Credits

Best Interest Free Credit Cards UK & US: Complete Guide

Table of Contents

- Why 0% Credit Cards Matter More Than Ever in 2026

- What Is a 0% Interest Credit Card?

- Best UK Interest-Free Credit Cards: July 2026

- Best US 0% Interest Credit Cards: July 2026

- The Golden Rules: How to Use a 0% Card Without Getting Caught Out

- UK Only: Section 75 Protection — The Hidden Benefit of 0% Credit Cards

- Balance Transfer Cards in Depth: Clearing Existing Debt for Free

- How to Choose the Right 0% Card for Your Situation

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why 0% Credit Cards Matter More Than Ever in 2026

Credit card interest rates have reached a 20-year high in the UK. According to the most recent data from MoneyfactsCompare, the average APR across UK credit cards in 2026 stands at 35.8% — a figure that means anyone carrying a balance on a standard card is paying a rate that would have seemed extreme not long ago. In the United States, average credit card APRs remain elevated following the Federal Reserve's rate cycle, hovering in the mid-to-upper 20% range. Against this backdrop, a genuine 0% introductory period on a credit card is more valuable than it has been in a generation.A 0% purchase credit card lets you spread the cost of essential spending over months — or, in the best current UK deals, over two years — without paying a penny in interest, provided you follow the rules. A 0% balance transfer card lets you move existing high-interest debt to a new card where it accrues no interest for a defined period, giving you time to repay without the interest meter running. At 35.8% average APR, the value of avoiding that interest on a £5,000 balance for 36 months is the difference between paying approximately £5,370 in interest over three years or paying nothing. That is the concrete financial value of the best balance transfer deals currently on the market.

This guide covers the best interest-free credit cards in both the UK and US as of July 2026, how each type of 0% card works, the golden rules that protect you from losing the 0% deal and ending up worse off, how to calculate your monthly repayments to clear the balance in time, and how to choose between the different options — including whether to go for the longest period, the lowest post-deal APR, or the best added rewards.

What Is a 0% Interest Credit Card?

A 0% interest credit card is a credit card that charges no interest on purchases, balance transfers, or both during a defined introductory period — typically between 3 and 26 months in the UK, and between 15 and 21 months in the US. The 0% rate is a promotional offer for new customers; it does not last forever. When the promotional period ends, the card reverts to its standard variable APR — which for most 2026 UK cards is approximately 24.9%, and for most US cards is in the range of 17% to 28%.There are two main types of 0% credit card, and understanding the distinction determines which is right for you:

- 0% purchase cards: Designed for new spending. You use the card to pay for purchases — furniture, home improvements, a holiday, a large appliance — and pay no interest on that spending during the introductory period. As long as you clear the full balance before the 0% period ends, you have borrowed completely interest-free. The card does not usually offer 0% on balance transfers from other cards.

- 0% balance transfer cards: Designed for clearing existing debt. You transfer the outstanding balance from one or more existing credit cards (or in some cases loans) to the new card. The transferred balance accrues no interest during the 0% period, giving you time to clear it without the interest compounding. A balance transfer fee — typically 3% to 3.5% in the UK — is charged on most deals, though some fee-free options exist for shorter periods.

Some cards — often called all-in-one or dual 0% cards — offer introductory 0% periods on both purchases and balance transfers, though typically at slightly shorter terms than specialist cards for each purpose. These are useful if you both have existing debt to clear and anticipate significant new spending.

Why 0% cards matter so much in 2026: UK average credit card APR hits 35.8% — a 20-year high — MoneyfactsCompare data cited by Yahoo Finance and The Independent (April 2026) shows the average APR across UK credit cards at 35.8% — the highest in two decades. At this rate, a £3,000 balance left on a standard credit card for 12 months costs approximately £1,074 in interest. A 0% card for the same period costs nothing, provided the balance is cleared before the 0% deal expires

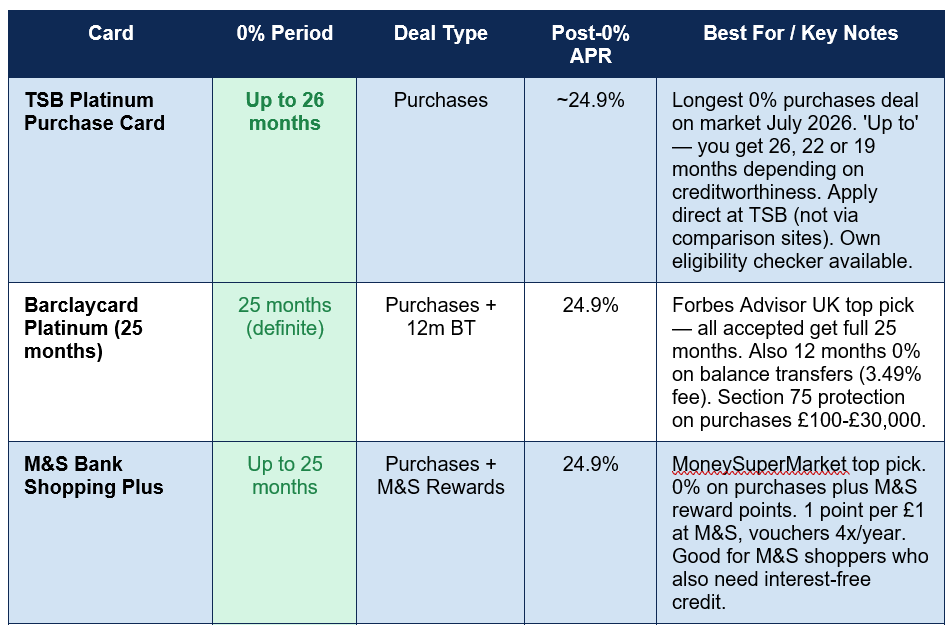

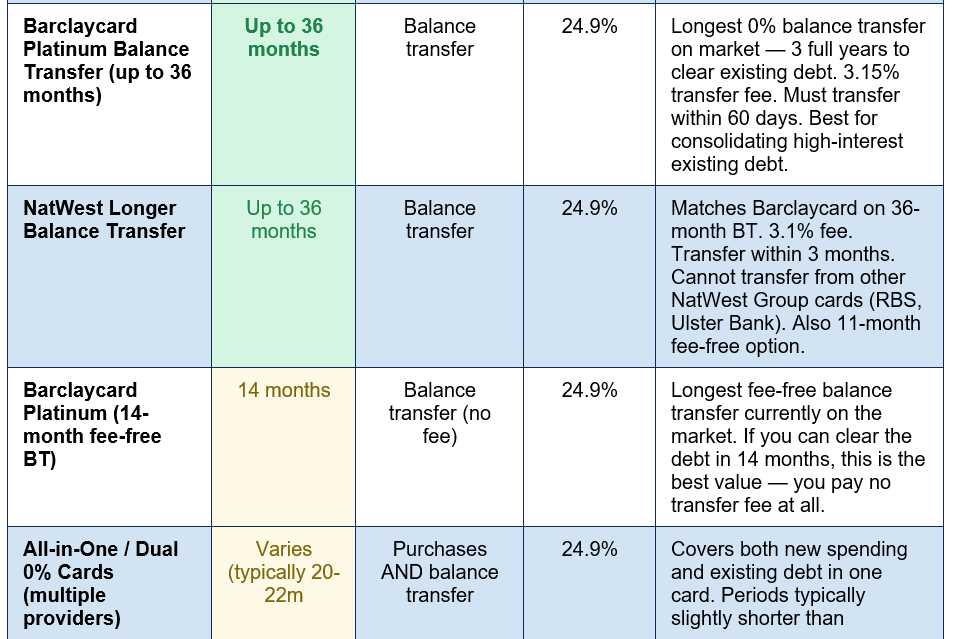

Best UK Interest-Free Credit Cards: July 2026

Which? surveyed 4,995 customers and compared 137 credit cards across the UK market (data correct to 1 July 2026) to identify the best 0% deals. MoneySavingExpert and Forbes Advisor UK updated their own rankings in the first week of July 2026. The table below consolidates the best UK 0% credit cards available in July 2026:

The 'up to' vs 'definite' distinction matters: Some 0% cards advertise their headline period as 'up to' a number of months — meaning different applicants receive different deals depending on their creditworthiness. TSB's 26-month headline is 'up to'; you might receive 26, 22, or 19 months. Barclaycard's 25-month period is described as 'definite' by MoneySavingExpert — all accepted applicants receive the full 25 months. If you have a good credit score and value certainty, a 'definite' deal is more predictable. Both TSB and most other providers now offer soft search eligibility checkers that tell you what period you will receive before you submit a full application — with no impact on your credit score. Always use these first.

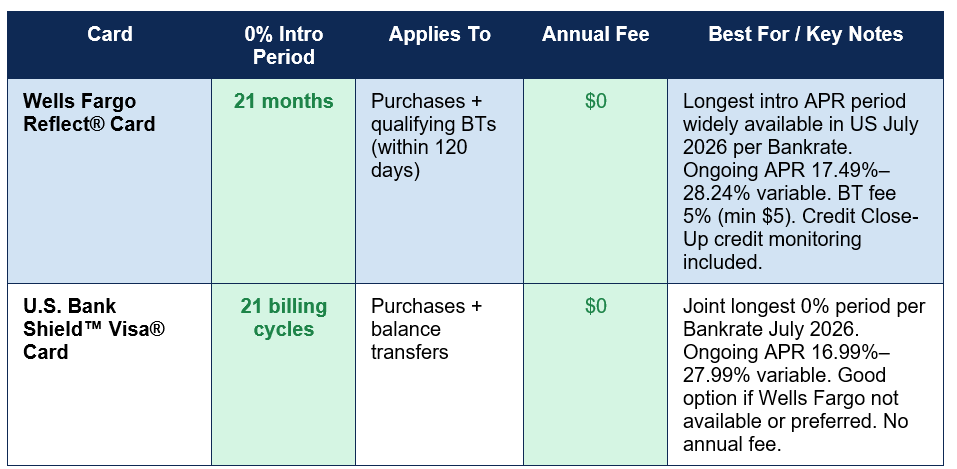

Best US 0% Interest Credit Cards: July 2026

In the United States, the longest 0% introductory APR periods available in July 2026 hover around 21 months, according to Bankrate's July 2026 rankings. Unlike the UK market where many 0% cards have no annual fee but post-0% APRs cluster around 24.9%, the US market features more variation in ongoing APRs (ranging from around 17% to 28%) and more integration of rewards programmes alongside the 0% intro period. The table below covers the best US 0% credit cards as of July 2026:

US vs UK COMPARISON NOTE: The UK 0% market currently offers significantly longer introductory periods (up to 36 months on balance transfers) than the US market (capped at around 21 months). UK post-0% APRs also tend to cluster around 24.9%, while US ongoing APRs show more variation (16.99% to 28.24%). US cards more frequently bundle meaningful rewards (5% category cash back, points, sign-up bonuses) alongside the 0% intro period, making them potentially more valuable for ongoing use after the intro period ends.

The Golden Rules: How to Use a 0% Card Without Getting Caught Out

Interest-free credit cards are genuinely powerful financial tools when used correctly — and genuinely expensive traps when used incorrectly. The same card that saves you hundreds of pounds in interest over two years can cost you significantly more if you miss a payment or fail to clear the balance in time. Every major consumer finance source — MoneySavingExpert, Forbes Advisor, Which?, Uswitch, Bankrate — emphasises the same core rules:- Set up a direct debit for at least the minimum repayment immediately on acceptance: Miss a single monthly minimum payment and most issuers will cancel your 0% deal immediately, reverting the entire balance to the standard APR. A single missed payment can also be recorded on your credit file. Set up an automatic direct debit as the first thing you do after being accepted — not as something you plan to do when you get round to it.

- Calculate the monthly repayment needed to clear the balance in time: Divide your total balance (or the total planned spending) by the number of months in the 0% period. This is your target monthly payment. For a £3,000 purchase on a 24-month 0% card: £3,000 ÷ 24 = £125 per month. Set up a direct debit for this amount, not just the minimum. Uswitch provides a 0% purchase card calculator to do this automatically.

- Set a calendar reminder for 1 month before the 0% period ends: Mark the exact date your 0% deal expires in your calendar with a reminder one month before. If you still have a balance approaching that date, either pay it off in full or apply for a 0% balance transfer card to carry the remaining balance forward without interest. Never wait until the day the rate reverts.

- Never use the card to withdraw cash: Cash withdrawals on a 0% purchase card are not included in the 0% deal. They attract immediate interest (typically at a much higher rate) from the day of withdrawal, plus a cash advance fee. Both apply even during the 0% promotional period. These cards are for purchases only — never for cash.

- Do not use a 0% purchase card for balance transfers (and vice versa): A 0% purchase card will charge a balance transfer fee and offer less favourable terms on transferred balances than a specialist balance transfer card. A 0% balance transfer card is for clearing existing debt, not for making new purchases. Match the card to the need it is designed for.

- Check eligibility before applying: A hard credit search (a full credit application) leaves a mark on your credit file and can affect your score if multiple applications are made in a short period. All major UK card providers and most US providers now offer soft search eligibility tools — use them to check your likelihood of acceptance before submitting a full application.

WHAT HAPPENS WHEN THE 0% PERIOD ENDS: If you have any remaining balance when the introductory period expires, it immediately starts accruing interest at the card's standard APR — typically 24.9% in the UK, or 17%-28% in the US. At these rates, a £2,000 remaining balance can accumulate £498 per year in interest (at 24.9%). If you cannot clear the full balance in time, apply for a new 0% balance transfer card before the period ends to carry the balance forward interest-free. Do not assume you can deal with this later — the revert APR applies from day one of the next statement period after the 0% deal expires.

UK Only: Section 75 Protection — The Hidden Benefit of 0% Credit Cards

One of the most valuable and least-publicised features of 0% purchase credit cards in the UK is Section 75 of the Consumer Credit Act 1974. Under Section 75, any purchase of more than £100 and up to £30,000 made on a credit card is protected: if the goods or services are faulty, not as described, or not delivered, and the retailer fails to resolve the issue, you can make an identical claim against the credit card company. The card issuer is jointly liable with the retailer.This protection applies even if you paid only part of the purchase price on the credit card. Buying a £1,500 sofa and paying £101 on your 0% credit card and the rest by bank transfer means the entire £1,500 purchase is protected by Section 75 — you only needed to put £1 over the £100 threshold on the card to trigger full coverage. This makes 0% purchase cards not just a zero-cost borrowing tool but also a meaningful consumer protection mechanism for large purchases from retailers who might otherwise dispute or be unable to fulfil refund claims.

Section 75 is a UK-specific protection with no direct US equivalent, though US credit cards offer chargeback rights (typically 120 days from the transaction) and some premium cards offer purchase protection insurance. For UK consumers, the combination of 0% interest-free borrowing and Section 75 protection makes a 0% purchase credit card the most sensible way to pay for any planned purchase over £100.

Balance Transfer Cards in Depth: Clearing Existing Debt for Free

A 0% balance transfer card is specifically designed for people who already have credit card debt accruing interest at a standard APR. The mechanism is straightforward: you apply for a new 0% balance transfer card, and within the specified window (typically 60 to 90 days of opening the account), you request to transfer some or all of your existing card balances to the new card. The new card pays off your old card(s) and you now owe the money to the new provider — at 0% interest for the promotional period.The critical calculation is the balance transfer fee versus the interest you would otherwise pay. The Barclaycard Platinum 36-month deal charges a 3.15% balance transfer fee. On a £5,000 balance, this fee is £157.50. At the average UK APR of 24.9% (close to the 35.8% average for those on non-promotional deals), that same £5,000 balance would accrue approximately £1,245 in interest in the first year alone, or approximately £3,735 over 36 months. The fee of £157.50 is a compelling price for avoiding £3,735 in interest — a net saving of over £3,577.

For the fee-free 14-month Barclaycard Platinum option, the same £5,000 balance saves even more in total because there is no transfer fee — but only if you can clear the full balance within 14 months (requiring approximately £357 per month). The choice between the long-fee and short-free-fee options depends entirely on whether you can realistically clear the balance within the shorter window.

How to Choose the Right 0% Card for Your Situation

The right 0% card depends on what you are trying to achieve. The following framework maps common financial situations to the appropriate card type:

- You want to make a large essential purchase (home improvement, appliance, holiday, car repair) and spread the cost over 1-2 years: A 0% purchase card with the longest period you qualify for. In the UK, target TSB (up to 26 months) or Barclaycard (25 months definite). In the US, target Wells Fargo Reflect or U.S. Bank Shield (both 21 months). Calculate the monthly repayment to clear the balance before the period ends.

- You have existing credit card debt accruing interest at a high APR and want to stop the interest: A 0% balance transfer card. In the UK, Barclaycard Platinum (up to 36 months, 3.15% fee) or NatWest (up to 36 months, 3.1% fee) are the strongest options. If you can clear in 14 months, the fee-free Barclaycard offer saves even more. Balance transfers typically cannot be made between cards from the same banking group.

- You have both existing debt AND expect new spending: An all-in-one card that offers 0% on both purchases and balance transfers. The 0% periods will typically be shorter than specialist cards, so consider whether the dual purpose justifies the shorter window.

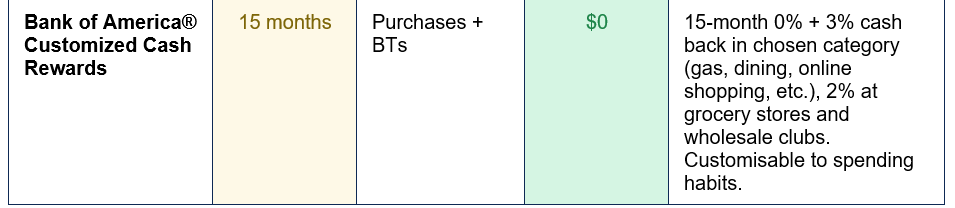

- You want 0% intro plus ongoing long-term rewards (US only): Chase Freedom Unlimited (15 months 0% + strong ongoing 5%/3%/1.5% cash back) or Discover it Cash Back (15 months 0% + Cashback Match first year) are the best options for those who want value beyond the intro period as well as short-term interest-free access.

ELIGIBILITY CHECK FIRST, APPLY SECOND: In both the UK and US, applying for multiple credit cards in quick succession leaves multiple hard searches on your credit file and can lower your credit score, making subsequent applications less likely to succeed. Always use the soft search eligibility tools that most providers now offer before submitting any full application. In the UK, MoneySavingExpert's eligibility calculator shows your chances across multiple cards simultaneously. In the US, most major card providers offer pre-qualification tools on their websites.

Conclusion

Interest-free credit cards in July 2026 offer some of the most valuable short-to-medium-term borrowing available to consumers in both the UK and the US — at a time when standard credit card rates have reached generational highs. In the UK, the best 0% purchase deal extends to 26 months (TSB) and the best balance transfer deal to 36 months (Barclaycard Platinum and NatWest), against a backdrop of average APRs at a 20-year high of 35.8%. In the US, the longest available intro APR period reaches 21 months across Wells Fargo Reflect, U.S. Bank Shield, and Citi Diamond Preferred — all with no annual fee and the option to carry that 0% into both purchases and qualifying balance transfers.The mathematical case for using these cards for planned, essential spending is compelling. A £3,000 purchase spread over 24 months on a 0% card costs £125 per month and zero in interest. The same purchase on a standard card at 35.8% APR costs hundreds of pounds more. Section 75 protection in the UK adds a further layer of value, making a 0% credit card both cheaper and safer than paying by bank transfer or cash for purchases above £100.

The golden rules that make this work are simple and non-negotiable: set up a direct debit for at least the minimum on day one, calculate and pay the monthly amount needed to clear the balance before the 0% period expires, mark the end date in your calendar, never withdraw cash, and always use a soft search eligibility checker before making a full application. A 0% credit card used according to these rules is one of the most powerful tools in a consumer's financial toolkit. A 0% card used carelessly — with missed payments, balance left at the end of the period, or cash withdrawals — is an expensive mistake. The card itself is neutral; the rules determine which it becomes.

Frequently Asked Questions (FAQ)

What is the longest 0% interest credit card in the UK in 2026?

For purchases, the longest 0% deal available in the UK in July 2026 is TSB's Platinum Purchase Card, which offers up to 26 months at 0% on new spending. This is an 'up to' deal — accepted applicants receive either 26, 22, or 19 months depending on their creditworthiness. For a guaranteed full period, Barclaycard Platinum offers 25 months to all accepted applicants. For balance transfers, both Barclaycard Platinum and NatWest offer up to 36 months at 0% on transferred balances (with transfer fees of 3.15% and 3.1% respectively). Barclaycard also offers a fee-free balance transfer for up to 14 months — the longest fee-free balance transfer deal currently on the market.What happens if I miss a payment on a 0% credit card?

Missing even a single minimum monthly payment on a 0% credit card will typically result in losing your 0% promotional deal immediately. The card reverts to its standard APR (typically 24.9% in the UK, 17%-28% in the US) on the outstanding balance, and a late payment fee of around £12 in the UK is usually charged. The missed payment may also be recorded on your credit file, which can affect your credit score and your ability to obtain credit in the future. To prevent this, set up a direct debit for at least the minimum monthly repayment as soon as you are accepted — not as a future task, but immediately.What is the difference between a 0% purchase card and a 0% balance transfer card?

A 0% purchase card is designed for new spending — you use it to make purchases and pay no interest on them during the introductory period. A 0% balance transfer card is designed to help you clear existing credit card debt — you transfer the balance from one or more existing cards to the new card, where it accrues no interest during the promotional period. Most 0% purchase cards do not offer 0% on balance transfers (or offer it at shorter terms with higher fees), and most 0% balance transfer cards charge the standard APR on new purchases immediately. Some all-in-one cards offer 0% on both, but typically at shorter terms than specialist cards for each purpose.Can I withdraw cash on a 0% credit card?

Technically yes, but you should never do so unless it is a genuine emergency. Cash withdrawals are not covered by the 0% introductory deal on any 0% purchase card. Interest begins accruing on the cash withdrawal from the day you make it, typically at a rate higher than the card's standard APR, plus a cash advance fee (usually 3-5% in the UK, minimum £3). The 0% deal covers new purchases made with the card in shops, online, or at restaurants — not cash advances from ATMs or any equivalent cash transaction (including buying foreign currency, gift cards, or gambling transactions). Treat 0% purchase cards as cards to spend on purchases only.What is Section 75 protection and why does it matter for UK credit card users?

Section 75 of the UK Consumer Credit Act 1974 makes a credit card issuer jointly liable with a retailer for any purchase of more than £100 and up to £30,000. If the goods or services you purchased are faulty, not as described, or not delivered, and the retailer fails to resolve the issue, you can claim the full refund from your credit card company under Section 75 — regardless of how much of the purchase price you paid on the card. You only need to put a minimum of £1 over the £100 threshold on the card to trigger full protection on the entire purchase amount. This makes a 0% purchase credit card not just a zero-cost borrowing tool but also a consumer protection mechanism that significantly exceeds the protection offered by debit card or bank transfer payments for any significant purchase.External References & Further Reading

The following authoritative sources were used in researching this article and are recommended for further reading and live card comparisons:1. MoneySavingExpert — Best 0% Credit Cards: July 2026 (Updated 1 week ago)

https://www.moneysavingexpert.com/credit-cards/best-0-credit-cards/

2. Which? — Best Interest-Free Purchase Credit Cards (Data correct to 1 July 2026, 137 cards compared)

https://www.which.co.uk/money/credit-cards-and-loans/credit-cards/best-credit-card-deals/best-interest-free-credit-cards-aKZ701r6uXXP

3. Forbes Advisor UK — Best 0% Purchase Credit Cards (May 2026)

https://www.forbes.com/advisor/uk/credit-cards/best-0-purchase-credit-cards/

4. Bankrate US — Best 0% Intro APR Credit Cards: July 2026 (Updated 3 weeks ago)

https://www.bankrate.com/credit-cards/zero-interest/best-zero-interest-cards/

5. MoneySuperMarket — Compare Interest Free Credit Cards (Accurate to 30 June 2026)

https://www.moneysupermarket.com/credit-cards/compare-interest-free/

6. Uswitch — Compare 0% Purchase Credit Cards July 2026

https://www.uswitch.com/credit-cards/0-percent-purchase-credit-cards/

7. money.co.uk — Best 0% Interest-Free Credit Cards (Updated 5 days ago)

https://www.money.co.uk/credit-cards/0-purchases-credit-cards

8. Yahoo Finance / The Independent — UK Credit Card Interest Rates at 20-Year High (April 2026)

https://uk.finance.yahoo.com/news/best-0-balance-transfer-credit-142342351.html

0 Comments Comments