Making Money

How to Become a Millionaire in 12 Months

Table of Contents

- Introduction

- The Honest Truth About Becoming a Millionaire Quickly

- The Millionaire Mindset: The Internal Foundation

- Income vs Wage Thinking

- Asset Accumulation vs Consumption

- Obsession With Value Creation

- The 12-Month Wealth Blueprint: Phase by Phase

- Phase 1 (Months 1-2): The Financial Foundation Audit

- Phase 2 (Months 3-4): Income Acceleration

- Phase 3 (Months 5-7): Diversification and Digital Assets

- High-Impact Income Streams to Consider

- Phase 4 (Months 8-10): Leverage, Automation, and Scale

- The Three Forms of Leverage

- Phase 5 (Months 11-12): The Final Push to $1 Million

- Critical Mistakes That Derail Rapid Wealth Creation

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Introduction

Let us be clear from the outset: becoming a millionaire in twelve months is not guaranteed, and it is not easy. Anyone who tells you otherwise is selling something. But is it possible? For a specific type of person — one who combines the right skills, the right strategy, relentless execution, and an honest starting assessment of their own situation — the answer is yes. History and current data both confirm it.The Federal Reserve's Survey of Consumer Finances reports that the United States now has more millionaires than at any point in history, and the pace of new millionaire creation has accelerated dramatically since 2020. The pandemic era revealed a truth about wealth creation that traditional financial advice had long obscured: income velocity matters more than saving rates, and the internet has unlocked income-generation opportunities that simply did not exist a generation ago. Businesses that took decades to build in the 1980s can now reach global scale in months.

This guide does not offer lottery tickets, cryptocurrency speculation, or overnight success fables. Instead, it provides a structured, honest, and strategically rigorous blueprint for those who want to understand what rapid wealth creation actually requires, what realistic paths exist, how to sequence your actions across twelve months, and what mindset and behavioral changes separate those who achieve this goal from those who merely aspire to it. Whether you reach $1 million in exactly twelve months or whether this plan sets you on a trajectory to get there in eighteen or twenty-four, the principles here will fundamentally reshape your financial future.

The Honest Truth About Becoming a Millionaire Quickly

Before mapping the path, it is essential to dismantle two damaging myths that sit at opposite extremes of the conversation about rapid wealth.The first myth is that becoming a millionaire quickly is impossible for ordinary people. This is demonstrably false. Self-made millionaires — those who built their wealth from modest beginnings rather than inheriting it — now constitute approximately 80% of all millionaires in the United States, according to research by Dave Ramsey's organisation. Many of them did not start with exceptional privilege, extraordinary intelligence, or unique talent. They started with a clear strategy and the discipline to execute it.

The second myth — equally dangerous — is that becoming a millionaire in a year requires a single lucky break, a viral moment, or a speculative bet. This path exists, but it is not a strategy; it is a lottery. The people who consistently build significant wealth in compressed timeframes do so through specific, repeatable actions: they identify or create high-value products or services, they generate multiple streams of income simultaneously, they control expenses ruthlessly while scaling revenue aggressively, and they reinvest returns into assets that compound.

The honest prerequisite is this: reaching $1 million in net worth within twelve months from a standing start requires either a significant existing income base to leverage, a business or skill set with high earning potential, an existing asset that can be scaled, or a combination of the above. The lower your starting point, the more aggressive your income growth must be. This is not discouraging — it is clarifying. Knowing your honest starting position is the foundation of an honest plan.

The Millionaire Mindset: The Internal Foundation

Every financial result begins with a mental model. The mindset of someone who builds wealth rapidly is categorically different from the mindset of someone who earns well but never accumulates. Understanding these differences is not a motivational exercise — it is strategic preparation.Income vs Wage Thinking

Wage thinkers exchange time for money at a fixed rate. Income thinkers ask how to decouple money from time. A consultant who bills $200 per hour is doing better than an employee on $100,000 per year — but a consultant who builds a course, book, or system that delivers the same value to 1,000 clients simultaneously has crossed into a fundamentally different wealth trajectory. The shift from asking 'How much can I earn per hour?' to 'How can I earn while I sleep?' is the single most important mindset transition in wealth creation.Asset Accumulation vs Consumption

A defining characteristic of rapid wealth builders is the deliberate suppression of lifestyle inflation during the acceleration phase. Income grows; lifestyle does not, or grows only modestly. Every dollar not spent on depreciating goods or lifestyle upgrades is a dollar available for investment in assets that generate future returns. Robert Kiyosaki's distinction between assets (things that put money in your pocket) and liabilities (things that take money out) is simple but profound in its application.Obsession With Value Creation

The fastest path to a million dollars is to solve a significant problem for a meaningful number of people at a meaningful price. The question 'What value can I create for whom, and how much are they willing to pay for it?' is more powerful than any investment formula. Every millionaire made in a short timeframe — whether through business, consulting, real estate, content creation, or digital products — did so by finding the answer to that question and executing on it relentlessly.The 12-Month Wealth Blueprint: Phase by Phase

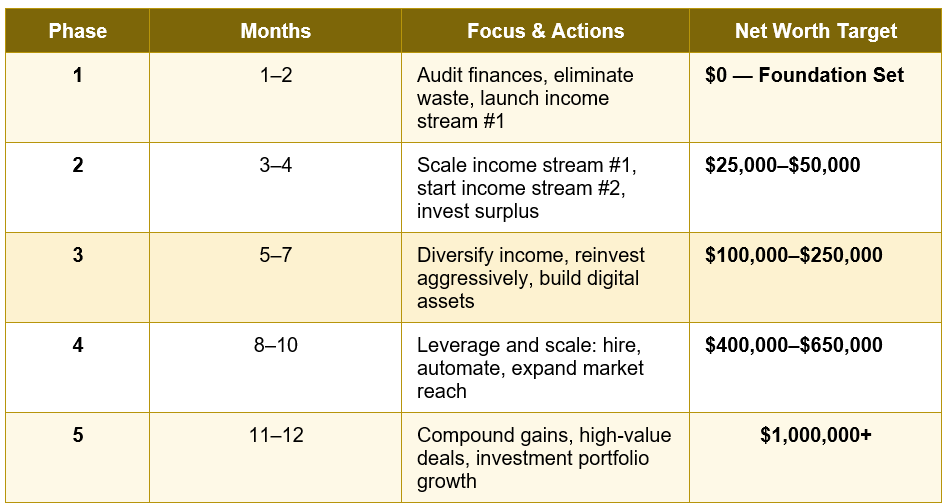

The following table maps the five phases of a structured twelve-month wealth acceleration plan, from financial foundation to millionaire milestone:

Phase 1 (Months 1-2): The Financial Foundation Audit

No wealth strategy works on a leaking foundation. The first two months are about brutal honesty and decisive action — not income generation, but income preparation.- Complete a full financial audit: List every income source, every fixed expense, every debt, and every asset. Calculate your current monthly surplus — the number your entire wealth strategy depends on. Most people discover significant waste in subscriptions, unused services, and unnecessary expenses that can be immediately redirected.

- Eliminate all high-interest debt: Credit card debt at 20%+ APR is a guaranteed negative return on capital. Paying it off first is the equivalent of a guaranteed 20% investment. Use the avalanche method (highest interest first) to eliminate consumer debt as the first priority of month one.

- Build a minimal emergency fund: Three months of essential expenses in a high-yield savings account prevents a single unexpected event from derailing your entire twelve-month plan. This is not wealth building — it is risk management.

- Identify and launch income stream number one: Your first additional income stream should leverage an existing skill or knowledge base. Consulting, freelancing, coaching, or professional services in your area of expertise are the fastest routes to meaningful additional income because they require no product development, no stock, and no infrastructure. A single high-value client can generate $5,000 to $50,000 in the first month alone.

Phase 2 (Months 3-4): Income Acceleration

With foundations in place, months three and four shift focus entirely to revenue growth. Every dollar of surplus income generated in this phase is immediately deployed — never left idle.Scale your primary income stream by raising prices, increasing client volume, or extending your offering. Many service providers significantly underprice their expertise early in the process. Raising prices by 30% to 50% is often more impactful than doubling your client base, and it simultaneously attracts higher-quality clients.

Introduce a second income stream that is complementary to the first but operates on a different model. If income stream one is active (consulting, freelancing), income stream two should trend toward semi-passive (digital products, online courses, licensing). The target is to begin converting time invested into recurring or scalable revenue.

The income milestones for this phase range from $25,000 to $50,000 in accumulated net worth, depending on your starting point and the income velocity you have built. Anyone generating $15,000 to $25,000 per month in total income and holding expenses at their baseline level will reach this range comfortably within the phase.

Phase 3 (Months 5-7): Diversification and Digital Assets

By month five, you should have proven income from at least two streams. Phase three is about diversification — building income channels that are less dependent on your direct time and attention, and beginning to invest surplus capital into assets.High-Impact Income Streams to Consider

- Digital products: Online courses, templates, e-books, software tools, and membership communities can scale to thousands of buyers without proportional increases in effort. A $197 course purchased by 5,000 students generates nearly $1 million in revenue.

- Affiliate marketing and referral partnerships: Recommending products or services you already use and trust, earning commission on resulting sales, creates income with zero product cost or support overhead.

- Content monetisation: YouTube, podcasting, newsletter publishing, and social media content creation build audiences that generate advertising revenue, sponsorship income, and product sales. The lead time is longer than direct services but the income ceiling is significantly higher.

- Real estate income: Short-term rental arbitrage — leasing a property and subletting it on Airbnb with the landlord's permission — is a proven model for generating real estate income without owning property. Alternatively, REITs allow investment in real estate from as little as $10 with immediate dividend income.

- Stock market investments: Surplus income above living expenses should be consistently invested in a diversified portfolio of low-cost index funds. At this stage, total return matters less than the habit of investing every month without exception.

Phase 4 (Months 8-10): Leverage, Automation, and Scale

Phase four is where significant wealth separation occurs between those who continue trading time for money and those who learn to leverage. Leverage in wealth creation means using other people's time, systems, money, or platforms to multiply your output beyond what your individual effort could achieve.The Three Forms of Leverage

- People leverage: Hiring virtual assistants, contractors, or employees to handle tasks that consume your time but can be systematised and delegated. Paying someone $20 per hour to handle administrative work while you focus on activities that generate $500 per hour is not an expense — it is a multiplier.

- Systems leverage: Building workflows, automations, and processes that deliver results without your direct involvement. Email marketing automations, sales funnels, chatbots, and standard operating procedures (SOPs) allow a business to generate income continuously, around the clock, across time zones.

- Financial leverage: Using borrowed capital to acquire income-generating assets that generate returns exceeding the cost of borrowing. Used responsibly — with adequate cash flow cover and realistic exit scenarios — financial leverage is one of the primary mechanisms through which significant wealth is built in compressed timeframes.

At the end of Phase 4, your net worth target range is $400,000 to $650,000. This requires consistent monthly income at six figures, aggressive reinvestment, and the compounding effect of multiple income streams running simultaneously. If your trajectory is on track, Phase 5 is not a dramatic leap — it is the natural conclusion of everything built across the preceding ten months.

Phase 5 (Months 11-12): The Final Push to $1 Million

The final phase of the twelve-month plan is about consolidation, high-value transactions, and compounding the gains you have already built. By this stage, your business systems should be generating income with reduced direct involvement, your investment portfolio should be growing, and your network should be delivering opportunities that were unavailable to you twelve months earlier.Month eleven and twelve are the time for high-value deals: selling a business, closing a significant contract, launching a premium-priced product to an established audience, or completing a real estate transaction. These are not Hail Mary moves — they are the natural harvest of the infrastructure, audience, reputation, and relationships you have built over the preceding ten months. The deals available to someone with a proven business, a strong network, and a track record are categorically different from those available to someone starting from zero.

Aggressive portfolio investment of remaining surplus capital in this phase, combined with the compounding of all previously invested assets, pushes total net worth across the $1 million threshold for those who have executed the preceding phases with discipline and consistency.

Critical Mistakes That Derail Rapid Wealth Creation

Understanding what not to do is as important as knowing what to do. The following are the most common wealth-destruction patterns among people who start ambitiously but fail to reach their goals:- Lifestyle inflation: Increasing spending proportionally with income is the single most common reason people with high incomes never build wealth. Keep your lifestyle at baseline until the $1 million milestone is reached.

- Speculative shortcuts: Cryptocurrency gambling, penny stock trading, and multi-level marketing are not wealth strategies — they are wealth destruction vehicles for the majority of participants. Legitimate rapid wealth is built on value creation and income, not speculation.

- Lack of focus: Chasing every opportunity without executing deeply on any of them is the entrepreneurial equivalent of digging ten shallow wells and finding no water. Execute one or two income streams to significant scale before adding more.

- Underpricing your value: Chronic underpricing is one of the most expensive habits a professional or entrepreneur can have. Pricing courage — the willingness to charge what your expertise and outcomes are genuinely worth — is a direct multiplier of income velocity.

- Isolation: The people around you dramatically affect your trajectory. Surrounding yourself with other ambitious, strategically minded wealth builders accelerates your progress through shared knowledge, accountability, and deal flow. Join masterminds, attend industry events, and invest in networks intentionally.

Conclusion

Becoming a millionaire in twelve months is not a fantasy — but it is a commitment. It requires an honest assessment of your starting point, an aggressive but structured approach to income generation, the discipline to suppress consumption while scaling production, and the strategic intelligence to leverage every gain into the next level of growth. None of these requirements are beyond the reach of a determined, adaptable person with a marketable skill or a scalable business idea.The blueprint outlined in this guide — five phases moving from financial foundation to income acceleration, diversification, leverage, and compounding — is not theoretical. It reflects the actual trajectory of thousands of self-made millionaires who built their wealth through business, digital income, real estate, and investment rather than through inheritance or luck.

Begin now, not when conditions are perfect. The greatest enemy of wealth creation is not lack of opportunity — it is delayed action while waiting for circumstances to align. Map your current position, identify your highest-value income opportunity, take the first step in the next twenty-four hours, and let the compounding logic of this plan do the work. Twelve months from today, your financial reality can be unrecognisable from where it stands right now.

Frequently Asked Questions (FAQ)

Is it realistic to become a millionaire in exactly 12 months?

It is realistic for a specific profile of person: someone with a high-value skill or established business, a high tolerance for risk and discomfort, significant available time to dedicate to income generation, and the discipline to reinvest aggressively rather than spend. For those starting from very low income or significant debt, twelve months is an ambitious timeline but the same strategy applied over twenty-four to thirty-six months is highly achievable. The plan is equally valid at either pace — the timeline adjusts to your starting point.What is the fastest legitimate way to make $1 million?

The fastest legitimate routes to $1 million include: building and selling a high-growth business (the most common path for self-made millionaires under 40), scaling a high-ticket service business (consulting, coaching, agency work) to six-figure monthly revenue, creating and selling digital products to a large audience, investing in and scaling real estate through leverage, and building a personal brand with multiple monetisation streams. The common thread is value creation at scale, not a single lucky transaction.Do I need significant starting capital to build wealth quickly?

No — and this is one of the most important things to understand. The fastest income generators in the modern economy — consulting, coaching, freelancing, digital products, and content creation — require minimal starting capital. A laptop, an internet connection, and a marketable skill are sufficient to begin generating $10,000 to $50,000 per month for those who execute with intensity. Capital becomes a powerful accelerator once initial income is established, but it is not a prerequisite for beginning.How many income streams should I have?

The quality and scalability of your income streams matter more than the quantity. Most people who achieve rapid wealth start with one high-income stream executed extremely well, add a second that is complementary and more passive, and build from there. Trying to manage five or six income streams simultaneously from the beginning results in all of them being mediocre. The goal is depth first, then breadth as systems and team members allow each stream to run without constant direct involvement.What role does investing play in a 12-month millionaire plan?

Investing plays a critical compounding role, but it is a supporting character rather than the hero of a twelve-month plan. Market investments typically return 7-10% annually — excellent for long-term wealth preservation and growth, but insufficient as the primary engine of rapid wealth creation. In a twelve-month plan, investing is where surplus income is parked and grown, while the primary wealth engine is active income from high-value business activity. As income scales and surplus capital accumulates, investment returns become an increasingly significant component of total wealth growth.External References

The following authoritative sources informed this guide and are recommended for further reading:1. Federal Reserve — Survey of Consumer Finances (Wealth Data)

https://www.federalreserve.gov/econres/scfindex.htm

2. Ramsey Solutions — The National Study of Millionaires

https://www.ramseysolutions.com/retirement/the-national-study-of-millionaires-research

3. Investopedia — How to Become a Millionaire

https://www.investopedia.com/articles/personal-finance/092314/how-become-millionaire.asp

4. Forbes — Wealth Creation and Entrepreneurship Insights

https://www.forbes.com/wealth/

5. MoneySavingExpert (UK) — Building Wealth from Scratch

https://www.moneysavingexpert.com/savings/

6. BiggerPockets — Real Estate Wealth Building Strategies

https://www.biggerpockets.com/

7. Harvard Business Review — Entrepreneurship and Wealth Creation

https://hbr.org/topic/subject/entrepreneurship

8. The Balance — Multiple Income Streams Guide

https://www.thebalancemoney.com/multiple-streams-of-income-4064592

0 Comments Comments