Credits

Accountant Picks Best Credit Card Rewards in the UK: Complete Guide

Table of Contents

- Making Your Everyday Spending Work Harder

- How UK Reward Credit Cards Work

- Best UK Cashback Credit Cards: July 2026

- Best UK Points and Travel Reward Cards: July 2026

- The Amex Preferred Rewards Gold: The Recommended Starting Point for Most People

- How to Value UK Rewards Points: A Practical Guide

- Avios (British Airways Executive Club)

- Amex Membership Rewards Points

- Nectar Points

- How to Choose the Right Rewards Card for Your Spending Profile

- The Golden Rules: Making Reward Cards Pay, Not Cost

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Making Your Everyday Spending Work Harder

A rewards credit card turns every pound you would have spent anyway into something back — cashback in your account, Avios for a future flight, Nectar points for your weekly shop, or Membership Rewards points redeemable across airlines, hotels, and retailers. Used correctly — meaning the balance is cleared in full every month, so no interest is ever paid — a rewards credit card is one of the simplest and most consistently underused tools in UK personal finance.The UK rewards card market is dominated by American Express, which offers the strongest welcome bonuses, the highest ongoing earn rates, and the most flexible points currency in the market. The FCA's 0.3% interchange fee cap significantly limits what UK issuers can offer compared to the United States — where uncapped fees allow 2% to 5% cashback routinely — but it does not prevent meaningful returns for consistent users. A UK household spending £2,000 per month through the right Amex card can realistically earn £200 to £400 in value per year, plus the equivalent of a short-haul flight from welcome bonuses. The right Visa or Mastercard can generate £200 to £300 per year for those who prefer wider acceptance.

This guide covers the three main types of UK rewards cards — cashback cards, points and travel cards, and store loyalty cards — with the best July 2026 picks in each category. It explains how to value points and Avios, the critical golden rules that keep a rewards card profitable, how to choose between Amex and Visa/Mastercard, and how to stack rewards for maximum return. All welcome bonus information reflects July 2026 offers — bonuses change frequently, and you should always confirm the current offer directly with the provider before applying.

How UK Reward Credit Cards Work

A reward credit card works like a standard credit card with one additional mechanism: every time you make a purchase, the card earns a proportional reward — expressed either as a cashback percentage, a points accrual rate, or an airline miles rate. The reward is funded by the interchange fee that the retailer pays to accept the card payment. The UK's FCA interchange fee cap of 0.3% (compared to 2% or more in the US before their Durbin Amendment equivalent) is the primary reason why UK cashback rates cluster around 0.25% to 1%, while US cards routinely offer 2% to 5%. American Express operates outside this cap for certain charge card products, which is why Amex offers higher earn rates than Visa or Mastercard alternatives.There are three distinct reward mechanics to understand:

- Cashback: A percentage of your spending returned to your account as cash or a statement credit. The advantage is simplicity — there is no points currency to understand or track, no risk of devaluation, and no expiry. Cashback from cards like the Amex Platinum Cashback Everyday (0.5%), Chase UK (1%), and the fee-bearing Amex Platinum Cashback (up to 1.25%) lands directly and unambiguously on your account.

- Points and miles: Every pound of spending earns a number of points in a specific currency — Amex Membership Rewards points, Avios (British Airways), Virgin Points, Nectar points, Tesco Clubcard points, or Barclaycard Avios. Points can be redeemed for flights, hotel stays, shopping vouchers, or statement credit. Their value depends entirely on how you redeem them: Avios used for premium cabin flights can be worth 3p to 5p each; Avios used to top up a flight price are worth approximately 1p. Understanding the redemption value of your specific points currency before accumulating them is essential.

- Store and loyalty integration: Some cards — the John Lewis Partnership Card, the Amazon Barclaycard, the Nectar Amex — are specifically designed to boost earnings at a specific retailer or within a specific loyalty scheme. These produce higher earn rates at the target retailer but lower rates elsewhere, making them best suited to those who spend heavily with the specific partner.

The FCA interchange cap explained: UK cards typically offer 0.25–1% cashback vs 2–5% routinely available in the US — the FCA's 0.3% interchange fee cap limits what UK card issuers can offer through standard Visa and Mastercard products. American Express operates partly outside this cap, explaining why Amex consistently offers the strongest UK rewards rates. For Visa and Mastercard products, Chase UK's flat 1% is the strongest widely available cashback rate (Wallester / PocketWise 2026).

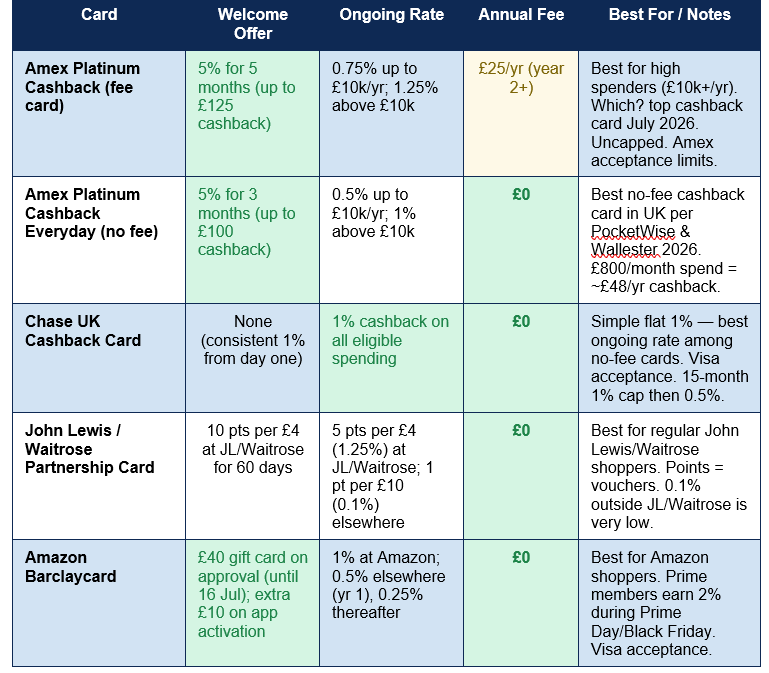

Best UK Cashback Credit Cards: July 2026

Cashback cards are the simplest and most reliable form of reward — no points currency to track, no redemption complexity, no expiry risk. The table below covers the best UK cashback credit cards as of July 2026, sourced from Which? (data correct to 1 July 2026), Money to the Masses (updated 6 days ago), PocketWise (May 2026), and Wallester (2026):

Why Amex dominates cashback — and its key limitation: American Express consistently offers the highest cashback rates in the UK because it operates partly outside the FCA's 0.3% interchange fee cap on standard credit card transactions, allowing it to fund higher reward rates. The trade-off is acceptance: American Express is not accepted at all UK retailers. Major supermarkets, most restaurants, and online retailers accept Amex — but some smaller merchants, budget airlines, and petrol stations do not. For anyone who primarily spends at major UK retailers, Amex acceptance is rarely a problem in practice. For those who regularly spend where Amex is not taken, Chase UK's flat 1% Visa card provides the strongest alternative.

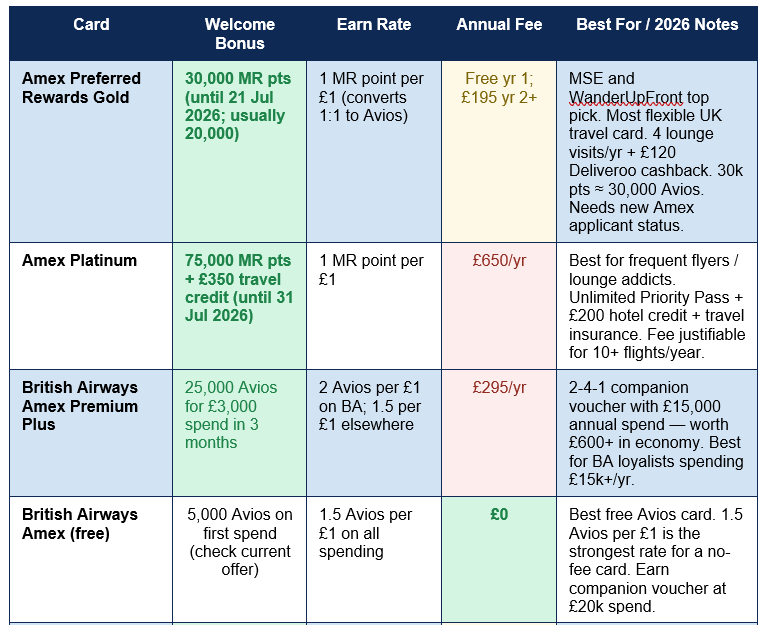

Best UK Points and Travel Reward Cards: July 2026

Points and miles cards can deliver significantly more value than cashback when points are redeemed strategically — particularly for premium cabin flights, where Avios or Membership Rewards points can be worth 3p to 5p each rather than the approximately 1p a cashback card pays. The catch is effort: you have to choose a card aligned to a specific programme, collect consistently, and redeem smartly. The table below covers the best UK points and travel reward cards as of July 2026. Welcome bonuses shown are those available as of publication — these change frequently, and several major bonuses in the table are time-limited. Always confirm current terms directly with the provider:

TIME-SENSITIVE OFFERS IN JULY 2026: The Amex Preferred Rewards Gold 30,000 MR points welcome bonus (up from the usual 20,000) runs until 21 July 2026. The Amex Platinum 75,000 points + £350 travel credit offer runs until 31 July 2026. The Amazon Barclaycard £40 welcome gift card runs until 16 July 2026. These enhanced bonuses represent materially better value than the standard offers. If any of these cards match your profile, applying before their respective deadlines captures the full elevated welcome bonus.

The Amex Preferred Rewards Gold: The Recommended Starting Point for Most People

MoneySavingExpert, WanderUpFront, GetSmartSaver, and Money to the Masses all converge on the same recommendation for most UK consumers entering the rewards card space for the first time: the American Express Preferred Rewards Gold. Understanding why helps clarify what makes a good rewards card in the current UK market.The Amex Gold earns one Membership Rewards (MR) point per £1 spent. MR points are the most flexible rewards currency in the UK — they transfer at 1:1 to Avios (British Airways, Qatar, Iberia, Aer Lingus, and others), to Virgin Atlantic Flying Club points, to Air France/KLM Flying Blue, and to multiple hotel programmes including Marriott Bonvoy, Hilton Honors, and Radisson Rewards. This flexibility means you accumulate points without committing to a specific airline or hotel — and you decide the best redemption when your points pot is large enough.

The July 2026 welcome bonus of 30,000 MR points (50% more than the standard 20,000 — valid until 21 July 2026) is worth approximately 30,000 Avios — enough for a return short-haul economy flight on British Airways to most European destinations outside peak periods, or a significant contribution toward a long-haul redemption. The card is free in year one, with a £195 fee applying from year two. Ongoing benefits include four complimentary airport lounge visits per year and up to £120 per year in Deliveroo cashback (£5 back per month on two qualifying orders). For cardholders who use these benefits, they meaningfully offset the year-two fee.

The 24-month rule is the critical eligibility requirement: you do not qualify for the welcome bonus if you have held any personal American Express card (including the Nectar Amex, the BA Amex, or any charge card) in the previous 24 months. Business Amex cards do not count against you. If you are approaching this card and have held any personal Amex recently, wait until the 24-month anniversary passes before applying, to capture the full welcome bonus.

How to Value UK Rewards Points: A Practical Guide

One of the most common mistakes in UK credit card rewards is accumulating points without understanding what they are actually worth — and therefore making poor redemption decisions. The following valuations reflect the practical 2026 market:Avios (British Airways Executive Club)

Avios are the UK's most widely used airline reward currency and are earned from British Airways flights, the BA Amex, the Barclaycard Avios, and convertible from Nectar points and Amex MR points. The value of an Avios depends entirely on how they are redeemed. A rough framework: approximately 1p per Avios for short-haul economy redemptions; 1p to 1.5p for business class short-haul; 2p to 4p or more for long-haul business or first class redemptions where Avios go furthest relative to cash prices. The headline rule from GetSmartSaver's 2026 guide is to treat Avios as worth approximately 1p each unless you have a specific plan to redeem them for premium cabin flights, where the value climbs materially higher.Amex Membership Rewards Points

MR points convert 1:1 to Avios, making them worth at least 1p each under the Avios framework above. They also convert to Virgin Points (1:1), Flying Blue miles (1:1), and multiple hotel programmes. The flexibility of MR points means they have option value beyond pure Avios — you can hold them and transfer to whichever programme offers the best redemption at the point you want to travel. MR points expire if your Amex account is closed, making it important to redeem before cancelling any card that earns them.Nectar Points

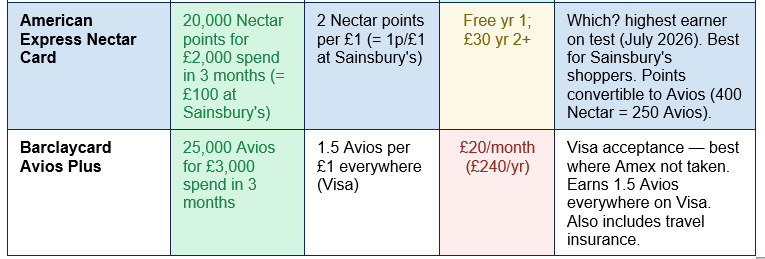

Nectar points earned via the American Express Nectar card are worth 0.5p each when redeemed at Sainsbury's, Argos, or other Nectar partners — effectively making the Nectar Amex's 2 points per £1 earn rate equivalent to 1p cashback per £1, directly competitive with Chase UK's flat 1%. Nectar points can also be converted to Avios at 400 points to 250 Avios — a rate of 0.625 Avios per Nectar point, making them slightly less valuable when converted to Avios than earned at face value. For Sainsbury's shoppers who also stack their Nectar card with the Amex Nectar card, the combined earn rate at Sainsbury's becomes meaningfully higher.How to Choose the Right Rewards Card for Your Spending Profile

The right UK rewards card depends on your monthly spending level, your willingness to manage a points programme, your acceptance requirements, and whether you travel by air enough for travel-specific rewards to make sense. The following framework maps common profiles to the optimal card:- Simplest cashback, no annual fee, Visa acceptance: Chase UK (1% on all eligible spending, Visa). Flat rate, no tracking, no redemption, cash in your account. The strongest no-fee cashback Visa in the UK market.

- Best no-fee cashback card overall: Amex Platinum Cashback Everyday (5% for 3 months, then 0.5%/1%). Best Amex acceptance and willing to maximise intro bonus.

- High spender (£10,000+ per year), cashback focused: Amex Platinum Cashback (fee card) at 1.25% above £10k, uncapped. The annual fee (£25/yr) is negligible against the higher earn rate.

- Flexible travel rewards, first Amex card, want the biggest welcome bonus: Amex Preferred Rewards Gold (30,000 MR points welcome until 21 July, free year 1, 4 lounge visits, Deliveroo cash). The natural starting point.

- Committed BA flyer spending £15,000+ per year on a card: BA Amex Premium Plus (2-4-1 companion voucher with £15k spend — worth £600+ in economy or several thousand in business).

- Sainsbury's/Nectar ecosystem shopper: American Express Nectar (20,000 Nectar points welcome = £100 at Sainsbury's; 2 Nectar points per £1 ongoing; Which?'s highest earner on test).

- Avios earner who needs Visa acceptance: Barclaycard Avios Plus (1.5 Avios per £1 everywhere on Visa; monthly fee of £20; includes travel insurance).

The Golden Rules: Making Reward Cards Pay, Not Cost

A reward card earns money only for cardholders who follow the fundamental rules. For anyone who breaks them, the rewards are instantly wiped out — and then some — by interest and fees:- Clear the full balance every single month: This is the cardinal rule, stated identically by every source reviewed for this guide. Reward rates of 0.5% to 1.5% are completely negated by interest rates of 24% to 35.8% APR if any balance is carried. Set up a direct debit for the full statement balance, not the minimum, immediately on receiving the card. The reward only exists if you never pay interest.

- Never use a rewards card for cash withdrawals: Cash advances are not covered by any reward programme and attract immediate interest at a high rate from the day of withdrawal, plus a cash advance fee. Reward cards are for purchases only.

- Track welcome bonus requirements precisely: Most welcome bonuses require a specific minimum spend within a specific time window — typically 3 months. Plan your spending so the required threshold is met organically, through spending you would make anyway. Overspending specifically to trigger a bonus is counterproductive.

- Subtract the annual fee before calculating net reward value: A card earning 1% on £10,000 annual spend produces £100 in rewards. If it charges a £150 annual fee, the net reward is negative £50. Always subtract the annual fee from the total expected reward value before judging whether a card is worth holding. GetSmartSaver's 2026 guide recommends treating this as a sensible rule of thumb before committing to any fee-bearing card.

- Check the 24-month Amex rule before applying: If you have held any personal American Express card in the previous 24 months, you will not receive the welcome bonus. This rule applies across the Gold, Platinum, and Green cards. Plan the sequence of Amex applications to maximise lifetime welcome bonus capture — for example, applying for the no-fee BA Amex (which does not share the 24-month exclusion with MR-earning cards) at a different point in the cycle.

- Understand your points' expiry rules: Points can expire if there is inactivity on your account. Avios expire after 36 months of inactivity in your BA Executive Club account. Amex MR points expire when you close your Amex account. Nectar points expire after 2 years of inactivity. Keep accounts active and monitor points to avoid losing accumulated value.

THE ONE RULE THAT MAKES OR BREAKS REWARD CARDS: Never carry a balance on a rewards credit card. A 1% reward rate on a £1,000 purchase earns £10. Carrying that £1,000 at 24.9% APR for one month costs £20.75. You are paying more in interest for one month than you earned in rewards on the entire purchase. If you ever find yourself unable to clear the full balance, stop using the reward card for new spending and consider a 0% balance transfer card to clear the outstanding amount before resuming. The reward is only real for those who never pay interest.

Conclusion

The UK rewards credit card market in July 2026 offers genuine value for cardholders who use it correctly — with the right card, clearing the balance in full monthly, and redeeming points strategically. American Express dominates the rewards landscape, offering the strongest welcome bonuses (30,000 MR points on the Gold until 21 July, 75,000 points plus £350 travel credit on the Platinum until 31 July), the highest ongoing earn rates, and the most flexible points currency. Which?'s July 2026 analysis found the American Express Nectar card earns the most consistently of all cards tested, while MoneySavingExpert and WanderUpFront both identify the Amex Preferred Rewards Gold as the strongest starting point for first-time rewards card holders.For those who need wider acceptance than Amex provides, Chase UK's flat 1% cashback on Visa is the strongest no-fee Visa alternative in 2026. For BA loyalists who spend heavily, the BA Amex Premium Plus and its 2-4-1 companion voucher provides the market's most valuable single benefit for cardholders spending £15,000 or more per year. For Sainsbury's shoppers, the Nectar Amex's 2 points per £1 (equivalent to 1p per £1 at Sainsbury's) and its 20,000-point welcome bonus make it the highest-return option for grocery-focused spending.

The critical discipline across every card in this guide is the same: clear the full balance every month. A reward rate of 0.5% to 1.5% is a genuine benefit when no interest is paid. Against an average credit card APR of 35.8%, even a month of carried balance wipes out months of rewards. Set up the direct debit for the full balance, not the minimum, on the day you receive the card. Everything else — choosing between Amex and Visa, between cashback and points, between the Gold and the Platinum — is secondary to this single foundational discipline.

Frequently Asked Questions (FAQ)

What is the best UK reward credit card in July 2026?

It depends on your spending profile and what you want from rewards. For flexible travel rewards with the strongest welcome bonus for new Amex applicants, the American Express Preferred Rewards Gold (30,000 MR points welcome until 21 July, free year one) is the most recommended starting point per MoneySavingExpert, WanderUpFront, and GetSmartSaver. For the highest consistent cashback with no annual fee and Visa acceptance, Chase UK's 1% flat rate card is the strongest. For Sainsbury's shoppers, Which?'s July 2026 testing identifies the American Express Nectar card as the highest earner. For BA loyalists spending £15,000+ per year, the BA Amex Premium Plus and its 2-4-1 companion voucher provides the strongest annual benefit value.How much cashback can I realistically earn from a UK reward card?

For a household spending approximately £800 per month through a no-fee rewards card, realistic annual cashback ranges from approximately £48 (Amex Cashback Everyday at 0.5%) to approximately £96 (Chase UK at 1%). For higher spenders — £2,000 per month — the range rises from approximately £120 (0.5% cards) to approximately £240 (1% cards) per year. Points cards can deliver more if points are redeemed for premium travel: the Amex Gold's 30,000 MR points welcome bonus alone is worth approximately £300 in flight redemptions at 1p per point, earned simply by opening the card and spending at your normal rate. The critical point from PocketWise's 2026 analysis: £800/month at 0.5% = £48/year cashback — meaningful, but only genuinely valuable if you never pay interest.How much are Avios worth on a UK credit card?

Avios value depends entirely on how you redeem them. For short-haul economy redemptions on British Airways, a rough guide is approximately 1p per Avios. For business class short-haul, 1p to 1.5p. For long-haul business or first class, where the cash price of tickets is highest, Avios can be worth 3p to 5p or more per point. GetSmartSaver's 2026 guide recommends treating Avios as worth approximately 1p each as a conservative base, and only planning above this when you have a specific premium cabin redemption in mind. At 1p per Avios, the Amex Gold's 30,000 welcome bonus is worth approximately £300; the BA Amex Premium Plus's 25,000 Avios welcome is worth approximately £250 at minimum.Why does American Express offer better rewards than Visa and Mastercard in the UK?

American Express operates partly outside the FCA's 0.3% interchange fee cap that applies to standard consumer credit card transactions on Visa and Mastercard networks. This cap significantly limits the interchange revenue that Visa and Mastercard issuers receive from retailers, which in turn limits the reward rates they can fund. American Express negotiates its own merchant acceptance terms and charges higher merchant fees in many cases, allowing it to fund higher reward rates and welcome bonuses. The trade-off is acceptance: not all UK merchants accept American Express, particularly some smaller retailers, budget airlines, and some petrol stations. For most spending at major UK retailers, supermarkets, and online merchants, Amex acceptance is not a significant practical constraint.Do reward credit cards affect my credit score?

Applying for a reward credit card will cause a small, temporary dip in your credit score due to the hard credit search. This typically recovers within 3 to 6 months of responsible card use. Used well — spending within your means, clearing the full balance every month, and staying well within your credit limit — a rewards card can actually improve your credit score over time by demonstrating consistent, on-time repayments and responsible credit management. Missing payments, carrying a high balance relative to your credit limit, or applying for multiple cards in quick succession can all harm your score. MoneySavingExpert notes that American Express reports to UK credit agencies in the same way as other card issuers, and responsible Amex use contributes positively to credit history.External References & Further Reading

1. Which? — Best Cashback and Reward Credit Cards July 2026 (Table correct to 1 July 2026)

https://www.which.co.uk/money/credit-cards-and-loans/credit-cards/best-credit-card-deals/best-cash-back-credit-cards-akfnR0Q4GK6X

2. Money to the Masses — Best UK Credit Cards for Rewards: July 2026 (Updated 6 days ago)

https://moneytothemasses.com/using-credit/credit-cards/which-are-the-best-rewards-credit-cards-in-the-uk

3. GetSmartSaver — Best Rewards Credit Cards UK 2026: Points, Miles and Perks (3 weeks ago)

https://getsmartsaver.co.uk/best-rewards-credit-cards-uk-2026/

4. PocketWise — Best Rewards Credit Cards UK 2026 (May 2026)

https://pocketwise.co.uk/credit-cards/best-cards/best-rewards-credit-cards-uk/

5. WanderUpFront — Best Travel Credit Cards UK 2026: Ranked for Miles, Lounges and Avios (June 2026)

https://wanderupfront.com/best-travel-credit-cards-uk-2026-ranked/

6. Head for Points — Best UK Avios and Airline Hotel Credit Cards (July 2026)

https://www.headforpoints.com/best-uk-avios-airline-hotel-credit-cards/

7. Forbes Advisor UK — Best Cashback and Rewards Credit Cards 2026

https://www.forbes.com/advisor/uk/credit-cards/best-cashback-and-reward/

0 Comments Comments