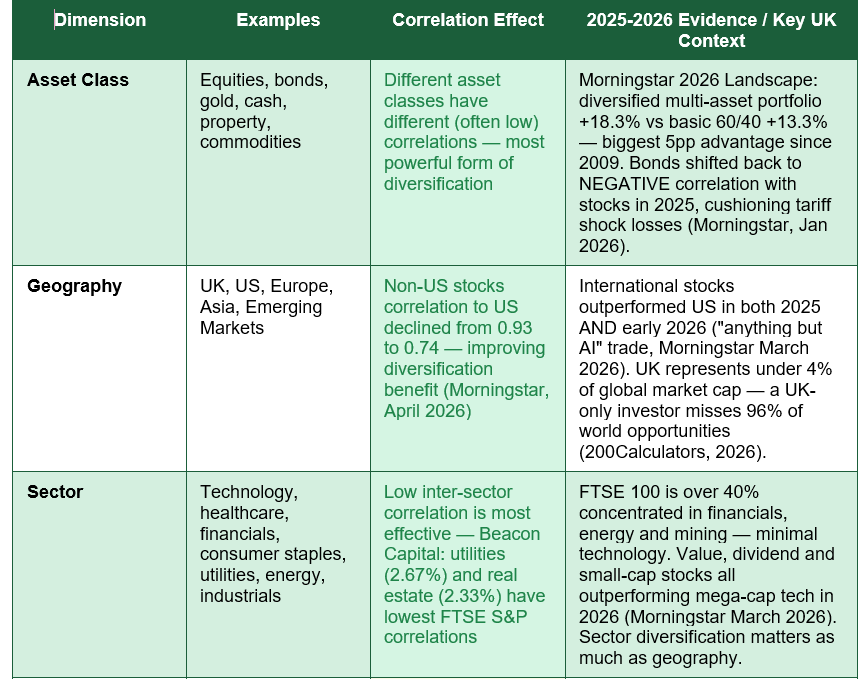

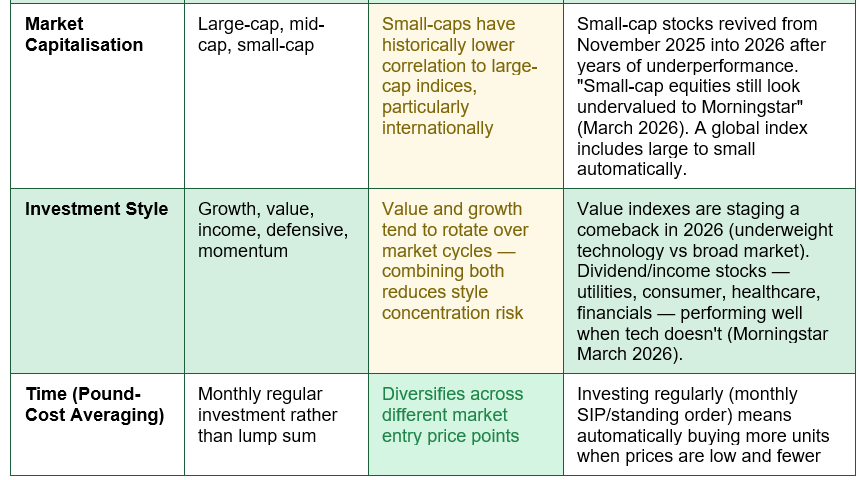

The Six Dimensions of Diversification: Complete 2026 Framework

Genuine diversification operates across six distinct dimensions. Most investors address one or two but miss the others — creating portfolios that feel diversified but remain exposed to significant concentrations:

What Diversification Cannot Do: The Systematic Risk Reality

Understanding diversification's power requires equally understanding its limits. The most important distinction in investment risk management is between systematic risk and unsystematic risk. Diversification eliminates unsystematic risk but cannot touch systematic risk:Unsystematic risk — also called specific or idiosyncratic risk — is the risk specific to a single company, sector, or geography. The bankruptcy of a single company, a product recall, a management scandal, a sector-specific regulatory change. This risk can be substantially eliminated by diversification: if one of 30 companies in a portfolio fails, the other 29 continue. As you add more well-chosen, low-correlated holdings, unsystematic risk decreases toward zero.

Systematic risk — also called market risk — is the risk that affects the entire market simultaneously: recessions, pandemics, major geopolitical crises, sudden interest rate spikes, global financial contagion. When the March 2020 COVID crash hit, virtually every stock market in every country fell simultaneously. When the April 2025 tariff shock hit, US equities fell broadly. No amount of stock-level diversification protects against these events because they affect all stocks at once. The correlation between all stocks rises toward 1.0 during severe market crises — precisely when diversification within equities is most needed and least available.

This is why true portfolio resilience requires diversification across asset classes, not just within equities. During the April 2025 tariff turmoil, the Morningstar US Core Bond Index rose while stocks fell — providing exactly the systematic-risk buffer that equity-only diversification cannot. Gold surged 70% across 2025 partly because its drivers (geopolitical stress, inflation expectations, safe-haven demand) are fundamentally different from those driving equity markets. These genuinely different asset classes — bonds, gold, commodities, cash — are the mechanism through which systematic risk exposure can be reduced, if not eliminated.

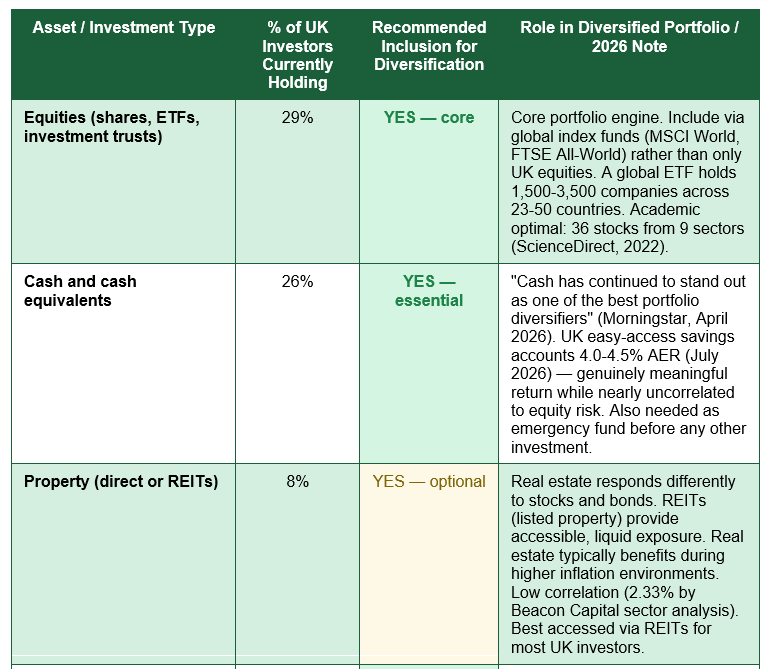

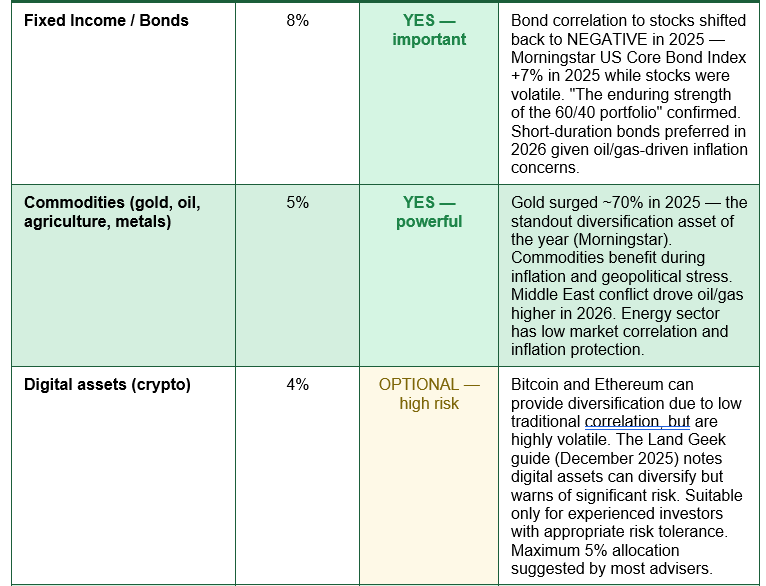

UK Investors: Holdings vs Best Practice — The 2026 Gap Analysis

A Market Financial Solutions survey of UK investors (July 2025, research by Opinium) provides the most current picture of how UK investors are actually allocated — and where the diversification gaps are largest. The table below maps actual UK investor holdings against recommended diversification practice:

The UK Home Bias Problem: The Biggest Diversification Mistake

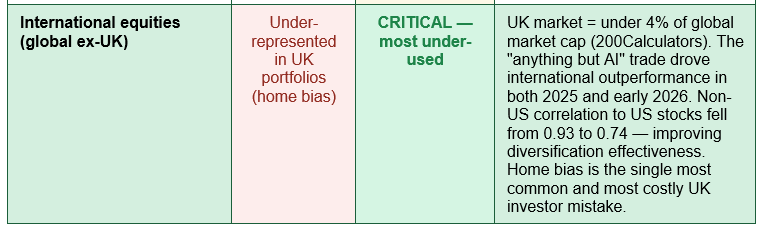

The single most common and most financially consequential diversification failure among UK investors is home bias — the tendency to overweight UK equities and underweight international exposure. The scale of the problem is striking: the UK represents under 4% of global stock market capitalisation (200Calculators, 2026), yet many UK investors hold 30%, 50%, or even 100% of their equity allocation in UK stocks. This means they are systematically underexposed to 96% of the world's investable equity market.The FTSE 100 compounds the problem through its own concentration. 200Calculators' 2026 analysis notes: 'The FTSE 100 is heavily concentrated in financials (banks, insurers), energy (BP, Shell) and mining companies — sectors that make up over 40% of the index. It has minimal technology exposure compared to global indices. Investing solely in the FTSE 100 concentrates you in specific sectors and one geography.' A UK investor who believes they are 'invested in the stock market' through a FTSE 100 tracker is actually heavily concentrated in a narrow set of sectors with an industry mix that looks very different from global capitalism.

The 2025-2026 data makes the cost of home bias exceptionally clear. Non-US international equities outperformed US equities in 2025 — and have continued to outperform in early 2026 as the 'anything but AI' rotation benefits the value and income sectors that international markets are more heavily weighted toward. The correlation between international stocks and US stocks has fallen from 0.93 to 0.74, meaning international exposure is providing better diversification benefit than it has in years (Morningstar, April 2026). For UK investors, adding global equity exposure — through a low-cost MSCI World ETF or FTSE All-World ETF within a Stocks and Shares ISA — is the single most impactful diversification action currently available.

UK INVESTORS: THE PRACTICAL PORTFOLIO CHECK Open your investment accounts and calculate what percentage of your total invested assets each of the following represents: UK equities, non-UK equities, bonds, gold or commodities, and cash earmarked for investment. If UK equities + cash accounts for more than 60% of your total portfolio, you have significant home bias and concentration risk. If you have no non-UK equity exposure, you are missing the single biggest diversification improvement available. A single global equity ETF — such as the iShares MSCI World ETF or Vanguard FTSE All-World — provides exposure to thousands of companies across over 40 countries and can be held within a Stocks and Shares ISA at an annual cost well below 0.5%.

Diversification in 2026: The 'Anything But AI' Rotation

Morningstar's March 4, 2026 article — 'These Diversification Strategies Are Winning in 2026' — identifies a particularly instructive development in the current year that illustrates why diversification matters in real time. By the end of 2025, the US stock market was more heavily concentrated in its 10 largest names than at any point since 1932 — with much of that concentration driven by AI-related mega-cap technology stocks. Investors who had concentrated their portfolios in these names had been richly rewarded in 2023 and 2024.In early 2026, the picture shifted. Concerns about AI capital spending, questions about AI's economic impact, and a rotation in investor sentiment produced what Morningstar's Susan Dziubinski describes as the 'anything but AI' trade. The result: 'most mega-cap names are in negative territory so far in 2026.' Meanwhile, the diversifying assets that many investors had neglected are performing strongly: international stocks (continuing their 2025 outperformance), value stocks (underweight in technology vs the broad market), small-cap equities (still undervalued according to Morningstar), and dividend-paying companies in utilities, consumer staples, healthcare, and financials.

Dan Lefkovitz, Morningstar's indexes strategist, frames the lesson with precision: 'Dividend-payers, which skew toward old economy sectors, allow investors to participate in the equity market without as much reliance on the AI theme. And these sectors often perform well when tech doesn't.' The entire 2026 experience encapsulates why diversification exists: not to eliminate the possibility of concentration bets paying off, but to ensure that when the concentrated trade reverses — as all concentrated trades eventually do — the portfolio has genuine exposure to the assets benefiting from the rotation.

THE CONCENTRATION WARNING — AI, TECH, AND THE TOP 10: The US stock market's concentration in its top 10 names reached levels not seen since 1932 by the end of 2025 (Morningstar, March 2026). Investors in global equity index funds are more exposed to this concentration than they may realise — the Morningstar UK January 2026 analysis warns: 'Investors buying global equity funds may not be getting the broad diversification they perhaps expect given that global equity indices have such a large allocation to the US equity market and within that, to a handful of tech stocks.' Check the top 10 holdings of any global equity fund you own. Consider whether a value tilt, a small-cap allocation, international equities, UK equities, or dividend-focused funds might provide additional diversification against the concentrated AI trade that has made the global index less diversified than it appears.

The Six Most Common Diversification Mistakes

Understanding diversification correctly means understanding the common errors that defeat it in practice:- Confusing quantity of holdings with genuine diversification: 30 UK bank stocks provide almost no diversification — they are highly correlated and fall together in banking crises. 10 stocks across 10 different sectors and geographies provide more. Diversification quality — measured by actual correlations — matters more than the count of holdings.

- Overlapping funds: Owning a UK equity fund, a FTSE 100 tracker, a UK dividend fund, and a UK income fund typically means holding the same companies in each. Check the top 10 holdings of every fund you own. Genuine overlap in key names means you have less diversification than the number of funds suggests. Vanguard's guide specifically warns: 'Some investors, in an attempt to diversify, invest in too many funds with overlapping holdings, unnecessarily increasing investment costs.'

- Ignoring bond-stock correlations: The bond-stock relationship is not fixed. In 2022, bonds and stocks fell simultaneously — a historically unusual event driven by aggressive rate hikes. In 2025, bonds returned to their traditional negative correlation with stocks, rising during the April tariff sell-off. Morningstar UK (January 2026): 'The relationship between asset classes is fluid.' Check current correlations annually; do not assume historical relationships will persist.

- Neglecting rebalancing: A portfolio that was 60% equities and 40% bonds in 2020 may have drifted to 75% equities and 25% bonds by 2026 as equities outperformed. This drift increases risk relative to the original intention. Annual rebalancing — selling the assets that have outperformed and buying those that have underperformed — maintains the intended risk level and is itself a form of systematic value discipline.

- Treating gold and silver as diversifiers from each other: Vanguard's diversification guide offers the most concise version of this trap: 'You might think buying gold, silver, and platinum is helping you diversify, but since these metals tend to perform similarly, they may not offer the diversity you seek.' True diversification requires assets that respond to genuinely different economic drivers — not different instruments within the same asset class.

- Ignoring time horizon in asset allocation: A 25-year-old investing for retirement in 40 years can tolerate far more equity volatility than a 60-year-old planning to retire in 5 years. Age-appropriate asset allocation — gradually shifting from high-equity to more defensive multi-asset portfolios as the investment horizon shortens — is itself a form of diversification across risk profiles over time.

Conclusion

Investment diversification is the most empirically robust principle in portfolio management and the one whose benefits 2025 demonstrated most vividly in years. A thoughtfully diversified portfolio returned 18.3% in 2025 against 13.3% for a basic 60/40 blend — a 5-percentage-point advantage that was the biggest since 2009. Gold surged 70%. International equities outperformed US stocks in 2025 and continued to do so in 2026 as the 'anything but AI' rotation benefited the sectors and geographies that diversified investors had exposure to. Bonds returned to their traditional role as equity buffers. The lesson: genuine diversification — across asset classes, geographies, sectors, market caps, and investment styles — consistently and demonstrably adds value over market cycles.The six dimensions of diversification identified in this guide — asset class, geography, sector, market capitalisation, investment style, and time (through pound-cost averaging) — each contribute independently to portfolio resilience. Most UK investors, according to the Market Financial Solutions July 2025 survey, have meaningful concentrations in domestic cash and equities while underweighting bonds, international equities, and commodities. The single most impactful improvement available to most UK investors is simple: replace domestic equity concentration with a low-cost global equity index fund — immediately gaining exposure to 1,500 to 3,500 companies across over 40 countries at an annual cost well below 0.5%. The UK represents under 4% of global market capitalisation. A UK-only equity investor has, by construction, ignored 96% of the world's investable opportunities.

Markowitz's 'free lunch' metaphor holds up over seven decades of evidence. Diversification does not guarantee profits or prevent all losses — systematic risk affects all portfolios and cannot be eliminated, only managed through asset class breadth. But for the specific risks that investors can control — company-specific failures, sector disruptions, geographic concentration, style-cycle exposure — diversification provides a proven, low-cost, accessible mechanism for reducing volatility without proportionally reducing expected return. In a world where the US stock market concentration has reached levels unseen since 1932 and the 'anything but AI' rotation is underway in 2026, the case for genuine multi-dimensional diversification has rarely been stronger.

0 Comments Comments