Real Estate

What Is the 28/36 Mortgage Rule?

Table of Contents

- The Rule That Defines How Much House You Can Afford

- What Is the 28/36 Mortgage Rule?

- The Two Components: Front-End and Back-End Ratios Explained

- The 28% Front-End Ratio: Your Housing Cost Ceiling

- The 36% Back-End Ratio: Your Total Debt Ceiling

- How to Calculate Your 28/36 Ratios: Step by Step

- Worked Examples: The 28/36 Rule in Practice

- Example 1 — Chase Bank Amy: Meeting Both Ratios

- Example 2 — UK First-Time Buyer: Calculating Borrowing Capacity

- The 28/36 Rule in Real Numbers: US and UK Income Reference Table

- Mortgage Affordability Rules Compared: What Lenders Actually Use

- The 28/36 Rule in the UK: How British Mortgage Affordability Works

- Limitations of the 28/36 Rule: What It Cannot Tell You

- Conclusion

- Frequently Asked Questions (FAQ)

Note: This guide covers the 28/36 mortgage rule — the widely used home affordability guideline sometimes also referred to by slight variations. The standard documented rule used by lenders and financial planners is 28% front-end and 36% back-end, as confirmed by Bankrate (June 2026), Rocket Mortgage (March 2026), Chase, and all major mortgage authorities cited in this guide.

The Rule That Defines How Much House You Can Afford

When you apply for a mortgage, your lender does not simply look at how much you earn and decide whether to approve your loan. They apply a set of debt-to-income ratio tests that have been the foundation of mortgage underwriting for decades. The most widely referenced of these is the 28/36 rule — a simple but powerful framework that defines the boundaries of responsible home buying based on two percentage thresholds applied to your gross monthly income.The 28/36 rule states that your total monthly housing costs should not exceed 28% of your gross monthly income, and that your total monthly debt obligations — including your mortgage — should not exceed 36% of your gross monthly income. As Bankrate's June 2026 guide confirms: 'While it's commonly called a rule, 28/36 is not a law, just a guideline. Mortgage lenders use it to determine how much house you can afford if you were to take out a conventional conforming loan, the most common type of mortgage.'

The rule matters in 2026 more than at almost any point in recent memory. A Hometap survey found that 79.5% of homeowners believe the cost of homeownership is rising faster than their income — and that 54.4% say housing costs are actively preventing them from achieving other financial goals. Bankrate's worked example illustrates the challenge concretely: a $500,000 home bought with 20% down and a 30-year mortgage at 6.5% requires a gross household income of at least $125,500 per year to remain within the 28% front-end limit. In a market where median home prices have reached record highs in many UK and US cities, understanding exactly what the rule requires — and when lenders allow flexibility beyond it — is essential for any prospective buyer.

What Is the 28/36 Mortgage Rule?

The 28/36 rule is a mortgage affordability guideline that uses two debt-to-income (DTI) ratio tests — a front-end ratio and a back-end ratio — both applied to gross monthly income to assess whether a borrower can comfortably afford a proposed mortgage alongside their existing debt obligations. Chase's mortgage education guide provides a clean definition: 'The 28/36 rule suggests that a borrower should use no more than 28% of their income on housing, and no more than 36% of their income on overall debts. Even if you are not planning to buy a home soon, applying the 28/36 rule to your finances can help improve financial stability and your appearance to potential lenders.'An important distinction: the rule is based on gross income — the amount you earn before income tax, National Insurance, pension contributions, or other deductions. This is a fundamentally different and more generous base than the after-tax take-home pay used in everyday budgeting rules like the 60/20/20 or 50/30/20. Because gross income is higher than take-home pay, the absolute amounts available for housing under the 28% gross rule are materially higher than they would be under a rule applied to net income. This is both the rule's strength (it reflects the standard lenders actually use) and one of its practical limitations (paying a mortgage from take-home pay, not gross, means the real percentage of usable income going to housing is higher than 28%).

The rule has two distinct components that work together to define both the housing cost ceiling and the total debt ceiling:

The housing affordability pressure in 2026: 79.5% of homeowners believe housing costs are rising faster than their income — and 54.4% say it prevents other financial goals — Hometap survey (December 2025): the 28/36 rule 'isn't just about qualifying for a mortgage anymore; it's about homeowners gaining control over their financial lives.' A $500,000 home at 6.5% for 30 years requires $125,500 gross annual income to stay within the 28% front-end threshold (Bankrate, June 2, 2026). In the current high-price, high-rate environment, the rule is harder to satisfy than at any point since the early 1980s.

The Two Components: Front-End and Back-End Ratios Explained

The 28% Front-End Ratio: Your Housing Cost Ceiling

The front-end ratio — sometimes called the housing expense ratio or mortgage-to-income ratio — is the first number in the 28/36 rule. It limits your total monthly housing costs to a maximum of 28% of your gross monthly income. Housing costs in this context are defined by the PITI acronym: Principal (the portion of your mortgage payment that reduces the loan balance), Interest (the cost of borrowing), Taxes (property taxes, typically estimated monthly and held in escrow by the lender), and Insurance (homeowners insurance, and private mortgage insurance or PMI if your down payment is less than 20%).Rocket Mortgage's March 2026 guide expands the list: 'Housing costs typically include PITI, which includes the following: principal, interest, property taxes, homeowner's insurance, any HOA fees.' Homeowners' association fees — common in apartment buildings, gated communities, and new-build estates — count within the 28% front-end ratio and can be material: HOA fees in the US can range from $200 to $1,000+ per month in high-end developments.

The front-end ratio is the more directly consumer-relevant number: it answers the question 'how much house can I afford?' in terms of the monthly payment. If your gross monthly income is $8,000, the 28% rule says your total PITI should not exceed $2,240 per month. If your income is £6,000 per month gross, the 28% ceiling is £1,680 in monthly housing costs.

The 36% Back-End Ratio: Your Total Debt Ceiling

The back-end ratio — also called the debt-to-income (DTI) ratio — is the second and broader component of the rule. It limits all of your monthly debt obligations combined — including the housing costs from the 28% calculation — to a maximum of 36% of gross monthly income. Calculatorian's March 2026 guide is comprehensive on what this includes: 'The back-end ratio (36%) caps your total monthly debt at 36% of gross income. This includes your housing payment plus all other recurring debt obligations: car loans, student loan payments, credit card minimums, personal loans, and child support.'The critical insight from the back-end ratio is what it implies about non-housing debt. If the 28% front-end limit is fully used by housing costs, only 8% of gross income remains for all other debt obligations within the 36% back-end ceiling. On a $7,000 monthly gross income, that is a maximum of $560 per month for car payments, student loans, credit card minimums, and any other debt. In a world where student loan debt is common and car payments have increased significantly, many borrowers find the 8% residual (36% minus 28%) is insufficient to accommodate their existing debt obligations — which is precisely why the back-end ratio is often the binding constraint for borrowers with meaningful pre-existing debt.

The student loan trap: Calculatorian's March 2026 analysis identifies a critical detail that trips many first-time buyers: 'Student loans on income-driven repayment plans with a $0 monthly payment aren't treated as $0 by most lenders. Fannie Mae calculates 1% of the outstanding balance as the monthly obligation. On $50,000 in student debt, that adds $500 per month to your DTI calculation, reducing your home buying power by roughly $60,000–$75,000.' This means that a buyer with $50,000 in student loans on an income-driven plan that actually requires no monthly payment is still treated as having a $500/month debt obligation by Fannie Mae underwriting — a significant but often invisible reduction in borrowing capacity.

How to Calculate Your 28/36 Ratios: Step by Step

- Find your gross monthly income: Use your pre-tax monthly earnings from all sources — employment income, rental income, self-employment income, investment income. If paid annually, divide by 12. If paid weekly, multiply by 52 then divide by 12. Include only reliable, documentable income. Do not include bonuses or overtime unless they are guaranteed.

- Calculate your 28% housing ceiling: Multiply gross monthly income by 0.28. This is the maximum total monthly housing cost (PITI + HOA) your mortgage should not exceed.

- Calculate your 36% total debt ceiling: Multiply gross monthly income by 0.36. This is the maximum total monthly debt payments (housing + all other debts) combined.

- Calculate available non-housing debt room: Subtract your actual monthly housing cost from the 36% ceiling. This is the maximum remaining capacity for all other monthly debt payments (car, student loans, credit cards, personal loans, child support).

- Compare your current debts to the ceilings: List all existing monthly debt obligations. Add them together and compare to the non-housing debt room. If your existing debts already exceed the available room, your borrowing capacity for a mortgage is reduced accordingly — the back-end ratio will be the binding constraint.

- Calculate the maximum mortgage you can afford: Working backward from your 28% housing ceiling, use a mortgage calculator with the current interest rate and your intended loan term to find the loan amount whose monthly PITI payment equals or is less than 28% of your gross monthly income. This is the rough maximum loan the 28/36 rule suggests you can afford.

Worked Examples: The 28/36 Rule in Practice

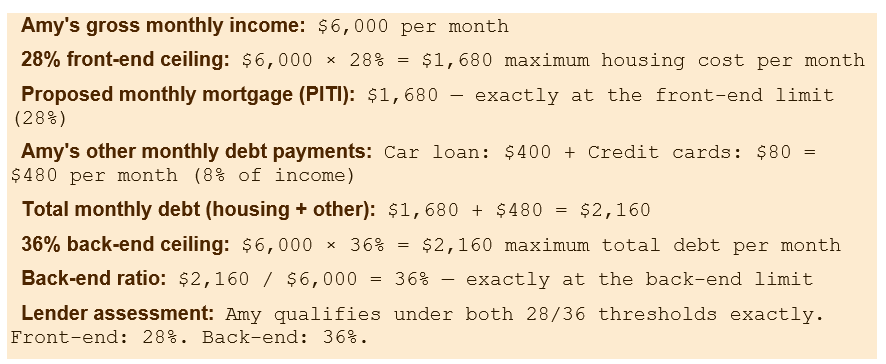

Example 1 — Chase Bank Amy: Meeting Both Ratios

This is the worked example provided by Chase Bank in their mortgage education guide:

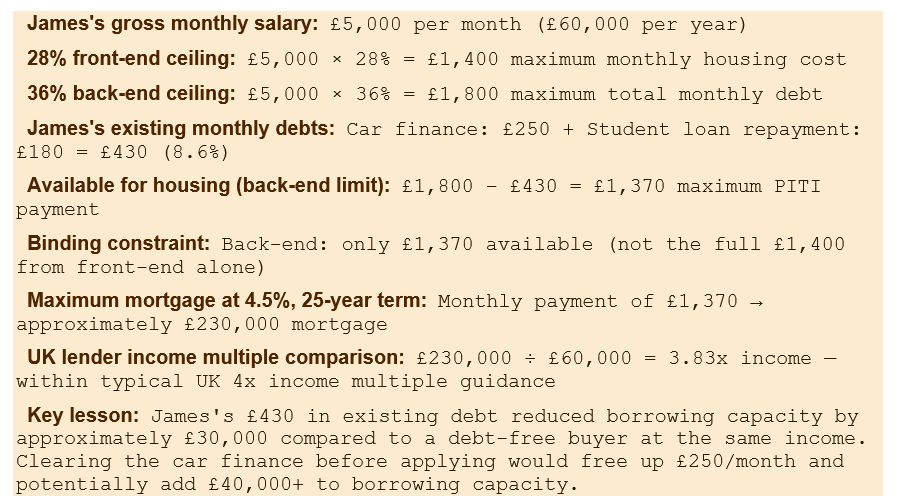

Example 2 — UK First-Time Buyer: Calculating Borrowing Capacity

THE DEBT CLEARANCE STRATEGY: If your back-end ratio is the binding constraint (your existing debts leave insufficient room for the mortgage you want), prioritising the clearance of high monthly-payment debts before applying can significantly improve borrowing capacity. A car finance payment of £300/month uses 6% of a £5,000 gross monthly income's back-end budget. Eliminating it before applying frees that entire 6% for mortgage capacity, potentially adding £40,000-£50,000 to borrowing power at current UK interest rates. Calculatorian (March 2026): "Anyone above 33% [DTI] should have a clear plan for covering payments if income drops or expenses spike."

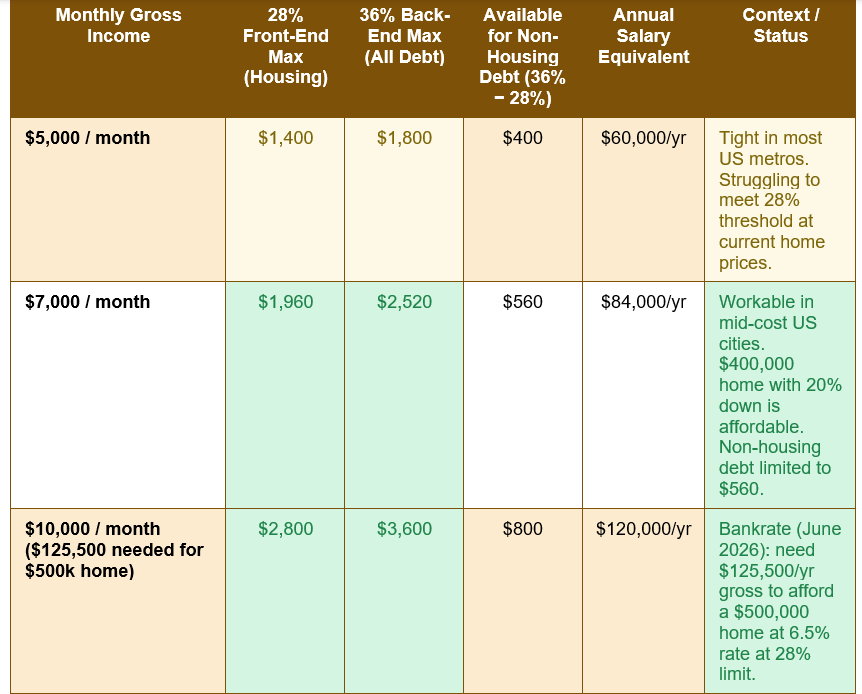

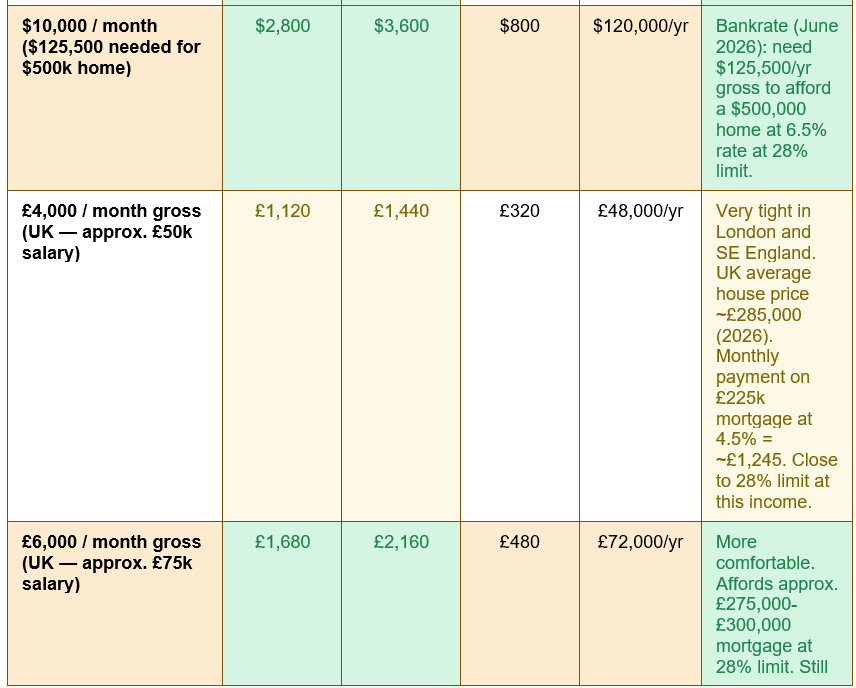

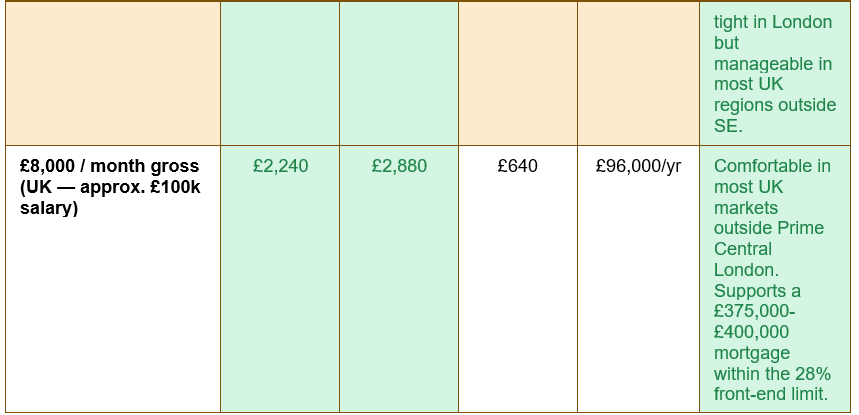

The 28/36 Rule in Real Numbers: US and UK Income Reference Table

The table below applies the 28/36 rule to common income levels in both the US and UK, showing the maximum housing cost, total debt ceiling, and available non-housing debt room at each income level:

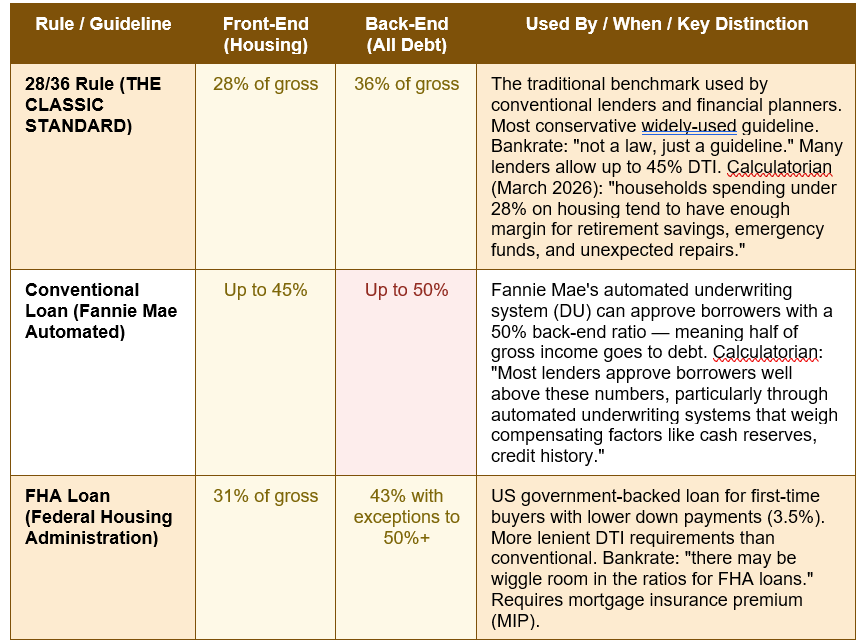

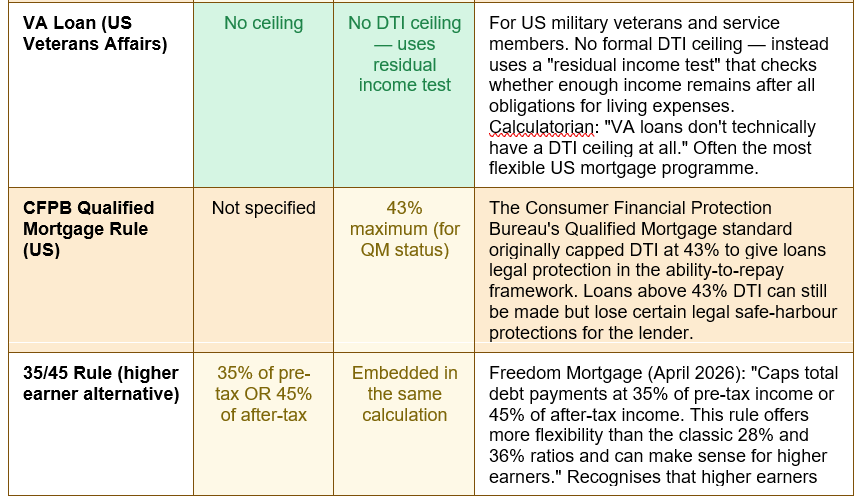

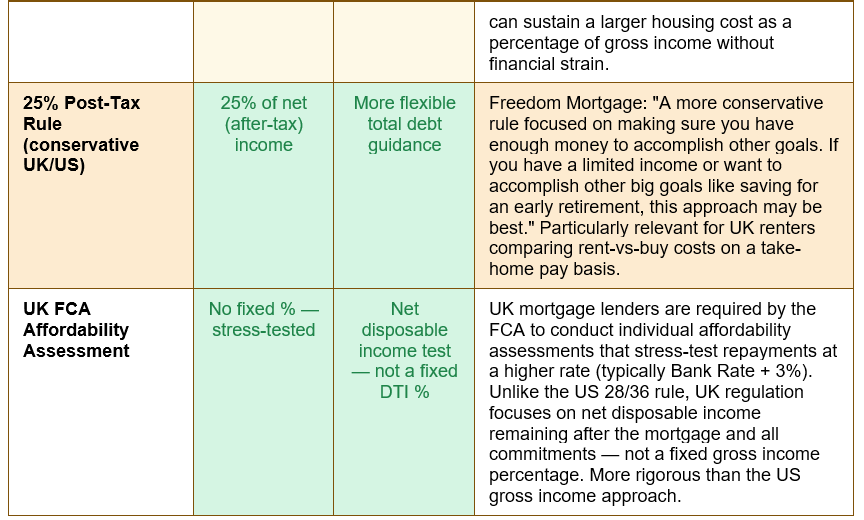

Mortgage Affordability Rules Compared: What Lenders Actually Use

The 28/36 rule is the most widely cited guideline, but it is neither the only framework nor the most lenient. Different loan programmes, lenders, and markets apply different affordability tests. The table below maps the complete landscape of rules currently in use:

The most important practical takeaway from this comparison: the 28/36 rule is the most conservative widely-used guideline, not the absolute ceiling for approval. Bankrate's June 2026 guide is explicit: 'Many lenders will allow a DTI of up to 45% on conventional loans.' Calculatorian confirms that Fannie Mae's automated underwriting can approve borrowers at 50% back-end DTI. This means that failing the 28/36 rule does not automatically disqualify a borrower — it signals elevated financial risk and the need for compensating factors such as a larger down payment, excellent credit score, significant cash reserves, or a lower loan-to-value ratio.

The 28/36 Rule in the UK: How British Mortgage Affordability Works

While the 28/36 rule originated in the US market and applies directly to US conventional mortgage lending, UK mortgage affordability is assessed under a different but comparably rigorous framework that shares the same underlying goal: ensuring borrowers can afford their mortgage payments sustainably.UK mortgage lenders are regulated by the Financial Conduct Authority (FCA) and must conduct individual affordability assessments that go beyond a simple gross income percentage test. The UK framework has several distinctive features. First, it uses net income (after tax and commitments) rather than gross income to assess the disposable income available for mortgage payments — a more conservative and more realistic approach than the gross income basis of the US 28/36 rule. Second, UK lenders stress-test mortgage affordability at a higher interest rate than the current borrowing rate, typically the Bank Rate plus 3%, to assess whether the borrower could continue to afford payments if rates rise. Third, income multiples are commonly used alongside the affordability assessment: most mainstream UK lenders will lend a maximum of 4 to 4.5 times a single income or combined income, with some lenders going to 5 or even 5.5 times for high earners or specific professional categories.

Applying the 28% front-end ratio to gross income in the UK context produces similar results to the standard UK income multiple approach at typical income levels, but the UK framework's stress testing and net disposable income focus means that in practice, UK lenders may approve somewhat less than the raw 28/36 rule suggests in high-rate environments.

Limitations of the 28/36 Rule: What It Cannot Tell You

The 28/36 rule is a useful starting point for assessing mortgage affordability, but it has significant limitations that every prospective buyer should understand before relying on it exclusively:- 7. It uses gross income, not take-home pay: The 28% ceiling applies to gross income before tax. In practice, your mortgage payment comes from your take-home pay. For a basic-rate UK taxpayer, take-home pay is roughly 75-80% of gross income — meaning the 28% gross income ceiling represents approximately 35-37% of actual after-tax income. Calculatorian (March 2026) recommends: 'Single-income earners, freelancers, or families planning for children should target 25% or lower [of gross income]. Anyone above 33% should have a clear plan.' The 25% post-tax rule offers a more conservative and arguably more realistic alternative for UK buyers.

- 8. It ignores everyday living expenses: Bankrate's June 2026 guide identifies this as the most significant blind spot: 'The 28/36 rule doesn't account for your credit score. One blindspot of the 28/36 rule is that it doesn't account for everyday expenses, like childcare, groceries, healthcare, and transportation.' A family with two young children in full-time childcare — which can cost £1,500 to £2,500 per month in the UK — has materially less financial capacity for a mortgage than a dual-income couple without dependants at the same gross income. The rule treats both households identically.

- 9. It does not reflect local housing market realities: In markets where house prices are extremely high relative to incomes — London, New York, San Francisco, Sydney — the 28% front-end limit mathematically requires incomes that are far above local medians to afford average properties. Rocket Mortgage (March 2026) acknowledges: 'It can be more difficult to follow the 28/36 rule if you live in a higher-cost area, your income hasn't kept up with inflation, or if you're burdened with a ton of debt.'

- 10. It is a snapshot, not a stress test: The rule tests affordability at the current interest rate with current income. It does not assess whether payments remain affordable if rates rise (a risk particularly relevant for variable-rate mortgages), if income falls due to redundancy or illness, or if additional costs arise from property maintenance, life events, or dependants. The UK's FCA-mandated stress testing is specifically designed to address this gap.

- 11. It does not include the cost of homeownership beyond the mortgage: Homeownership involves costs beyond PITI: maintenance and repairs (commonly estimated at 1-3% of property value annually), furniture and appliances, emergency repairs, and council tax (UK) or HOA fees (US). Calculatorian (March 2026) notes that 'households spending under 28% on housing tend to have enough margin for retirement savings, emergency funds, and the unexpected $8,000 roof repair that every homeowner eventually faces' — the converse being that those at exactly 28% may have no such margin.

THE HOUSE-POOR RISK: Buying a home at the absolute limit of what lenders will approve — the maximum DTI ratio rather than a comfortable level — leaves no financial margin for the ordinary and extraordinary costs of homeownership: a boiler replacement, a roof repair, a period of reduced income, a new family member. The 28/36 rule defines the ceiling of lender comfort, not the ceiling of financial wisdom. Rocket Mortgage (March 2026): 'Being house poor can leave you strapped for cash and can put you in a financially unstable situation if an emergency happens or your income declines.' For most buyers, targeting a front-end ratio of 20-25% and a back-end ratio of 30-33% — well within the 28/36 thresholds — provides meaningful financial breathing room while still accessing mortgage finance.

Conclusion

The 28/36 mortgage rule is the most widely referenced affordability guideline in residential mortgage lending — a simple, two-number framework that has defined lender expectations and buyer planning for decades. It states that total monthly housing costs (principal, interest, property taxes, insurance, and HOA fees) should not exceed 28% of gross monthly income, and that all monthly debt payments combined should not exceed 36% of gross monthly income. The difference between 28% and 36% — a maximum of 8% of gross income — represents the total available room for all non-housing debt obligations: car payments, student loans, credit card minimums, and personal loans.In 2026, the rule's relevance has never been greater — or harder to satisfy. With 79.5% of homeowners reporting that housing costs are rising faster than their income, and with a $500,000 home requiring a gross annual income of at least $125,500 to qualify within the 28% front-end limit at a 6.5% mortgage rate, the gap between the rule's requirements and many buyers' actual financial position has widened significantly in the current high-price, elevated-rate environment. Many conventional lenders and Fannie Mae's automated underwriting system approve borrowers at DTI ratios well above 36% — up to 45% and even 50% — as long as compensating factors like credit score, cash reserves, and loan-to-value ratio are strong.

The rule's limitations are real: it uses gross rather than after-tax income, ignores everyday living expenses like childcare and food, does not account for local house price realities, and provides no stress test for rate increases. For UK buyers, the FCA's more rigorous individual affordability assessment — which stress-tests at higher rates and considers net disposable income — provides stronger consumer protection than the US gross-income rule, though the underlying principle is the same. The 28/36 rule is best understood not as a definitive limit but as a starting point for financial planning: a benchmark that tells you where lenders broadly expect mortgage costs to sit, and a warning signal that housing spending above these thresholds reduces financial resilience in ways that only become apparent when something goes wrong.

0 Comments Comments