Real Estate

Borrow From Your Home Without Touching Your Mortgage

Table of Contents

- The Scale of the Opportunity: Home Equity Statistics

- What Does 'Without Touching Your Mortgage' Actually Mean?

- Option 1: Home Equity Line of Credit (HELOC)

- How HELOCs Work

- Best Uses for a HELOC

- Option 2: Home Equity Loan (Second Mortgage)

- Key Characteristics

- Option 3: Second Charge Mortgage (UK)

- When Second Charge Mortgages Make Sense in the UK

- Option 4: Equity Release (UK Homeowners Aged 55+)

- Lifetime Mortgage Key Features

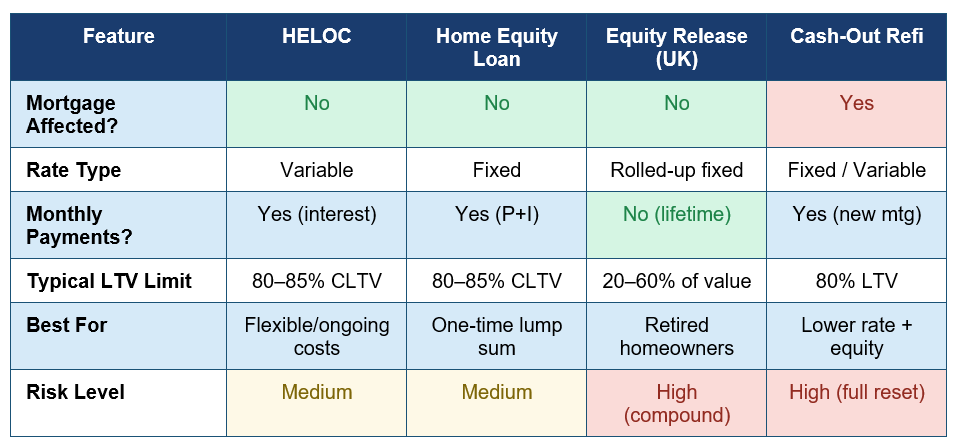

- Side-by-Side Comparison: All Four Options

- Key Risks and Essential Safeguards

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Your home is likely the most valuable financial asset you own. For millions of homeowners in the United States and United Kingdom, decades of mortgage payments, rising property values, and market appreciation have built up substantial equity — the portion of your home's value that you actually own outright. Yet most homeowners treat this equity as a locked vault, accessible only by selling the property or refinancing the entire mortgage.

The reality is more flexible and more financially advantageous than many people realise. There is a range of powerful financial products specifically designed to help homeowners access the wealth stored in their property without disturbing their existing mortgage. Whether you need funds for home improvements, debt consolidation, education costs, investment opportunities, or retirement income, the tools to access that equity are available — and for many people, using them wisely can deliver significant financial benefits at competitive interest rates that unsecured borrowing simply cannot match.

This guide explains every practical method available for borrowing from your home equity without touching your existing mortgage. It covers Home Equity Lines of Credit (HELOCs), home equity loans, second charge mortgages, equity release products for older homeowners, and the key questions you need to ask before choosing between them. Backed by current statistics on the scale of available home equity and current borrowing rates, it provides a clear and honest framework for making one of the most significant financial decisions a homeowner can face.

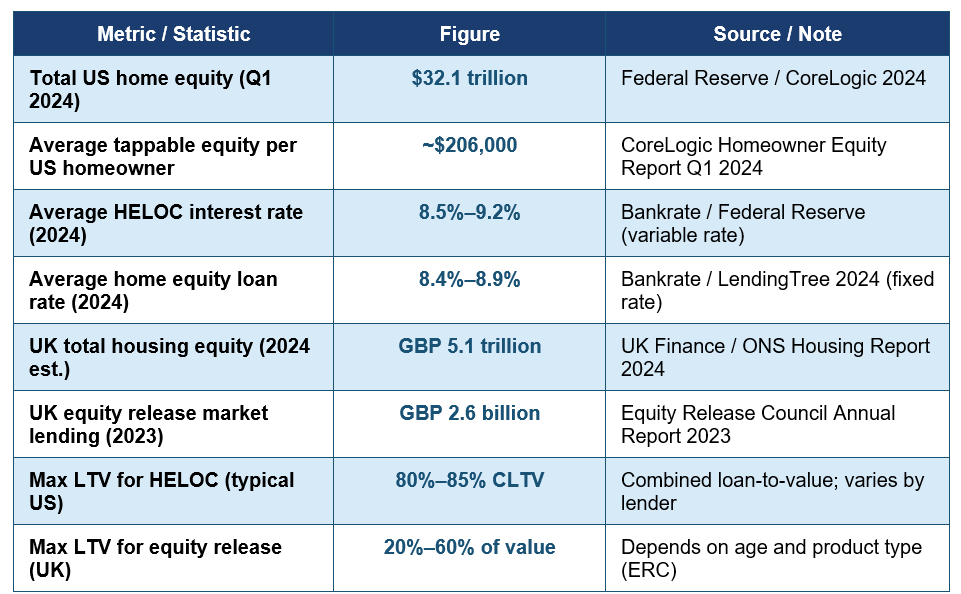

The Scale of the Opportunity: Home Equity Statistics

Understanding the scale of home equity available to homeowners in both the US and UK helps to contextualise why these borrowing products have become such a significant part of the personal finance landscape.

These figures illustrate a striking reality: the aggregate home equity held by US homeowners alone exceeds $32 trillion — a sum larger than the GDP of the United States itself. The average American homeowner has approximately $206,000 in tappable equity, and most of it sits entirely idle. For UK homeowners, a lifetime of property ownership has created an estimated $5.1 trillion in aggregate housing equity, much of it concentrated in the hands of older homeowners approaching or in retirement.

Key stat: $32.1 trillion — total US home equity in Q1 2024 — the largest store of household wealth in American history (CoreLogic / Federal Reserve)

Key stat: GBP 2.6 billion — equity release lending in the UK in 2023 alone — reflecting surging demand among older homeowners seeking to access property wealth (Equity Release Council)

What Does 'Without Touching Your Mortgage' Actually Mean?

When we refer to borrowing from your home without touching your mortgage, we mean accessing your home equity through a separate financial product that sits alongside your existing mortgage rather than replacing it. This is a critically important distinction.The alternative — a cash-out refinance — involves replacing your existing mortgage entirely with a new, larger one, releasing the difference as a lump sum. While this can sometimes make sense when prevailing rates are significantly lower than your current mortgage rate, in a period of elevated interest rates it means abandoning a potentially lower fixed rate and refinancing your entire outstanding balance at a higher rate. For homeowners who locked in historically low rates between 2020 and 2022, a cash-out refinance is almost certainly the most expensive way to access equity available to them.

For US homeowners who locked in a 30-year fixed mortgage at 2.75%–3.5% between 2020 and 2022, a 2024 cash-out refinance at 7%+ would increase the interest cost on their entire outstanding balance. Borrowing separately through a HELOC or home equity loan — even at 8–9% — keeps the lower rate intact on the main mortgage and only charges the higher rate on the new equity borrowed.

The products that allow you to access equity without remortgaging are therefore not just convenient — in the current interest rate environment, they are often significantly cheaper in total interest terms than replacing a low-rate existing mortgage. Understanding this distinction is the foundation of the entire case for these products.

Option 1: Home Equity Line of Credit (HELOC)

A Home Equity Line of Credit — a HELOC — is a revolving credit facility secured against your home's equity, operating in a manner similar to a credit card. Once approved, you receive access to a credit line up to a maximum limit, and you can draw from it, repay it, and redraw as needed during the draw period, which typically lasts five to ten years. Only the amount you actually draw incurs interest, making it ideal for ongoing or uncertain expenditure needs.How HELOCs Work

- The borrowing limit is typically set at 80-85% of your home's appraised value, minus your outstanding mortgage balance. For example, a home worth $400,000 with a $200,000 mortgage balance could support a HELOC of up to $140,000 at 85% CLTV.

- During the draw period, you make interest-only payments on the amount drawn. The interest rate is variable, tied to an index such as the US Prime Rate or SOFR.

- After the draw period ends, the HELOC enters a repayment period of typically 10-20 years during which the outstanding balance is repaid with principal and interest.

- In the UK, HELOCs are less common but equivalent products are available through specialist lenders and certain banks as flexible second charge mortgages.

Best Uses for a HELOC

HELOCs are ideally suited for expenditures that are staggered over time: home renovation projects paid in phases, ongoing education costs, a business launch requiring phased funding, or as a flexible emergency reserve for those without sufficient liquid savings. The flexibility to draw only what is needed — and repay it before drawing again — makes HELOCs one of the most capital-efficient borrowing tools available to homeowners.Average HELOC rate (2024): 8.5%–9.2% — variable, compared to credit card APRs averaging 20.75% — representing a potential interest saving of 11–12 percentage points on the same borrowed amount

Option 2: Home Equity Loan (Second Mortgage)

A home equity loan provides a fixed lump sum borrowed against your equity, repaid over a fixed term at a fixed interest rate. Unlike a HELOC, a home equity loan delivers the entire amount upfront and begins repayment immediately with equal monthly instalments of principal and interest. It is the predictability and certainty of this structure that makes it attractive for specific, defined borrowing needs.Key Characteristics

- Fixed interest rate for the entire loan term — typically 5 to 30 years — providing payment certainty and protection against rate rises.

- Lump-sum disbursement makes it ideal for one-time, specific expenditures: a defined home renovation, debt consolidation, a large purchase, or education fees.

- The loan is secured against your property as a second charge, meaning the original mortgage lender retains first priority in the event of default. Home equity loan lenders hold second priority.

- Closing costs typically range from 2-5% of the loan amount, which should be factored into the total cost comparison against other borrowing options.

A home equity loan is particularly well-suited to debt consolidation. A homeowner carrying $30,000 in credit card debt at 20% APR could consolidate this into a home equity loan at 8.5% fixed, reducing annual interest costs from approximately $6,000 to $2,550 — a saving of $3,450 per year — while simultaneously converting variable, unpredictable payments into a single, fixed monthly obligation. The trade-off is that unsecured debt becomes secured debt: defaulting now puts the home at risk.

Critical caution: Consolidating unsecured debt into a home equity loan reduces your interest rate but increases your risk. If you subsequently cannot make payments on the consolidated loan, your home is at risk of repossession. Only proceed with debt consolidation using home equity if you are confident in your long-term ability to service the new repayment and have addressed the spending behaviours that created the original debt.

Option 3: Second Charge Mortgage (UK)

In the UK, the primary product for borrowing against home equity without remortgaging is the second charge mortgage — a separate secured loan taken out alongside an existing first charge mortgage. Second charge mortgages are regulated by the Financial Conduct Authority (FCA) and offer UK homeowners an alternative to remortgaging when their existing deal has significant early repayment charges or a rate worth protecting.Second charge mortgages are available from specialist lenders including Shawbrook Bank, Together Money, Pepper Money, and United Trust Bank, among others. Loan amounts typically range from £10,000 to £2.5 million, with terms of 3 to 25 years. Interest rates are generally higher than first charge mortgages — reflecting the higher risk to the second charge lender — but significantly below unsecured borrowing rates such as personal loans or credit cards.

When Second Charge Mortgages Make Sense in the UK

- Your existing mortgage has substantial early repayment charges that make full remortgaging prohibitively expensive during the current fixed term.

- Your current mortgage rate is significantly below market rates — protecting it is worth the higher rate on a smaller second charge facility.

- You need to borrow more than unsecured personal loans allow (typically capped at £25,000-£50,000) or for a purpose that personal loan lenders will not fund.

- Your credit history prevents accessing competitive first charge remortgage rates, but sufficient equity and property security makes a second charge application viable.

Option 4: Equity Release (UK Homeowners Aged 55+)

Equity release is a product category specifically designed for UK homeowners aged 55 and over who want to access the equity in their home without making monthly repayments. The most common form is the lifetime mortgage, in which a loan is taken out against the property's value and interest rolls up — compounding over time — until the property is sold, typically when the homeowner moves into care or passes away.The equity release market in the UK is significant and growing: the Equity Release Council reported GBP 2.6 billion in equity release lending in 2023, serving over 93,000 new and returning customers. Products are regulated by the FCA and must comply with the Equity Release Council's Standards, which include a no-negative equity guarantee — ensuring that no matter how much interest accumulates, borrowers will never owe more than the property is worth.

Lifetime Mortgage Key Features

- No monthly repayments required — interest rolls up and is settled when the property is sold.

- The homeowner retains full ownership and the right to live in the property for life.

- Loan amounts typically range from 20% to 60% of property value, depending on age and product.

- The no-negative equity guarantee (a mandatory Equity Release Council standard) protects beneficiaries from inheriting debt greater than the property value.

- Optional partial repayment facilities allow interest to be paid voluntarily, reducing the compounding effect.

Equity release compound interest warning: 5.5%–6.5% typical fixed rate — at 6% compound interest, a GBP 100,000 equity release loan doubles to GBP 200,000 in approximately 12 years — making it essential to understand the long-term cost before proceeding

Equity release is not appropriate for everyone. The compounding of interest over a long period can significantly erode the inheritance available to beneficiaries. However, for homeowners who are asset-rich and income-poor — with substantial property wealth but limited pension income — equity release can provide life-changing financial freedom. The decision should always be made with independent financial advice from a qualified equity release adviser regulated by the FCA.

Side-by-Side Comparison: All Four Options

The comparison table below summarises the key characteristics of each equity access method, including whether your existing mortgage is affected, to help you identify the most suitable option for your situation:

Key Risks and Essential Safeguards

All forms of equity borrowing share a fundamental characteristic: your home is the collateral. This makes them categorically different from unsecured personal loans or credit cards. The following risks and safeguards apply across all products:- Property repossession risk: Failure to maintain repayments on a HELOC or home equity loan places your home at risk of repossession. Only borrow what you can afford to repay throughout the full term, including under adverse income scenarios such as redundancy, illness, or interest rate rises.

- Falling property values: If property prices fall significantly after you borrow, you could enter negative equity — owing more than the property is worth. Borrowing conservatively within your equity — well below the maximum LTV — provides a buffer against price corrections.

- Interest rate risk (HELOCs): Variable-rate HELOCs expose you to interest rate rises throughout the draw period. Model the impact of a 2-3% rate increase on your monthly payments before committing, and consider whether a fixed-rate home equity loan provides better payment certainty for your situation.

- Compound interest risk (equity release): The compounding of interest in a lifetime mortgage over a 10-20 year period can substantially reduce or eliminate the equity available to your estate. Always obtain a projection of the outstanding balance at multiple future dates before proceeding.

- Independent legal and financial advice: For all equity borrowing products — and especially for equity release — independent professional advice from a qualified adviser is strongly recommended and, in the case of equity release, required by most lenders. The cost of advice is modest relative to the financial significance of these decisions.

Conclusion

The equity stored in your home does not have to remain inaccessible until you sell. For homeowners who have built significant equity over years of mortgage payments and property appreciation, a range of carefully structured financial products provides the ability to access that wealth — for home improvements, debt consolidation, investment, education, or retirement income — without disturbing the existing mortgage or sacrificing the rate protection it provides.The right product depends entirely on your specific circumstances: your age, the size of your equity, your current mortgage terms, your need for lump-sum versus flexible access, and whether you require monthly payment obligations or can defer repayment. A HELOC offers the most flexible ongoing access. A home equity loan provides the certainty of a fixed rate and fixed repayment. A second charge mortgage is the UK's answer for homeowners with protected existing deals. Equity release provides a monthly-payment-free option for older UK homeowners with property wealth and limited income.

Whatever route you choose, approach it with clear eyes about the risks involved, a precise understanding of the total cost over the product's full term, and qualified professional advice to validate your decision. Your home is your most valuable financial asset — accessing its equity wisely can transform your financial position; accessing it carelessly can put the asset itself at risk. The difference between those two outcomes is preparation, information, and advice.

Frequently Asked Questions (FAQ)

Can I borrow against my home equity if I still have an outstanding mortgage?

Yes. All of the products covered in this guide — HELOCs, home equity loans, second charge mortgages, and equity release — are specifically designed for homeowners who still have an existing mortgage. What matters is not whether you have a mortgage, but how much equity you have: the difference between your property's current market value and your outstanding mortgage balance. Most lenders require at least 15-20% equity to qualify for a HELOC or home equity loan, and more for equity release products.What is the difference between a HELOC and a home equity loan?

A HELOC is a revolving line of credit — you draw from it as needed, repay it, and draw again, paying variable interest only on the amount outstanding. A home equity loan is a fixed-term, fixed-rate lump sum repaid in equal monthly instalments from the outset. The choice between them depends on whether you need ongoing flexible access (HELOC) or a single, defined amount with payment certainty (home equity loan).Is equity release safe? What are the risks?

Equity release products regulated by the FCA and compliant with Equity Release Council standards include a no-negative equity guarantee, protecting borrowers and their estates from ever owing more than the property is worth. However, the key risk is compound interest erosion: a 6% interest rate rolling up for 15-20 years can substantially reduce or eliminate the equity available to your estate. Equity release should always be discussed with a qualified independent financial adviser and your family, as it materially affects the inheritance you can leave.How much can I borrow against my home equity?

For HELOCs and home equity loans in the US, the maximum combined loan-to-value (CLTV) is typically 80-85% of your property's appraised value. For a home worth $400,000 with a $200,000 mortgage, the maximum HELOC or home equity loan at 85% CLTV would be $140,000. In the UK, second charge mortgage lenders and equity release providers apply their own LTV criteria — typically ranging from 65-80% for second charge mortgages and 20-60% for equity release, depending on age and product.Is interest on a HELOC or home equity loan tax deductible?

In the United States, under the Tax Cuts and Jobs Act of 2017, interest on a HELOC or home equity loan is tax deductible only if the funds are used to buy, build, or substantially improve the home that secures the loan. If you use the funds for other purposes — such as debt consolidation or personal spending — the interest is not deductible. In the UK, interest on second charge mortgages used for buy-to-let properties may be deductible against rental income, but interest on borrowing secured against a primary residence for personal purposes is not tax-deductible. Always consult a qualified tax adviser to confirm the deductibility rules applicable to your specific situation.

External References

The following authoritative sources were used in researching this article and are recommended for further guidance:1. CoreLogic — Homeowner Equity Report Q1 2024

https://www.corelogic.com/intelligence/homeowner-equity-insights/

2. Federal Reserve — Household Debt and Credit Statistics

https://www.federalreserve.gov/releases/g19/current/

3. Bankrate — Current HELOC and Home Equity Loan Rates (2024)

https://www.bankrate.com/home-equity/

4. Consumer Financial Protection Bureau (CFPB) — What Is a HELOC?

https://www.consumerfinance.gov/ask-cfpb/what-is-a-home-equity-line-of-credit-heloc-en-106/

5. Equity Release Council (UK) — Annual Market Statistics

https://www.equityreleasecouncil.com/data-hub/

6. MoneyHelper (UK) — Equity Release and Second Charge Mortgages

https://www.moneyhelper.org.uk/en/homes/buying-a-home/equity-release

7. Financial Conduct Authority (FCA) — Second Charge Mortgages Explained

https://www.fca.org.uk/consumers/mortgages

8. Investopedia — HELOC vs Home Equity Loan: Which Is Right for You?

https://www.investopedia.com/mortgage/heloc/

0 Comments Comments