Finance

What Is Inflation? The Complete Guide

Table of Contents

- Why Inflation Matters to Every Household

- What Is Inflation?

- How Is Inflation Measured? CPI, CPIH, RPI and Core Inflation

- Types of Inflation and Measures: The Complete Reference

- What Causes Inflation? The Key Forces Driving Prices

- Demand-Pull Inflation

- Cost-Push Inflation

- Built-In Inflation (The Wage-Price Spiral)

- UK Inflation: The Complete Timeline 2020–2026

- The Bank of England's Role: How Interest Rates Fight Inflation

- How Inflation Affects UK Households: The Real-World Impact

- Purchasing Power Erosion

- Savings and Investments

- Mortgages and Borrowing

- How to Protect Your Finances from Inflation

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why Inflation Matters to Every Household

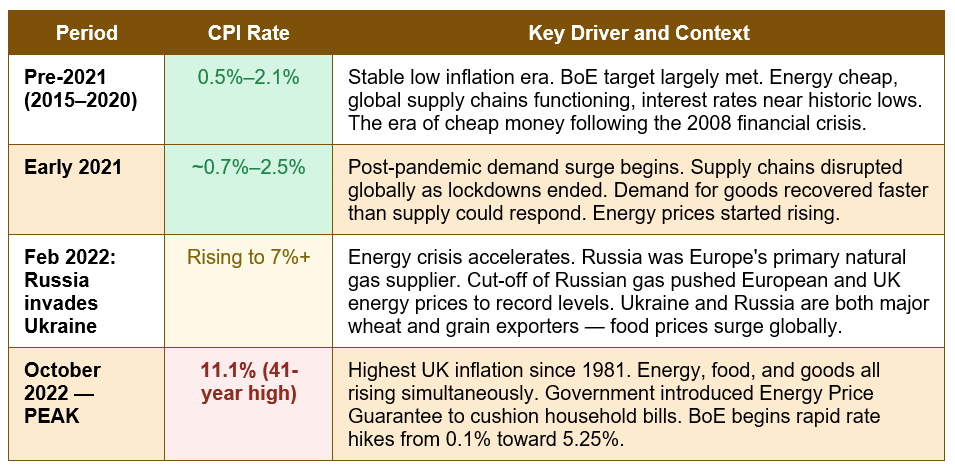

An average loaf of white bread cost around 52 pence in the year 2000. By 2025, that same loaf cost approximately £1.40 — nearly three times as much. This is inflation in its most tangible and personal form: the steady erosion of money's purchasing power over time, meaning each pound in your wallet buys progressively less than it did a year, five years, or a decade ago. When people talk about the cost of living rising, about their wages not stretching as far, about feeling financially squeezed even when nothing obvious has changed in their circumstances — they are talking about the effects of inflation.Inflation has dominated UK public life since 2021 in a way it had not for a generation. The Consumer Prices Index (CPI) — the UK's primary measure of inflation — rose from under 1% in early 2021 to 11.1% in October 2022, the highest level in 41 years. That surge was driven by the collision of post-pandemic supply chain disruption, Russia's invasion of Ukraine and the resulting energy and food price crisis, and the end of an era of ultra-cheap energy that had suppressed prices for a decade. UK consumer prices increased by more than 20% in the three years between 2021 and 2024. Even as the rate of inflation has since fallen — the ONS confirmed CPI at 2.8% in May 2026 — the cumulative price increase has not reversed. A cost of living crisis that began in 2021 has continued into 2026 not because prices are still rising at 11%, but because they rose so sharply that even moderate subsequent increases compound an already painful base.

This guide explains everything about inflation for a UK audience in 2026: what it is and how it is measured, the different types including demand-pull and cost-push, what caused the 2021-2022 spike and where prices are heading in the remainder of 2026, how the Bank of England uses interest rates to control it, what inflation does to savings and purchasing power, and the practical steps individuals can take to protect their finances in an inflationary environment.

What Is Inflation?

Inflation is the rate at which the general level of prices for goods and services rises over time — and correspondingly, the rate at which the purchasing power of money falls. It is expressed as a percentage change over a specific period, almost always year-on-year (the annual inflation rate). If inflation is 2.8%, it means that a basket of goods and services that cost £100 a year ago now costs £102.80 on average.The Bank of England's explanation is the clearest: 'If a loaf of bread cost £1 a year ago and now it costs £1.03, then its price has risen by 3%. Inflation is a measure of how much the prices of goods and services have gone up over time.' The Bank of England is tasked by the UK government with keeping CPI inflation at a target of 2% — neither too high (which erodes purchasing power and creates economic uncertainty) nor too low (which can signal weak demand and encourage consumers to delay spending in expectation of future price falls).

The critical insight about inflation is that it is an average measure across a basket of hundreds of goods and services. Not every price in the economy rises at the same rate. In May 2026, education prices in the UK were rising at 7.6% annually while clothing and footwear prices were rising at the slowest rate. Energy prices, food prices, and services prices each move at different rates and are driven by different underlying forces. The single headline CPI figure is a weighted average of all of these movements, designed to represent the experience of the typical UK household — but individual households whose spending patterns differ significantly from the average will experience their personal rate of inflation differently from the headline figure.

The cumulative impact of the 2021-2026 inflation surge: UK consumer prices rose over 20% in three years — even at 2.8% today, that accumulated increase has not reversed — the House of Commons Library (published today, July 10, 2026) confirms UK prices have increased by over 20% in the last three years. 67% of UK households reported their cost of living was still increasing in March 2026 (Statista/ONS). Even with CPI at 2.8%, households are experiencing the ongoing effects of the most significant inflationary period in a generation (ONS / House of Commons Library, July 2026)

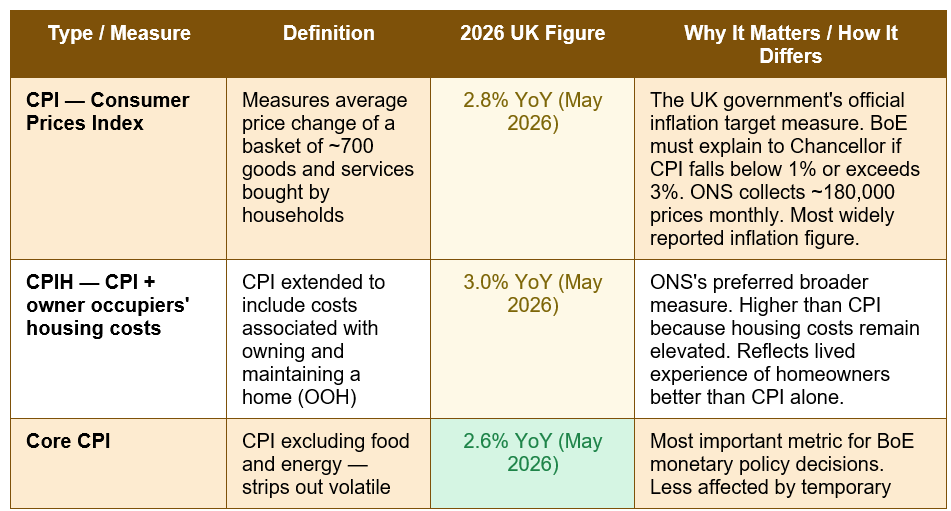

How Is Inflation Measured? CPI, CPIH, RPI and Core Inflation

The UK has several different measures of inflation, each capturing a slightly different picture of price changes across the economy. Understanding the distinctions between them matters because they are used for different purposes and can paint meaningfully different pictures of inflationary pressures.The Consumer Prices Index (CPI) is the headline figure — the measure the Bank of England targets and the one most widely reported in news coverage. It is calculated by the Office for National Statistics (ONS), which collects approximately 180,000 prices of around 700 different items each month. These items are grouped into categories — food and drink, clothing, housing and utilities, transport, recreation and culture, restaurants and hotels, and others — and weighted according to how much of a typical household's budget is spent on each category. The ONS reviews the 'basket of goods' every year, adding and removing items to keep the sample current. In 2026, the ONS removed items including premium bottled lager and individual sheets of wrapping paper, and added items better reflecting current consumption patterns.

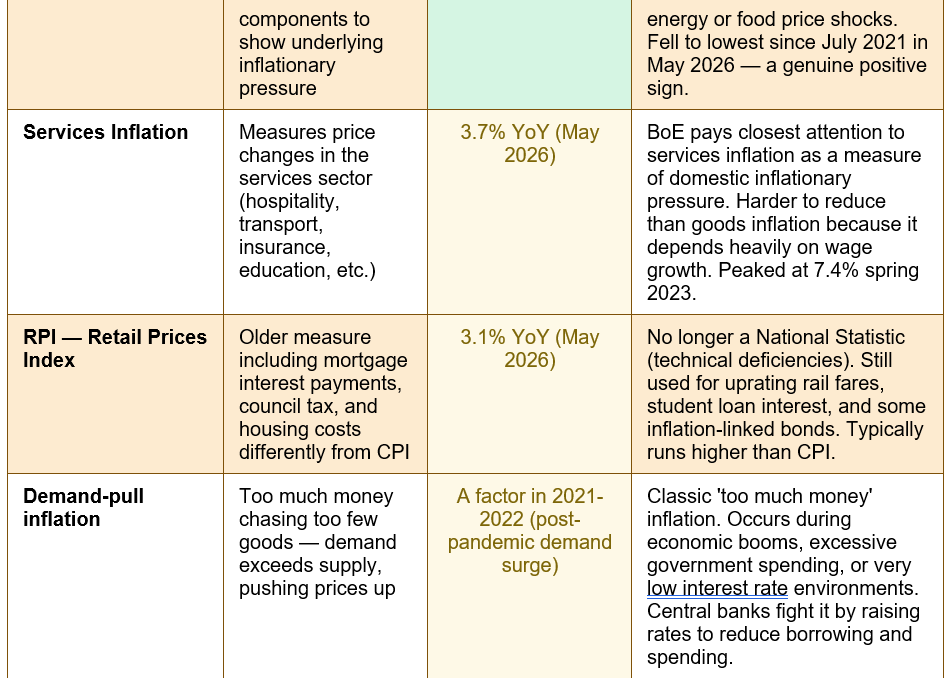

The annual rate of CPI is calculated by comparing the current month's price index to the same month of the previous year. In May 2026, the ONS confirmed that CPI rose 2.8% in the 12 months to May 2026, unchanged from April. This figure was accompanied by related measures: CPIH (CPI plus owner occupiers' housing costs) at 3.0%; core CPI at 2.6% (its lowest since July 2021); and services inflation at 3.7%.

Why the Bank of England cares most about services inflation: The Bank of England pays particularly close attention to services inflation when setting interest rates, as services prices are considered less exposed to global factors (energy shocks, food commodity prices) and more dependent on domestic wage costs. Services inflation peaked at a 31-year high of 7.4% in spring/summer 2023 and was still running at 3.7% in May 2026. This 'stickier' domestic inflation is the primary reason the Bank of England has been cautious about cutting rates even as headline CPI has fallen back toward the 2% target. The House of Commons Library analysis (published today) notes: 'The Bank of England pays close attention to services prices when setting interest rates, as they are seen as less exposed to global factors and more dependent on domestic costs. Inflation in services is also considered to be more persistent than inflation in goods.'

Types of Inflation and Measures: The Complete Reference

Inflation comes in several distinct types, each driven by different economic forces and requiring different policy responses. The table below maps every major type and measure of inflation relevant to UK readers in 2026:

What Causes Inflation? The Key Forces Driving Prices

Demand-Pull Inflation

Demand-pull inflation occurs when total demand in the economy — from consumers, businesses, and the government combined — exceeds the economy's capacity to supply goods and services. The result is too much money chasing too few goods, and prices rise to balance the equation. This form of inflation is often described as the 'good times' inflation: it tends to emerge during periods of strong economic growth, low unemployment, and rising wages, when consumers feel confident and spend freely.The post-pandemic period of 2021 included a significant demand-pull component. As lockdowns ended and economies reopened, pent-up consumer demand was released simultaneously — people who had saved money during the pandemic rushed to spend on travel, dining, experiences, and goods. Supply chains, still recovering from pandemic disruptions, could not keep up. The demand exceeded supply at the existing price level, so prices rose. Moneyfacts' inflation guide describes this mechanism directly: 'This is when demand for a particular product or service is greater than businesses can supply, forcing them to raise prices.'

Cost-Push Inflation

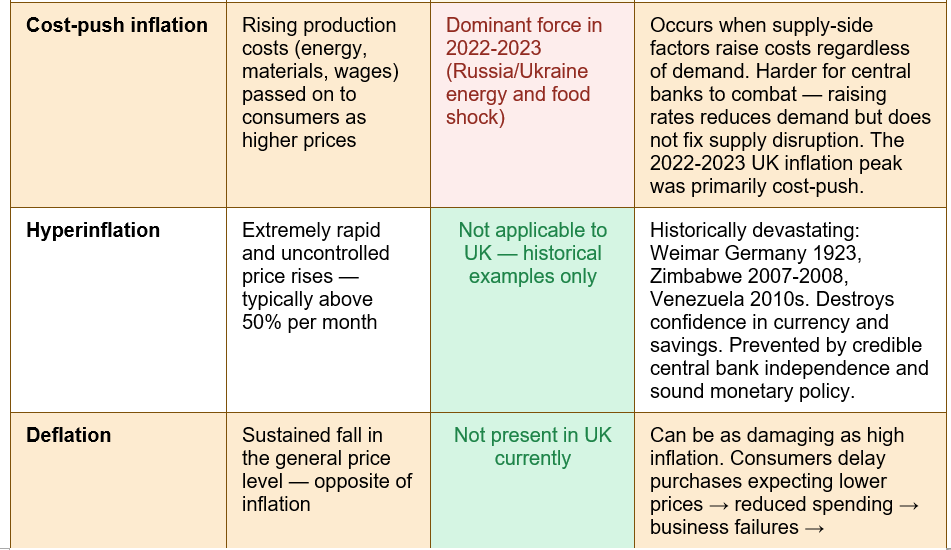

Cost-push inflation occurs when the costs of production rise — whether from energy, raw materials, wages, or other inputs — and businesses pass those higher costs on to consumers through higher prices. Unlike demand-pull inflation, which emerges from the demand side of the economy, cost-push inflation is a supply-side phenomenon: prices rise not because consumers are spending more freely but because it costs more to make and deliver goods and services.The 2022-2023 UK inflation surge was primarily cost-push in character. Russia's invasion of Ukraine in February 2022 removed a major supplier of natural gas from European markets — Russia had supplied roughly 40% of Europe's gas before the invasion — causing energy prices to spike to record levels. Energy costs affect almost every other cost in the economy: transporting food costs more if fuel is expensive; heating warehouses, factories, and farms costs more; manufacturing electricity costs more. These second-round effects spread the initial energy shock throughout the price of almost every good and service in the economy. Simultaneously, both Russia and Ukraine are major exporters of wheat, sunflower oil, and other food commodities — their exports were disrupted, causing global food commodity prices to surge and UK food inflation to follow.

Built-In Inflation (The Wage-Price Spiral)

Built-in inflation — sometimes called the wage-price spiral — occurs when workers and businesses adjust their behaviour in response to existing inflation in ways that entrench and perpetuate it. When prices have been rising, workers demand higher wages to maintain their purchasing power. When businesses pay higher wages, their labour costs rise, and they raise prices to maintain profit margins. Higher prices then prompt the next round of wage demands, and so on. This self-reinforcing cycle is one of the most persistent forms of inflation and a key reason why central banks act quickly to prevent high inflation from becoming entrenched: once inflation expectations become embedded in wage and price-setting behaviour, they are much harder and more costly (in terms of economic damage) to remove.The persistence of services inflation in the UK — running at 3.7% in May 2026, well above the BoE's 2% target even as energy and food inflation have eased — partly reflects this wage-pressure dynamic. Average earnings growth in the UK has remained elevated because workers successfully negotiated higher wages during the 2022-2023 peak inflation period, and those wage increases have been sustained in an environment of near-full employment.

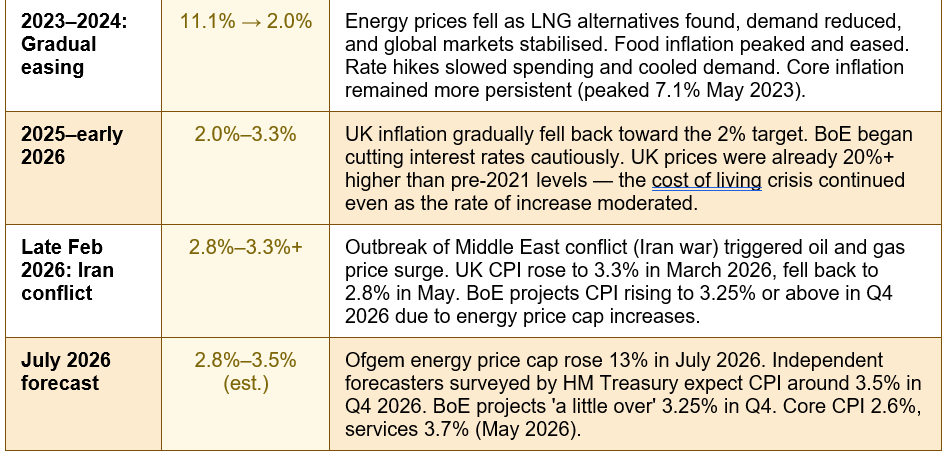

UK Inflation: The Complete Timeline 2020–2026

The table below maps the full UK inflation story from the pre-pandemic era of price stability through to the 2022 peak and the current 2026 environment, with the key drivers at each stage:

The Bank of England's Role: How Interest Rates Fight Inflation

The Bank of England is the UK's central bank and has a legally mandated target to keep CPI inflation at 2%, set by the government. The primary tool it uses to achieve this target is the Bank Rate — the interest rate at which the Bank of England lends to commercial banks, which in turn influences the interest rates that banks charge on mortgages, loans, and credit cards, and the rates they pay on savings accounts.When inflation rises above target, the Bank of England typically raises interest rates. Higher interest rates have several inflation-dampening effects: they make borrowing more expensive, reducing consumer spending on credit-financed purchases; they make mortgages more expensive, reducing disposable income for homeowners; they make saving more attractive relative to spending; and they strengthen the pound, making imports cheaper and thereby reducing import-driven inflation. The cumulative effect is to reduce demand across the economy, cooling the upward pressure on prices.

In response to the 2022-2023 inflation surge, the Bank of England raised its Bank Rate from 0.1% in December 2021 to a peak of 5.25% in August 2023 — the fastest and largest sequence of rate rises in decades. These higher rates contributed significantly to the subsequent fall in inflation from 11.1% toward the 2% target. By 2025, with inflation falling, the Bank began cutting rates cautiously. The current path — and what it means for future rate decisions — depends heavily on whether inflation continues toward the 2% target or rises again due to energy price increases from the Middle East conflict.

The Bank of England's most recent forecast (April 2026) projected CPI to remain just under 3% for most of 2026 before rising to 'a little over 3.25%' in Q4. However, the May 2026 data came in at 2.8% — below the Bank's April forecast of 3.0% — which MoneyWeek notes as a positive surprise. Independent forecasters surveyed by HM Treasury in May 2026 expect CPI around 3.5% in Q4, partly due to the July 2026 Ofgem energy price cap rising 13%.

THE BANK RATE AND YOUR MONEY: The Bank Rate affects almost every financial product you hold. When it rises, mortgage rates rise (especially variable and tracker mortgages), personal loan rates rise, and credit card rates typically increase. Savings account rates also generally rise, which is why the 2022-2023 rate hiking cycle was the first time in over a decade that cash savings earned meaningful interest. When the Bank cuts rates (as it began doing in 2025), savings rates fall, mortgage rates may ease, and borrowing becomes cheaper. Monitoring Bank Rate decisions — made by the Monetary Policy Committee (MPC) eight times per year — is one of the most practically important pieces of financial monitoring any UK household can do.

How Inflation Affects UK Households: The Real-World Impact

Purchasing Power Erosion

The most fundamental effect of inflation is the erosion of purchasing power — the gradual reduction in how much a given amount of money can buy. If your income stays flat while prices rise by 3%, your real purchasing power has fallen by 3%: you can afford less with the same money than you could a year ago. The bread example illustrates this dramatically: 52 pence in 2000 could buy a loaf of bread; by 2025, the same 52 pence could not buy half a loaf. The cumulative effect of two decades of modest inflation has more than halved the purchasing power of that 52 pence.The past five years of elevated UK inflation have been particularly damaging to real purchasing power. With CPI peaking at 11.1% in 2022 and prices rising more than 20% in three years, many UK households experienced their biggest fall in living standards in decades. Lower-income households were disproportionately affected because food and energy — the categories that rose fastest — account for a much larger proportion of spending for households with lower incomes than for those with higher incomes.

Savings and Investments

Inflation directly erodes the real value of cash savings. If you hold £10,000 in a savings account earning 1% interest while inflation is running at 3%, the real value of your savings is falling by 2% per year. After five years at those rates, your £10,000 would nominally grow to approximately £10,510 but would only have the purchasing power of roughly £9,057 in today's money — a real-terms loss of nearly 10%. This is why financial advisers consistently emphasise that cash savings must earn a return above the inflation rate to protect their real value — and why equity investments, which tend to grow faster than inflation over the long run, are often recommended as an inflation hedge for money with a longer time horizon.The good news is that the same interest rate increases designed to fight inflation also raised savings rates in the UK. After a decade of near-zero returns on cash savings following the 2008 financial crisis, UK savers in 2023 and 2024 could earn 5% or more on easy-access savings accounts and over 5% on fixed-rate cash ISAs — for the first time in years, cash savings rates broadly kept pace with or exceeded the falling headline inflation rate. As the Bank begins cutting rates in 2025-2026, this window of attractive cash savings rates is gradually narrowing.

Mortgages and Borrowing

Inflation's effect on borrowers is more nuanced than its effect on savers. In the simplest sense, inflation helps existing borrowers with fixed-rate debt: if you owe £100,000 and inflation runs at 5%, the real value of your debt is gradually being eroded — it represents a smaller share of what you earn and own in real terms over time. However, the interest rate rises that central banks use to combat inflation increase the cost of new and variable-rate borrowing, which hurts both new buyers and homeowners on tracker or standard variable rate mortgages. The surge in UK mortgage rates in 2022-2023 — following the Bank Rate rising from 0.1% to 5.25% — added hundreds of pounds to monthly payments for millions of UK mortgage holders, amplifying the cost of living squeeze.THE COST OF LIVING CRISIS IS NOT OVER: Even with CPI at 2.8% in May 2026, the cost of living crisis continues for millions of UK households. This is because the 20%+ cumulative price increase since 2021 has NOT reversed — prices have not fallen back to their 2021 levels. They have simply stopped rising as fast. A household spending £2,000 per month in 2021 was spending approximately £2,400 per month in 2024 just to maintain the same standard of living. That £400 per month additional burden is permanent unless wages grow to compensate, or prices fall (deflation) — which the Bank of England specifically tries to prevent. For lower-income households, this permanent shift in the cost of basics (food, energy, housing) represents a fundamental reduction in living standards.

How to Protect Your Finances from Inflation

While individuals cannot control the headline inflation rate, they can take practical steps to reduce the impact of rising prices on their own financial position and to protect the real value of their money:- Ensure savings earn above-inflation returns: Keep a minimum of 3-6 months' expenses in easily accessible cash savings, but move any money with a longer time horizon into accounts or investments that offer returns above the current inflation rate. In July 2026 with CPI at 2.8%, a cash ISA or savings account paying 4%+ represents a positive real return. Use the MoneyHelper savings comparison tool or MoneySuperMarket to find the best current savings rates.

- Consider inflation-linked investments: Index-linked UK government bonds (gilts) pay a return that is linked to the RPI inflation measure — their value rises with inflation. Equity investments in diversified stock market funds have historically outpaced inflation over periods of five years or more, making them a meaningful long-term inflation hedge. Premium Bonds' prize fund rate is also reviewed regularly by NS&I and has risen substantially alongside Bank Rate increases.

- Review and negotiate regular bills: Inflation creates opportunities to save by switching providers. Many broadband, insurance, and energy contracts increase annually, often above the headline rate. MoneyfactsCompare's personal finance guide recommends proactively switching suppliers, comparing energy tariffs, and buying own-brand products to reduce the personal inflation rate you experience. Food price inflation was 2.2% in May 2026 — but switching supermarkets or buying own-brand can reduce your personal food cost increase to effectively zero.

- Claim salary increases that at least match inflation: Wage growth that keeps pace with inflation preserves real purchasing power. During 2022-2023, average UK earnings growth lagged well behind inflation, meaning most workers experienced a real-terms pay cut. If your salary has not grown at least in line with CPI over the past few years, your real standard of living has declined even if your nominal salary has risen. The House of Commons Library notes that by May 2026 average earnings (adjusted for inflation) are 'about the same as they were at the end of 2025' — suggesting real wage growth has stalled.

- Use ISAs and pensions to shelter returns from tax: Investment returns above inflation are only valuable if you keep them. ISAs allow up to £20,000 per year of savings and investments to grow completely free of income tax and capital gains tax. Pension contributions attract income tax relief on entry, reducing the cost of the investment and compounding real returns over time. These wrappers are particularly valuable in an inflationary environment where the return needed to beat inflation is already thin.

Conclusion

Inflation is the sustained rise in the general level of prices over time — and its consequences, from the erosion of purchasing power to the upheaval of interest rates and the real cost of living, touch every aspect of personal and household finance. The UK's experience since 2021 has been a stark reminder of how quickly moderate, stable inflation can become a genuine economic crisis: from under 1% in early 2021 to 11.1% in October 2022 — the highest in 41 years — and back down to 2.8% in May 2026, with prices having risen more than 20% in total along the way.The current 2026 inflation environment is one of cautious uncertainty. CPI at 2.8% is close to the Bank of England's 2% target, and core inflation at 2.6% (its lowest since July 2021) is a genuine positive. But the outlook is for further rises: the Bank of England projects CPI moving to 'a little over 3.25%' in Q4 2026, independent forecasters expect 3.5%, and the July 2026 Ofgem energy price cap increase of 13% will feed through to household costs through the second half of the year. The Middle East conflict adds geopolitical uncertainty to the energy price outlook.

Understanding inflation — what drives it, how it is measured across different indices (CPI, CPIH, core CPI, RPI), and how the Bank of England uses interest rates to manage it — is one of the most practically important areas of financial literacy for UK households. Inflation determines the real value of your savings, the cost of your mortgage, the trajectory of your wages, and the purchasing power of your income. For those who understand it, the tools to protect against it — inflation-linked savings, diversified investments, ISA and pension wrappers, and proactive cost management — are available and accessible. For those who do not, the silent compounding of rising prices over years and decades is the most persistent and most underestimated risk to financial security in ordinary life.

Frequently Asked Questions (FAQ)

What is the current UK inflation rate in 2026?

The UK CPI (Consumer Prices Index) inflation rate was 2.8% in the 12 months to May 2026, according to the Office for National Statistics, published on 18 June 2026. This was unchanged from April 2026. The related measure CPIH (which includes owner-occupiers' housing costs) was 3.0%. Core CPI — which excludes food and energy to show underlying price pressures — was 2.6%, its lowest since July 2021. Services inflation was 3.7%. The RPI (Retail Prices Index, no longer a National Statistic but still widely referenced) was 3.1%. The Bank of England's inflation target is 2%. Forecasters expect CPI to rise again through the remainder of 2026 due to higher energy prices following the July Ofgem energy price cap increase of 13%, with independent forecasters expecting approximately 3.5% by Q4 2026.What caused the UK inflation surge of 2022?

The 2022 UK inflation surge — which peaked at 11.1% in October 2022, the highest rate in 41 years — was driven by a combination of factors that converged simultaneously. The post-pandemic demand surge of 2021 created demand-pull pressure as consumers spent pent-up savings while supply chains were still recovering. Russia's invasion of Ukraine in February 2022 removed Russia as a major natural gas supplier to European markets (Russia had supplied approximately 40% of Europe's gas), causing energy prices to surge to record levels. The same conflict disrupted global food commodity markets: both Russia and Ukraine are major exporters of wheat, sunflower oil, and other food staples. The combination of an energy shock and a food shock — the two categories with the greatest weight in lower-income household budgets — produced a cost-push inflation crisis that spread through supply chains to affect almost every price in the economy.What is the difference between CPI and RPI?

CPI (Consumer Prices Index) and RPI (Retail Prices Index) are both measures of inflation — they track the change in prices over time — but they differ in what they include and how they calculate price changes. CPI is the UK government's official inflation target measure and is what the Bank of England is mandated to keep at 2%. It covers a broad basket of consumer goods and services but excludes mortgage interest payments and council tax. RPI includes these additional housing costs and uses a slightly different mathematical formula (which tends to produce higher results than CPI's calculation method). The ONS no longer classifies RPI as a National Statistic because of technical deficiencies in its calculation. However, RPI is still used in practice for uprating rail fares, student loan interest, and the returns on some inflation-linked bonds. In May 2026, CPI was 2.8% and RPI was 3.1%.How does inflation affect savings?

Inflation erodes the real value of cash savings. If your savings account pays 2% annual interest while inflation is running at 3%, the real purchasing power of your money is falling by approximately 1% per year — even though the nominal balance is growing. After 10 years of this, a £10,000 saving would nominally become approximately £12,190 but would only have the purchasing power of roughly £10,980 in today's money at 2% interest with 3% inflation. To preserve the real value of savings, the interest rate earned must exceed the inflation rate. In mid-2026, with CPI at 2.8%, savings accounts and fixed-rate ISAs offering 4%+ provide a positive real return. Cash savings that earn below the inflation rate are losing real value every month. For money with a longer time horizon (five years or more), equities historically provide returns that outpace inflation, making them a meaningful inflation hedge for the non-emergency portion of savings.What is the Bank of England's inflation target and what happens if it is missed?

The UK government has set the Bank of England a target to keep CPI inflation at 2%. The Monetary Policy Committee (MPC) — which meets eight times a year — sets the Bank Rate to try to achieve this target. If CPI falls more than one percentage point below the target (below 1%) or rises more than one percentage point above it (above 3%), the Governor of the Bank of England is required to write an open letter to the Chancellor of the Exchequer explaining why the target has been missed and what the Bank intends to do to bring inflation back to 2%. These letters are published publicly. During the 2022-2023 inflation surge, the Governor wrote multiple such letters as CPI remained well above 3%. The most recent such letter was published on 30 April 2026. A 2% inflation target is considered optimal because it provides a small buffer against deflation, gives businesses and consumers confidence in price stability, and allows the economy enough flexibility to absorb occasional price shocks.

External References

1. ONS — Inflation and Price Indices: UK CPI, CPIH, RPI (3 weeks ago — May 2026 data: CPI 2.8%, CPIH 3.0%)https://www.ons.gov.uk/economy/inflationandpriceindices

2. House of Commons Library — Inflation in the UK: Economic Indicators (Published today, July 10, 2026)

https://commonslibrary.parliament.uk/research-briefings/sn02792/

3. Bank of England — Inflation and the 2% Target (Official BoE explanation, last updated May 2026)

https://www.bankofengland.co.uk/monetary-policy/inflation

4. House of Commons Library — Economic Update: Beating the Forecasts, for Now (Published today, July 10, 2026 — GDP 0.6% Q1, inflation 2.8% May)

https://commonslibrary.parliament.uk/research-briefings/cbp-10857/

5. MoneyWeek — UK Inflation Forecast: Where Are Prices Heading Next? (3 weeks ago — BoE projects 3.25%+ Q4 2026, July Ofgem cap +13%)

https://moneyweek.com/economy/inflation/inflation-forecast-where-are-prices-heading-next

6. MoneyfactsCompare — Inflation Explained and How to Deal With It (April 2026 — causes, measures, practical steps)

https://moneyfactscompare.co.uk/guides/money/uk-inflation-explained-and-how-to-deal-with-it/

7. Statista / ONS — UK CPI Inflation Rate January 2015 to May 2026 (Published June 17, 2026)

https://www.statista.com/statistics/306648/inflation-rate-consumer-price-index-cpi-united-kingdom-uk/

8. MoneyHelper — Understanding Inflation and Protecting Your Savings

https://www.moneyhelper.org.uk/en/everyday-money/budgeting/how-to-deal-with-the-cost-of-living-crisis

0 Comments Comments