Real Estate

More Credit Score Options for Mortgages: What to Know

On April 22, 2026, the Federal Housing Finance Agency announced the most significant change to mortgage credit scoring in decades. VantageScore 4.0 is now live for Fannie Mae and Freddie Mac loans. FICO 10T is on the way. FHA is joining in. Here is everything a homebuyer needs to understand about what changed, why it matters, and what to do about it.

Specifically, Fannie Mae and Freddie Mac updated their selling policies to allow approved lenders to use VantageScore 4.0 effective immediately. FICO 10T — a second new model — was also approved and its full roll-out is expected to follow in the coming months, once historical score data for the model is published in summer 2026. The Federal Housing Administration (FHA), which insures mortgages for many first-time buyers, simultaneously announced it would also permit the use of both VantageScore 4.0 and FICO 10T for FHA-insured mortgage underwriting.

The Classic FICO score — the only model approved for use in conforming mortgage underwriting for the past few decades — remains valid. The change is additive, not a replacement. Lenders now have a choice: they can continue using Classic FICO, or they can opt to use VantageScore 4.0. Twenty-one large mortgage lenders formed the first wave of participants using VantageScore 4.0, with FHFA Director Pulte noting that Freddie Mac had already taken $10 million in loans approved using the new model within days of the announcement.

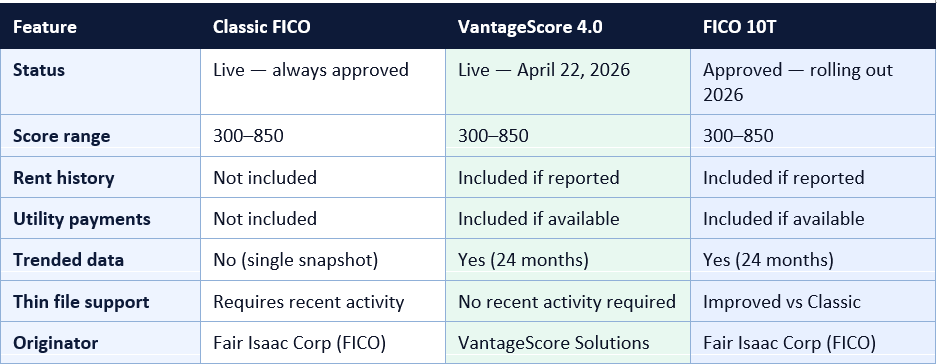

Classic FICO is the version of the FICO scoring model that has been in use since the 1990s. It generates scores on a scale of 300 to 850, based on five categories: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit (10%). It is a reliable model that has decades of data behind it, and most mortgage professionals understand its strengths and limitations well.

However, Classic FICO has significant blind spots. It does not consider a consumer's history of paying rent, utilities, phone bills, or subscription services — payments that hundreds of millions of Americans make reliably every month but which have no bearing on their Classic FICO score unless they miss a payment that gets sent to collections. It also takes a single-point-in-time snapshot of a borrower's credit behaviour rather than tracking trends over time.

This meant that many creditworthy Americans — particularly younger borrowers, recent immigrants, veterans who have relied mainly on cash and military pay rather than credit cards, and low-to-moderate-income earners who rent rather than own — were effectively invisible to or undervalued by the credit scoring system that gatekept homeownership. The Credit Score Competition Act, signed by President Trump in 2018 and implemented through subsequent FHFA rulemaking, was designed to address this problem by requiring the GSEs to validate and eventually permit alternative credit score models.

The two most significant differences from Classic FICO are its treatment of rental payment history and its use of trended data. On rent and utility payments: if a consumer's rent payments or utility bills are reported to the credit bureaus — either because the landlord reports them, because the tenant has enrolled in a service like Experian RentBureau or Self, or through other data-reporting channels — VantageScore 4.0 will incorporate that payment history into the score calculation. This is directly relevant to first-time homebuyers who have been renting for years but building their credit primarily through rent rather than credit cards or loans.

The trended data aspect means VantageScore 4.0 looks at your credit card balances and payment behaviour over the past 24 months, not just at a single point in time. This makes it possible to distinguish between a borrower who is actively paying down their credit card debt (a positive signal) and one who is steadily increasing their balances (a negative signal) — even if both have the same balance on the day their credit is checked. A borrower who has been methodically reducing their debt for two years may score meaningfully higher under VantageScore 4.0 than under Classic FICO, which would see only the current balance.

VantageScore 4.0 also removes the requirement for recent credit activity that Classic FICO imposes. Classic FICO requires at least one account opened within the last six months and at least one account that has been reported to the bureau in the last six months. VantageScore 4.0 eliminates this requirement, meaning that consumers with older credit histories who have not opened new accounts recently — including veterans who have been deployed or individuals who have lived abroad — may now be scoreable under VantageScore 4.0 even when they receive no score under Classic FICO.

We are modernizing credit scoring with more predictive models, helping millions of Americans who responsibly pay rent qualify for mortgages. That's fair, it's commonsense, and it's finally delivering the benefits of competition to homebuyers.

— FHFA DIRECTOR WILLIAM PULTE, APRIL 22, 2026

FICO 10T was validated and approved for use by the GSEs in October 2022, alongside VantageScore 4.0. However, its full implementation has been on a slower track. Historical FICO 10T credit score data — covering loans acquired between April 2013 and September 2025 — is expected to be published by the GSEs in summer 2026, and the full roll-out for lenders to originate loans using FICO 10T scores is expected to follow thereafter.

One practical implication of FICO 10T's trended data approach is that, unlike with Classic FICO, a short-term credit card paydown immediately before applying for a mortgage — a strategy some borrowers have used to boost their Classic FICO score quickly — will have less impact under FICO 10T. As credit expert John Ulzheimer noted in commentary around the announcement: under FICO 10T, borrowers will need to manage their credit card debt responsibly over time, not just in the month or two before putting in a mortgage application.

Under Classic FICO, a person who has paid their rent reliably for ten years gains absolutely nothing to their credit score from that track record. The same applies to utility bills, phone bills, and subscription services. Unless a payment is missed and sent to a collection agency, these payments are invisible to Classic FICO. This created a significant disadvantage for renters compared to homeowners, who automatically built credit through their mortgage payment history.

Under VantageScore 4.0, if rent and utility payments are reported to the credit bureaus, they can positively influence a credit score. This is conditional on the data being available — not all landlords report rent payments, and not all utility companies report to the bureaus. Tenants can take proactive steps to make this data available to lenders, including signing up for rent-reporting services such as Experian RentBureau, Self (formerly Self Lender), PayYourRent, or Rent Reporters. Some of these services are free; others charge a small monthly fee. For a renter with a thin traditional credit file, the investment can be well worth it if it results in a scoreable or higher credit score under the new models.

It is important to be realistic: rent-reporting services will only help if the payments being reported are on time. Late rent payments reported to the bureaus will negatively affect a VantageScore 4.0 score, just as a late mortgage payment would affect a Classic FICO score. But for consumers who have been consistently paying their rent on time — which research suggests is the case for the large majority of renters — this change opens a new and meaningful pathway to demonstrable creditworthiness.

The tri-merge credit reporting requirement — meaning lenders must pull credit reports from all three national credit bureaus (Equifax, Experian, and TransUnion) — remains in place for loans delivered to Fannie Mae and Freddie Mac. This was a deliberate decision by FHFA Director Pulte, who reversed a previous plan under his predecessor to move to a bi-merge (two-bureau) requirement. He has stated that maintaining the tri-merge requirement keeps costs and complexity manageable during the transition period.

Classic FICO scores remain fully valid and approved for all GSE loans. No lender is required to switch to VantageScore 4.0 — it is an option available to those who choose to use it. Lenders not participating in the initial limited roll-out must continue to use Classic FICO scores through a tri-merge credit report until VantageScore 4.0 is made broadly available to all. Borrowers applying for mortgages with lenders who have not yet adopted VantageScore 4.0 will still be evaluated using Classic FICO.

The minimum credit score requirements for conventional loans, FHA loans, and other programme types also remain the same for now. Approval thresholds, loan-to-value requirements, debt-to-income ratios, and other underwriting standards are separate from the credit scoring model question. FHFA Director Pulte indicated that separate pricing grids for VantageScore 4.0 loans would be released, suggesting that pricing and loan-level adjustments will be updated to reflect the new model's predictive characteristics as the roll-out matures.

If your lender is one of the 21 large mortgage lenders in the first wave, they now have the option — not the obligation — to use VantageScore 4.0 when evaluating your loan. They may still choose Classic FICO. If your VantageScore 4.0 is significantly higher than your Classic FICO — for example, because you have a strong rent payment history — it would be worth asking your loan officer which score model they will be using and whether switching to VantageScore 4.0 could affect your eligibility or rate.

If your lender is not yet in the initial roll-out group, Classic FICO will be used as normal. The broader roll-out of VantageScore 4.0 to all lenders is expected to proceed over the coming months, and FICO 10T will follow once the historical score data is published in summer 2026 and lenders receive advance notice of its full implementation date.

For homebuyers who are not yet at the application stage, this is an ideal time to check your credit standing under both Classic FICO and VantageScore 4.0. Free VantageScore checks are available through a number of bank apps, credit monitoring services, and sites like Credit Karma. Checking your score does not affect it. Understanding the difference between your Classic FICO and VantageScore 4.0 can help you decide whether to target lenders who are using the new model or take steps to improve your standing under both.

For the millions of Americans who have been reliably paying their rent, utilities, and bills but who have struggled to qualify for a mortgage because those payments did not count under Classic FICO, this change creates a genuine new pathway to homeownership. For borrowers who have been actively paying down debt, it rewards the behaviour rather than just the balance. And for the broader mortgage market, competition between approved credit score models is expected to drive down costs and improve the accuracy of risk assessment over time. If you are planning to buy a home, now is the time to check your VantageScore, talk to your lender about which model they use, and make sure your credit behaviour over the next 24 months reflects the world the mortgage market is moving toward.

TABLE OF CONTENTS

- What Happened on April 22, 2026

- A Decades-Long Monopoly: Why Classic FICO Dominated

- The Three Approved Credit Score Models Explained

- What VantageScore 4.0 Does Differently

- What FICO 10T Does Differently

- Why Rent and Utility Payment History Now Matters

- Who Benefits Most From the New Models

- What Stays the Same: Tri-Merge Reports and Classic FICO

- What This Means for Your Mortgage Application Right Now

- How to Prepare Your Credit Under the New Models

- Conclusion

- Frequently Asked Questions

- References

What Happened on April 22, 2026

On April 22, 2026, the US Federal Housing Finance Agency (FHFA) — the regulator that oversees Fannie Mae and Freddie Mac — made a joint announcement with the Department of Housing and Urban Development (HUD) that marks the most consequential change to mortgage credit scoring in decades. In a press conference, FHFA Director William Pulte and HUD Secretary Scott Turner confirmed that mortgage lenders would now have a choice of approved credit score models when originating loans sold to the government-sponsored enterprises (GSEs).Specifically, Fannie Mae and Freddie Mac updated their selling policies to allow approved lenders to use VantageScore 4.0 effective immediately. FICO 10T — a second new model — was also approved and its full roll-out is expected to follow in the coming months, once historical score data for the model is published in summer 2026. The Federal Housing Administration (FHA), which insures mortgages for many first-time buyers, simultaneously announced it would also permit the use of both VantageScore 4.0 and FICO 10T for FHA-insured mortgage underwriting.

The Classic FICO score — the only model approved for use in conforming mortgage underwriting for the past few decades — remains valid. The change is additive, not a replacement. Lenders now have a choice: they can continue using Classic FICO, or they can opt to use VantageScore 4.0. Twenty-one large mortgage lenders formed the first wave of participants using VantageScore 4.0, with FHFA Director Pulte noting that Freddie Mac had already taken $10 million in loans approved using the new model within days of the announcement.

A Decades-Long Monopoly: Why Classic FICO Dominated

To understand why this change is significant, it helps to understand how entrenched the Classic FICO model had become in American mortgage underwriting. For most of the past three decades, any loan sold to Fannie Mae or Freddie Mac — which together buy the majority of mortgages originated in the US — was required to be evaluated using a score generated by the Classic FICO model. This was not simply a market preference. It was effectively a regulatory requirement built into the GSEs' selling guidelines.Classic FICO is the version of the FICO scoring model that has been in use since the 1990s. It generates scores on a scale of 300 to 850, based on five categories: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit (10%). It is a reliable model that has decades of data behind it, and most mortgage professionals understand its strengths and limitations well.

However, Classic FICO has significant blind spots. It does not consider a consumer's history of paying rent, utilities, phone bills, or subscription services — payments that hundreds of millions of Americans make reliably every month but which have no bearing on their Classic FICO score unless they miss a payment that gets sent to collections. It also takes a single-point-in-time snapshot of a borrower's credit behaviour rather than tracking trends over time.

This meant that many creditworthy Americans — particularly younger borrowers, recent immigrants, veterans who have relied mainly on cash and military pay rather than credit cards, and low-to-moderate-income earners who rent rather than own — were effectively invisible to or undervalued by the credit scoring system that gatekept homeownership. The Credit Score Competition Act, signed by President Trump in 2018 and implemented through subsequent FHFA rulemaking, was designed to address this problem by requiring the GSEs to validate and eventually permit alternative credit score models.

The Three Approved Credit Score Models Explained

As of May 2026, there are three credit score models approved for use in Fannie Mae and Freddie Mac mortgage underwriting. Here is a plain-English guide to what each one is and how it differs.

What VantageScore 4.0 Does Differently

VantageScore 4.0 is the most current version of the VantageScore model, developed jointly by the three national credit bureaus — Equifax, Experian, and TransUnion. It was validated for use by Fannie Mae and Freddie Mac back in October 2022, but its full implementation has only now arrived with the FHFA's April 2026 announcement.The two most significant differences from Classic FICO are its treatment of rental payment history and its use of trended data. On rent and utility payments: if a consumer's rent payments or utility bills are reported to the credit bureaus — either because the landlord reports them, because the tenant has enrolled in a service like Experian RentBureau or Self, or through other data-reporting channels — VantageScore 4.0 will incorporate that payment history into the score calculation. This is directly relevant to first-time homebuyers who have been renting for years but building their credit primarily through rent rather than credit cards or loans.

The trended data aspect means VantageScore 4.0 looks at your credit card balances and payment behaviour over the past 24 months, not just at a single point in time. This makes it possible to distinguish between a borrower who is actively paying down their credit card debt (a positive signal) and one who is steadily increasing their balances (a negative signal) — even if both have the same balance on the day their credit is checked. A borrower who has been methodically reducing their debt for two years may score meaningfully higher under VantageScore 4.0 than under Classic FICO, which would see only the current balance.

VantageScore 4.0 also removes the requirement for recent credit activity that Classic FICO imposes. Classic FICO requires at least one account opened within the last six months and at least one account that has been reported to the bureau in the last six months. VantageScore 4.0 eliminates this requirement, meaning that consumers with older credit histories who have not opened new accounts recently — including veterans who have been deployed or individuals who have lived abroad — may now be scoreable under VantageScore 4.0 even when they receive no score under Classic FICO.

We are modernizing credit scoring with more predictive models, helping millions of Americans who responsibly pay rent qualify for mortgages. That's fair, it's commonsense, and it's finally delivering the benefits of competition to homebuyers.

— FHFA DIRECTOR WILLIAM PULTE, APRIL 22, 2026

What FICO 10T Does Differently

FICO 10T is Fair Isaac Corporation's newest mortgage credit score model, and it shares many of the same innovations as VantageScore 4.0. The 'T' stands for 'trended' — meaning the model incorporates 24 months of credit history data rather than the point-in-time snapshot used by Classic FICO. Like VantageScore 4.0, FICO 10T considers whether a borrower's credit card balances have been rising or falling over the past two years, which makes it a more dynamic and arguably more accurate predictor of future default risk.FICO 10T was validated and approved for use by the GSEs in October 2022, alongside VantageScore 4.0. However, its full implementation has been on a slower track. Historical FICO 10T credit score data — covering loans acquired between April 2013 and September 2025 — is expected to be published by the GSEs in summer 2026, and the full roll-out for lenders to originate loans using FICO 10T scores is expected to follow thereafter.

One practical implication of FICO 10T's trended data approach is that, unlike with Classic FICO, a short-term credit card paydown immediately before applying for a mortgage — a strategy some borrowers have used to boost their Classic FICO score quickly — will have less impact under FICO 10T. As credit expert John Ulzheimer noted in commentary around the announcement: under FICO 10T, borrowers will need to manage their credit card debt responsibly over time, not just in the month or two before putting in a mortgage application.

Why Rent and Utility Payment History Now Matters

For many potential homebuyers — particularly renters who have not yet started building traditional credit through loans and credit cards — the inclusion of rent payment history in VantageScore 4.0 and FICO 10T represents one of the most meaningful practical changes.Under Classic FICO, a person who has paid their rent reliably for ten years gains absolutely nothing to their credit score from that track record. The same applies to utility bills, phone bills, and subscription services. Unless a payment is missed and sent to a collection agency, these payments are invisible to Classic FICO. This created a significant disadvantage for renters compared to homeowners, who automatically built credit through their mortgage payment history.

Under VantageScore 4.0, if rent and utility payments are reported to the credit bureaus, they can positively influence a credit score. This is conditional on the data being available — not all landlords report rent payments, and not all utility companies report to the bureaus. Tenants can take proactive steps to make this data available to lenders, including signing up for rent-reporting services such as Experian RentBureau, Self (formerly Self Lender), PayYourRent, or Rent Reporters. Some of these services are free; others charge a small monthly fee. For a renter with a thin traditional credit file, the investment can be well worth it if it results in a scoreable or higher credit score under the new models.

It is important to be realistic: rent-reporting services will only help if the payments being reported are on time. Late rent payments reported to the bureaus will negatively affect a VantageScore 4.0 score, just as a late mortgage payment would affect a Classic FICO score. But for consumers who have been consistently paying their rent on time — which research suggests is the case for the large majority of renters — this change opens a new and meaningful pathway to demonstrable creditworthiness.

Who Benefits Most From the New Models

The FHFA has been explicit about the population of consumers it expects to benefit most from the shift to VantageScore 4.0 and FICO 10T. Several groups stand out as likely winners.First-time buyers and younger borrowers

Young adults who have been renting and building credit primarily through rent and utility payments, rather than through long credit card histories or installment loans, are among the most likely beneficiaries. Under Classic FICO, their lack of a long traditional credit history often results in a lower score than their actual financial behaviour warrants. Under VantageScore 4.0, their consistent rent payment record may be reflected in a higher and more accurate score.Thin-file consumers

Millions of Americans have what credit bureaus call a 'thin file' — too little credit history to generate a reliable Classic FICO score. VantageScore 4.0 explicitly eliminates the requirement for recent credit activity, meaning many thin-file consumers who were previously unscorable — and therefore automatically disqualified from most conventional mortgage programmes — may now receive a score and qualify for financing.Veterans and service members

Active military personnel and recently discharged veterans often have limited traditional credit histories because they have relied on military pay and cash rather than civilian credit products. VantageScore 4.0 and FICO 10T's broader data sources and relaxed activity requirements may produce scores for service members who currently receive no Classic FICO score, opening the door to conventional mortgage financing alongside their existing VA loan eligibility.Debt-reduction-minded borrowers

Consumers who have been actively paying down credit card debt over the past 24 months — even if their current balance is not dramatically lower — may benefit from the trended data approach of both new models. The direction of travel on debt matters in VantageScore 4.0 and FICO 10T, not just the destination.Who should check their VantageScore 4.0 before applying for a mortgage

- Renters who have been paying rent on time for at least 12 months and have enrolled in a rent-reporting service

- Borrowers with thin or no traditional credit history who have struggled to generate a Classic FICO score

- Veterans, active military, or anyone who has been living abroad or off the traditional credit grid

- Borrowers who have been actively paying down credit card or other debt over the past 24 months

- Recent immigrants who have US bank accounts and utility payments but limited credit card history

- Anyone who was previously told they had 'no score' or an insufficient score to qualify for a conventional mortgage

What Stays the Same: Tri-Merge Reports and Classic FICO

Despite the significance of the April 22 announcement, it is important to understand what has not changed — because several key features of the mortgage credit assessment process remain intact.The tri-merge credit reporting requirement — meaning lenders must pull credit reports from all three national credit bureaus (Equifax, Experian, and TransUnion) — remains in place for loans delivered to Fannie Mae and Freddie Mac. This was a deliberate decision by FHFA Director Pulte, who reversed a previous plan under his predecessor to move to a bi-merge (two-bureau) requirement. He has stated that maintaining the tri-merge requirement keeps costs and complexity manageable during the transition period.

Classic FICO scores remain fully valid and approved for all GSE loans. No lender is required to switch to VantageScore 4.0 — it is an option available to those who choose to use it. Lenders not participating in the initial limited roll-out must continue to use Classic FICO scores through a tri-merge credit report until VantageScore 4.0 is made broadly available to all. Borrowers applying for mortgages with lenders who have not yet adopted VantageScore 4.0 will still be evaluated using Classic FICO.

The minimum credit score requirements for conventional loans, FHA loans, and other programme types also remain the same for now. Approval thresholds, loan-to-value requirements, debt-to-income ratios, and other underwriting standards are separate from the credit scoring model question. FHFA Director Pulte indicated that separate pricing grids for VantageScore 4.0 loans would be released, suggesting that pricing and loan-level adjustments will be updated to reflect the new model's predictive characteristics as the roll-out matures.

What This Means for Your Mortgage Application Right Now

For the vast majority of homebuyers starting a mortgage application today, the practical impact of the April 22 changes depends on which lender they choose and whether that lender has enrolled in the initial VantageScore 4.0 roll-out.If your lender is one of the 21 large mortgage lenders in the first wave, they now have the option — not the obligation — to use VantageScore 4.0 when evaluating your loan. They may still choose Classic FICO. If your VantageScore 4.0 is significantly higher than your Classic FICO — for example, because you have a strong rent payment history — it would be worth asking your loan officer which score model they will be using and whether switching to VantageScore 4.0 could affect your eligibility or rate.

If your lender is not yet in the initial roll-out group, Classic FICO will be used as normal. The broader roll-out of VantageScore 4.0 to all lenders is expected to proceed over the coming months, and FICO 10T will follow once the historical score data is published in summer 2026 and lenders receive advance notice of its full implementation date.

For homebuyers who are not yet at the application stage, this is an ideal time to check your credit standing under both Classic FICO and VantageScore 4.0. Free VantageScore checks are available through a number of bank apps, credit monitoring services, and sites like Credit Karma. Checking your score does not affect it. Understanding the difference between your Classic FICO and VantageScore 4.0 can help you decide whether to target lenders who are using the new model or take steps to improve your standing under both.

How to Prepare Your Credit Under the New Models

Whether you are planning to buy a home in the next six months or the next few years, the shift toward VantageScore 4.0 and FICO 10T changes what optimal credit behaviour looks like for mortgage applicants. Here is a practical guide.Preparing your credit for the new mortgage scoring models

- Sign up for a rent-reporting service: If you rent and pay on time, enrol with Experian RentBureau, Self, PayYourRent, or Rent Reporters to have your rent history reported to the credit bureaus. This can positively affect your VantageScore 4.0.

- Manage credit card debt consistently over time: Under FICO 10T and VantageScore 4.0, the trend of your balances matters. A two-year track record of paying down debt is more valuable than a short-term paydown immediately before application.

- Check both your Classic FICO and VantageScore 4.0: Use AnnualCreditReport.com for free credit reports and Credit Karma or similar services to see your VantageScore. If there is a meaningful gap between the two, factor that into your lender search.

- Address errors on all three bureau reports: Since the tri-merge requirement remains in place, errors on any of the three bureaus' reports can affect your score. Dispute errors at Equifax, Experian, and TransUnion directly.

- Keep credit utilisation low over time: This matters under all three models. Aim to keep balances below 30% of credit limits across all cards — consistently, not just at the month end.

- Avoid unnecessary new credit applications in the 12 months before applying: Hard enquiries affect all three models. Apply for new credit sparingly as you approach a mortgage application.

- Ask your lender which model they use: Once you start shopping for a mortgage, ask loan officers directly whether they are using Classic FICO or VantageScore 4.0. This will affect whether your rent history and trended data work for or against you.

CONCLUSION

The April 22, 2026 announcement from FHFA and HUD represents the most significant shift in mortgage credit scoring in a generation. For the first time since the 1990s, lenders originating conforming loans have a genuine choice of approved credit score models — and the two new additions, VantageScore 4.0 and the soon-to-arrive FICO 10T, are meaningfully more sophisticated and more inclusive than the Classic FICO model they sit alongside.For the millions of Americans who have been reliably paying their rent, utilities, and bills but who have struggled to qualify for a mortgage because those payments did not count under Classic FICO, this change creates a genuine new pathway to homeownership. For borrowers who have been actively paying down debt, it rewards the behaviour rather than just the balance. And for the broader mortgage market, competition between approved credit score models is expected to drive down costs and improve the accuracy of risk assessment over time. If you are planning to buy a home, now is the time to check your VantageScore, talk to your lender about which model they use, and make sure your credit behaviour over the next 24 months reflects the world the mortgage market is moving toward.

0 Comments Comments