Vehicles & Cars

Can I Choose My Next Car Without Crashing Finances?

TABLE OF CONTENTS

- Why Car Buying Decisions Are a Major Financial Event

- Setting a Realistic Car Budget

- New vs Used: Which Makes Financial Sense?

- Understanding Car Finance Options

- The Hidden Costs of Car Ownership

- Negotiating the Best Deal

- Electric and Hybrid: Do They Save You Money?

- Conclusion

- Frequently Asked Questions

- References

Why Car Buying Decisions Are a Major Financial Event

Buying a car is almost always one of the two or three largest financial decisions a household will make — after a home and perhaps a degree. Yet while most people will spend months agonising over a mortgage, many car buyers spend less than a week comparing their options before signing on the dotted line. The result is that cars, more than any other major purchase, tend to be bought with the heart and justified with the head — often imperfectly.In the UK, the average new car now costs more than £33,000. Even a three-year-old used model in good condition typically commands £14,000 to £20,000. Add insurance, fuel, servicing, road tax, and tyres, and you are looking at a total annual cost of ownership that can easily exceed £6,000 for an average family car. For many households, this makes the car the second-biggest item in the monthly budget after the mortgage or rent.

The good news is that with a structured approach — budgeting carefully, comparing finance options, understanding the full cost of ownership, and negotiating intelligently — it is entirely possible to choose a car you love without destabilising your finances. This guide walks you through every step of that process.

2. Setting a Realistic Car Budget

The most common mistake car buyers make is to focus exclusively on the monthly payment rather than the total cost of the vehicle over the ownership period. A monthly payment of £300 sounds manageable, but over four years that is £14,400 — plus interest, plus insurance, plus servicing. The monthly figure is the starting point of your budgeting, not the ending point.Financial advisers commonly suggest that total vehicle costs — including finance repayments, insurance, fuel, and maintenance — should not exceed 15% to 20% of your net monthly household income. If your household takes home £3,500 a month, that means keeping all car-related outgoings under £525 to £700. This is a useful sanity check before you start browsing showrooms.

The monthly payment is where car finance marketing begins. Your financial planning needs to start from total cost of ownership.

— MONEY ADVICE SERVICE

Begin by listing three figures: the maximum deposit you can comfortably put down (drawing on savings but leaving an emergency fund intact), the maximum monthly payment that fits your budget after all essential outgoings, and the maximum total amount you are willing to spend. The lowest of these three constraints defines your true budget ceiling — not the highest.

Budget Checklist: Before You Visit a Showroom

- Calculate your net monthly income minus all fixed outgoings

- Set a maximum car cost at 15-20% of net monthly income

- Check your credit score at Experian, Equifax, or TransUnion (free)

- Decide on deposit: aim for at least 10% of vehicle value

- Research insurance costs for specific models before falling in love with them

- Factor in fuel, road tax, and servicing before committing

New vs Used: Which Makes Financial Sense?

The financial case for buying used is compelling and well-documented. A new car typically loses between 15% and 25% of its value the moment it is driven off the forecourt, and around 40% to 50% of its value within the first three years. This depreciation is the largest single cost of owning a car — dwarfing interest charges, fuel, or servicing — yet it is largely invisible because it does not appear on a monthly statement.By buying a car that is two to four years old, you let the first owner absorb that steep initial depreciation curve. You still get a relatively modern, reliable car — often still under manufacturer warranty if purchased from a franchised dealer — but at a significantly lower price. In 2026, the used car market in the UK has benefited from a surge in nearly-new electric and hybrid vehicles coming off lease, offering particularly good value in those categories.

That said, new cars are not always the wrong financial choice. Manufacturer finance deals on new models — particularly 0% or near-0% PCP offers run as promotional incentives — can occasionally make a new car cheaper to finance than an equivalent used car on a commercial rate. If you plan to keep the car for seven years or more, spreading the depreciation over a longer period reduces its per-year impact significantly. The key is to run the numbers for your specific situation rather than accepting a general rule of thumb.

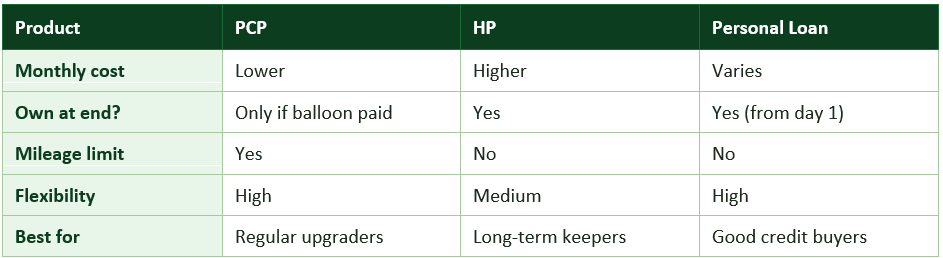

Understanding Car Finance Options

The vast majority of cars in the UK are now bought on finance: according to the Finance & Leasing Association, around 91% of new cars registered in 2025 were funded through some form of credit. Understanding which product suits your circumstances is one of the most financially consequential decisions in the whole car-buying process.Personal Contract Purchase (PCP)

PCP is the most popular car finance product in the UK. You pay a deposit, then fixed monthly payments over a term (typically two to four years), and at the end you have three choices: hand the car back, pay a final 'balloon' payment to own it outright, or part-exchange it for a new deal. Monthly payments are relatively low because you are only financing the depreciation during your ownership period, not the full vehicle value.PCP works well if you like changing your car regularly and enjoy driving a newer vehicle than you could otherwise afford. It works poorly if you exceed the agreed mileage limit (excess mileage charges can be steep), if the car suffers damage beyond fair wear and tear, or if you intend to own the car at the end — in which case the balloon payment often means you pay more in total than with a hire purchase or personal loan.

Hire Purchase (HP)

With HP, you pay a deposit and then fixed monthly instalments, and the car is yours outright at the end of the term. There is no balloon payment, no mileage limit, and no end-of-contract negotiation. Total interest costs are usually higher than PCP on a monthly basis, but the overall picture can be cheaper if you keep the car for a long time after the finance ends — because there is no balloon to pay and no need to refinance.Personal Loan

A personal loan from a bank or building society means you own the car outright from day one. Interest rates are often lower than dealer finance (particularly for borrowers with good credit scores), and there are no mileage limits or condition requirements. The main risk is that if you borrow more than the car is worth at any point and then need to sell, you may be in negative equity.

The Hidden Costs of Car Ownership

The sticker price or the monthly finance payment is only the beginning. A comprehensive budget must also account for the full range of running costs — many of which catch first-time car owners by surprise.Insurance is typically the largest annual running cost after finance repayments. For drivers under 25, comprehensive insurance on even a modest hatchback can exceed £2,000 a year. Telematics ('black box') policies can reduce this significantly for younger drivers who demonstrate safe driving habits. For all drivers, comparing quotes annually and considering a higher voluntary excess can yield meaningful savings.

Servicing, MOT, and tyres represent another significant outlay. A full service on an average family car costs between £150 and £300 at an independent garage, rising to £400 or more at a franchised dealer. Tyres on a mid-sized car typically cost £80 to £130 each; brakes, batteries, and other consumables add further unpredictable costs. A rule of thumb is to budget at least £600 to £800 a year for mechanical upkeep on a car that is more than three years old.

Road tax (Vehicle Excise Duty) varies dramatically by vehicle. Zero-emission electric vehicles attract no road tax in 2026, while some older petrol and diesel cars can cost over £600 per year. Fuel costs depend heavily on your annual mileage: at UK average pump prices, a car achieving 40mpg and covering 8,000 miles a year will spend approximately £1,200 on fuel. A larger SUV achieving 25mpg will spend close to £2,000.

Negotiating the Best Deal

One of the most consistent findings from consumer research is that car buyers who negotiate achieve meaningfully better outcomes than those who accept the first price offered. Yet many buyers feel uncomfortable haggling, particularly in a showroom environment. Understanding a few principles can help.Dealers make margin not just on the vehicle price but also on finance, insurance add-ons, extended warranties, and paint protection products. This means there is often room to negotiate across multiple dimensions simultaneously. If the dealer will not reduce the vehicle price, you may be able to negotiate a better finance rate, a larger contribution toward your deposit, or free accessories.

Timing matters. Dealers are under the most pressure to hit sales targets at the end of the month, the end of the quarter, and the end of the registration year (March and September in the UK). Visiting at these points can significantly increase your negotiating leverage. Similarly, being a cash buyer — or having a pre-approved personal loan — removes the dealer's most profitable revenue stream (finance commission) and can be used as a negotiating chip.

Always get the final agreed price in writing before handing over any money, and read the entire finance agreement carefully before signing. Pay particular attention to the annual percentage rate (APR), the total amount repayable, the mileage limit (for PCP), and the terms for early settlement.

Electric and Hybrid: Do They Save You Money?

The financial case for electric vehicles (EVs) has become considerably more nuanced in 2026 than the headlines suggest. EVs have substantially lower fuel and servicing costs than petrol equivalents — electricity costs roughly a third of the equivalent fuel cost per mile for most drivers, and EVs have fewer moving parts, meaning lower servicing bills. Road tax for EVs is zero, and company car drivers benefit from significantly lower Benefit-in-Kind tax rates.However, EVs still carry a significant purchase price premium over comparable petrol models — typically £4,000 to £8,000 for mainstream models — and the used EV market, while growing rapidly, still lacks the depth and price transparency of the traditional used car market. Battery health and range are also considerations that require careful investigation before buying a used EV.

Plug-in hybrid vehicles (PHEVs) occupy a middle ground. If your daily commute is less than 30 miles and you can charge at home, a PHEV can offer near-EV running costs for local journeys while retaining the flexibility of a petrol engine for longer trips. If you cannot charge at home — in a flat or terraced house without a driveway, for instance — a PHEV offers little benefit over a standard hybrid and may work out more expensive overall.

For most buyers, the financially optimal choice in 2026 is a nearly-new electric or hybrid vehicle from a reputable brand, purchased two to three years into its depreciation curve, with a solid battery health record and charged primarily on a home charger or workplace tariff.

CONCLUSION

Choosing your next car without crashing your finances is entirely achievable — but it requires discipline, preparation, and a willingness to let the numbers guide you as much as your instincts. The key principles are consistent across all buyer situations: know your true total budget before you start looking, understand the full cost of ownership beyond the monthly payment, compare finance products independently rather than relying solely on dealer finance, and negotiate across the whole deal rather than just the purchase price.The car market in 2026 offers more choice — and more complexity — than at any point in history. Petrol, diesel, hybrid, plug-in hybrid, and electric powertrains all have different ownership economics that suit different drivers and lifestyles. The best car for your finances is not necessarily the one with the lowest price tag or the flashiest specification: it is the one whose total cost of ownership — purchase price, depreciation, fuel, insurance, and servicing — fits most comfortably within your budget over the length of time you intend to own it.

Frequently Asked Questions

How much should I spend on a car relative to my income?

Most financial advisers suggest keeping total car-related costs — including finance, insurance, fuel, and maintenance — to no more than 15% to 20% of your net monthly income. For a household taking home £3,500 per month, that means a maximum of £525 to £700 per month on all car-related expenses combined, not just the monthly payment.Is PCP or HP better for my finances?

It depends on your priorities. PCP offers lower monthly payments and flexibility to change cars regularly, but you do not automatically own the car at the end and there are mileage limits. HP costs more per month but you own the car outright at the end with no balloon payment. If you keep a car for a long time, HP often works out cheaper overall. If you prefer regular upgrades and predictable payments, PCP may suit better — but always compare the total amount repayable, not just the monthly figure.Is it better to buy new or used?

Used cars are almost always the better financial choice for most buyers. New cars depreciate rapidly — losing up to 25% of their value in the first year alone. By buying a two- to four-year-old car, you avoid the steepest part of that depreciation curve. Exceptions exist: manufacturer 0% finance promotions on new cars, or plans to keep a car for many years, can occasionally make new the wiser option.What credit score do I need to get good car finance rates?

Most lenders offer their best rates to borrowers with a credit score rated 'good' or 'excellent' — typically 670 or above on major scoring systems. You can check your credit score for free using services such as Experian, Equifax, or ClearScore. If your score is below average, consider improving it before applying (paying down existing debt, registering on the electoral roll, ensuring no errors appear on your report), or factor in a higher APR when budgeting.Are electric cars cheaper to run than petrol cars?

For most drivers, yes — but the picture depends on your circumstances. Electricity costs roughly one-third of the equivalent fuel cost per mile. EVs also have lower servicing costs and pay no road tax in 2026. However, the higher purchase price of new EVs means the breakeven point against a petrol equivalent can take several years to reach. Used EVs offer better value, but buyers should check battery health carefully before purchase.Can I negotiate the price on a financed car?

Yes, and you should. The vehicle price, the finance rate, and optional extras are all negotiable. Dealers often have more flexibility on finance rates and added extras than on the headline vehicle price. Shopping at the end of the month or quarter, having a pre-approved loan as leverage, and being willing to walk away are all effective negotiating tactics. Always get the final agreed terms in writing before signing.References and Further Reading

Money Helper (MaPS) — Car Finance Guide https://www.moneyhelper.org.uk/en/everyday-money/credit/car-financeFinance & Leasing Association — UK Car Finance Statistics 2025 https://www.fla.org.uk/news-research/motor-finance-statistics/

Which? — Best and Worst Used Cars to Buy https://www.which.co.uk/reviews/used-cars

Gov.uk — Vehicle Excise Duty Rates 2026 https://www.gov.uk/vehicle-tax-rate-tables

Auto Trader — Car Valuation and Market Data https://www.autotrader.co.uk/content/advice/car-finance-explained

Experian — Check Your Credit Score (Free) https://www.experian.co.uk/consumer/credit-score.html

ZapMap — EV Charging Cost Calculator https://www.zap-map.com/

Confused.com — Car Insurance Comparison https://www.confused.com/car-insurance

0 Comments Comments