Real Estate

High Housing Costs Push Foreclosures to Six-Year High

Homeowners insurance up 70% in five years. Property taxes climbing. Mortgage rates still above 6%. The cost of simply owning a home — not buying one — is now pushing tens of thousands of American families into foreclosure every single month.

This is the highest rate of foreclosure activity the US has seen since 2019 — before the pandemic-era freeze on evictions and foreclosures artificially suppressed the numbers. Through the middle of 2025, roughly 188,000 properties had received foreclosure filings, putting the country on track to far exceed the approximately 322,000 properties that went into foreclosure across the whole of 2024. That trend has continued into 2026, with foreclosure filings rising every single month on a year-over-year basis.

To be clear about the context: these numbers are still well below the catastrophic levels of 2008 to 2012, when millions of homes entered foreclosure every year and the financial system nearly collapsed. At the 2010 peak, foreclosure filings affected 2.23% of all US housing units. Today's figure is around 0.26%. But the direction of travel is unmistakable, and the causes are different — and in some ways more structural — than the last crisis.

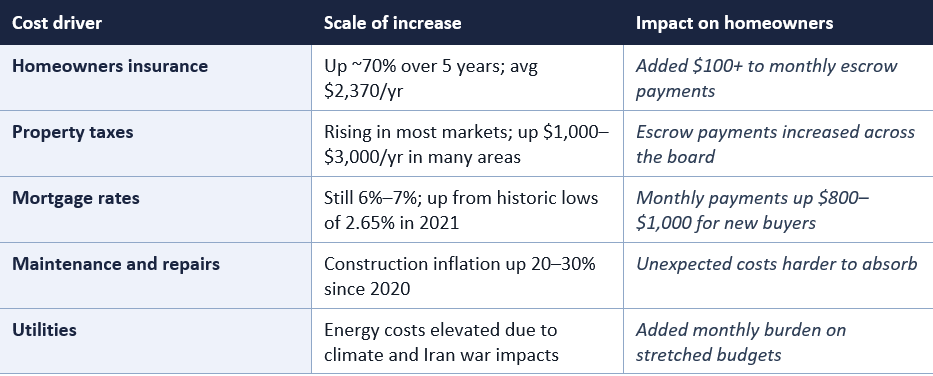

Single-family homeowners with a mortgage today pay an average of $2,370 a year for homeowners insurance — up nearly 70% from five years ago, according to data from ICE Mortgage Technology. Property taxes have risen sharply in most major markets as county assessors have caught up with pandemic-era home price increases. Utilities costs have climbed. Maintenance and repair bills, driven by inflation in the construction labour and materials sectors, have increased significantly. And for many homeowners — particularly in high-risk states like Florida, California, Texas, and Colorado — insurance is becoming unaffordable or completely unavailable from standard carriers.

All of these rising costs associated with holding a home create increasing pressure on existing homeowners to continue to be able to afford and pay for their mortgages.

— GEOFF SMITH, EXECUTIVE DIRECTOR, INSTITUTE FOR HOUSING STUDIES AT DEPAUL UNIVERSITY (CBS NEWS, 2025)

The result is what housing economists call a "cost-of-holding" crisis — distinct from the "cost-of-buying" crisis that gets more headlines. A family that bought a $300,000 house in 2019 at a 3.5% mortgage rate may have a perfectly manageable mortgage payment of around $1,350 a month. But if their homeowners insurance has risen from $1,200 to $2,370 a year, their property taxes have increased by $2,000 a year, and their utility and maintenance costs have gone up substantially, their total housing cost may have grown by $500 a month or more with no increase in their income to match.

In high-risk states, the situation is far more severe. In Florida and California, homeowners insurance can account for 15% to 20% of a homeowner's total monthly housing payment. In some counties — particularly those exposed to hurricane risk, wildfires, or flooding — standard insurers have pulled out of the market entirely, forcing homeowners onto expensive state-backed plans of last resort.

The reason premiums have risen so sharply is not difficult to understand. In 2023, US insurers paid out $1.11 in claims for every $1.00 they earned in homeowners insurance premiums. Climate-driven losses have surged. The January 2025 Los Angeles wildfires resulted in an estimated $4 billion in losses for California's FAIR Plan. Hurricane Milton caused $3.62 billion in residential losses in Florida. By September 2025, severe convective storms — tornadoes, hailstorms, and high winds across the Midwest and Southeast — had caused $42 billion in insured losses.

Research from the Federal Reserve Bank of Dallas has found that a homeowner is significantly more likely to become delinquent on their mortgage in the months following an increase in their homeowners insurance premium. The connection is direct: when insurance costs rise and the increase is rolled into a monthly mortgage escrow payment, many households — particularly those already stretched thin — find they simply cannot keep up. Premiums are projected to rise another 8% in both 2026 and 2027.

In rapidly appreciating markets, property tax bills doubled or even tripled between 2020 and 2025. A homeowner who bought a modest house in a Texas suburb for $280,000 in 2018 and watched it appreciate to $420,000 by 2022 might have seen their annual property tax bill climb from $5,600 to $8,400 — an extra $233 a month added to their housing costs with no notice and no recourse other than a formal appeal process that most homeowners do not know how to navigate.

Unlike mortgage payments, property taxes cannot be refinanced or restructured. They are a fixed obligation that rises with the assessed value of the property, regardless of whether the homeowner's income has kept pace. For retired homeowners on fixed incomes, for families who bought during the pandemic at the top of the market, and for lower-income homeowners in gentrifying neighbourhoods, escalating property taxes have become the single biggest threat to keeping their homes.

Directly, homeowners who took out adjustable-rate mortgages in 2021 and 2022 — when rates were artificially low — have seen their payments reset to much higher levels as those loans have reached their adjustment periods. FHA loans, which serve first-time buyers and lower-income households with down payments as low as 3.5%, have been particularly hard hit. The FHA loan delinquency rate reached 11.52% in the fourth quarter of 2025 — the highest level since the second quarter of 2021, and 6.5 times higher than the 1.78% conventional loan delinquency rate in the same period.

Indirectly, high mortgage rates have created a "lock-in effect" that has frozen the housing market. Homeowners who secured 3% or below mortgages in 2020 and 2021 are reluctant to sell and give up those rates by taking out a new mortgage at 6% or 7%. This has suppressed housing supply, kept prices high, and reduced the ability of struggling homeowners to sell their way out of trouble before reaching foreclosure. When your house is worth more than you owe but selling it would require you to take on a mortgage at twice your current rate, selling becomes a much less attractive option than it might appear on paper.

Housing economists at foreclosuredatahub.com note that mortgage payments now consume over 30% of median household income — compared with 21% before the pandemic. To restore pre-pandemic affordability, one of three things would need to happen: mortgage rates would need to fall to around 2.65%, median household income would need to rise 56%, or home prices would need to drop 35%. None of these outcomes is considered likely in the near term. Major housing expenses exceeded historic affordability norms in 96.6% of US counties analysed in the first quarter of 2026.

First-time buyers who purchased during 2021 and 2022 — at or near peak prices, with thin down payments and limited equity cushions — are disproportionately represented in foreclosure filings. Many of these buyers used FHA or VA loans with down payments of 3% to 5%. When home prices in some markets have softened slightly and insurance and tax bills have risen sharply, these households have very little financial buffer.

Lower-income and minority homeowners face compounded risks. Research from Americans for Financial Reform shows that 7% of homeowners lack homeowners insurance entirely — a proportion that is higher among lower-income households and households of colour. When an uninsured homeowner faces a significant repair need — a roof damaged by a hailstorm, a basement flooded — the choice between making the repair and making the mortgage payment becomes stark. Research also shows that insurance premium increases falling on the 20% of ZIP codes with the highest climate risk outpaced overall inflation by nearly 15 percentage points between 2018 and 2022.

Older homeowners on fixed incomes represent a third group at serious risk. Many bought their homes decades ago and have substantial equity, but their monthly income from Social Security or pension is no longer sufficient to cover rising insurance premiums, property taxes, maintenance costs, and healthcare expenses simultaneously. For these homeowners, the threat of foreclosure often goes unnoticed until it is nearly too late.

Florida and Texas stand out for different reasons. Florida faces a severe insurance crisis driven by hurricane risk, with many homeowners unable to find or afford coverage from standard carriers. Texas leads the country in raw foreclosure volume — with 3,390 foreclosure starts in February 2026 alone — driven by a combination of insurance cost spikes, rising property taxes, and economic pressures in certain regional markets. States like California, with its high baseline housing costs, and Illinois, with its historically high property taxes, also appear consistently among the highest-risk markets.

Markets with a higher proportion of FHA loans — typically areas where first-time and lower-income buyers are concentrated — are seeing the steepest increases in delinquencies and defaults. The geographic pattern reflects the structural concentration of the crisis: it is worst where affordability was already stretched the thinnest, insurance costs are rising the fastest, and borrowers have the least financial cushion to absorb shocks.

Today's situation is structurally different. The vast majority of current mortgages were underwritten to post-2008 standards. American homeowners hold roughly $32 trillion in home equity — a record high. Mortgage delinquencies overall remain near historical lows, even as foreclosure filings rise, because many homeowners who fall behind are able to work out payment plans with their lenders or sell their homes before reaching the auction stage.

What today's foreclosure increase represents is better described as market normalisation — a return to the levels of distress that existed before pandemic-era forbearance programmes and emergency protections artificially suppressed foreclosure activity. It is also a structural warning about the sustainability of homeownership costs. The households entering foreclosure today are not victims of fraudulent loans. They are victims of an affordability environment that has made it increasingly difficult for ordinary Americans to hold onto homes they own, in communities they have lived in for years or decades, because the annual cost of insuring, taxing, and maintaining that home has grown faster than their income.

This is not yet a systemic crisis, and most American homeowners have enough equity and institutional protection to avoid foreclosure if they act early and seek help. But the trend is real, the numbers are rising, and the structural pressures behind them are unlikely to resolve quickly. Homeowners who understand what is driving this crisis — and what options they have — are in a far better position than those who simply wait and hope for the best.

ATTOM / Lamun Mock Cunnyngham — Rising Foreclosure Rates in 2026 https://www.lamunmock.com/news/rising-foreclosure-rates-in-2026

ForeclosureDataHub — Is the Housing Market Going to Crash in 2026? https://www.foreclosuredatahub.com/blog/housing-market-crash-2026-foreclosure-data-analysis

Nolo — Rising US Foreclosure Rates in 2025: Causes, Trends, and Homeowner Protections https://www.nolo.com/legal-encyclopedia/are-foreclosures-on-the-rise.html

Nolo — Rising US Foreclosure Rates in 2026: What Homeowners and Buyers Should Know https://www.nolo.com/legal-encyclopedia/foreclosure-rates-2023.html

HomeBuyingInstitute — Why Home Insurance Premiums in the US Are Still Rising in 2026 https://homebuyinginstitute.com/mortgage/why-home-insurance-premiums-are-rising/

TABLE OF CONTENTS

- The Six-Year High: What the Numbers Say

- The Real Culprit: The Rising Cost of Owning a Home

- The Insurance Crisis Driving Foreclosures

- Property Taxes: The Hidden Time Bomb

- Mortgage Rates and the Affordability Cliff

- Who Is Being Hit the Hardest

- Which States Have the Highest Foreclosure Rates

- Is This 2008 All Over Again?

- What Homeowners Can Do Right Now

- Conclusion

- Frequently Asked Questions

- References

The Six-Year High: What the Numbers Say

The number of Americans losing their homes to foreclosure has been climbing for more than a year — and the pace is accelerating. According to ATTOM, a national property data company, foreclosure filings in the United States rose year-over-year for 12 consecutive months as of February 2026. In January 2026, over 40,500 properties received a foreclosure filing — including default notices, scheduled auctions, and bank repossessions. That was a 32% increase compared with January 2025. February saw 38,840 filings, with foreclosure starts up 26% and completed foreclosures jumping roughly 59% annually.This is the highest rate of foreclosure activity the US has seen since 2019 — before the pandemic-era freeze on evictions and foreclosures artificially suppressed the numbers. Through the middle of 2025, roughly 188,000 properties had received foreclosure filings, putting the country on track to far exceed the approximately 322,000 properties that went into foreclosure across the whole of 2024. That trend has continued into 2026, with foreclosure filings rising every single month on a year-over-year basis.

To be clear about the context: these numbers are still well below the catastrophic levels of 2008 to 2012, when millions of homes entered foreclosure every year and the financial system nearly collapsed. At the 2010 peak, foreclosure filings affected 2.23% of all US housing units. Today's figure is around 0.26%. But the direction of travel is unmistakable, and the causes are different — and in some ways more structural — than the last crisis.

The Real Culprit: The Rising Cost of Owning a Home

In 2008, the foreclosure crisis was driven primarily by reckless mortgage lending — subprime loans, adjustable-rate mortgages that reset to unaffordable levels, and outright fraud. Today's foreclosure wave has a different cause. Most of the homeowners losing their homes to foreclosure in 2025 and 2026 have fixed-rate mortgages at reasonable interest rates. Many have significant equity in their properties. The problem is not their mortgage payment. The problem is everything else.Single-family homeowners with a mortgage today pay an average of $2,370 a year for homeowners insurance — up nearly 70% from five years ago, according to data from ICE Mortgage Technology. Property taxes have risen sharply in most major markets as county assessors have caught up with pandemic-era home price increases. Utilities costs have climbed. Maintenance and repair bills, driven by inflation in the construction labour and materials sectors, have increased significantly. And for many homeowners — particularly in high-risk states like Florida, California, Texas, and Colorado — insurance is becoming unaffordable or completely unavailable from standard carriers.

All of these rising costs associated with holding a home create increasing pressure on existing homeowners to continue to be able to afford and pay for their mortgages.

— GEOFF SMITH, EXECUTIVE DIRECTOR, INSTITUTE FOR HOUSING STUDIES AT DEPAUL UNIVERSITY (CBS NEWS, 2025)

The result is what housing economists call a "cost-of-holding" crisis — distinct from the "cost-of-buying" crisis that gets more headlines. A family that bought a $300,000 house in 2019 at a 3.5% mortgage rate may have a perfectly manageable mortgage payment of around $1,350 a month. But if their homeowners insurance has risen from $1,200 to $2,370 a year, their property taxes have increased by $2,000 a year, and their utility and maintenance costs have gone up substantially, their total housing cost may have grown by $500 a month or more with no increase in their income to match.

The Insurance Crisis Driving Foreclosures

Of all the rising costs pushing homeowners toward foreclosure, homeowners insurance is perhaps the most dramatic. Across the US, insurance premiums rose by approximately 24% between 2021 and 2024, outpacing general inflation by 11 percentage points, according to industry data. Insurance now accounts for 9% of the typical American homeowner's monthly mortgage payment — the highest share ever recorded.In high-risk states, the situation is far more severe. In Florida and California, homeowners insurance can account for 15% to 20% of a homeowner's total monthly housing payment. In some counties — particularly those exposed to hurricane risk, wildfires, or flooding — standard insurers have pulled out of the market entirely, forcing homeowners onto expensive state-backed plans of last resort.

The reason premiums have risen so sharply is not difficult to understand. In 2023, US insurers paid out $1.11 in claims for every $1.00 they earned in homeowners insurance premiums. Climate-driven losses have surged. The January 2025 Los Angeles wildfires resulted in an estimated $4 billion in losses for California's FAIR Plan. Hurricane Milton caused $3.62 billion in residential losses in Florida. By September 2025, severe convective storms — tornadoes, hailstorms, and high winds across the Midwest and Southeast — had caused $42 billion in insured losses.

Research from the Federal Reserve Bank of Dallas has found that a homeowner is significantly more likely to become delinquent on their mortgage in the months following an increase in their homeowners insurance premium. The connection is direct: when insurance costs rise and the increase is rolled into a monthly mortgage escrow payment, many households — particularly those already stretched thin — find they simply cannot keep up. Premiums are projected to rise another 8% in both 2026 and 2027.

Property Taxes: The Hidden Time Bomb

Homeowners insurance gets most of the headlines, but rising property taxes have been an equally significant driver of the foreclosure increase — and in some markets, a more severe one. When home prices surged during the pandemic, county property assessors across the country were slow to update their valuations. By 2023 and 2024, those reassessments started landing in mailboxes, and the increases were shocking to many homeowners who had assumed their fixed-rate mortgage meant their housing costs were stable.In rapidly appreciating markets, property tax bills doubled or even tripled between 2020 and 2025. A homeowner who bought a modest house in a Texas suburb for $280,000 in 2018 and watched it appreciate to $420,000 by 2022 might have seen their annual property tax bill climb from $5,600 to $8,400 — an extra $233 a month added to their housing costs with no notice and no recourse other than a formal appeal process that most homeowners do not know how to navigate.

Unlike mortgage payments, property taxes cannot be refinanced or restructured. They are a fixed obligation that rises with the assessed value of the property, regardless of whether the homeowner's income has kept pace. For retired homeowners on fixed incomes, for families who bought during the pandemic at the top of the market, and for lower-income homeowners in gentrifying neighbourhoods, escalating property taxes have become the single biggest threat to keeping their homes.

Mortgage Rates and the Affordability Cliff

While most of the homeowners entering foreclosure today have fixed-rate mortgages from earlier years, the broader affordability picture created by elevated interest rates plays an important role in the foreclosure trend — both directly and indirectly.Directly, homeowners who took out adjustable-rate mortgages in 2021 and 2022 — when rates were artificially low — have seen their payments reset to much higher levels as those loans have reached their adjustment periods. FHA loans, which serve first-time buyers and lower-income households with down payments as low as 3.5%, have been particularly hard hit. The FHA loan delinquency rate reached 11.52% in the fourth quarter of 2025 — the highest level since the second quarter of 2021, and 6.5 times higher than the 1.78% conventional loan delinquency rate in the same period.

Indirectly, high mortgage rates have created a "lock-in effect" that has frozen the housing market. Homeowners who secured 3% or below mortgages in 2020 and 2021 are reluctant to sell and give up those rates by taking out a new mortgage at 6% or 7%. This has suppressed housing supply, kept prices high, and reduced the ability of struggling homeowners to sell their way out of trouble before reaching foreclosure. When your house is worth more than you owe but selling it would require you to take on a mortgage at twice your current rate, selling becomes a much less attractive option than it might appear on paper.

Housing economists at foreclosuredatahub.com note that mortgage payments now consume over 30% of median household income — compared with 21% before the pandemic. To restore pre-pandemic affordability, one of three things would need to happen: mortgage rates would need to fall to around 2.65%, median household income would need to rise 56%, or home prices would need to drop 35%. None of these outcomes is considered likely in the near term. Major housing expenses exceeded historic affordability norms in 96.6% of US counties analysed in the first quarter of 2026.

Who Is Being Hit the Hardest

The foreclosure wave is not hitting all Americans equally. The pain is concentrated in specific groups who face the combination of high housing costs with limited financial resilience.First-time buyers who purchased during 2021 and 2022 — at or near peak prices, with thin down payments and limited equity cushions — are disproportionately represented in foreclosure filings. Many of these buyers used FHA or VA loans with down payments of 3% to 5%. When home prices in some markets have softened slightly and insurance and tax bills have risen sharply, these households have very little financial buffer.

Lower-income and minority homeowners face compounded risks. Research from Americans for Financial Reform shows that 7% of homeowners lack homeowners insurance entirely — a proportion that is higher among lower-income households and households of colour. When an uninsured homeowner faces a significant repair need — a roof damaged by a hailstorm, a basement flooded — the choice between making the repair and making the mortgage payment becomes stark. Research also shows that insurance premium increases falling on the 20% of ZIP codes with the highest climate risk outpaced overall inflation by nearly 15 percentage points between 2018 and 2022.

Older homeowners on fixed incomes represent a third group at serious risk. Many bought their homes decades ago and have substantial equity, but their monthly income from Social Security or pension is no longer sufficient to cover rising insurance premiums, property taxes, maintenance costs, and healthcare expenses simultaneously. For these homeowners, the threat of foreclosure often goes unnoticed until it is nearly too late.

Which States Have the Highest Foreclosure Rates

Foreclosure activity is not evenly distributed across the country. ATTOM data for the first quarter of 2026 shows that Indiana, South Carolina, Florida, Delaware, and Illinois reported the highest foreclosure rates relative to their housing stock. Indiana led the nation at approximately one in every 739 housing units receiving a foreclosure filing.Florida and Texas stand out for different reasons. Florida faces a severe insurance crisis driven by hurricane risk, with many homeowners unable to find or afford coverage from standard carriers. Texas leads the country in raw foreclosure volume — with 3,390 foreclosure starts in February 2026 alone — driven by a combination of insurance cost spikes, rising property taxes, and economic pressures in certain regional markets. States like California, with its high baseline housing costs, and Illinois, with its historically high property taxes, also appear consistently among the highest-risk markets.

Markets with a higher proportion of FHA loans — typically areas where first-time and lower-income buyers are concentrated — are seeing the steepest increases in delinquencies and defaults. The geographic pattern reflects the structural concentration of the crisis: it is worst where affordability was already stretched the thinnest, insurance costs are rising the fastest, and borrowers have the least financial cushion to absorb shocks.

Is This 2008 All Over Again?

The honest answer is: not even close — but that does not mean there is nothing to worry about. The 2008 foreclosure crisis was the result of systemic failures in mortgage lending, with millions of loans made to borrowers who could never have afforded them, bundled into financial products that obscured their true risk, and guaranteed by institutions that did not understand what they were holding. When those loans started defaulting at scale, the entire financial system was threatened.Today's situation is structurally different. The vast majority of current mortgages were underwritten to post-2008 standards. American homeowners hold roughly $32 trillion in home equity — a record high. Mortgage delinquencies overall remain near historical lows, even as foreclosure filings rise, because many homeowners who fall behind are able to work out payment plans with their lenders or sell their homes before reaching the auction stage.

What today's foreclosure increase represents is better described as market normalisation — a return to the levels of distress that existed before pandemic-era forbearance programmes and emergency protections artificially suppressed foreclosure activity. It is also a structural warning about the sustainability of homeownership costs. The households entering foreclosure today are not victims of fraudulent loans. They are victims of an affordability environment that has made it increasingly difficult for ordinary Americans to hold onto homes they own, in communities they have lived in for years or decades, because the annual cost of insuring, taxing, and maintaining that home has grown faster than their income.

What Homeowners Can Do Right Now

If you are a homeowner worried about rising costs or concerned that you might fall behind on your mortgage, there are concrete steps you can take before the situation becomes a crisis.Practical steps for homeowners facing cost pressures

- Contact your mortgage servicer early: If you think you might fall behind, call your lender before you miss a payment. Lenders have forbearance and loan modification programmes available, but they are much easier to access before you default.

- Appeal your property tax assessment: Most homeowners do not realise that property tax assessments can be appealed. If your assessed value seems too high, contact your county assessor's office to find out the appeals process and deadline.

- Shop for homeowners insurance every year: Premiums vary widely between insurers. Shopping annually and comparing quotes can save hundreds of dollars, and switching carriers is straightforward. Bundling home and auto insurance can save an additional 5% to 25%.

- Contact a HUD-approved housing counsellor: HUD-approved counsellors offer free or low-cost advice on mortgage delinquency, foreclosure prevention, and loss mitigation options. You can find one by visiting hud.gov or calling 1-800-569-4287.

- Explore loss mitigation options before foreclosure starts: Loan modifications, repayment plans, short sales, and deeds in lieu of foreclosure are all options that can help you avoid or minimise the credit damage of a full foreclosure. A housing counsellor or attorney can help you understand which option fits your situation.

- Know the 120-day rule: Under federal law, your lender cannot officially start the foreclosure process until you are more than 120 days delinquent. Use that window to get advice and explore your options.

CONCLUSION

The surge in US foreclosures to a six-year high is not driven by irresponsible borrowing or a repeat of the 2008 subprime crisis. It is driven by the steadily rising cost of simply owning a home — insurance that has gone up 70%, property taxes that have doubled in many markets, utilities, maintenance costs, and mortgage rates that are nearly three times what they were at the pandemic low. For millions of American families, these rising costs have quietly outpaced their incomes, and the financial margin between stability and foreclosure has shrunk to almost nothing.This is not yet a systemic crisis, and most American homeowners have enough equity and institutional protection to avoid foreclosure if they act early and seek help. But the trend is real, the numbers are rising, and the structural pressures behind them are unlikely to resolve quickly. Homeowners who understand what is driving this crisis — and what options they have — are in a far better position than those who simply wait and hope for the best.

Frequently Asked Questions

Why are foreclosures rising if home prices are still high?

Because the problem is not the mortgage payment — it is the total cost of owning a home. High home prices have pushed up property taxes and insurance costs sharply. Homeowners who bought years ago at low mortgage rates may have manageable monthly mortgage payments but are being squeezed by insurance premiums up 70% in five years, higher property taxes, and rising utilities and maintenance costs. It is the total bill, not just the mortgage, that is pushing families into foreclosure.How many foreclosure filings are there each month right now?

In January 2026, ATTOM recorded over 40,500 foreclosure filings nationwide — a 32% year-over-year increase. February 2026 saw 38,840 filings, with foreclosure starts up 26% and completed foreclosures up roughly 59% on a year-over-year basis. This represents the 12th consecutive month of year-over-year increases in foreclosure activity.Is this a repeat of the 2008 housing crisis?

No. The 2008 crisis was caused by systemic mortgage fraud, millions of subprime loans, and the collapse of mortgage-backed securities. Today's foreclosure increase reflects a return to more normal levels of housing distress after pandemic-era protections expired, combined with the structural impact of rising housing costs. American homeowners currently hold record levels of home equity, and overall mortgage delinquencies remain near historical lows. At today's foreclosure rate, activity would need to increase 8.6 times to match the 2010 peak.Which states have the highest foreclosure rates in 2026?

According to ATTOM data for Q1 2026, Indiana, South Carolina, Florida, Delaware, and Illinois have the highest foreclosure rates relative to their housing stock. Indiana leads the nation at approximately one in every 739 housing units with a foreclosure filing. Texas leads in raw volume, with 3,390 foreclosure starts in February 2026 alone.What can I do if I am struggling to make my mortgage payments?

The most important thing is to act before you miss a payment. Call your mortgage servicer to discuss forbearance or loan modification options. Contact a free HUD-approved housing counsellor at hud.gov or 1-800-569-4287 for independent advice. Under federal law, your lender cannot begin the official foreclosure process until you are more than 120 days delinquent — use that window to explore your options. Do not ignore the problem or wait for it to go away on its own.How much has homeowners insurance gone up in recent years?

According to ICE Mortgage Technology data, single-family homeowners with a mortgage pay an average of $2,370 per year for homeowners insurance — up nearly 70% from five years ago. A broader industry analysis found that premiums rose approximately 24% between 2021 and 2024, outpacing general consumer price inflation by 11 percentage points. Premiums are projected to rise a further 8% in both 2026 and 2027. In high-risk states like Florida and California, insurance can account for 15% to 20% of a homeowner's total monthly housing payment.What is the FHA delinquency rate and why does it matter?

The FHA delinquency rate measures the proportion of FHA-insured mortgage loans where borrowers are behind on payments. In the fourth quarter of 2025, the FHA delinquency rate reached 11.52% — the highest level since 2021, and 6.5 times higher than the 1.78% delinquency rate on conventional loans. FHA loans serve first-time buyers and lower-income borrowers with small down payments, so a high FHA delinquency rate indicates that the housing affordability crisis is falling hardest on the people least financially equipped to handle it.References

CBS News — Foreclosures Are Surging as US Homeowners Grapple With Rising Costs https://www.cbsnews.com/news/housing-market-foreclosure-increasing-attom-august-2025/ATTOM / Lamun Mock Cunnyngham — Rising Foreclosure Rates in 2026 https://www.lamunmock.com/news/rising-foreclosure-rates-in-2026

ForeclosureDataHub — Is the Housing Market Going to Crash in 2026? https://www.foreclosuredatahub.com/blog/housing-market-crash-2026-foreclosure-data-analysis

Nolo — Rising US Foreclosure Rates in 2025: Causes, Trends, and Homeowner Protections https://www.nolo.com/legal-encyclopedia/are-foreclosures-on-the-rise.html

Nolo — Rising US Foreclosure Rates in 2026: What Homeowners and Buyers Should Know https://www.nolo.com/legal-encyclopedia/foreclosure-rates-2023.html

HomeBuyingInstitute — Why Home Insurance Premiums in the US Are Still Rising in 2026 https://homebuyinginstitute.com/mortgage/why-home-insurance-premiums-are-rising/

0 Comments Comments